Michael Vi

Interest rate hikes do not entirely work in favor of Discover Financial Services (NYSE: DFS) today. The interest on deposits on borrowings offset loan and investment yields. It remains viable, but returns are lower. Moreover, DFS must be more cautious with its liquidity, although cash reserves remain high.

Meanwhile, dividends stay consistent and well-covered with attractive yields. However, the stock price does not seem cheap despite the continued decrease in the last year. It may still have to decrease to reflect the intrinsic value of the company.

Company Performance

Inflation is a double-edged sword for the banking and consumer finance industry. And Discover Financial Services is not an exception. It sees inflation raise interest rates and affect core operations. Although it has lulled in recent months, it remains way higher than pre-pandemic levels. Interest rate increments are projected to slow down, but the actual value may still increase.

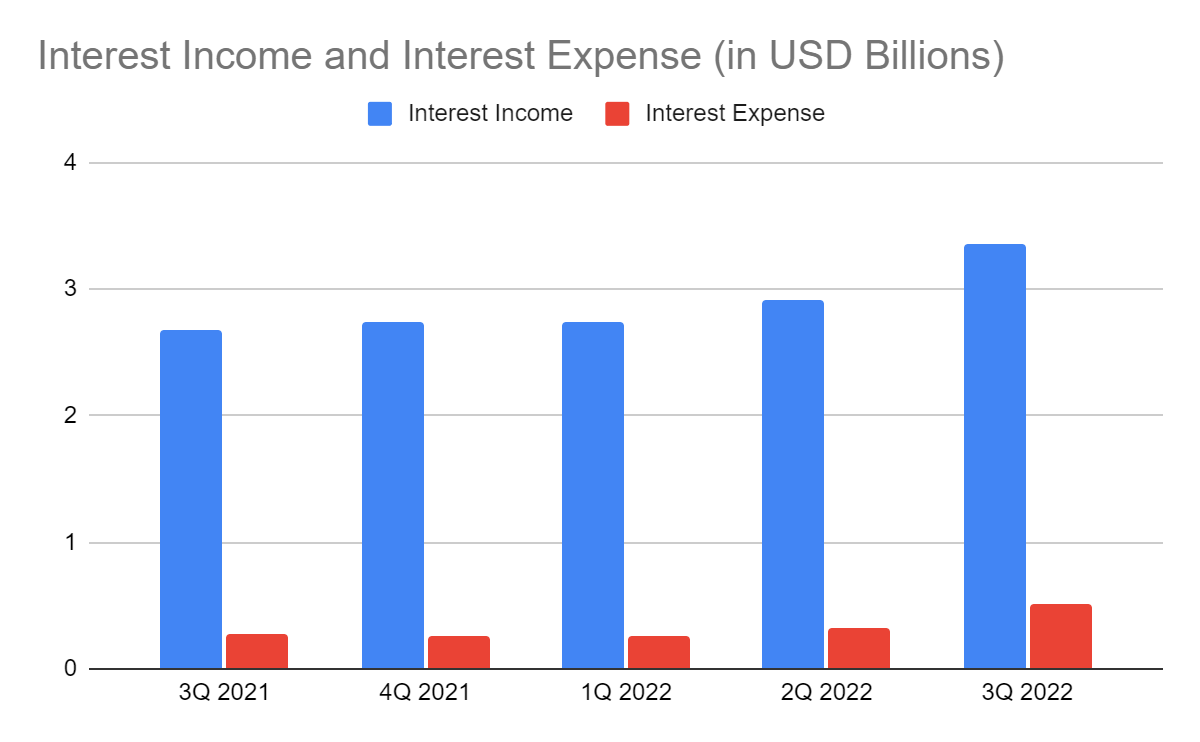

Discover Financial Services have an accumulated operating revenue of $9.02 billion. In the three quarters of 2022, it has sequentially risen substantially. The 3Q value of $3.36 billion is a 26% year-over-year increase. Various factors contributed to its massive revenue growth. The most obvious one is the impeccable loan growth. All loan components keep increasing, especially credit cards. With its increased loan and loan yields, DFS shows a robust earning-asset performance. Despite the massive increase in provisions, it shows a disciplined and conservative approach to credit management. It also shows its strength by integrating its digital banking and payments model. As such, loans are well-positioned for macroeconomic changes.

Interest Income And Interest Expense (MarketWatch)

However, other revenue components are not so impressive. Investment income shows a 22% year-over-year decrease. Although it is not a primary driver, comprising only 2% of revenues, investment securities are vital for the company. There is a notable decrease in government-backed securities and an increase in mortgage-backed securities. Treasury securities are inflation-linked so they can hedge inflationary risks and lower valuations.

Meanwhile, interest expense has an 88% year-over-year increase. It offsets the increase in interest income. It is driven by all its components, with deposit expense increasing by more than twice its previous value. Long-term borrowing interest expense is now 49% higher than it was in 3Q 2021. With their combined value, the margin is lower at 84% versus 89% in 3Q 2021. It is even lower when we take provisions into account at 62% versus 82% in 3Q 2021. What’s more noticeable here is that there is a higher increase in loans than deposits and borrowings. It shows that the current macroeconomic conditions are less advantageous for the company. The company derives fewer returns as it spends more on covering deposit and borrowing costs.

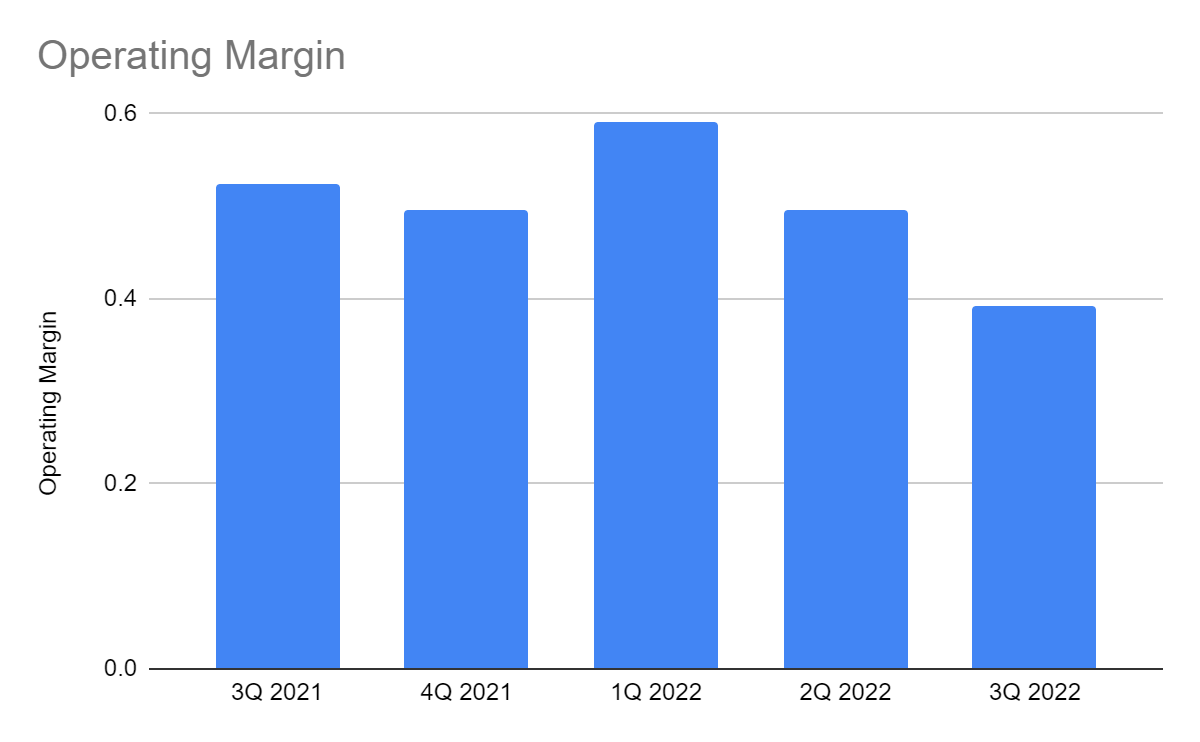

Thankfully, it continues to stabilize its non-interest segment. There is a proportionate increase between non-interest income and expense. Also, the increase in interest income offsets interest expense. Higher commissions and other transaction fees are enough to cover labor-related and equipment expenses. There is not much change in the trend. Its operating margin of 40% is still lower than 52% in 3Q 2021. But the gap in the comparative operating margin narrows from 20% to 12%. It shows a stronger non-interest segment, which helps stabilize viability.

Operating Margin (MarketWatch)

Market Risks And Opportunities

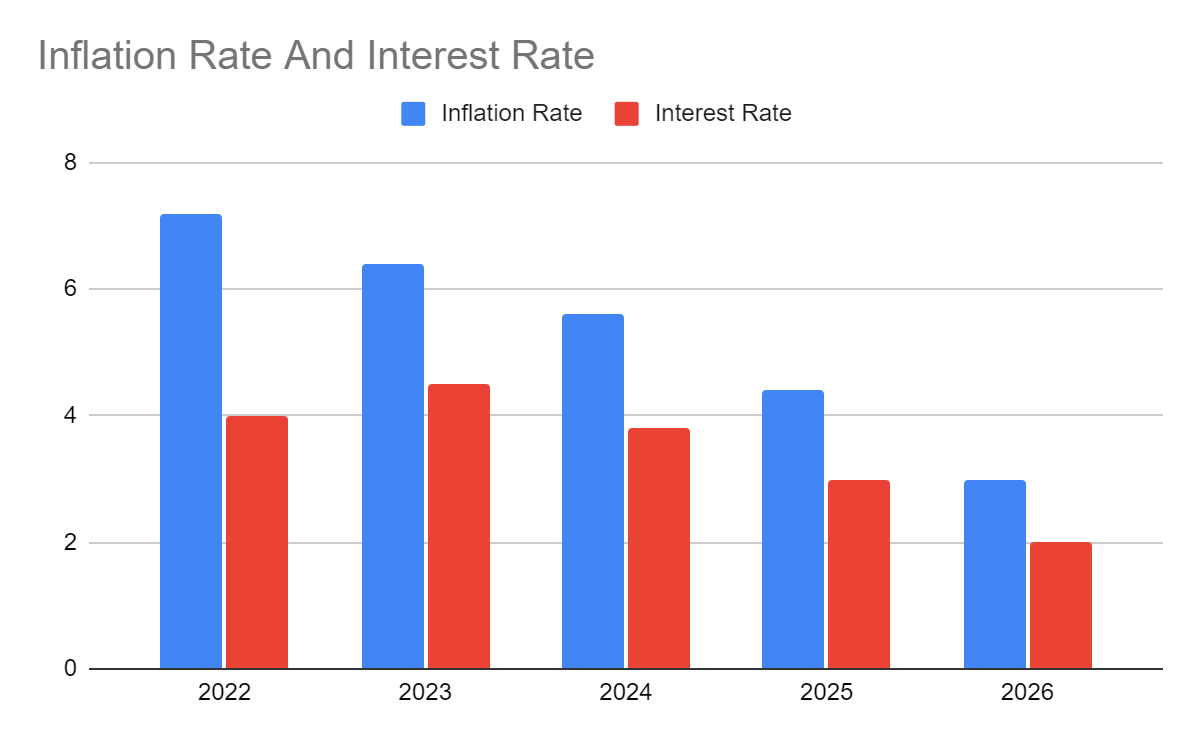

The current market conditions have a mixed impact on the company. But it is more geared toward hammered growth and viability. As such, the company must be more careful with its loan and security management and diversification. Fortunately, inflation has lulled to 7.1%, and hopefully, it is already done with its peak. But for a more conservative approach, I estimate the year-end rate at 7.2-7.4%%. Holidays lead to more spending, which can raise prices. But for the next few years, I expect it to decrease further to 5-6% before stabilizing at 3-4%. Meanwhile, I expect interest rates to keep increasing to 4-4.5%. But I still believe increments may slow down, given the decreased inflation rate. It will eventually follow the inflation downtrend, but near-term uptrends must still be anticipated. Hence, DFS must expect near-term headwinds, so growth may stay hampered in the next twelve months.

Inflation Rate And Interest Rate (Author Estimation)

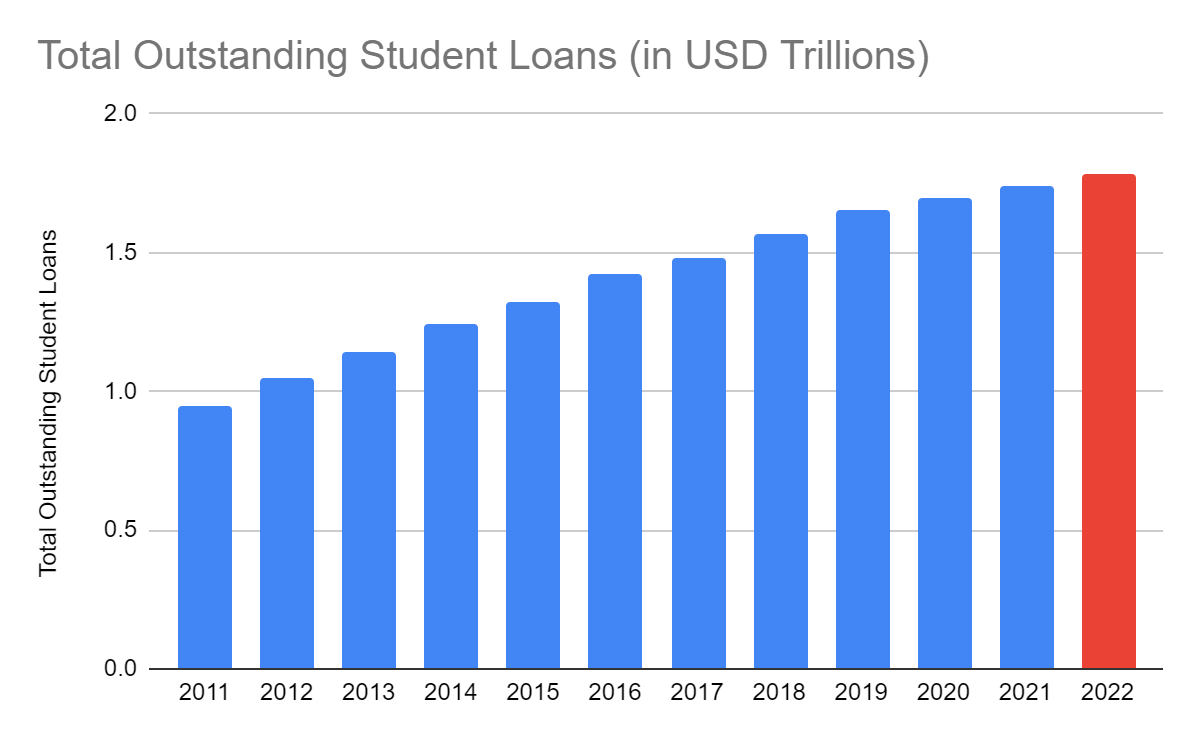

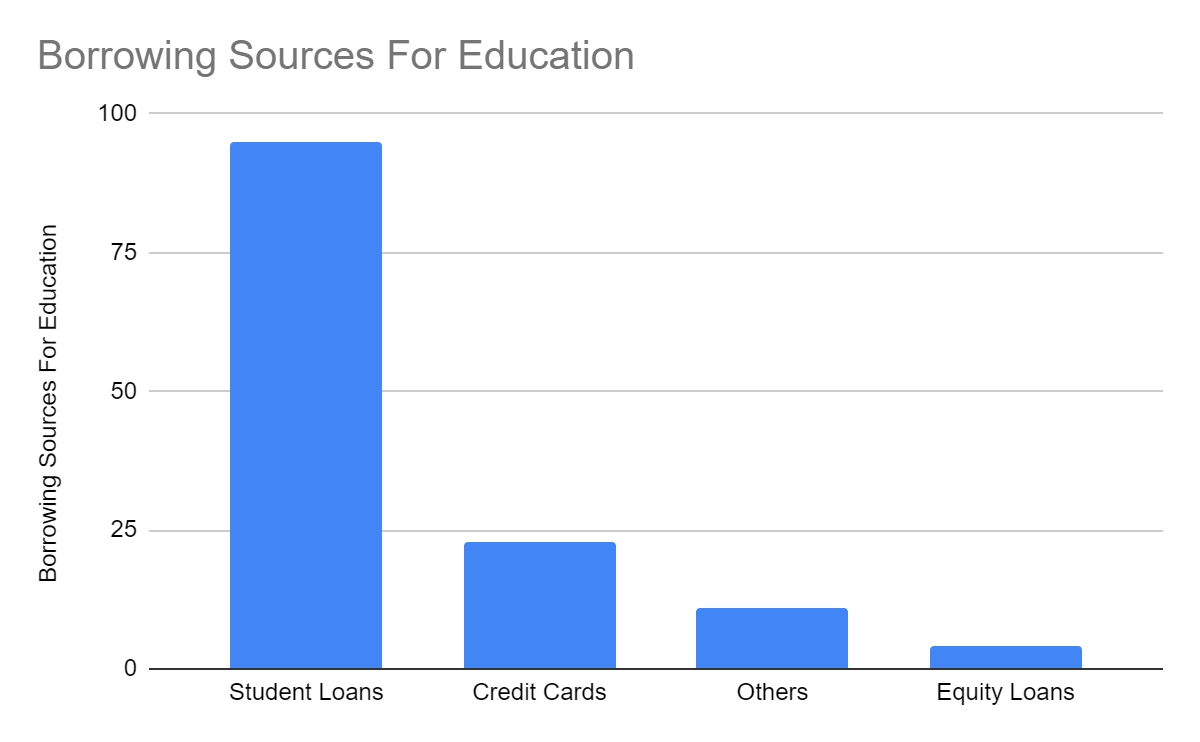

The consolation we have now is the low unemployment rate. It shows stable purchasing power and the capacity to repay borrowings. Also, student loans remain a staple for many households. It means more demand for DFS loans. Over the past decade, its value has nearly doubled. In the most recent data, student loans are already at $1.76 trillion. This year, I expect it to increase to $1.78-1.79 billion in line with the increased interest rates and school enrollment. In most households in the US, student loans and credit cards are the primary funding sources for education. That is why DFS still offers consumer value as its products help make ends meet. Amidst the higher prices, people may turn more to credit cards for their needs if income becomes inadequate. With the rising interest rates, working households may prefer credit cards over payday loans and bank borrowings. All these aspects can drive an influx of demand for the company’s products and services.

Total Outstanding Student Loans (Bankrate)

Borrowing Sources For Education (Bankrate)

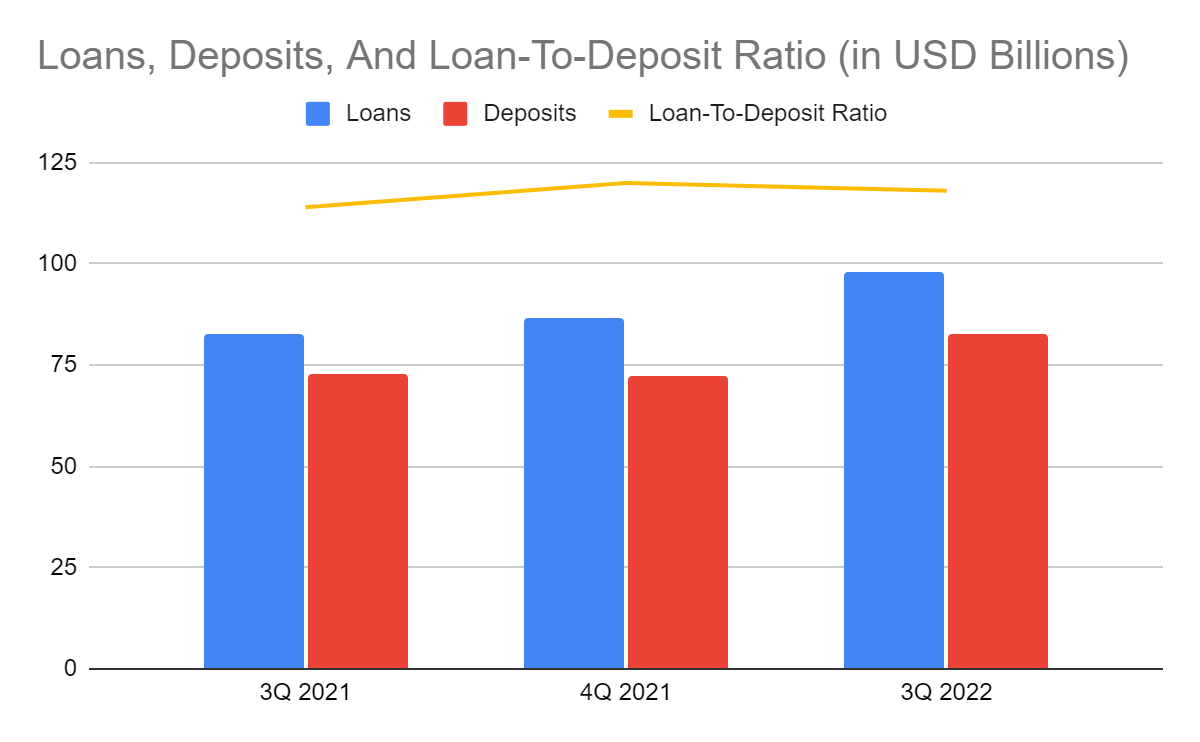

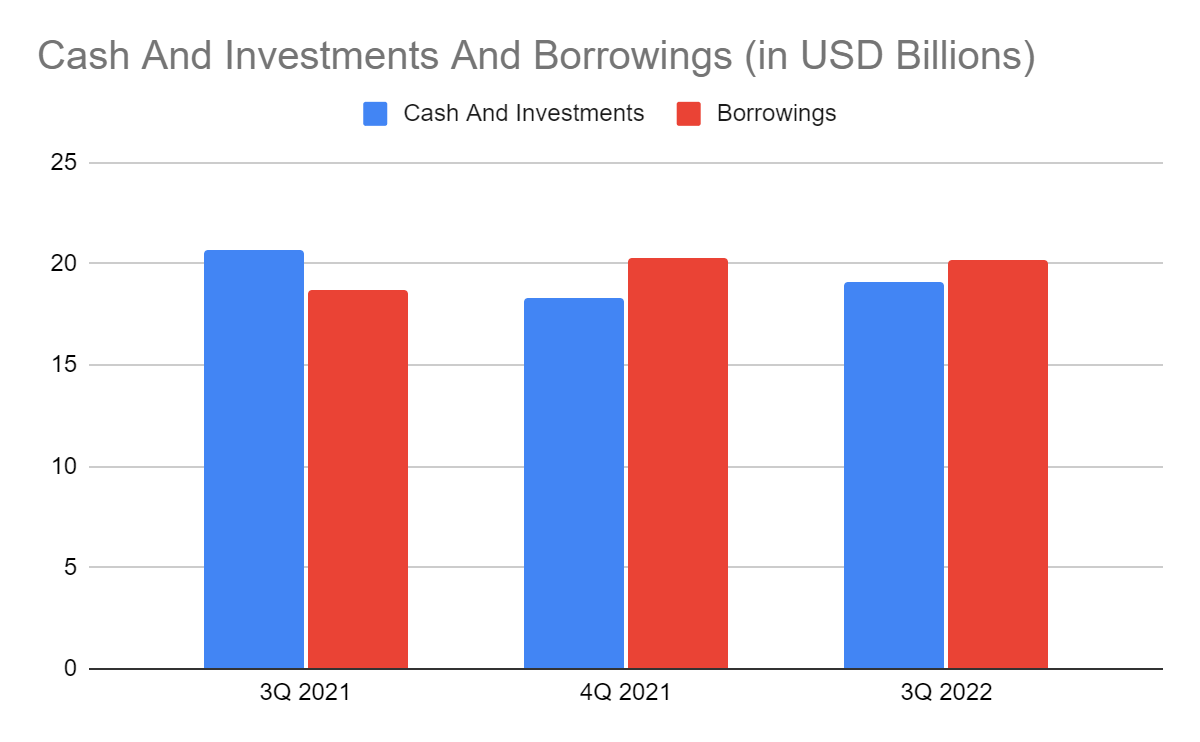

However, the company must be more careful with its liquidity. There is impressive loan growth that drives interest income. But it is way higher than deposits, leading to a loan-to-deposit ratio of 118% versus 114% in 3Q 2021. There may be limited reserves should there be defaults. It must not be too complacent as recessionary fears remain evident. Also, the fact that deposits bear more interest than loans is already a big thing. So whether the company sells a portion of loans or halts the flow of loans and deposits, margins may still be lower. Thankfully, cash continues to increase, comprising 10% of the total assets. It can support the company should there be loan defaults or higher borrowing repayments. With the potential opportunities and adequate financial capacity, DFS can bounce back once the economy becomes more stable.

Loans, Deposits, And Loan-To-Deposit Ratio (MarketWatch)

Cash And Investments And Borrowings (MarketWatch)

Stock Price Assessment

The stock price of Discover Financial Services has been in a downtrend in the last year. It has not bounced back yet but stays reasonable due to credit risk concerns. At $95.28, it has already been cut by 18% from the starting price. But it does not appear very enticing despite price metrics optimism. The price-earnings multiple of 6.2x shows an enticing stock price. If we multiply it by the NASDAQ estimate of $15.33, the target price will be $95.04. My EPS estimation of $14.72 shows a target price of $91.26. But under normal circumstances, earnings are more attractive with a PE multiple of 8-10x on average. If we use it to find the target price, the value will increase to $118-148.

However, the continued share repurchases affect the intrinsic value of the stock. In a few years, the company has cut a substantial portion of ordinary shares by buying them back. Its treasury shares are now 52% of the issued shares so only 48% are outstanding. Share repurchases have indeed fared well to counter credit risk pessimism this year. So the investor must ask how long the company can sustain this action to maintain the price level. Thankfully, DCF has high cash reserves to cover its adjustments in capital and financial leverage. With the slight economic improvement, there may be hope for an upside in its fundamental and stock performance. But right now, near-term headwinds are present, hammering its potential.

Meanwhile, dividend payments of DFS remain well-covered and consistent. It also has an attractive yield of 2.52. It is way better than the S&P 500 average of 1.70%. Even better, it only has a dividend payout ratio of 17%, so the company can cover dividends. To assess the stock price better, we will use the DCF Model

FCFF $1,299,000,000

Cash $11,900,000,000

Borrowings $20,180,000,000

Perpetual Growth Rate 4.8%

WACC 9.2%

Common Shares Outstanding 223,265,275

Stock Price $95.28

Derived Value $92.20

The derived value also conveys that the stock is not cheap despite the low PE multiple. It agrees with my EPS estimation to find the target price. There may be a 3-4% downside in the next 12-18 months.

Bottomline

Discover Financial Services experiences hammered growth in a high-inflation environment. But its efficient asset management and high cash reserves allow it to withstand the blows. It can sustain its operations, bounce back, and cover dividends. Indeed, it is still a secure stock despite the near-term headwinds. It remains a household staple, making it a durable company with promising rebound potential. However, the stock price is not a good bargain despite the enticing price metrics. With its solid fundamentals but lower target price, Discover Financial Services is a hold.

Be the first to comment