Ekaterina79

Is it too early to start putting together our 2023 Christmas wish list?

You probably already know my thoughts on the subject, and not just because I asked the question to begin with. I’m a very big proponent of keeping a catalogue of what you want to buy: stocks that would be stellar to own, but only at the right price.

When they do hit the right price, it can feel like Christmas Day any day of the year.

In which case, 2022 was a great year for at least some real estate investment trust investors. Particularly the new ones or those who were looking to add to their portfolios.

There were a lot of great REITs on sale.

A lot of them.

This did make it rather frustrating for anyone already holding these positions – the ones who were content with their portions. They could at least console themselves that:

- A paper loss is not an actual loss. (we just published on that topic at iREIT on Alpha)

- They still got reliable dividends along the way.

But still. Nobody likes to see their portfolio value decline in any sense of the word. In which case, 2022 was disappointing for the REIT sector.

I touched on this recently in my “REIT Roadmap: How to Navigate REITs in 2023.” Published exclusively on iREIT on Alpha, it goes sector by sector, evaluating each with the future in mind.

Surprisingly, there’s a lot of positive to see. If you only know where to look.

The “Naughty” Side of REITs

Here’s just a little snippet of this year’s “REIT Roadmap” – a part that’s acknowledging the unfortunate obvious about 2022:

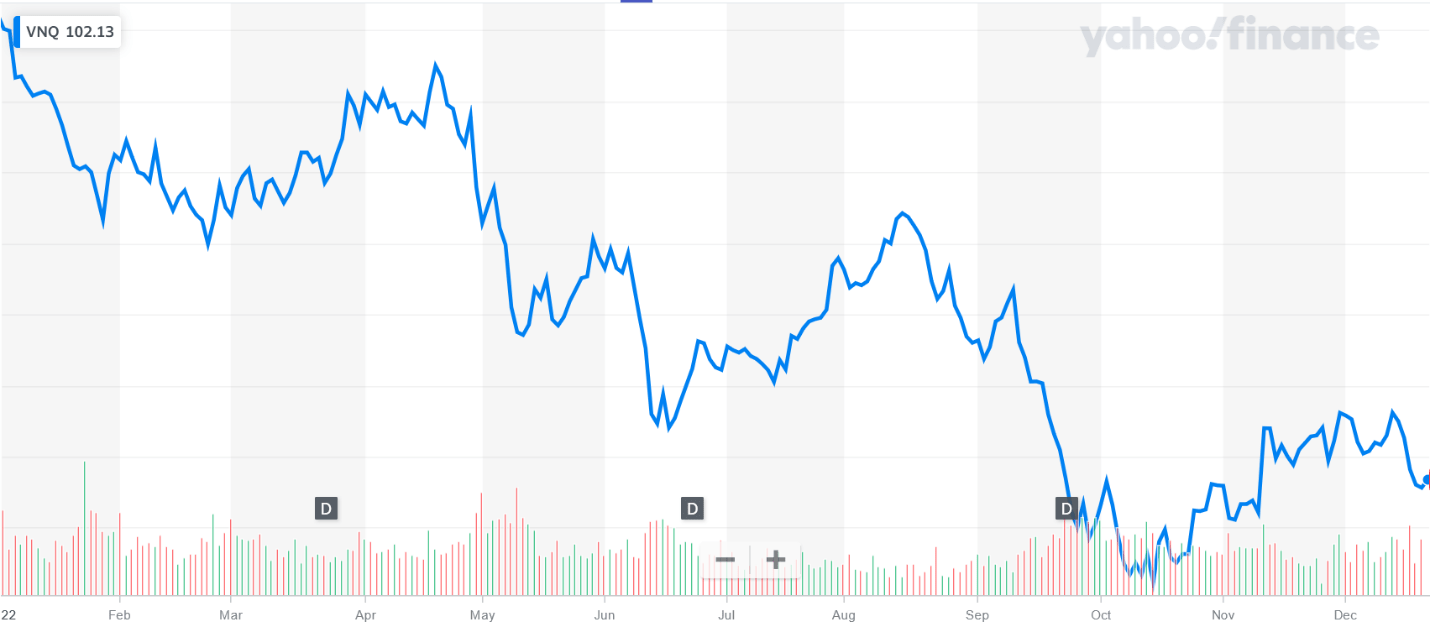

“As for REITs specifically, here’s a chart of the Vanguard Real Estate Fund (VNQ), which can serve as a basic REIT index.”

Yahoo Finance

“As of December 21, it was down 26.73% year-to-date. Which makes it an even worse performer than the larger real estate category. And I doubt the last few days of 2022 can change that.

So what do we expect in 2023? Could it be any better?

We ultimately have to wait and see, of course. But I do have some insights I want to share.”

It’s a very, very long report with an enormous amount of information in it. But one insight is how the pandemic changed a lot about our “normal,” take-for-granted lives.

Look no further than New York City-specific REIT SL Green (SLG) for proof of that. It had to slash its dividend a few weeks ago, as reported by Zacks Equity Research:

“SLG recently announced a cut in its annual ordinary dividend payment on its common stock and units of its operating partnership from $3.73 per share to $3.25. This marks a reduction of 12.9%…

This move comes as part of the company’s efforts to match its present estimation of funds available for distribution (FAD) for 2023, which is $221.3 million. This permits SLG to balance out between the yield on its common stock, and its liquidity forecast of nearly $1.6 billion, and its target to lower its combined debt by almost $2.4 billion in 2023.”

Who would have seen that coming four years ago?

Yet as I also mention in my “Roadmap,” real estate remains “a commodity with limited supply and long-lasting demand. And REITs are still an important part of that pie.”

Santa Isn’t Real, but REITs Are (And That’s Good Enough for Me)

The truth is that time changes things, sometimes in small ways, sometimes more drastically. I’m reminded of that every time I see my grandson, Asher.

This was his first Christmas, and man how he’s growing up. I remember the first time I saw him: how small, innocent, and helpless he was.

Today, he’s still small – though pounds bigger and inches taller. And he’s still innocent – though developing quite the personality with the clear ability to let you know when he is and isn’t pleased. And he’s still helpless – though getting stronger and more independent all the same.

Before I know it, he’ll be walking. Then talking. Then going off to school for his first day of kindergarten.

Not that I’ll share those thoughts with his mom. Something tells me she doesn’t want to hear a bit of it right now… even though it’s going to happen one way or the other.

Which is an overall good thing!

Those changes will eventually take him off to college, then into the business world. It will take him into relationships and eventually down the aisle to have a family of his own.

Life brings transformations and alterations, and it’s our job to find the best path forward regardless.

That’s true about aging – even when we learn that Santa isn’t real and our presents aren’t magically brought to us from the North Pole. Once we learn that, we start learning about where those presents do come from…

How we can benefit from those presents further than mere passing fun…

And how much better presents can get as we grow further.

By that, of course, I mean in the investment field with REITs like the following…

2 Sweet REIT Treats

Realty Income (O) is my largest holding and I’m still buying.

Shares are down 10% year-to-date, but that’s actually not too shabby, when compared to the Vanguard Real Estate ETF that’s fallen by over 28% YTD.

Looking back over five years, Realty shares are up over 19%, compared to VNQ that has broken even.

I consider Realty a “set and forget” pick and over the last ten years I have been accumulating shares whenever Mr. Market provides me with that window of opportunity.

I never get too fixated on a stock’s share price, at least when I’m analyzing the quality of the business. My primary research is rooted in corporate earnings – or in the case of REITs, Adjusted Funds From Operations (‘AFFO’).

One of the impressive things about Realty is that the company has generated positive earnings in 25 out of 26 years (as a public company). The only negative year of earnings growth EVER was in 2009 – during the Great Recession.

I wasn’t surprised to see Realty grow earnings during Covid-19.

Keep in mind, the primary reason I’m overweight Realty is because I know the company is built like a fortress and it can plow through most any economic cycle, including a global pandemic.

The two most important levers for a REIT are its scale and cost of capital advantages, and over the decades I have witnessed the evolution of Realty’s business model – enhancing its balance sheet to generate more stable and predictable rental revenue.

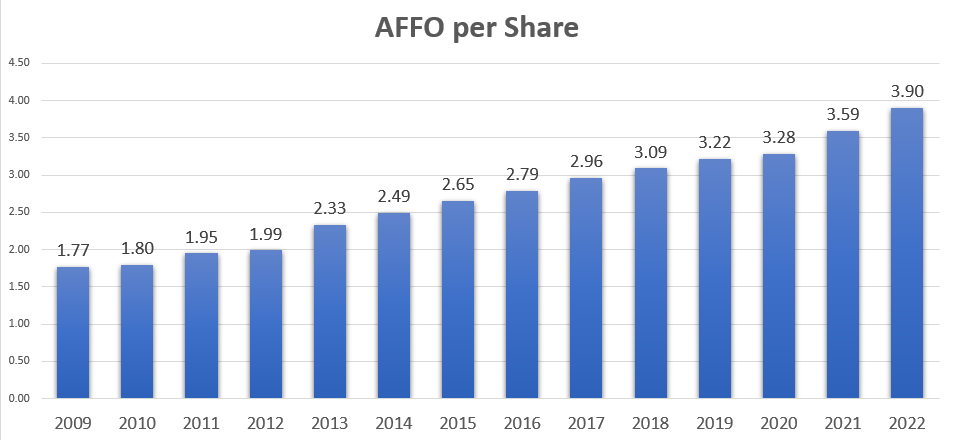

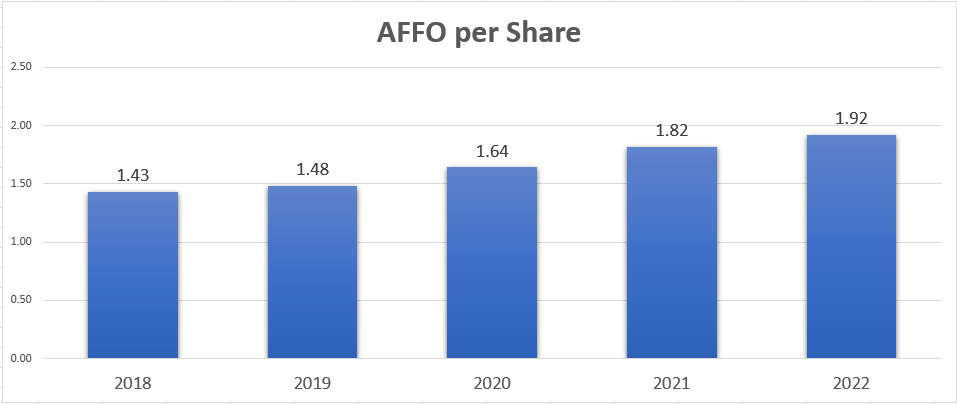

Speaking of stability, just look at the company’s earnings stream over the last 14 years:

iREIT on Alpha

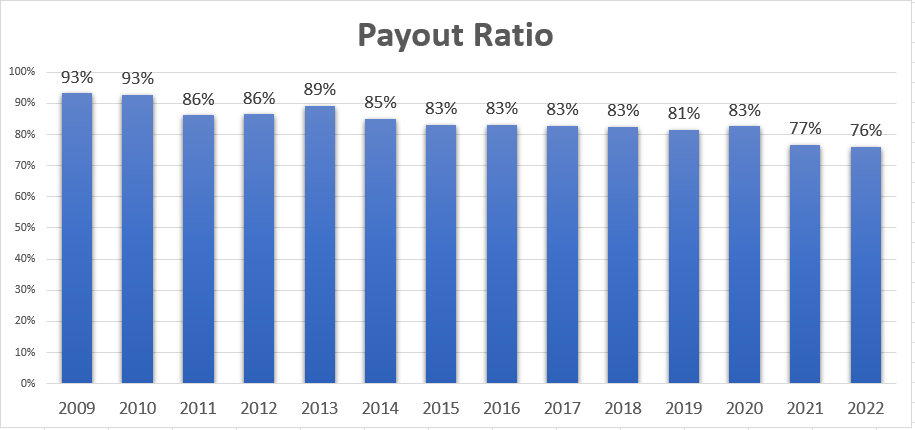

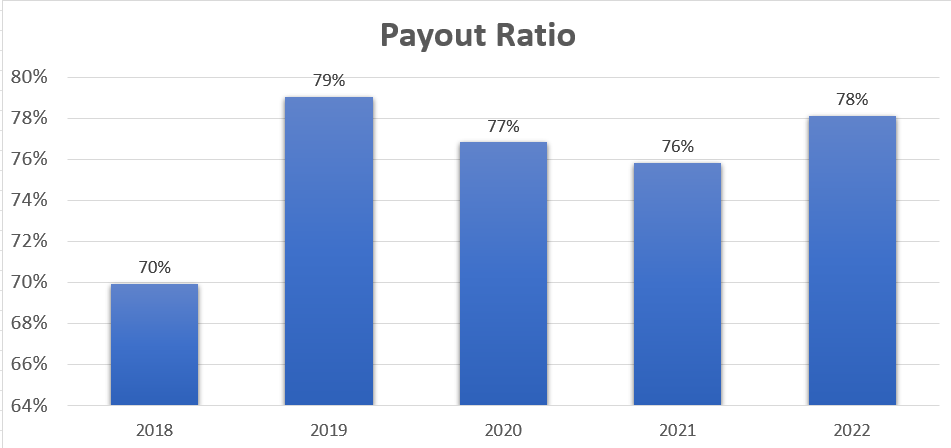

As you can see, AFFO has increased by an average of 6.3% over the last 14 years, and impressively the company has also reduced its payout ratio, which means that the dividend is much safer.

iREIT on Alpha

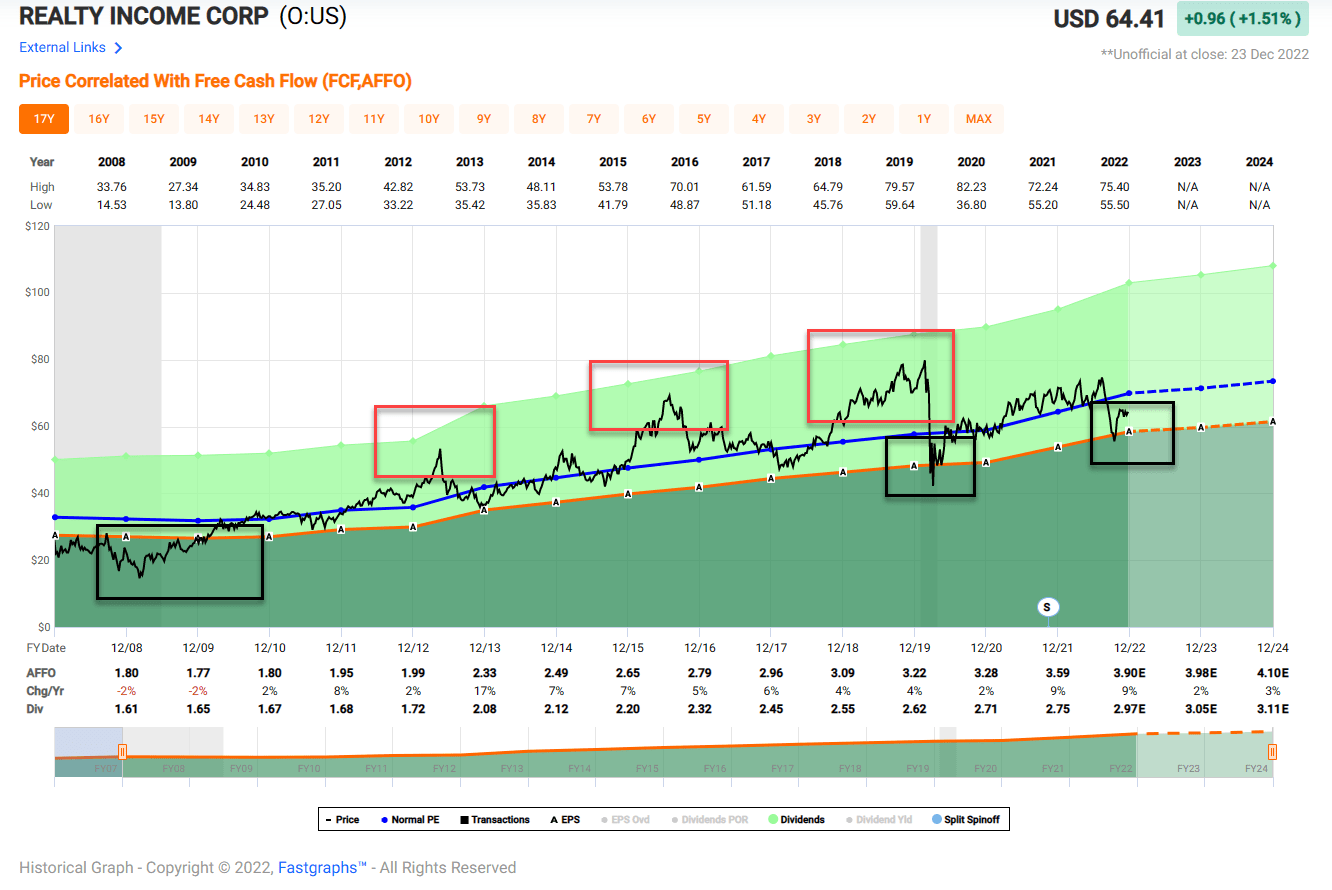

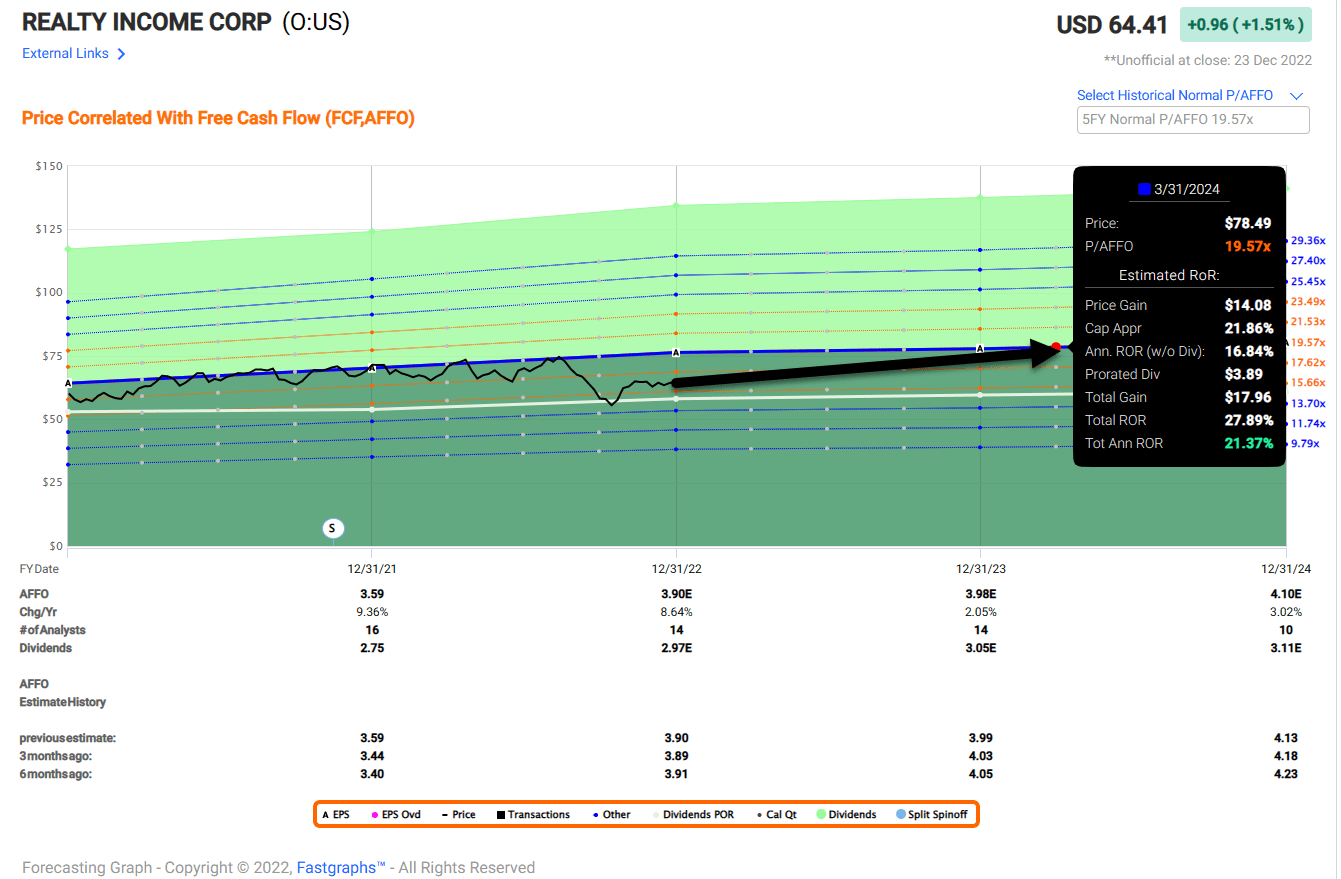

As you can see below, Realty is now trading with a margin of safety – current priced at $64.41 with a P/AFFO of 16.5x. Looking back over the last 15 years, the average multiple was 18x. The dividend yield is 4.6% and while growth estimates for 2023 are just 2%, we consider the valuation attractive.

FAST Graphs

Realty recently closed on the Boston Encore casino property in Boston and this suggests the company could pursue additional gaming assets in the US and Europe. In addition, we would not be surprised to see the company pursue a sale-leaseback with Six Flags (SIX) or possibly other experiential investments.

We also consider Spirit Realty (SRC) a prime-time takeover target and Realty is the most likely buyer in our opinion. And at the current valuation level, Realty investors have very attractive upside – we’re modeling shares to return ~20% over 12 months.

FAST Graphs

VICI Properties (VICI) is my #1 REIT pick in 2022.

Shares are up over 8% year-to-date and this gaming REIT has been hitting all-cylinders.

During the pandemic I took the opportunity to increase my stake in VICI, recognizing that the shutdown would not impact the company’s ability to collect rent.

While market sentiment was negative for most of 2020, VICI collected 100% of its rents and began to consolidate the sector. In April 2022, the company acquired MGM Growth Properties (formerly MGP) for $17.2 billion and since that time it announced several other strategic deals:

- Invests $127M to indoor water parks operator Great Wolf Resorts for the development of a project in Texas.

- Acquires Rocky Gap casino for $204M

- Enters funding agreement for up to $200M to fund the development of Canyon Ranch’s wellness-resort offering in Austin, Texas.

- Agreed to buyout Blackstone’s (BX) 49.9% interest in the MGM Grand Las Vegas and the Mandalay Bay Resort for $5.5B (assuming $3B in debt).

- Entered into sale-leaseback with Hard Rock International, as part of Hard Rock’s acquisition of the operations of the Mirage Hotel & Casino, it said Monday.

- Acquired two hotels and casino properties in Mississippi for a total price of $293.4M from Foundation Gaming & Entertainment.

In other words, VICI has been extremely active, and the company does not appear to be slowing down anytime soon. Since formation (in 2017) VICI has executed ~$30bn of investments and raised ~$20bn of equity proceeds and was added to the S&P 500 Index in record time (June 2022).

I don’t think any other REIT has listed and appeared in the S&P in just 5 years.

Although VICI doesn’t have the “Dividend Aristocrat” status as Realty Income, the company has generated very impressive earnings in five years (as seen below):

iREIT on Alpha

That chart (above) represents average earnings (AFFO per share) growth of 7.7% over 5 years, while VICI has maintained a stable payout ratio – as viewed below:

iREIT on Alpha

Impressively, VICI has maintained exceptional occupancy and we consider many of the investments “mission critical” in that the licenses are critical to the operation of casinos. Many of the properties owned by VICI provide that gaming regulators require gross gaming revenue reporting from the underlying assets.

Also, 47% of VICI’s rent roll have CPI-linked escalation for 2022E with 96% of CPI-linked escalation by 2035E. Also, VICI has the lowest exposure to G&A costs among the net lease REIT peers – 2% G&A as a % of Revenue on a Q3’22 LTM Basis.

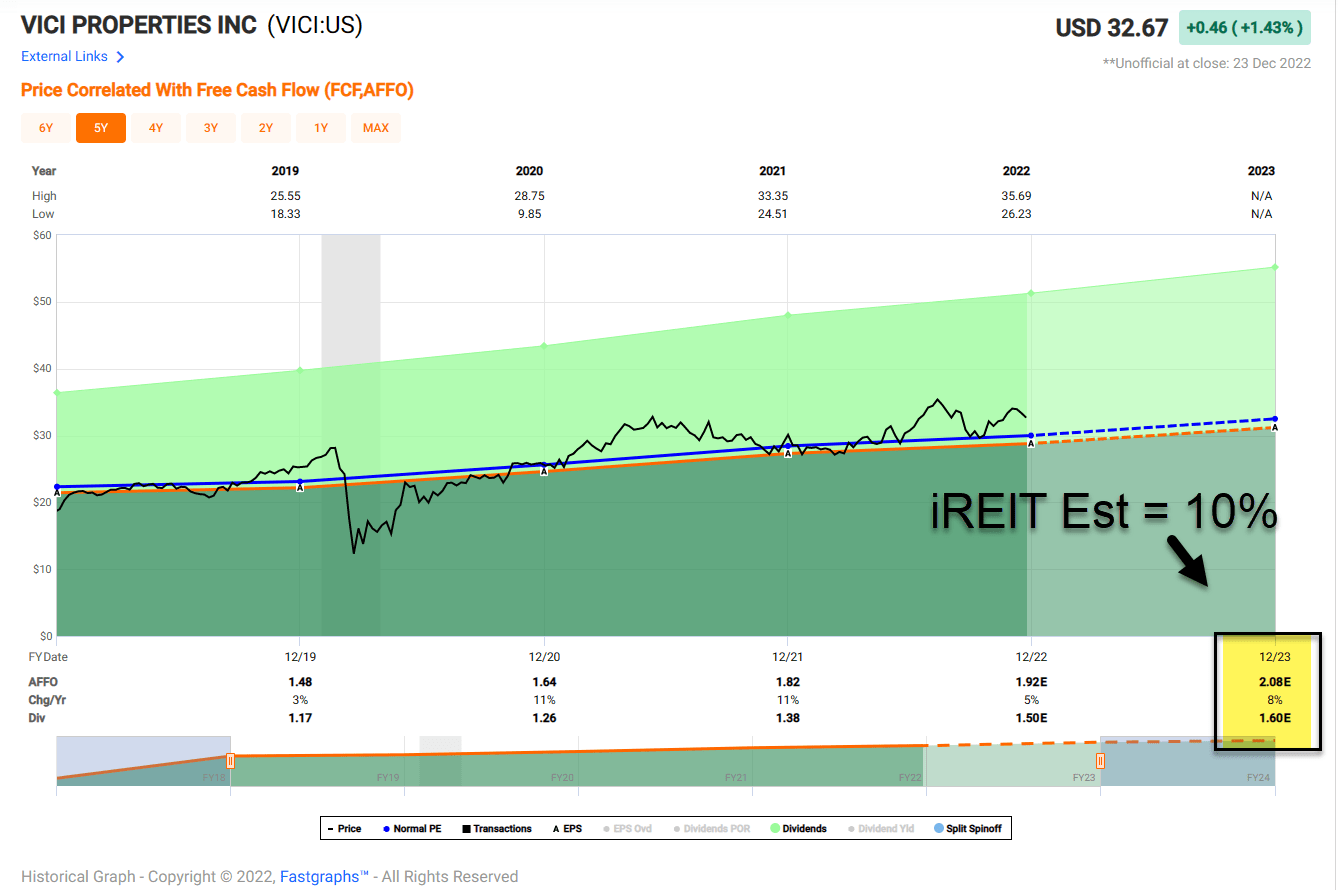

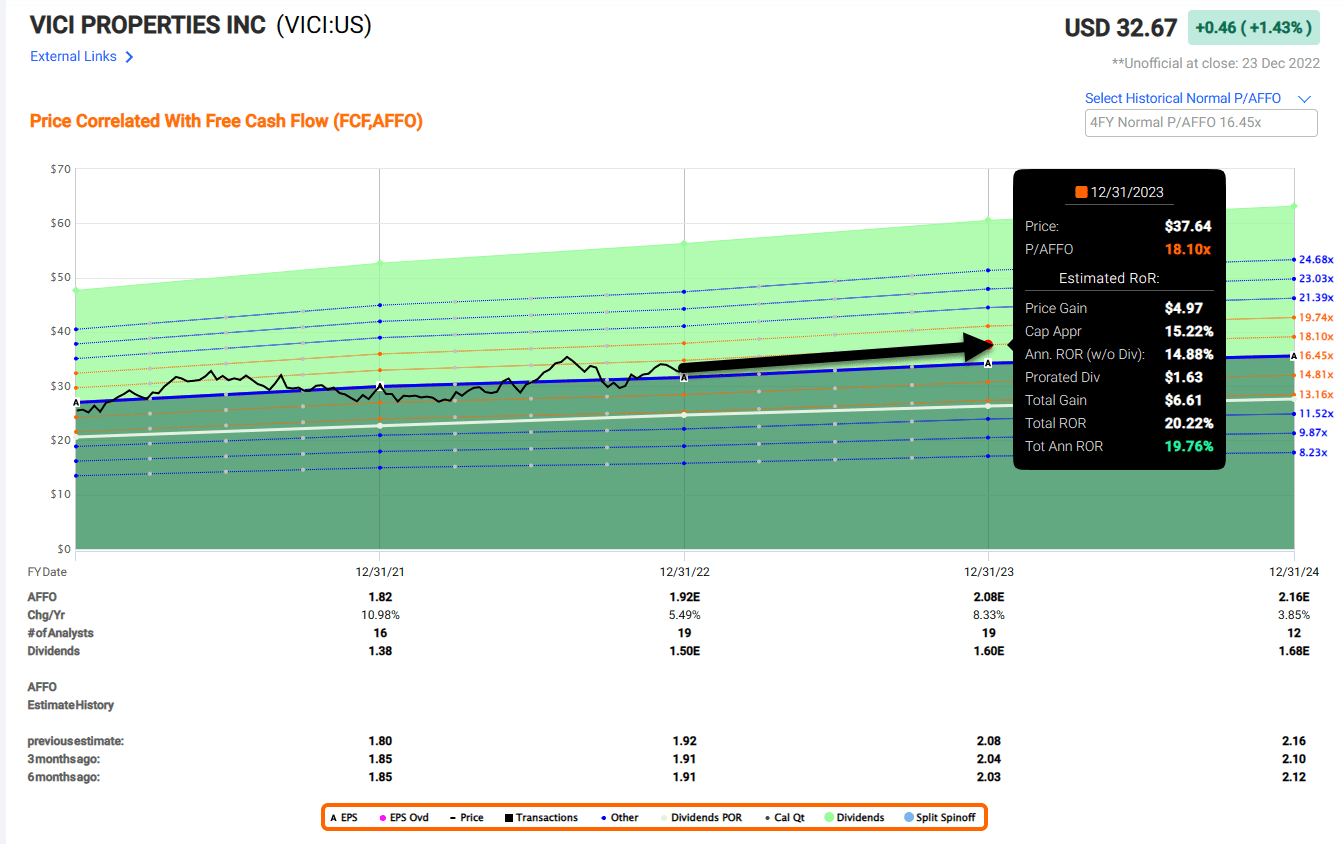

Even though VICI shares outperformed most REITs in 2022, we believe shares remain relatively attractive – trading at $32.67 with a P/AFFO multiple of 17.0x. Especially given the tremendous growth prospects for VICI – we believe the company could be the fastest growing net lease peer in 2023.

FAST Graphs

Much like Realty Income, we consider VICI a “consolidator” that will be able to grow earnings both internally and externally. VICI’s powerful CPI-linked leases provide steady organic growth, while the super-charged acquisitions generate added alpha.

I credit VICI’s management team for delivering on its promise and we suspect the company will enter Europe sooner than later. The dividend yield is a safe 4.8% and we forecast shares to return 20% over the next 12 months.

FAST Graphs

Thank You

I want to conclude my holiday-inspired article with a special word of thanks.

Over the last decade or so, all of you have inspired me to push harder, and to deliver top-notch research.

One of the great things about writing on Seeking Alpha is the feedback and friendships created.

You have challenged me to seek out excellence as my daily routines are inspired by your remarks, criticisms, and kind words.

All of you are gifts and whether we agree or not on a particular stock, this platform reinforces my belief that “the most durable education is self-education”.

I wish you all a safe, healthy, and prosperous holiday.

Merry Christmas and happy SWAN investing!

Be the first to comment