martinrlee/iStock Editorial via Getty Images

Value investors usually have to compromise in order to get rock-bottom valuations. This can be risky: sometimes you get melting ice cubes, which are usually very cheap companies where the value is shrinking. It therefore becomes a race as to whether the valuation re-rating takes place before the business shrinks to nothing, or if the company is able to provide enough share repurchases and dividends to compensate for the business erosion. One such example where we question if even Warren Buffett made a mistake investing is HP Inc. (HPQ), which is a well-run company operating a mostly declining businesses.

So what is a value investor’s dream stock? Value investors like Peter Lynch typically look for companies with strong financials, a history of steady or increasing profitability, and a competitive advantage in their industry. We believe that would be a well-run company with a rock-bottom valuation, but which is continuing to grow, has a strong balance sheet and profit margins, and competitive advantages. For obvious reasons it is difficult to get such a combination, as companies that have these characteristics usually get bid up. This is why we get very excited when we find one such opportunity. In this case we believe Deutsche Post (OTCPK:DPSGY)(OTCPK:DPSTF) is one of those rare finds. The company has good growth prospects and benefits from the e-commerce tailwinds, has a single-digit p/e ratio, has a strong balance sheet and profit margins, appears to have good management, and has very strong competitive advantages.

Company Overview

Deutsche Post DHL is a global logistics company that provides a range of services, including mail and parcel delivery, warehousing and distribution, and supply chain management. It is also a leader in the logistics industry and has a well-established brand and global network of operations. Together with (UPS) and FedEx (FDX), it is one of the worldwide leaders in package shipping.

Deutsche Post DHL Investor Presentation

Financials

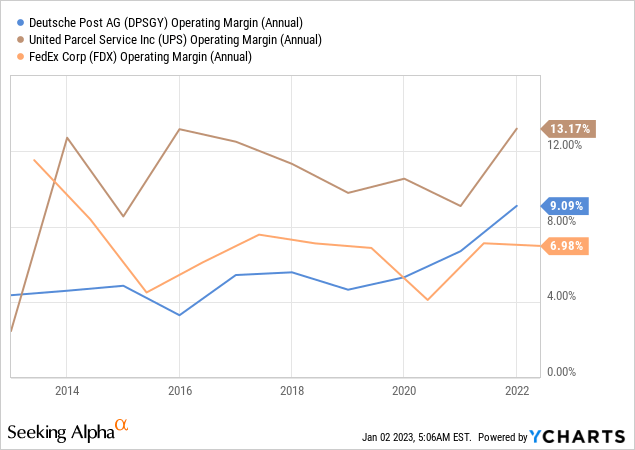

Deutsche Post DHL has strong profit margins that are getting even stronger. As can be seen below its operating margin is now ~9% for the group. This has improved from previous years and has almost doubled in the past ten years.

Unlike FedEx, which recently issued a profit warning, Deutsche Post DHL increased its 2022 EBIT and Free Cash Flow guidance based on the strong performance of the first nine months of 2022. The company is also executing on some levers to counter macro slowdown and manage external uncertainties.

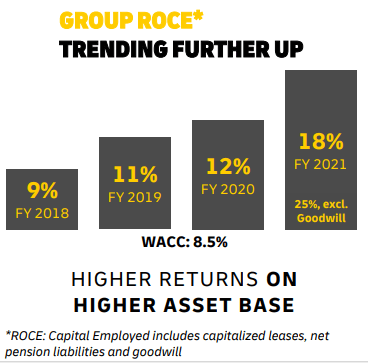

The return on capital employed for the company has been trending up in recent years and is significantly above its weighted average cost of capital. What is even more impressive is that ROCE has been going up at the same time that the company has been increasing its asset base.

Deutsche Post DHL Investor Presentation

Growth

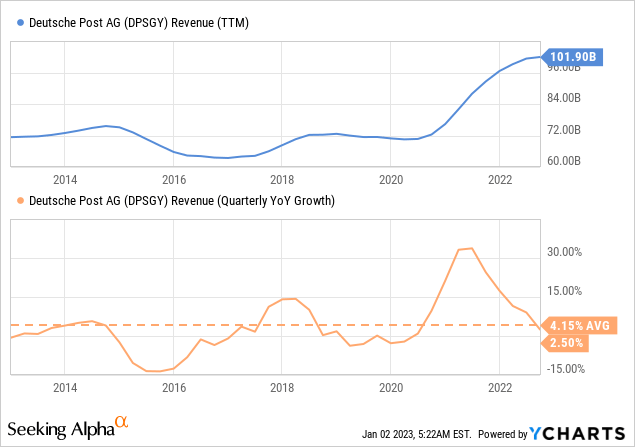

One of the few issues we find with Deutsche Post DHL as an investment idea is that prior to the Covid crisis revenue growth had been pretty anemic. The current valuation is so low that it appears some investors believe that revenue might actually revert somewhat.

