Justin Paget

Overview:

Valero Energy (NYSE:VLO) is primarily involved in the marketing and manufacturing of transportation fuels. The company is benefiting from falling crude prices, improving GDP and consumer spending, which in turn has led to record margins. Valero over the years has continued to invest in its refineries, improving its throughput and thereby ensuring that it continues to increase cash flow. Furthermore, it is significantly improving the output of its renewable diesel operations. Renewable diesel operations have continued to improve and when combined with demand from Europe, led to record levels of cash flow for the latest fiscal year.

Outperformance To Continue

The current environment is perfectly set up for Valero Energy to continue outperforming in the coming years. The stock is up 50% in a year where the broader market has struggled, as improving cash flow from the sale of both refined products and renewable products has driven revenue for the year. Valero energy’s outperformance can be attributed to both local demands, with the latest GDP figures improving by 3%, and consumer spending increasing by 2%. Consumers have seen their savings post-pandemic slowly deteriorate, due to inflation, and purchases that were put off finally come around. In addition, the war in Ukraine has meant that significant demand is now coming out of Europe for Valero’s products. Meanwhile, oil prices which were previously over $100 a barrel are now trading around $80 per barrel, which has allowed significant easing for consumers who were under pressure from the broader inflationary environment. Furthermore, the company is now pursuing multiple export opportunities, along with improving its overall portfolio by entering the Venezuelan market.

Oil prices are expected to remain range bound, with increasing interest rates, and a stronger dollar, oil-producing countries are increasingly hesitant to increase supply as they look to keep prices elevated, meanwhile shale producers can’t increase supply quickly either due to supply chain issues. And now the number of countries such as China opening up demand for crude should increase, and could send oil prices back to $100 a barrel if not higher. Therefore, in an environment where interest rates are at multi-decade highs and demand could slow Valero faces numerous risks, which could slow demand in the coming year. On the other positive factors stemming mainly from improving throughput, should allow for increasing dividends, even if demand slows down.

Valero Presentation 2022

Over the longer period, Valero’s investments in its renewable diesel operations, where it is looking to increase capacity and thereby increase its EBITDA to $1.7 billion by 2025, offer significant scope, due to the highly competitive nature of renewable diesel. Renewable diesel offers anywhere from 40-60% lower GHG emissions, and the state of California is increasingly looking to offer financial incentives to renewable diesel producers. With consumption doubling from 2020-2021, and high double-digit increases in 2022, could help achieve that target. Renewable diesel capacity is set to significantly increase over the next couple of years and will become an increasingly larger mix of fuel usage significant investment in renewables diesel combined with LCFS credit is the primary driver of revenue and should help continue to push margins upwards from their current levels of around 8% gross, and 5% net profit margins.

Valero’s margins have been improving, which has allowed the company to pay down its debt, and the lower levels of debt should help the company improve cash flow further. Debt is down by almost $4 billion over the recent past and now hovers around $9 billion. When combined with improving throughput, an increasing mix of renewable diesel has allowed the company to increase its margins, and margins have hit all-time highs in the recent past. Margins are now around 5-6%, although gross margins did decline in the recent past.

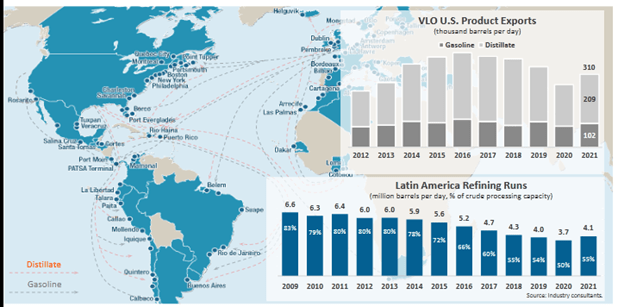

Valero’s lower levels of debt, and improving cash flow should allow the company to increase its dividend, which currently is relatively high, and one of the highest in the S&P 500. Cash flow significantly increased during the fiscal year 22’ and now stands at close $7 billion a significant increase from the previous years, where the company was having cash flow issues. This could send the dividend to around 4%. Free cash flow in the current fiscal year, will not grow as quickly as tailwinds in the previous fiscal year subside, expected around 10-15% growth for the year. But Valero is also increasingly pushing to improve its revenue through a number of avenues, including the push for Venezuelan crude and the push to bring in more credit-based revenue, mainly due to the back of its operations in California. Finally, some of the distillate supply that has been coming down should steady out into next year, with VLO exports continuing to improve.

A Quick Look At 2023

While analysts estimate that revenue could in come in lower than 2023, this is unlikely, and recessionary signals continue to affect the outlook. But considering that GDP and consumption have remained intact, and a significant amount of demand is coming from the replacement of traditional fuels with renewable fuels, which currently have lower GHG than EVs. This should help push Valero’s renewable diesel not only in the U.S. market but also in the European market as well. This would mean that revenue which was around $170 billion for the fiscal year should grow by around 5-7% for the year. The increase in free cash flow, improving EBITDA, and better market prospects stemming from renewables, should help the stock continue its upward trajectory into next year, despite the broader market being under pressure. This bodes well for investors who are concerned with the increasingly volatile stock market and are looking to put their money somewhere where it’s safe.

Valero Presentation

But, risks remain with oil prices having likely bottomed out, and despite lower levels of liquidity, demand and supply differences are likely to push up prices again next year. While the labor markets remain relatively steady for now, high-interest rates could see unemployment rise slightly, which could pull back demand. Finally, demand out of Europe is also circumspect, with increasing economic pressure, pushing European countries to renegotiate with Russia. All these factors could in turn affect total demand, which is holding up for now.

Be the first to comment