Kerkez/iStock via Getty Images

Co-produced with Treading Softly

When it comes to real estate, many of us love to achieve the classic “American Dream.” You know, the house with the white picket fence. Owning a piece of soil and knowing it’s yours. For many, this dream is seemingly unachievable. With the rapid craze in property values rising and now rapidly rising interest rates bringing the costs of home ownership to all-time highs, this dream is fading for some.

For others, the bank really owns their home through a lien or loan tied to it. Your mortgage means the bank owns an important piece until the day it’s entirely paid off. It doesn’t mean they will pitch in and help with your repairs of taxes though. Fully paying off your mortgage and owning your home “free and clear” is an exciting moment that few will ever know.

Even fewer of us will achieve the mark of being a landlord – either commercial or residential. If you struggle to own one home, how will you afford two, three, or more? Commercial property comes with its own unique hurdles to own or operate. Not to mention the headaches, lawyers, and mountains of paperwork involved.

Ever try to buy a hospital? I personally try to avoid going to them, let alone try to afford to own one!

I want the benefits of being a landlord. I love being paid rent, and collecting an income in exchange for my capital being invested in real estate. An asset that tends to appreciate faster than inflation, that produces income and has all sorts of tax advantages. I don’t want the drawbacks of tying up large amounts of capital, having an illiquid asset, dealing with problem tenants, or needing a team of lawyers.

So instead of attempting to become a landlord directly, I band together with thousands of others. Others who, like me, are deciding that direct ownership and becoming a landlord are not worth the work or effort required. How do we do this? With REITs.

I buy REITs which in turn buy properties and are overseen by expert management teams. They find opportunities, find tenants, and collect rent. They deal with the paperwork, lawyers, and headaches. I collect the return on my capital through dividends. If I choose to sell one type of property and invest in another, I can do so from my cell phone with just a few clicks. Through these channels, I can own hospitals and commercial real estate all over the United States and the globe.

Let’s dive in.

Pick #1: MPW – Yield 7.4%

Medical Properties Trust, Inc. (MPW) is a REIT with a unique niche and a very straightforward business model. They buy hospitals and lease them, and collect rent. While they might occasionally sell a property for a profit, the bulk of their profits comes from simply holding the properties and collecting rent. They are a landlord of hospitals and most of those hospitals are bought through a “sale-leaseback” which means that the company leasing the property is the same company that sold it.

The “sale-leaseback” has a long history in commercial real estate. Businesses have a lot of capital tied up in their real estate. While the real estate is essential to the operation of the business (what use is a hospital company without a hospital building!), the investment in the real estate means that capital can’t be used for other things. As a result, the business might have millions or even billions of capital tied up in the real estate, a relatively inefficient place to have capital if you aren’t in the real estate business.

Over the years, it has become quite common for companies in various sectors to construct their buildings, and then do a sale-leaseback. The only way a company can benefit from owning a property is by selling it. So they sell to an investor, ensure the continued right to use the property through a long-term lease, and then redeploy the proceeds from the sale into their core business to generate more profits. The company gets a large lump-sum, in exchange for a modest lease payment.

MPW provides the capital to buy the property and receives rent. With leases extending an average of 17.8 years, MPW is receiving income for a very long time. Plus, it has the option to sell the property whenever it wants, like it recently sold a 50% interest in 8 Massachusetts hospitals for a substantial gain.

Over the past few months, MPW has seen its share price decline. This has occurred despite MPW continuing to see healthy growth with AFFO/share (Adjusted Funds From Operations) up 9% year over year. At $0.37/share, AFFO easily covered the newly raised $0.29 dividend in Q1. MPW is also in the process of deleveraging and is very close to hitting the targets that Moody’s laid out for a credit rating increase.

In short, MPW is making more money, will make even more money over the next year, and is improving its risk profile. Objectively, MPW is a stronger and lower-risk company today than it was last year. Yet the share price is down 34% YTD. When investors see this, they often panic, wondering what they “missed”. They sell first and ask questions later if they bother asking at all.