While we believe the extremely high-growth the company experienced during the Covid pandemic is now gone, we think most of the gains made will stick, and the company will be able to continue growing this larger base.

One of the reasons we have this belief is that most of the company’s revenue is now tied to e-commerce. The German letter business, which seems to be the only business segment in structural decline, now accounts for only ~10% of group revenues.

Deutsche Post DHL Investor Presentation

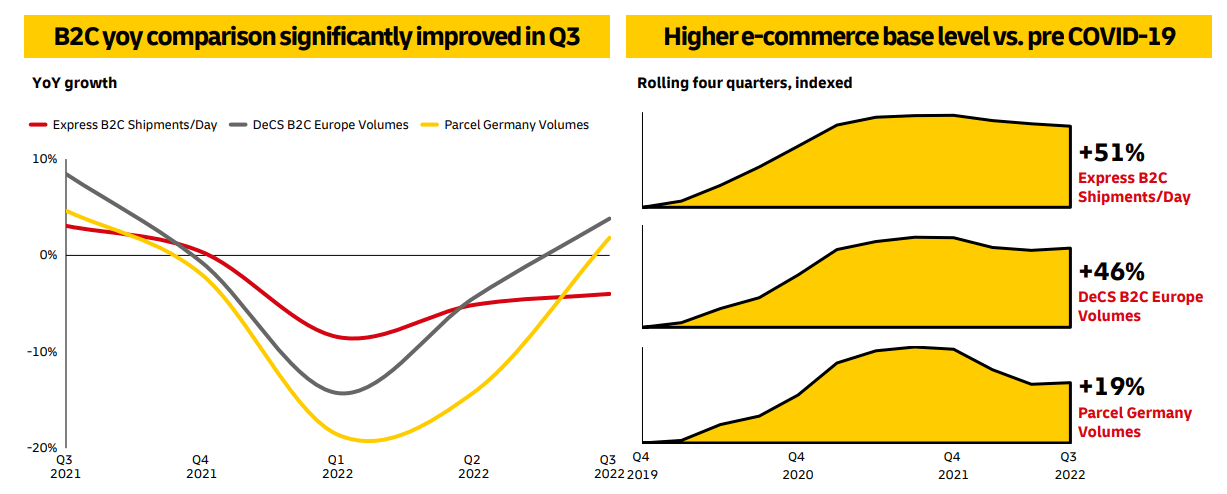

Importantly, post lock-down normalization is nearing completion for B2C and e-commerce. As can be seen in the graphs below, the higher base levels versus pre-Covid seem to be stabilizing and in some cases even growing again.

Deutsche Post DHL Investor Presentation

Competitive Advantages

In addition to being a beneficiary of structural e-commerce growth, Deutsche Post DHL has several competitive advantages. These competitive advantages include its network size and reach. Like UPS and FedEx, Deutsche Post DHL has a large global network, which allows it to offer a wide range of delivery options to its customers and reach remote locations. This network is difficult for potential competitors to replicate and creates a competitive moat for the company. Deutsche Post DHL also has a strong brand that is recognized and trusted by consumers around the world. This allows the company to charge premium prices for its services and gives it an advantage over competitors. The company has also invested heavily in technology and data analytics in order to streamline its operations and reduce costs. This has helped the company to become more efficient and competitive in the market. All of these factors have helped the company to become a leading player in the global logistics market.

Balance Sheet

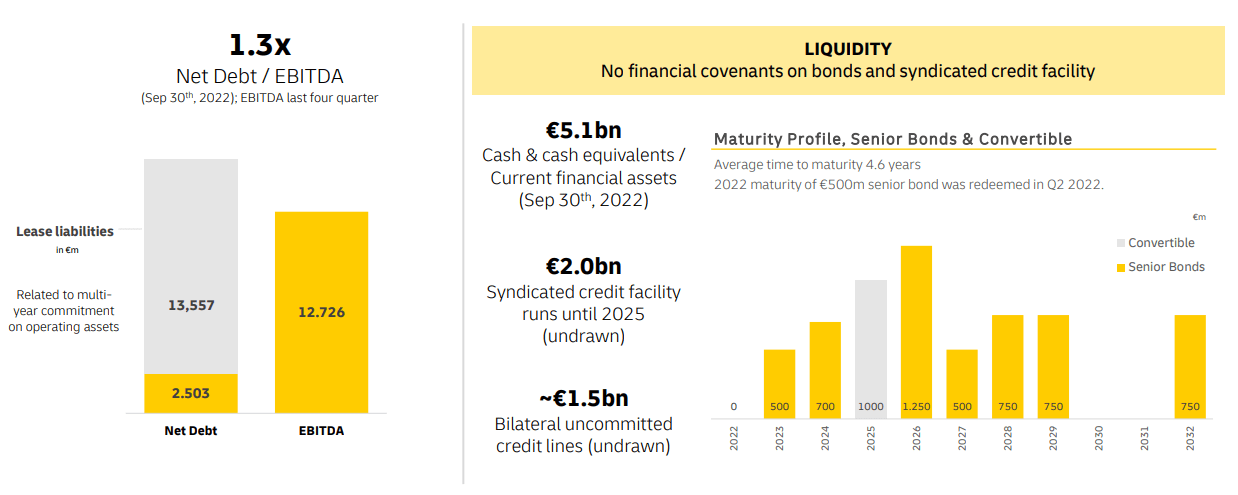

The company has a strong balance sheet and liquidity position, with net debt/EBITDA at only ~1.3x. There are no financial covenants on its bonds and credit facility, and the company has a massive €5.1 billion in cash and short-term investments. The average time to maturity is 4.6 years, which means the company is relatively well protected in the short term from the rising interest rate environment and gives the company plenty of time to refinance its debt.

Deutsche Post DHL Investor Presentation

Guidance

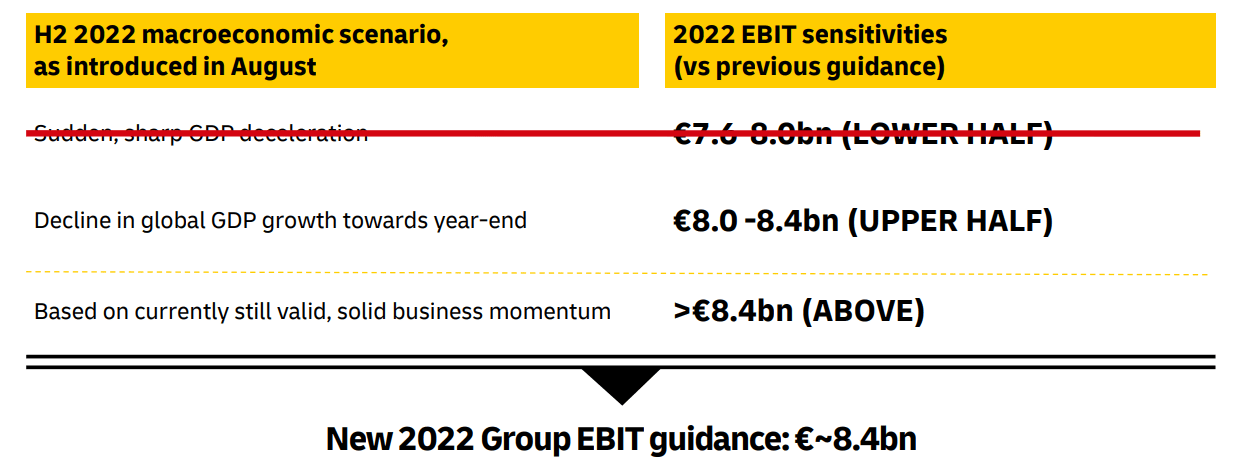

The company is guiding 2022 group EBIT to €~8.4 billion based on the solid performance it delivered in the first nine months of 2022. Given the macro-economic weakness, and the fact that competitors like FedEx issued profit warnings, we believe this guidance is very reassuring. It also shows that the company is confident that the normalization post-pandemic is almost complete, and the company can go back to growing again.

Deutsche Post DHL Investor Presentation

Valuation

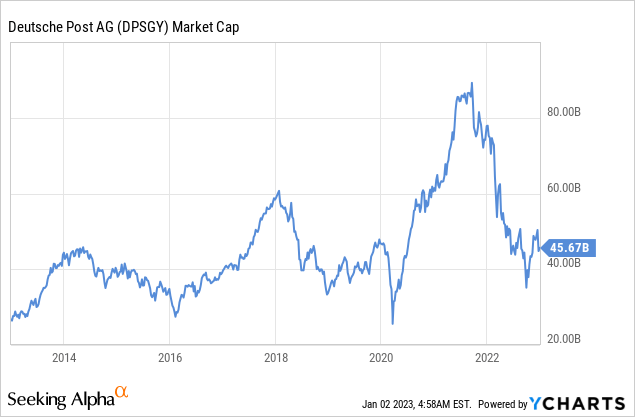

Given that the company is trading with a market cap of ~$45 billion, and that it has given EBIT guidance of €~8.4 billion for 2022, which is roughly $9 billion, it means the company is trading at a very low valuation of ~5x 2022 expected EBIT.

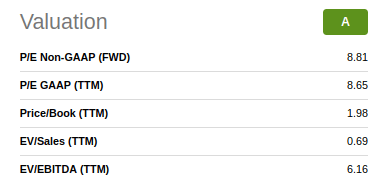

It is no surprise then that Seeking Alpha gives the company an ‘A’ valuation grade. EV/EBITDA is only ~6x.

Seeking Alpha

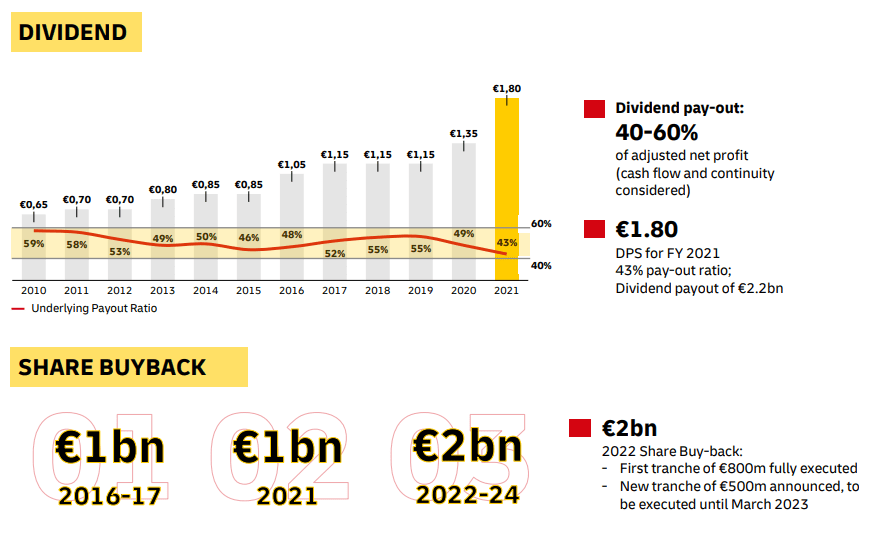

Importantly, the company shares these earnings with shareholders in the form of dividends and share buybacks. At current prices shares are yielding a little over 5%, and the payout ratio remains at a very reasonable level.

Deutsche Post DHL Investor Presentation

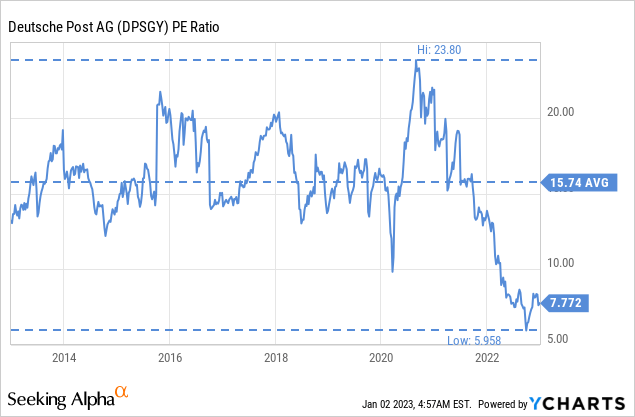

Compared to its historical valuation, shares are quite cheap. Its ten year average p/e ratio is ~15x, and currently shares can be bought for roughly half that multiple.

Risks

Shares are trading as if the company was going to give back some of the revenue gains it made recently. Given that it is showing signs of stabilization we believe it is going to retain much of the gains made, and that it will soon start growing again thanks to the e-commerce tailwind. One threat we believe is worth keeping an eye on is Amazon Logistics (AMZN), as they are quickly becoming one of the main players in the shipping of packages, even if most of these packages are their own. We believe these risks are mitigated by the company’s strong balance sheet and competitive advantages.

Conclusion

Deutsche Post DHL is a value investor’s dream stock in that it is trading at a bargain valuation but is not a melting ice cube. The company still has very good growth prospects thanks to the e-commerce tailwind and global GDP growth. In addition, the company appears to have good management and very strong competitive advantages. It is rare for a company with so many positive attributes to be trading at such a discounted valuation. There is fear that the company will give back some of the revenue gains it recently made, but revenue seems to be stabilizing already and in some areas is already starting to grow again from this higher base. We believe investors should give this company serious consideration, as it appears to be a wonderful business trading at a wonderful price, even if growth moderates in the future.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment