The best photo for all

Electronic signatures were first described way back in 1976, but it wasn’t until the ESIGN act was signed by President Bill Clinton in the year 2000 that the service became legally binding. After that point, a series of players entered the market, with DocuSign being one of the pioneers (founded in 2003). Since then, the company has become the number one digital signature solution by market share (according to the company), with over 1 million customers. DocuSign, Inc. (NASDAQ:DOCU) has penetrated large organizations and continued to produce strong financial results. In this post, I’m going to break down its business model, financials, and valuation, let’s dive in.

Business Model

DocuSign is the market leader in e-signature solutions with approximately 1.32 million customers. Its customer base includes a series of large enterprises which adds immense credibility to the solution. These customers include Apple, Microsoft, Salesforce, SAP, United Airlines, and many more. The beauty of DocuSign’s solution is it is applicable to all industries and geographies which gives it a large and diverse total addressable market. DocuSign estimates its total addressable market (“TAM”) to be a staggering $50 billion, based on a study commissioned by the company.

DocuSign Customers (IR presentation December 2022)

The benefits of an e-signature solution are simple yet powerful. Traditional paper signing is time-consuming, as it often requires a clunky printing and scanning process. On the other hand, DocuSign’s solution is usually completed in less than 15 minutes by 44% of people, and 79% of people complete a signature in less than one day, end-to-end. The company also has built-in viral/word-of-mouth growth as there are two parties to every transaction. Therefore when one company sends an eSign contract to another, they will likely ask, “Why aren’t we doing this?” I believe this built-in free advertising model has been a key factor in DocuSign’s growth. For example, I have used the platform multiple times, but I am not a customer myself.

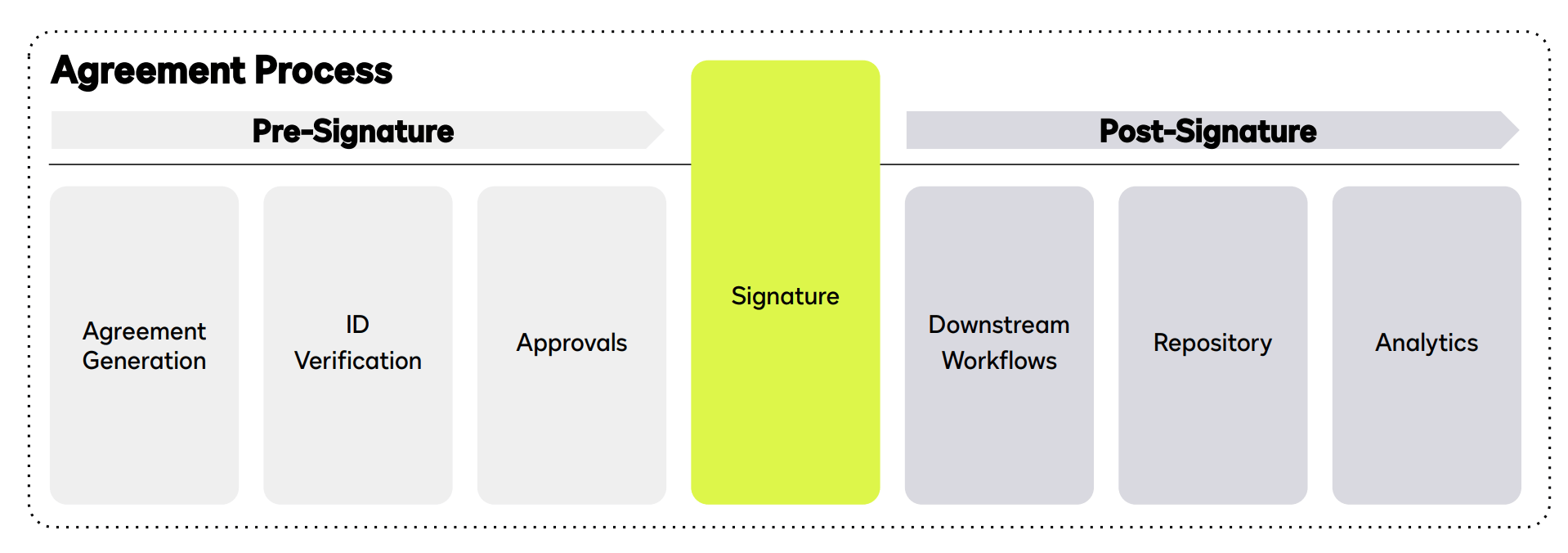

DocuSign has gradually expanded its solution to include “pre-signature” processes such as Agreement Generation, ID Verification, and Approvals. In addition, to “Post Signature” tasks such as Downstream Workflows and Analytics. This series of “automation” products is in the early stages, but I believe this product expansion will be essential to the company’s success. There are many competitors on the market which offer a simple eSignature solution. I will discuss more on these in the “Risks” section.