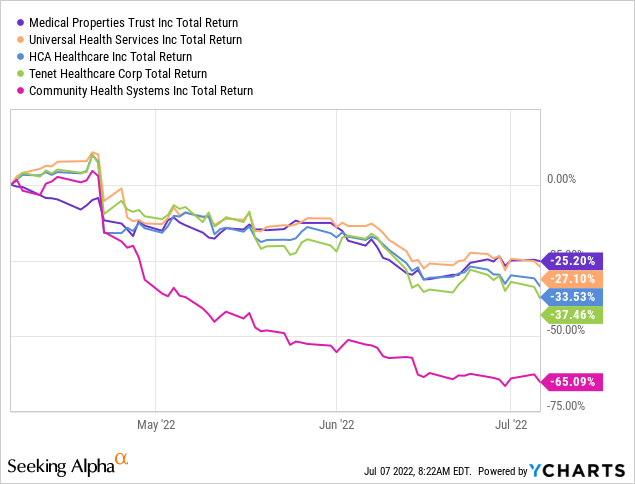

It likely isn’t a coincidence that MPW’s share price has fallen along with the share prices of its tenants. Here is a look at MPW in relation to publicly traded hospitals over the past 3 months:

Hospitals have taken it on the chin, and several of these are MPW tenants. It doesn’t help that the market itself is bearish on the macro-level, but hospitals are experiencing their own specific challenges. Q1 was considered very disappointing by investors as guidance and outlooks for 2022 were reduced, but remember, MPW is a landlord. How much profit a hospital makes is irrelevant to MPW, all that matters is that the hospital pays the rent.

Doing a review of earnings, is there anything in these companies that makes us believe they are bankruptcy risks? No. Reviewing the earnings calls, common themes are:

- COVID cases were high in Q1 in a lot of areas.

- Labor costs are rising, squeezing margins.

- Hospitals can’t just hike costs overnight.

- Prices are negotiated with insurers and the Government. So there is a gap between when expenses go up, and when hospitals can pass that increase along to the customers. As contracts are renegotiated, hospitals will start receiving higher revenues, and that process will take time.

For hospital investors, the coming year isn’t going to be particularly profitable. Earnings will be lower as hospitals operate on tighter margins until price hikes can be passed along to customers and labor costs stabilize.

Is this something that is going to cause MPW’s tenants to go bankrupt and be unable to pay rent? No.

We’re happy to pick up more shares of MPW while it is incredibly cheap

Pick #2: AWP – Yield 9.6%

As the entire market sold off, REITs have not been immune. Aberdeen Global Premier Properties Fund (AWP) is a great way to take advantage of this large-scale sell-off. (Incidentally, on June 30th, there was a minor name change for AWP to abrdn Global Premier Properties Fund).

REITs have an interesting relationship with interest rates. REITs tend to borrow a lot of money. After all, real estate is a business that lends itself to significant borrowing. Lenders love real estate as collateral because unlike a lot of collateral, real estate is notoriously hard to move and hide. It also tends to retain value. Look at your house, consider the mortgage you were able to get on it. Would anyone lend you that sum of money at such a low-interest rate for anything else?

With most companies, leverage at 4x-6x EBITDA would be considered a big risk. For REITs, it is a standard range, with many actually being higher than that.

When interest rates rise, a lot of investors will sell REITs for this reason, as higher rates mean higher interest. Since interest is the largest expense REITs have, a lot of investors assume it is bad.

In isolation, higher interest rates are negative. Lower expenses are always better. Yet the world doesn’t work with variables in isolation. Say your gasoline expense goes to zero, wouldn’t that be grand?

Well, say it was due to your car breaking down and now you can’t drive anywhere. You probably aren’t thrilled with the “savings.”

Say you get a new car and a new job that requires you to drive a bit further. Your daily gas expense goes up, but you don’t care because your new salary is a lot higher. So would you say that your higher gas expense is “bad”? Of course not. It’s a headwind that you have to factor into your decision to accept the new job. You would do the math, and determine if the new job offers enough to compensate for the gas expense and commute time. Most of you have probably done that calculation a time or two in your lives.

In life, there are many different variables that are all interacting at the same time. That which in isolation might be viewed as “bad”, can actually be positive when you consider the other impacts. You can’t make a good judgment on anything based on one variable.

Back to REITs, yes, interest rates are going up. It would be great if they were 0% forever, but they are never going to be. There is another variable at work. Why are interest rates higher? Inflation.

Where higher interest rates are a headwind, inflation is a tailwind for REITs that drives earnings higher. The question we need to ask is which factor is having a greater impact. For REITs, the answer is clear, inflation is a much more powerful driving force today. Why?

- REITs spent 2020-2021 refinancing at historically low-interest rates: Very few REITs have any meaningful debt maturing until 2024. Since the bulk of debt they take out is fixed, with maturities that are 5-10 years out, rising interest rates are not an immediate headwind. It is something that will slowly start impacting expenses in 2024, but for most REITs, it will be 2030 or later before even half of their debt needs to be refinanced.

- Inflation is happening now: The 2021 inflation numbers are in and for REITs that use CPI-linked leases, they’ve already started seeing the benefits of inflation. Same-property rents are up the most they’ve been in decades because of inflation. Additionally, REITs benefit from inflation more quickly with new leases. The exact impact varies by specific company and sector, but in general, REITs are already realizing the tailwinds of inflation.

The bottom line is that REITs will have to face refinancing at higher rates in the future, but they don’t have to face it now. Right now, they have the benefit of inflation, driving their revenues higher. This is something that will benefit them over the next 3-5 years as many leases will increase rent at renewal. By the time refinancing comes around, who knows what rates will be? If there is a recession, they could be right back at zero. Odds are high there will be at least one recession before 2030.

AWP provides us with immediate diversification to REITs.

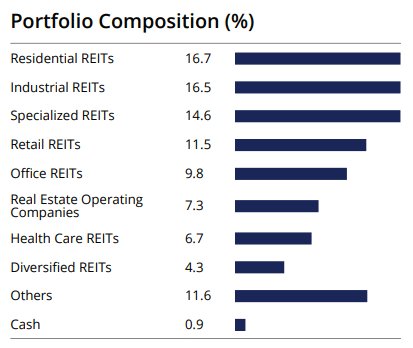

April 2022 Performance Data and Portfolio Composition

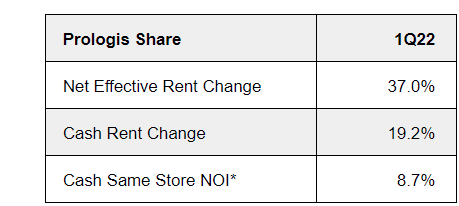

Note that AWP’s largest exposure is to sectors that are immediately benefiting from inflation with residential at the top of the list. With leases typically only one year, apartments are able to raise rent quickly to factor in inflation. Industrial REITs have also been reporting extremely strong rent growth. AWP’s largest single position is Prologis (PLD), an industrial REIT that reported extremely strong rent growth.

PLD Q1 2022 Earnings

When rent is growing this quickly, it provides a tailwind that will far outweigh the headwind of rising interest expense. Especially since it will be several years of inflation before interest expense starts to materially rise.

REITs are going through a period that is extremely favorable for their business model. AWP is one option to get instant diversified exposure to this hot sector before the market realizes how great the environment is for them.

Shutterstock

Conclusion

Through AWP and MPW, I can become an owner of a vast empire of real estate. I don’t have the capital intensity required if I tried to build the empire from the ground up myself, yet I can benefit from the empire size nonetheless. By employing expert management teams, I avoid many of the hassles of being a landlord while still getting the benefits from large dividends paid to my wallet.

My retirement is covered by countless dollars flowing into my wallet. This allows me to enjoy new places, experiences, and hobbies. I don’t fret about the movement of the market. I can celebrate the highs when the market climbs, or plan what to add and buy when it drops. Overall, I can easily maintain a positive outlook or take a break from the market whenever I want without fear about my income stream.

Hospitals are not going out of demand. Real Estate is needed and continues to have lasting value. These both pay me large dividends and I am all the wealthier for it.

That’s the joy of income investing.

Be the first to comment