LMS – Learning Management System Khaosai Wongnatthakan

Introduction

In 2005, there was a lecturer who taught at the University of Florence on Content Management Systems. One day, he observed and pondered about the time-inefficient nature of how learning programs were conducted.

In universities, is it really necessary for students to traverse the entire campus to collect a learning handout? In organizations, does time and money really need to be spent every time to fly people from all around the world for them to participate in a one-size fits all course?

These were the questions that Claudio Erba pondered almost 18 years ago. His curious nature and entrepreneurial spirit gave rise to an e-learning startup in Naples, Italy. Today, that startup is now a $1.7 billion market cap global SaaS company with $134 million in revenues, more than 700 employees and more than 3000 customers from over 70 countries.

This is my analysis of one of my core portfolio holdings – Docebo (NASDAQ:DCBO) – whose story I think has just begun.

Business Brief

Docebo is a corporate learning management system (LMS) that helps users create, manage, and deliver content to train employees, suppliers, partners and customers. It also allows for measurement and analysis of learning outcomes, linking them to business goals.

Docebo solves the problem of having multiple legacy LMS solutions across divisions and departments in siloed applications that do not configure well with existing business work flows in the technology stack.

Founded in 2005 in Italy, Docebo has steadily grown organically over the last 15 years to become one of the leading enterprise SaaS companies in its niche. Now, the company is embarking on an accelerated wave of industry tailwinds to continue scaling its business at a rapid, but healthy rate.

Thesis Summary

I am bullish on Docebo due to 3 key reasons:

- The corporate learning solutions market has a long runway of high, greenfield growth

- Docebo’s strong execution DNA gives it a competitive advantage

- Docebo is led by a founder CEO with an equity stake and a track record of exceeding expectations

The corporate learning solutions market has a long runway of high, greenfield growth

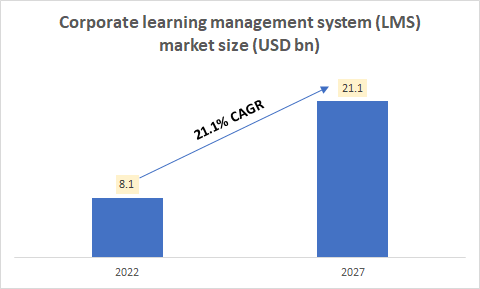

Corporate learning management system (LMS) market size (MarketsandMarkets, Author’s Analysis)

According to MarketsandMarkets Research, the corporate learning management system (LMS) market is expected to grow at a 21.1% CAGR over the next 5 years from $8.1 billion to $21.1 billion. Key drivers of growth within organizations include rapidly changing training needs to improve productivity and increase employee retention amid a growing demand for more complex skills.

An attractive feature of the industry opportunity is that 70% of the addressable growth market is based on untapped greenfield opportunities that relate to enterprises investing in training their ecosystem partners such as suppliers, distributors and customers. As noted by Fosway Group:

Corporates are extending their focus to train their external stakeholders online including customers and partners

Fosway Group; Europe’s #1 HR Industry Market Research firm

Wide, greenfield opportunities are preferable to a penetrated market as customer acquisition costs tend to be lower, thus leading to improved growth productivity metrics for software vendors.

The industry now sits at an important inflection point, with enterprises modernizing their learning and development strategies along an accelerated track that favors social, mobile-friendly and personalized learning, augmented by the usage of AI. Indeed, only 5% of executives believed learning and development practices wouldn’t change after the pandemic. This is giving modern, SaaS-based solutions such as Docebo a roadmap for market share gains over legacy vendors.

Docebo’s strong execution DNA gives it a competitive advantage

Docebo proves its mettle in its execution capabilities on multiple success parameters typical for SaaS companies:

Docebo’s marquee customer base gives it a referenceable edge

Sample of Docebo’s Customers (Docebo 3Q FY22 Investor Presentation)

For an enterprise software company selling only in its home market of Italy for the first 7 years, it is a long and arduous process to get a seat at the bidding table, let alone win bids with marquee clients such as Amazon’s AWS (AMZN), BMW (OTCPK:BMWYY), L’Oreal (OTCPK:LRLCF) (OTCPK:LRLCY), Thomson Reuters (TRI) and others. Yet, this is precisely what Docebo has been able to do over the last 10 years to get to its current portfolio of more than 3250 customers. A portfolio of big customers improves the brand awareness of Docebo, which makes incremental customer acquisitions easier.

Market leadership recognition gives Docebo a strong brand position to keep winning customers

Awards are important to analyze for software firms as they give signals about market leadership and improve brand awareness. Prospective customers often review vendors’ awards and ratings awarded by specialist industry research firms to conduct vendor shortlisting.

Docebo has scored the maximum possible performance score (which measures customer acceptance and satisfaction), the 2nd highest potential score (which measures solution scope and depth), and tied 1st position for the overall score in its mid-tier total cost of ownership class. It has achieved these rankings consistently for 5 consecutive years (2019 to 2023) in Fosway Group’s vendor positioning matrix for Learning Systems.

In December 2021, Docebo won 9 awards, including 6 gold awards in the Brandon Hall Group (BHG) Excellence in Technology forum. This made it part of an elite list; one of 16 other companies to win more than 5 awards, among a set of hundreds of companies in the niche. BHG is a specialist research and training firm for Learning & Talent Executives in Human Capital Management domain that has been operating for 30 years; again, a reputable source.

Docebo is gaining market share from incumbents

Docebo has shorter sales cycles compared to industry averages. For example, it tends to close deals with enterprises in 9 to 12 months compared to the industry norm of 18-24 months. Furthermore, Docebo’s solution addresses organizations’ learning and development requirements at the specific functional levels. This is in contrast to the more centralized learning solutions offered by legacy incumbents such as Cornerstone.

Increasingly, enterprises want to close quick deals for an integrated learning solution that still addresses specific departmental training needs. And Docebo is capitalizing on these trends to displace existing vendors:

But a dynamic that we are seeing is also that on the top of the pyramid, I mean, the very big, big deals we are seeing a shift from other vendors to us due to the consolidation that is happening between legacy players that are now creating a single entity. And there are customers that are not happy about that and they are shifting, and we are seeing an inflow of those kind of reckless sort of migration.

Claudio Erba, Founder CEO in Q3 FY22 earnings call (author’s emphasis)

Not too long ago, Deliveroo had multiple legacy and internally developed LMSs in place. Today, Docebo addresses their needs with a single LMS for internal and external stakeholders.

Alessio Artufo, President & COO in Q3 FY22 earnings call

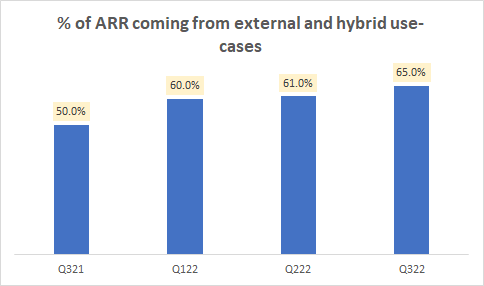

Docebo’s functional-department focused approach to learning solutions makes it better positioned to capture growth opportunities associated with training suppliers, partners and customers in the value chain. The company refers to this as ‘external and hybrid use cases’.

% of ARR coming from external and hybrid use-cases (Company Filings, Author’s Analysis)

There has been a steady climb in the contribution of such use cases from 50% 3 quarters ago to 65% as of Q3 FY22. This is favorable because the expansion increases the switching costs of the enterprise software solution, which in turn boosts retention rates and improves customer lifetime value (LTV).

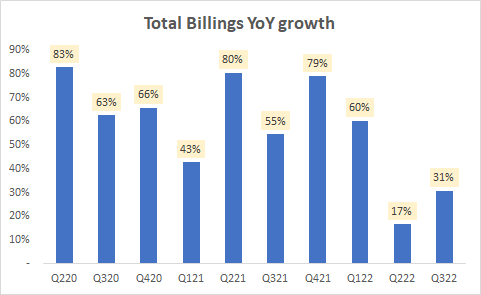

Docebo displays solid growth momentum at high gross margins

Total Billings YoY growth (Company Filings, Author’s Analysis)

In SaaS businesses, billings are a leading indicator of revenues. Docebo has had impressive billings growth, typically above 30% YoY. For context, according to Fosway, YoY growth below 15% in 2022 corresponded to loss in market share. Thus, this highlights that Docebo is growing much faster than the industry, confirming aforementioned analogies of market share growth with hard numbers.

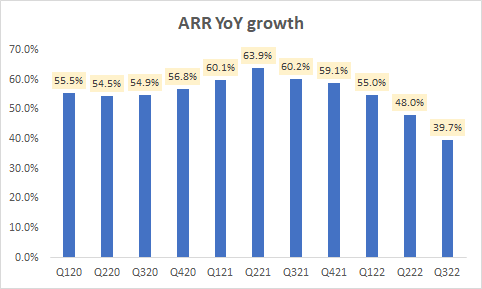

The strong billings growth has led to consistently high growth in annual recurring revenue (ARR), typically more than double the enterprise LMS industry growth rate of 21.1% YoY mentioned earlier:

ARR YoY growth (Company Filings, Author’s Analysis)

Q2 FY22 and Q3 FY22 showed a decline in the growth rates, although it is still high. Importantly, this was due to final stage contract-closing delays faced by customers’ operational disruptions amid business process and organizational structure changes. It was not due to falling demand:

To be very clear, demand hasn’t been impacted. We like the strong demand for products and services, and win rates remain really strong.

Alessio Artufo, President & CRO at Citi’s Global Technology Conference in September 2022

Hence, I anticipate pent-up effects of these contract-closing postponements to lead to stronger growth prints in the upcoming quarters.

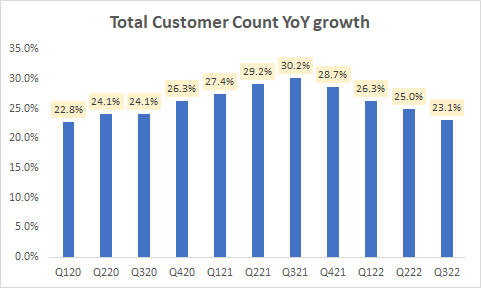

Regarding the composition of top-line growth, Docebo scores well on account growth and accounting mining parameters. Customers counts are consistently growing above 20% YoY:

Total Customer Count YoY growth (Company filings, Author’s analysis)

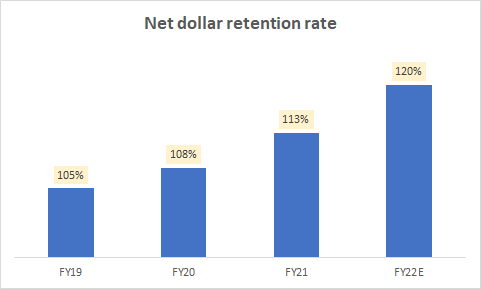

And a consistently increasing net dollar retention rate is proof that the company’s ‘land-and-expand’ client mining strategy is yielding fruitful results:

Net dollar retention rate (Company filings, Author’s analysis)

In FY22, I expect a sharp jump in net dollar retentions from 113% to 120% as management has indicated this figure to be upwards of 120% in the Q3 FY22 earnings call.

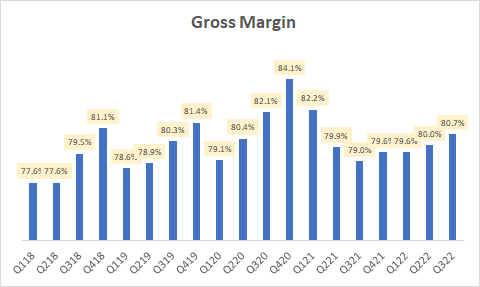

Gross Margins (Company Filings, Author’s Analysis)

Docebo’s gross margins are consistently around the 80% mark. This is quite impressive. For context, leading SaaS companies such as Salesforce’s (CRM) gross margins are in the low 70’s% range, ServiceNow’s (NOW) gross margins are marginally lower at 77-78%.

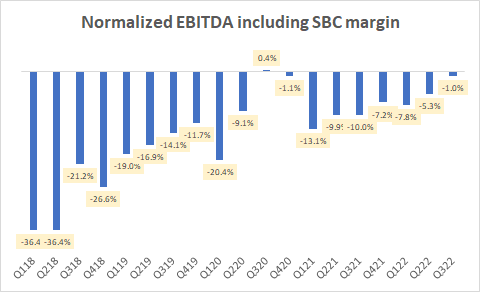

Docebo is on track to profitability without sacrificing growth

Normalized EBITDA including SBC margin (Company Filings, Author’s Analysis)

As the chart above shows, Docebo is rapidly moving towards profitability. Note that I include stock based compensation as that is a real cost to the business.

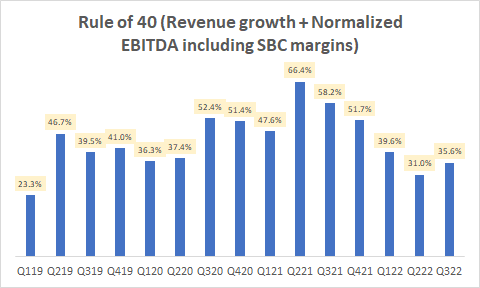

A key KPI for SaaS companies is the sum of the annual growth rate and the operating margins. If this number equals 40 or above, that’s a sign of a high quality SaaS company, according to the Rule of 40:

Rule of 40 (Revenue growth + Normalized EBITDA including SBC margins) (Company Filings, Author’s Analysis)

Over the past 15 quarters, Docebo has averaged a healthy 43.9% in the Rule of 40 metric. More recently, it has dipped below 40%, however I believe this is temporary as it is driven by postponements of deal signings instead of demand slowdown. I have contacted management for additional clarity on the levers here (see Risks and Monitorables section below).

Takeaway

In new growth fields, particularly in the technology and enterprise SaaS sector, I believe in consistent momentum in execution – winning marquee clients, gaining industry recognition and market share due to both new account growth and deeper account mining, all whilst moving steadily toward profitability – is what helps identify the makings of a SaaS behemoth early on. So far, I think Docebo fits this bill.

Docebo is led by a founder CEO with equity stake and a track record of exceeding expectations

Multiple pieces of literature, for example from Harvard Business Review, Value Walk and Schroders show that companies led by founder CEOs tend to make for better investments. Docebo is led by Claudio Erba; a founder CEO that holds a 3.72% equity stake in the business. This makes him the 4th-largest shareholder after Intercap, Cat Rock Capital Management and Fidelity. This is a positive sign as it aligns management’s interests with those of minority shareholders.

Now much of my analysis in the prior sections has been based on noting management’s commentary. But how reliable is the commentary?

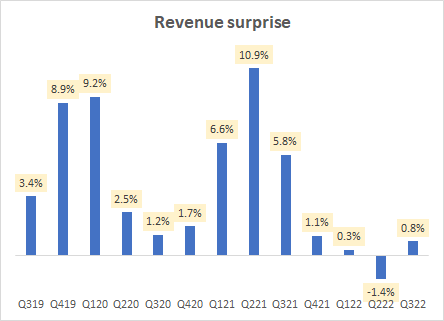

To determine this, I analyze the company’s surprise trends vs consensus estimates:

Revenue surprises (Company Filings, Capital IQ, Author’s Analysis)

Under Erba’s leadership, Docebo has generally beat Wall St’s expectations on revenues with a mean of 3.9% and a median of 2.5%.

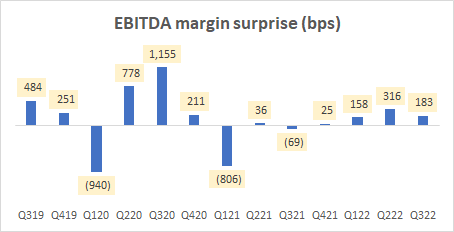

EBITDA margin surprise (bps) (Company Filings, Capital IQ, Author’s Analysis)

EBITDA margins have also generally beaten Wall St’s expectations with a mean of 137bps and a median of 183bps.

From these findings, I gain confidence to believe the bullish commentary of Erba and Docebo’s broader management team.

Valuation

Given my narrative for the stock, these are my key assumptions for a simple DCF valuation for Docebo:

Total YoY revenue growth (Company Filings, Author’s Analysis)

I have tapered the growth rates down gradually to end at 12% in 2031. I believe this is appropriate given the long growth runway for Docebo. These assumptions correspond to a 10-yr forward CAGR of 25.2%:

Total revenues CAGR (Company Filings, Author’s Analysis)

Given this company’s historical CAGRs, the 5-yr forward industry CAGR of 21.1%, and the fact that Docebo is currently growing at twice that rate, I believe my growth assumptions are quite reasonable.

EBITDA margin (Company Filings, Author’s Analysis)

I expect EBITDA margins to gradually expand due to operating leverage effects, and incremental EBITDA margins range between 40 to 60% in the tail end years. This is not unusual for well-run SaaS companies; Adobe (ADBE) for example prints a similar incremental EBITDA margin range today.