DocuSign (Q3,FY23)

The company charges for its solution through a combination of “Pricing by Functionality” and a Capacity based volume model. It sells its solution through a network of Independent Software Vendors [ISVs] such as Salesforce, WorkDay, Microsoft, and ServiceNow. In addition, it sells a series of “System Integrators” such as consultancies and resellers. As mentioned prior, e-signature solutions are abundant and therefore, distribution is a key differentiator.

Growing Financials

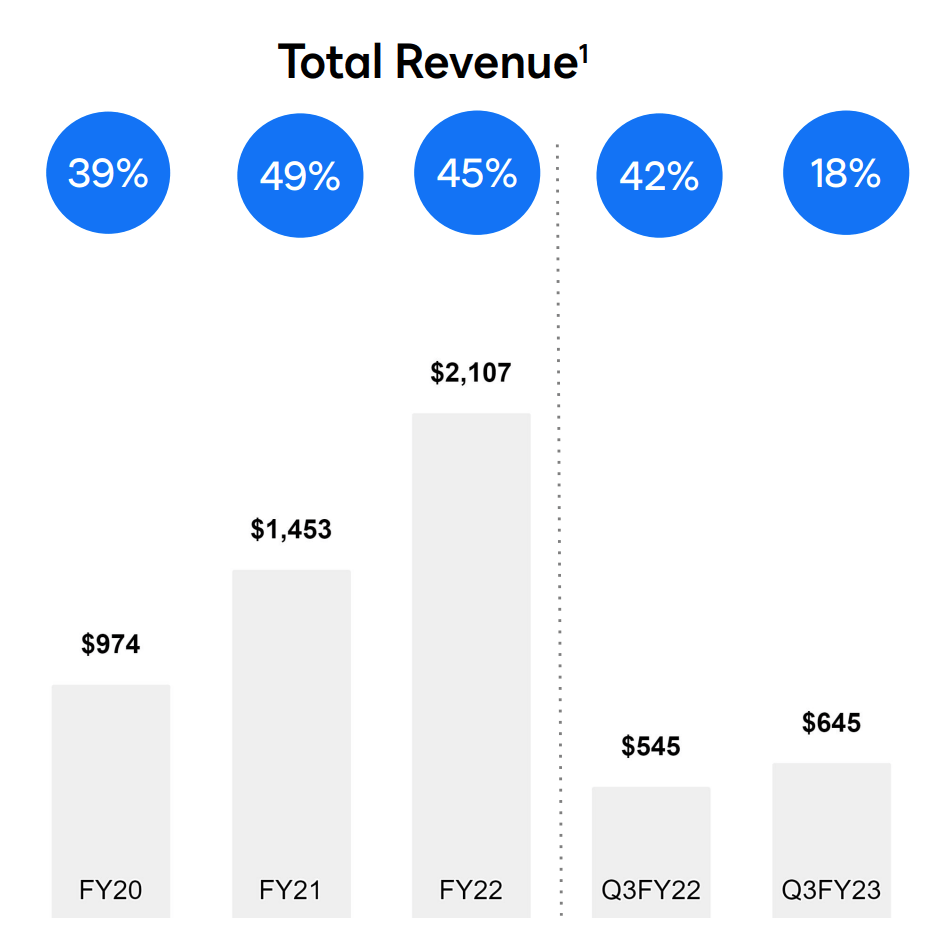

DocuSign reported strong financial results for the third quarter of fiscal year 2023. Revenue was $645.46 million, which beat analyst estimates by $18.08 million and increased by a solid 18.33% year over year. Foreign exchange headwinds from a strong U.S. dollar impacted revenue by ~2% but wasn’t a major issue. The first pillar of DocuSign’s growth strategy is to further expand its “international revenue” which currently contributes to just 24% of total revenue. So far this strategy is working well, with international revenue increasing by 23% year over year to $157 million. DocuSign also increased “Billings” which can be thought of as the true “top line” for SaaS companies, by 17% year over year to $659 million. This was driven by early customer renewals.

Revenue (Q3,FY23)

The second pillar of DocuSign’s growth strategy is to focus on continually expanding “upmarket” and targeting enterprises. This makes sense for a few reasons firstly enterprises tend to have larger account expansion potential and these organizations often have greater retention rates. A negative of selling to the enterprise is the sales cycle tends to be long, with a huge buying committee. DocuSign aims to reduce this friction by increasing its ability for customers to purchase the product via a “self-serve” option. Given an e-signature solution is not overly complicated, and many people have used one in the past, I believe this strategy is solid.

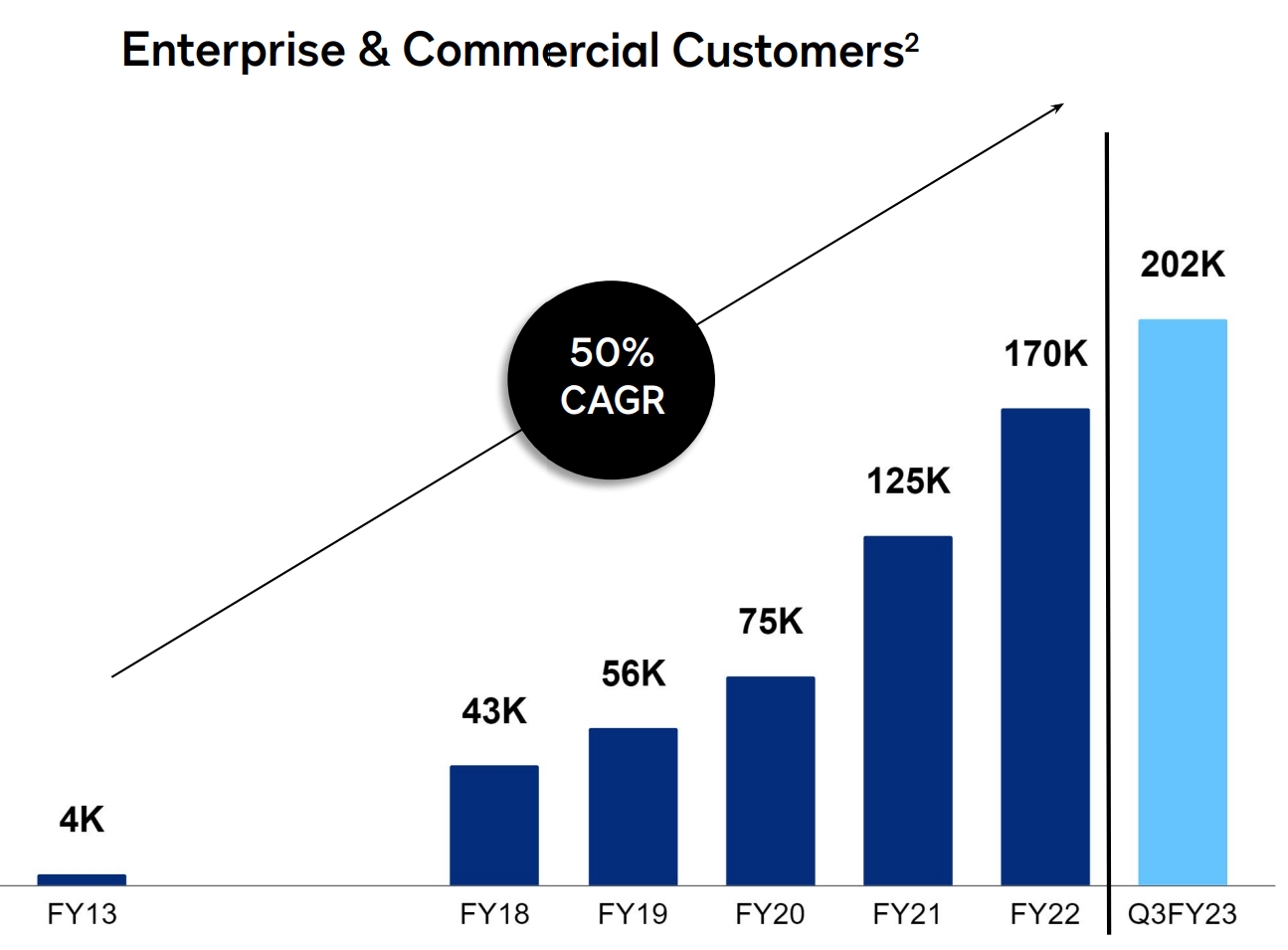

DocuSign has increased its Total customers by 19% year over year to 1.32 million, with approximately 42,000 new customers added during the quarter. In addition, its Enterprise customers have increased by a rapid 50% CAGR over the past few years to 202,000.

Enterprise Customers (Q3,FY23)

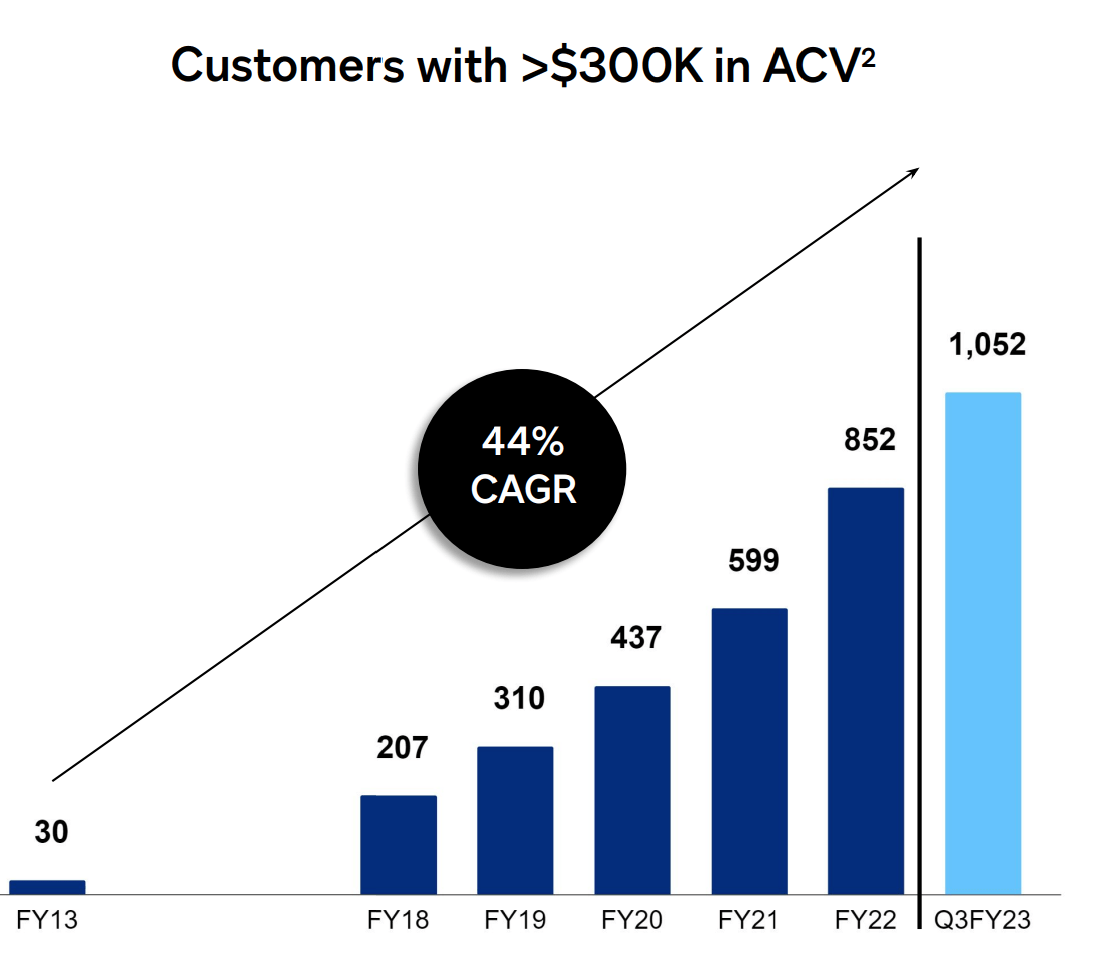

DocuSign also reported 1,052 high-ticket customers which have over $300,000 in annualized contract value. This represented an increase of 26% year over year. It is amazing to see that some customers are willing to pay such a high amount, for what would be considered a fairly simple solution. I believe this is driven by DocuSign’s product expansion which is a key differentiator. DocuSign’s management noted in its earnings call, that customers often choose the company, for its strong privacy and security credentials, versus competitors.

High ticket customers (Q3,FY23 report)

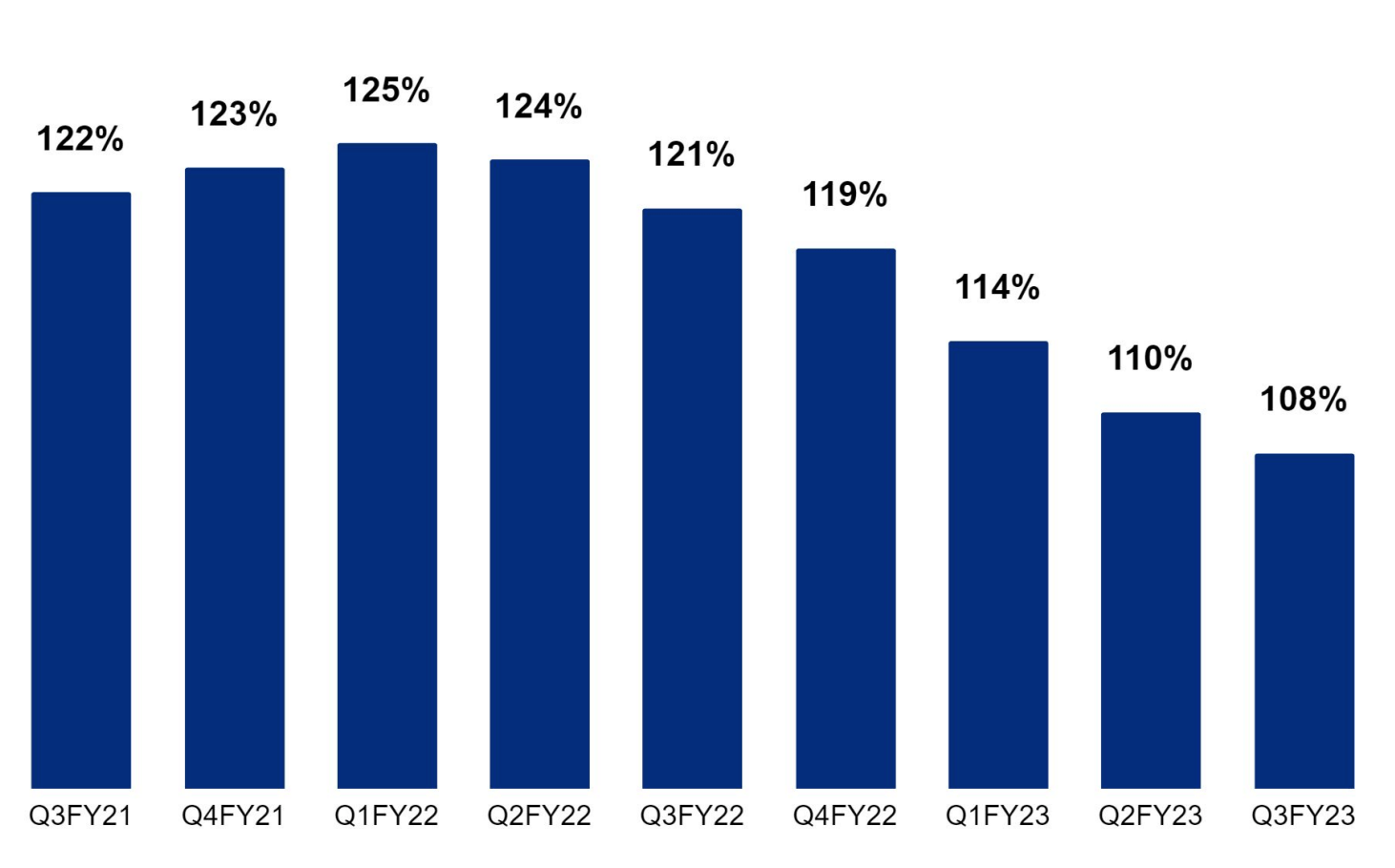

DocuSign reported a solid dollar net retention rate of 108%, which was down from prior years due to the macroeconomic environment and customers being cautious about expansion as a result. However, anything over 100% is solid as it means customers are finding the product “sticky” and spending more. Contract signatures are a key part of the day-to-day operations of many businesses. Therefore, a larger company switching to a competitor would be unlikely, as the transition period would likely cause disruption. This can be seen as a barrier to entry for the business as it has already established its solution in the market.

Retention rate (Q3,FY23)

Margins and Expenses

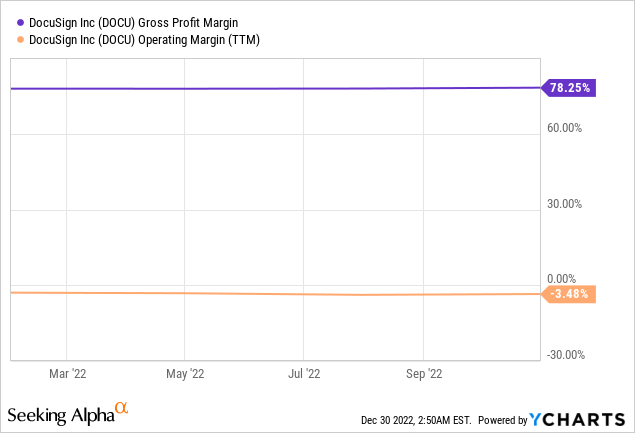

As a software company, DocuSign reported a solid Non-GAAP gross margin of 83%, which was up by 1% over the prior year. Its Non-GAAP operating margin also increased by 1% year over year to 23% which is the average of the software industry. Both these trends are positive especially given the high inflation environment which has squeezed the margins of many other companies. Management has been ruthless in managing its cost structure and is currently going through a “restructuring plan” to reduce its workforce of approximately 7,522 people. The “restructuring” did result in a $28 million one of expense, but long term it looks like the right strategy, going into an uncertain macroeconomic environment.

Earnings per share was negative $0.15, which beat analyst estimates by $0.04. On a Non-GAAP basis, DocuSign is profitable and reported EPS of $0.57, which beat analyst estimates by $0.15.

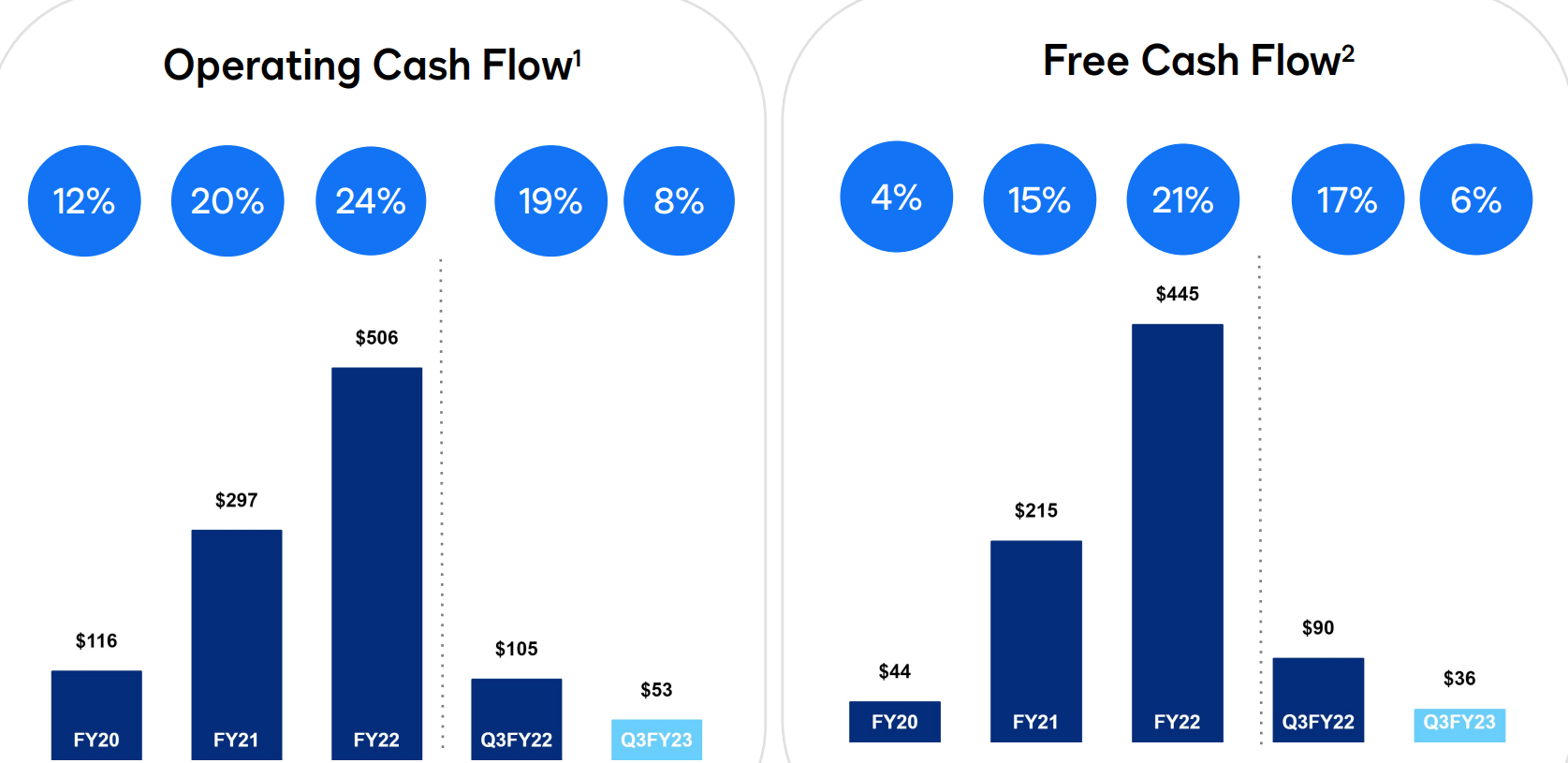

DocuSign reported solid Operating cash flow of $53 million, at an 8% margin. In addition to Free cash flow of $36 million at a 6% margin. Both were impacted by the timing of collections as the company transitioned to a new ERP system and the aforementioned “restructuring costs.”

Cash Flow (DocuSign)

DocuSign has a solid balance sheet with $1.1 billion in cash, cash equivalents, restricted cash, and marketable securities. The company does have fairly high debt of $837.7 million, but the vast majority of this $684.9 million is long-term debt and thus manageable.

The company also bought back ~740,000 shares, at a fair value of $38 million, which showed confidence by management. At the end of Q3, the company had $137 million in buyback capacity remaining.

Moving forward, management is forecasting slower revenue growth than prior years, with just 10% growth in Q4 expected, at a range between $637 million and $641 million. This is forecasted to be driven by the macroeconomic environment, which will likely result in longer sales cycles. A positive is for the full fiscal year 2023, revenue is forecasted to be between $2.483 billion and $2.497 billion, increasing by 18% to 19% year-over-year.

Advanced Valuation

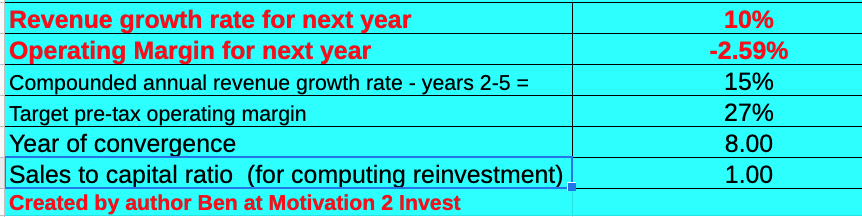

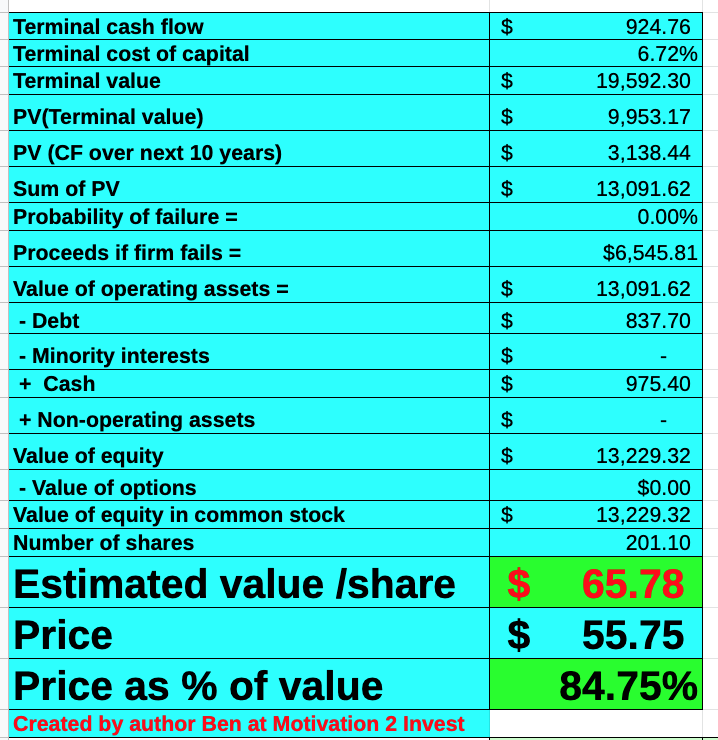

In order to value DocuSign, I have plugged the latest financials into my advanced valuation, which uses the discounted cash flow (“DCF”) method of valuation. I have forecasted 10% revenue growth for next year, which is fairly conservative and aligned with management forecasts for Q4. Then in years 2 to 5, I have forecasted growth rates to improve and revenue to increase by 15% per year.

DocuSign stock valuation 1 (created by author Ben at Motivation 2 Invest)

To increase the accuracy of the valuation, I have capitalized R&D expenses which has lifted net income. In addition, I have forecast the company will be able to grow its operating margin to 27% over the next 8 years. I expect this to be driven by increased upsells and account expansion opportunities, as the company returns to a higher net dollar retention rate of ~125%.

DocuSign stock valuation 2 (created by author Ben at Motivation 2 Invest)

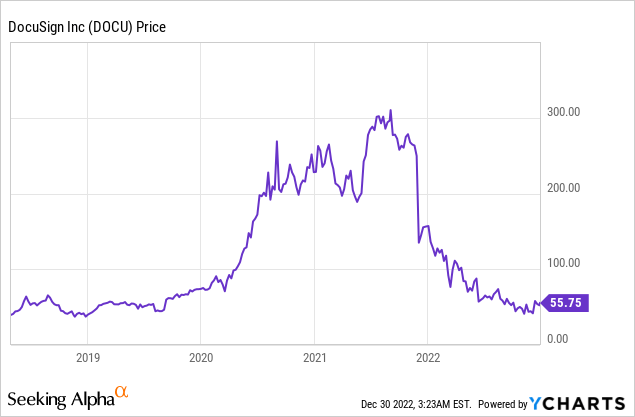

Given these factors, I get a fair value of $65.78 per share. DocuSign, Inc. stock is trading at $55.75 per share at the time of writing and thus is ~15% undervalued.

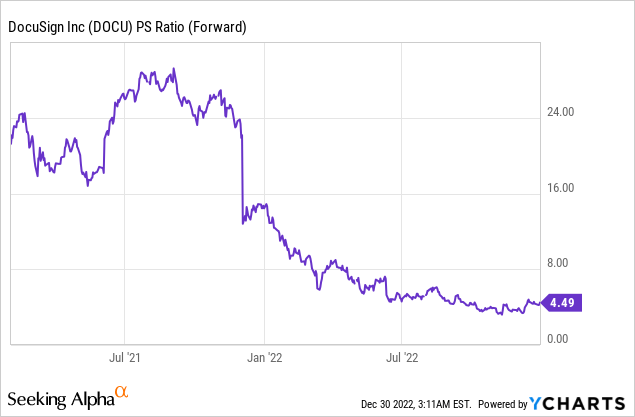

As an extra data point, DocuSign trades at a price-to-sales ratio = 4.33, which is 74% cheaper than its 5-year average.

Risks

Fierce Competition

I believe the biggest risk to DocuSign is competition. I personally have seen many cheap or even free eSign platforms online. In addition, we have other players such as Hello Sign, Adobe Acrobat Sign, SignNow, ZohoSign etc. A positive is DocuSign has the highest rating on Gartner and strong traction with the enterprise.

Recession

Management reported they were seeing “softening demand” in the third quarter and this included “smaller deal sizes and expansion.” I forecast this trend to continue at least for the next year as many analysts are forecasting a recession.

Final Thoughts

DocuSign, Inc. offers the leading e-signature solution and is poised to continue its growth among enterprises and internationally. The company has continued to produce solid financial results despite a tough economic backdrop. In addition, DocuSign, Inc. stock is undervalued intrinsically and relative to historic multiples and thus it could be a great long term investment.

Be the first to comment