ryasick

Markets continue to fall and trailing yields continue to rise. The inverse relationship, in theory, presents yield-hungry investors with enhanced opportunity. The challenge, as always, is whether to believe that what’s rising in the rear-view mirror will translate to hard cash in your account.

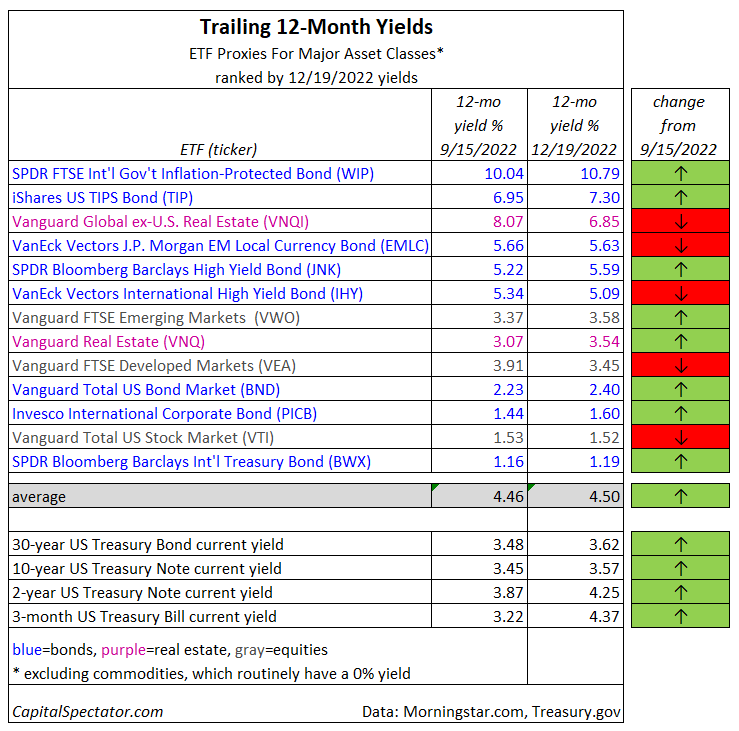

Confidence in the answer varies, depending on the market and fund. Most trailing yields have increased this year for the major asset classes, based on a set of ETF proxies. Deciding if those higher payouts are the genuine article on an ex ante basis requires careful analysis. But as a first approximation, it’s useful to stack up the latest yields and compare the changes in recent history. On that point, payout rates remain relatively attractive.

The average yield for the major asset classes ticked up to 4.50%, based on trailing data through Dec. 19, according to data from Morningstar.com. That’s slightly above the average for our previous update in mid-September. The change is far more dramatic vs. the year-ago average of 2.82%.

The highest-yielding market at the moment: 10.8% via government inflation-indexed bonds ex-US, based on SPDR FTSE International Government Inflation-Protected Bond ETF (WIP).

That’s a starkly compelling payout vs. the competition. It’s also attractive vs. inflation, at least from a US perspective. Consumer inflation rose roughly 7% over the past year through November and so WIP’s trailing one-year yield delivered a nearly 4 percentage points real premium.

Nice, but there are caveats to consider, including capital loss. WIP’s payout is alluring, but keep in mind that the ETF lost more than 13% over the past 12 months.

There are no free lunches in the desperate search for yield. Risk management, in short, is still required. Diversifying across asset classes can help. Studying the payout history of a given fund, and guesstimating the future path for interest rates and other macro factors, is also recommended. Rethinking the role of cash, and its rising yield, as an asset class deserves to be on the short list too. In addition, buying individual Treasuries, including the inflation-indexed variety, has appeal these days for locking in higher real and/or nominal yields.

The key question, of course, is whether yields have peaked. No one knows, which is why allocating some of your portfolios to cash may be tactically smart. The future’s still uncertain, which implies that hedging your bets is timely: rebalancing in favor of higher-yielding assets while holding cash to exploit the possibility of even higher yields down the road. The expected return for such a strategy is open for debate, but as a tool to reliably earn average/above-average results vs. the competition through time it’s probably the only game in town.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment