Scott Olson

Is the tide turning on rising labor costs and soaring commodity prices? It might just be so.

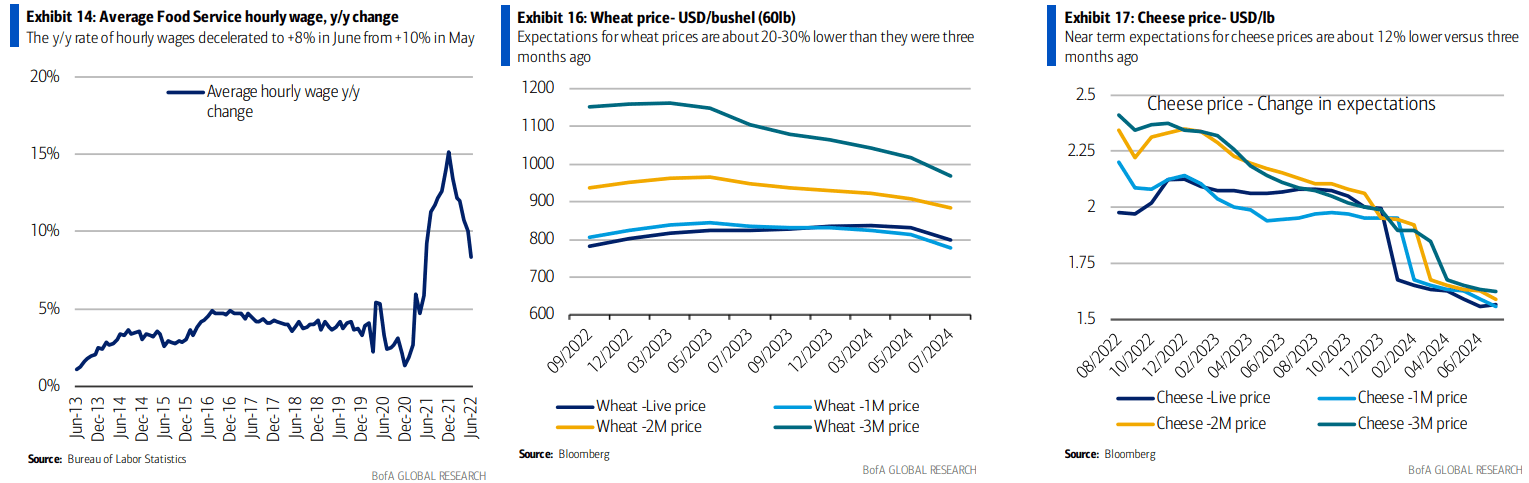

According to Bank of America, the year-on-year change in wage growth for food service workers peaked at +15% earlier this year and has since fallen to just +8% as of June.

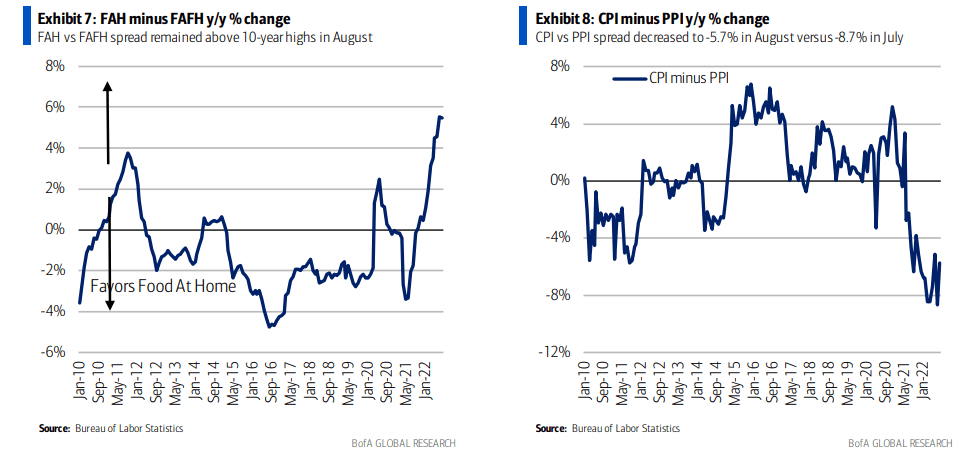

As for wholesale food prices, those are expected to be in outright decline, according to Bloomberg data. Finally, the all-important food at home minus food away from home (FAH-FAFH) remains hugely in favor of restaurants.

One popular pizza company kicks off earnings season this week.

Industry Fundamental Trends: Falling Labor Wage Growth, Easing Commodity Prices Expected, Extremely Favorable FAH-FAHM Spread

BofA Global Research

BofA Global Research

According to Bank of America Global Research, Domino’s Pizza (NYSE:DPZ) is the No. 1 pizza delivery company in the world with roughly 16,000 stores in 50 states and more than 70 countries. DPZ’s system is more than 97% franchised and 63% of stores are located internationally. The company has been benefitting from a steadily growing online/digital ordering mix that currently represents over 60% of domestic orders and has a long runway for growth.

The Michigan-based $11.3 billion market cap Hotels, Restaurants & Leisure industry company within the Consumer Discretionary sector trades at a high 24.6 trailing 12-month GAAP price-to-earnings ratio and pays a small 1.4% dividend yield, according to The Wall Street Journal. Ahead of earnings this week, just 4.2% of shares are short.

Domino’s has significant upside potential with falling year-on-year wage growth gains for low-end jobs along with improving supply chains across the globe. Moreover, a strong worldwide presence helps to diversify operations. Downside risks include a continued strong U.S. dollar and high competition in the fast-food pizza industry.

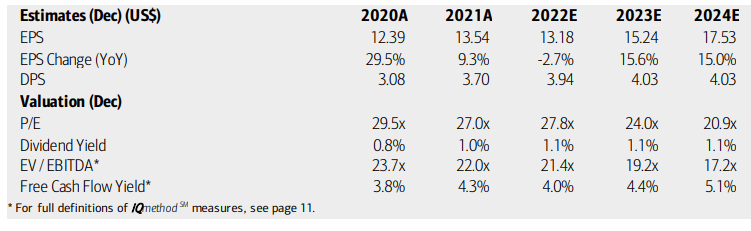

On valuation, analysts at BofA see earnings per share falling slightly this year but then rebounding sharply in 2023 and 2024. Dividends are also expected to increase into 2023. The stock’s high operating P/E ratio makes sense given a resumption of strong EPS growth next year. DPZ’s PEG ratio is thus reasonable at less than 2, but the firm’s EV/EBITDA multiple is quite elevated. Finally, Domino’s has a steady free cash flow yield, which should allow for shareholder-accretive activities.

DPZ: Earnings, Valuation, Dividend Forecasts

BofA Global Research

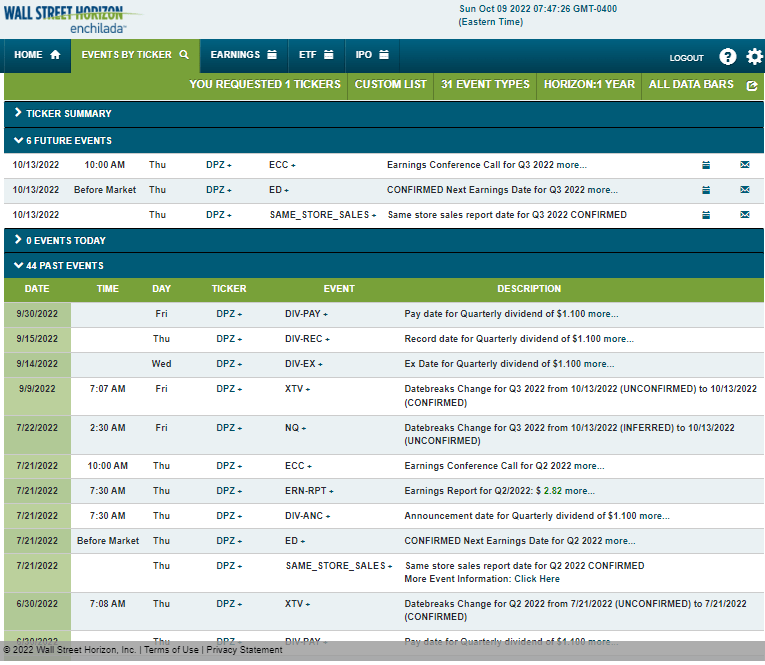

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q3 2022 earnings date of Thursday, Oct. 13 BMO with a conference call immediately after results hit the tape. You can listen live here.

Corporate Event Calendar

Wall Street Horizon

The Options Angle

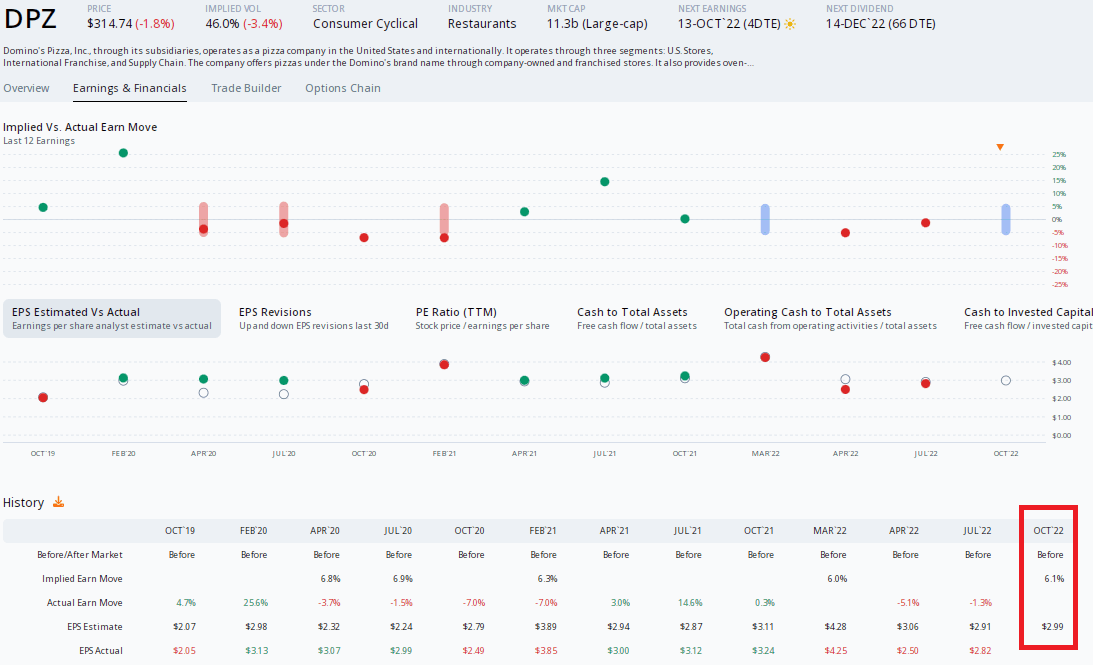

Data from Option Research & Technology Services (ORATS) show a consensus EPS estimate of $2.99 for DPZ. If that amount verifies, it would be a 4% year-over-year earnings drop. Unfortunately for the DPZ bulls, there have been three net downgrades of the stock since its last profit report. Moreover, Domino’s has missed earnings estimates in the past three quarterly releases.

The options market has priced in a 6.1% post-earnings stock price move using the nearest-expiring at-the-money straddle. That’s about in-line with previous expected moves and the stock has not swayed too much over its recent quarterly reports. So, the options appear fairly valued.

Earnings Preview: A 6% Stock Price Move Expected

ORATS

The Technical Take

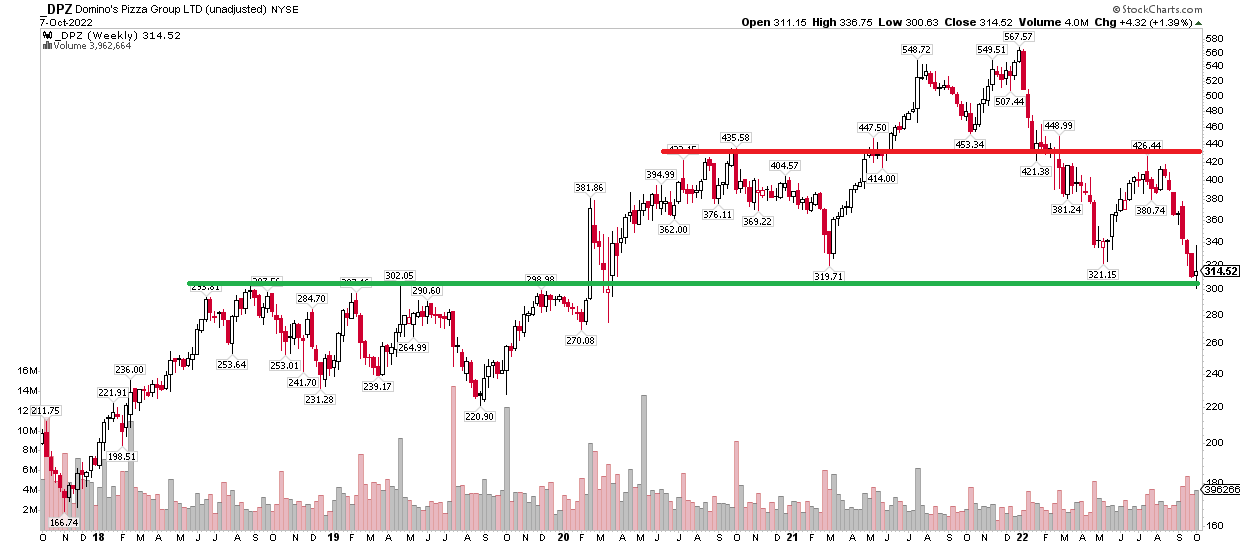

Here’s where things get exciting.

DPZ’s 5-year weekly chart illustrates that the stock has hit key support near just above the $300 mark. Now is a favorable risk/reward setup for this Discretionary stock as we head into an important earnings report. Going long here by purchasing shares or buying call options could make sense. A break below $300, particularly on a weekly closing basis, would be bearish.

What I also like here is that the stock might have fooled some investors when it moved below a $320 double-bottom pattern. A potential false breakdown from there could be bullish, too. I see resistance, however, in the $426 to $436 range – profits should be initially taken there on a share price rebound.

DPZ: Stock Approaches Support, $430 Resistance

StockCharts

The Bottom Line

Domino’s looks like a buy heading into earnings. Investors should be mindful of critical support just under Friday’s close price, though. A bullish position should be exited should the stock break decisively below $300, while $320 and about $430 could be resistance. On valuation, the company is quite reasonable right now after a nearly 40% drop from its high at the turn of the year.

Be the first to comment