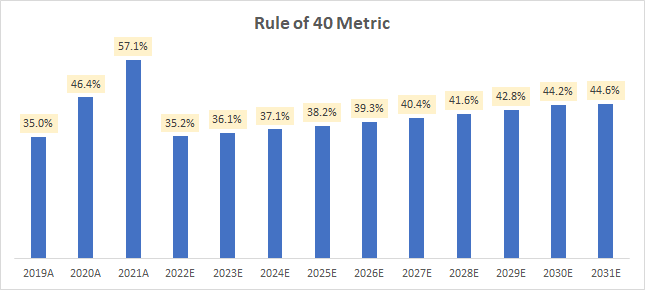

Rule of 40 Metric (Company Filings, Author’s Analysis)

My combined growth and margin assumptions imply a view that Docebo will continue to be a Rule of 40 company. I believe this assessment is realistic given management’s indications that Docebo will remain a rule-of-40 business:

I think it’s fair to assume that Docebo will remain a rule-of-40 business, with growth being the bigger contributor and the focus from our perspective, with us driving some incremental leverage, operating leverage and profitability into that rule of 40.

Sukaran Mehta, CFO in the Q2 FY22 earnings call

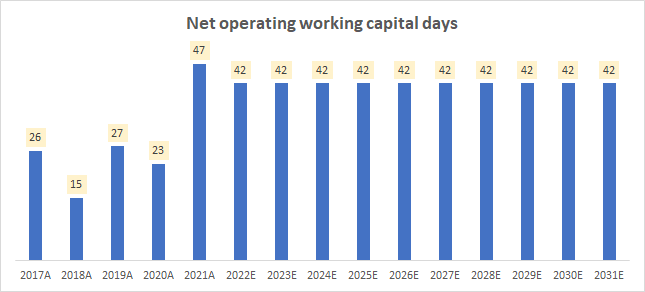

Net operating working capital days (Company Filings, Author’s Analysis)

As I have no specific view for thinking otherwise, I have kept net operating working capital days constant based on the latest quarterly levels.

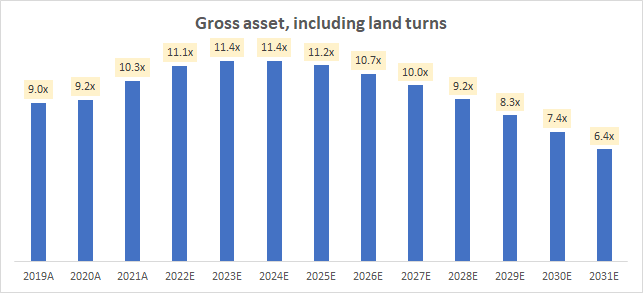

Net operating working capital days (Company Filings, Author’s Analysis)

Gross asset turns are expected to drop over a period of time, as I have assumed higher growth capex rates compared to the past, reflecting increased spends on intangible assets and potential facility expansions.

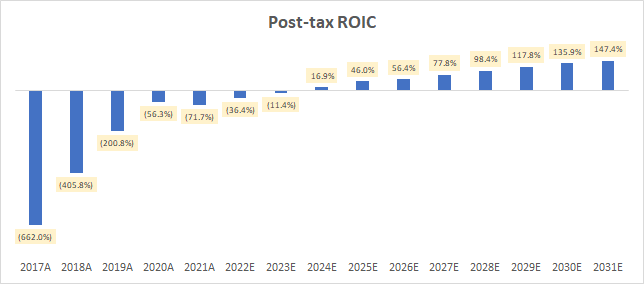

Post-tax ROIC (Company Filings, Damodaran’s Datasets, Author’s Analysis)

As SaaS companies are rather asset-light, it is not unusual for them to have high ROICs. This metric would be a direct consequence of operating margin, capex and a 25% corporate tax rate assumption, based on NYU Stern’s ‘Dean of Valuation‘, Professor Ashwath Damodaran’s data sets.

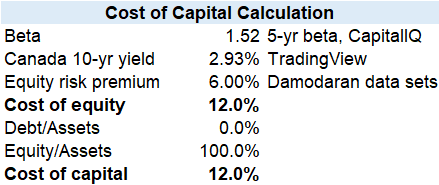

Cost of Capital Calculation (Company Filings, Capital IQ, Damodaran’s Datasets, Author’s Analysis)

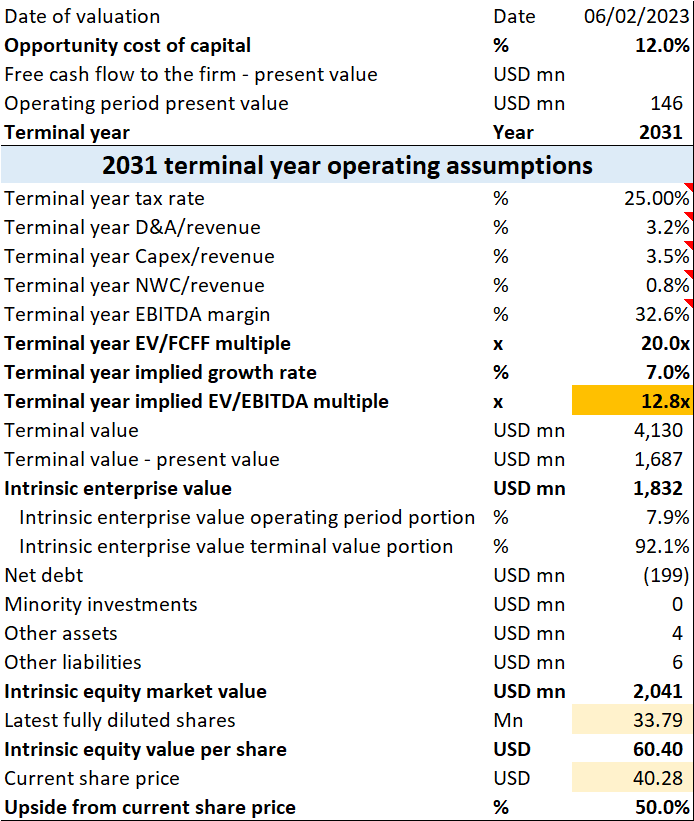

I arrive at an opportunity cost of capital of 12.0% using the assumptions outlined above.

Valuation Summary (Company Filings, Capital IQ, Damodaran’s Datasets, Author’s Analysis)

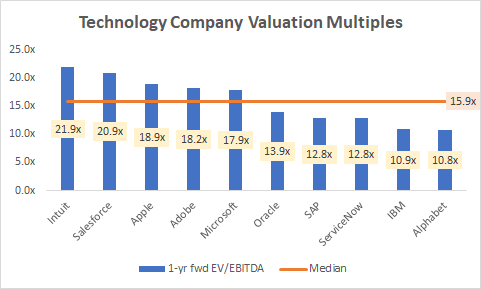

I use enterprise value to free cash flow to firm (EV/FCFF) terminal value multiples as this allows for explicit input of my terminal year (2031) operating assumption views as seen in the table above. This Twitter thread on valuation multiples explains this idea in more depth. In this case of Docebo, a 20.0x FY31 EV/FCFF multiple corresponds to a 12.8x FY31 EV/EBITDA multiple. I think this is reasonable for a growth stock such as Docebo. I do not believe my assumptions are unrealistic. For context, more mature technology companies trade at a higher median 1-yr forward EV/EBITDA of 15.9x:

Technology Company Valuation Multiples (Seeking Alpha, Capital IQ, Author’s Analysis)

Technology companies include Intuit (INTU), Salesforce (CRM), Apple (AAPL), Adobe (ADBE), Microsoft (MSFT), Oracle (ORCL), SAP (SAP), ServiceNow (NOW), IBM (IBM) and Alphabet (GOOG) (GOOGL)

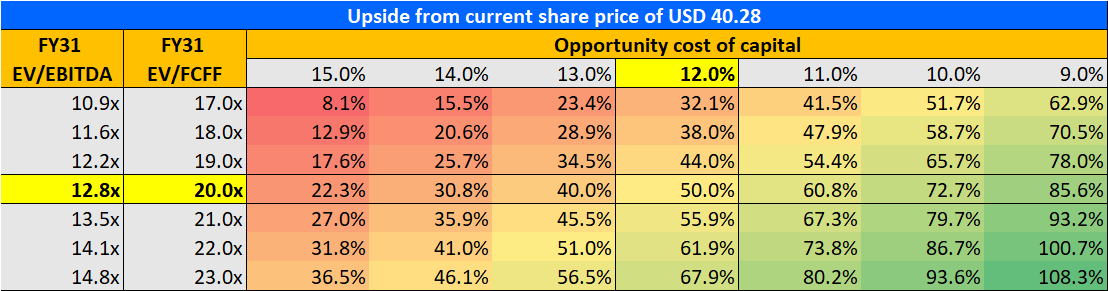

Valuation Sensitivity Analysis (Company Filings, Capital IQ, Damodaran’s Datasets, Author’s Analysis)

Sensitivity analysis on my DCF valuation of Docebo shows the stock to be attractively valued with limited downside. Overall, with an opportunity cost of capital of 12.0% and FY31 EV/FCFF of 20.0x, I see a 50.0% upside in the stock, corresponding to an intrinsic value per share of $60.40.

Key Risks and Monitorables

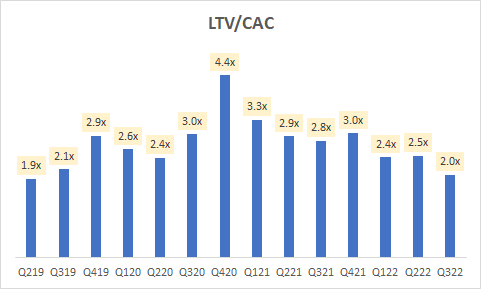

In addition to tracking the health of continued operational performance, I am also watching the company’s LTV/CAC metrics:

According to my calculations, the LTV/CAC is on a slight decline in recent quarters:

LTV/CAC (Company Filings, Author’s Analysis)

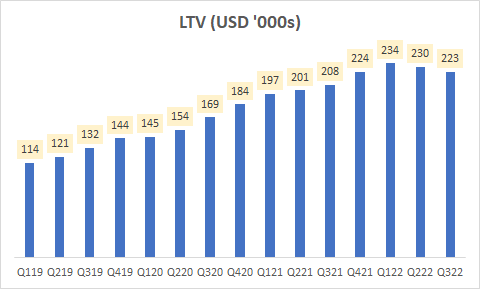

This coincides with a peaking-out of LTV:

LTV (Company Filings, Author’s Analysis)

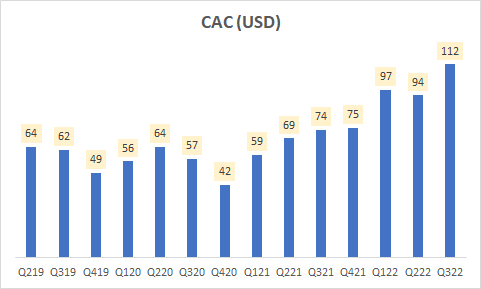

And rising CAC:

CAC (Company Filings, Author’s Analysis)

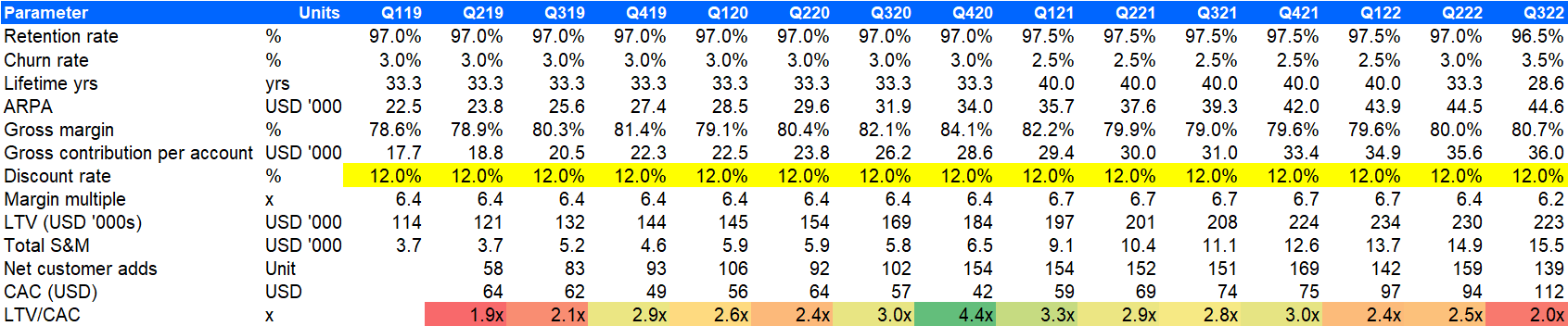

The following shows the calculation summary of Docebo’s LTV/CAC:

LTV/CAC Calculation (Company Filings, Author’s Analysis)

Of course, this may be a temporary blip down below the ideal 3.0x and above number due to delayed deal signings. However, it is still a key monitorable to track how efficiently the company is growing.

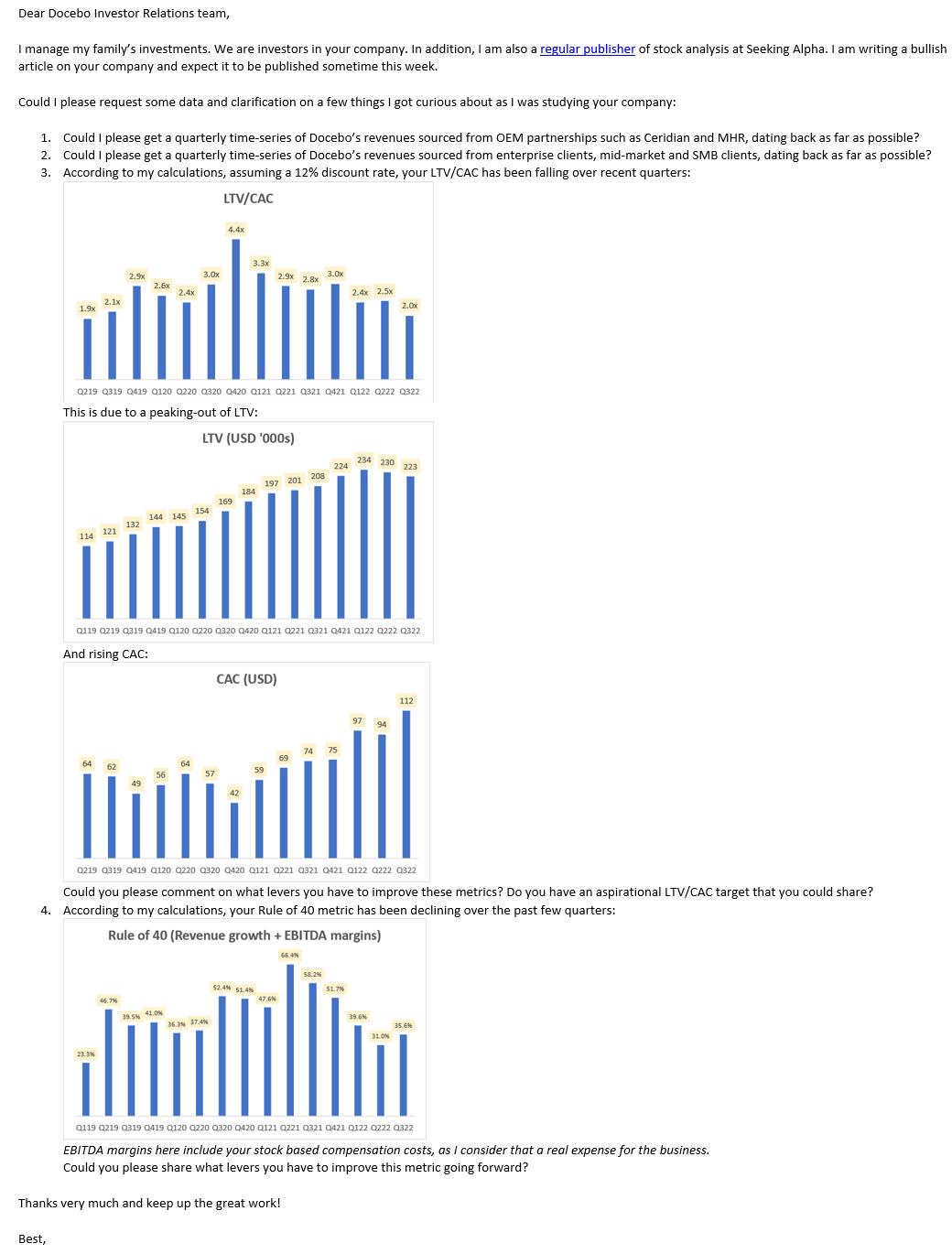

In addition to LTV/CAC, I will be monitoring the Rule of 40 Metric every quarter to see if the company is on track to rise back up over the 40% mark. I have emailed Docebo’s Investor Relations team to seek clarification on the levers they have to improve these key metrics:

Email to Docebo Investor Relations (Author’s Email to Docebo Investor Relations)

I have yet to receive a reply.

Conclusion

Docebo today is among the growth leaders in the high-growth corporate learning management system (LMS) market, which is seeing rapid modernization of enterprises’ approach to learning and development. It is doing many things right; winning marquee clients, gaining industry recognition and market share from both new account growth and deeper account mining, all whilst moving steadily toward profitability.

Moreover, management is led by a founder-CEO, which is advantageous as studies show these kinds of companies tend to outperform as investments. Finally, with the CEO being the 4th largest shareholder and a reliable track record in exceeding Wall St’s expectations, minority shareholders can find alignment of interests in the enterprise and confidence in the management’s ability to continue generating shareholder value.

My DCF-based valuation implies a 50% upside in the stock. Therefore, I rate Docebo a ‘Strong Buy’.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment