The CSX Corporation (NASDAQ:CSX) is one of the few dividend growth stocks that I absolutely love yet don’t own. That is solely based on the fact that I own three railroads already and my need for a somewhat higher yield, which is based on tax reasons. My most recent bullish article covering this Class I railroad was written back in October when the broader stock market sell-off presented new opportunities. The stock is up roughly 11% since then.

Fast forward to January 2023, we’re dealing with high recession risks. That’s bad news for everyone expecting to generate capital gains in the quarters ahead. However, it is likely to present new buying opportunities when it comes to dividend growth stocks like CSX.

I strongly believe the stock is poised to move lower as the economic growth outlook becomes increasingly cloudy.

However, the economic upswing that follows will be good. I expect CSX to benefit from rebounding economic growth on top of secular tailwinds like economic re-shoring and secular growth in energy and agriculture.

In other words, it looks like we get one more dip before CSX investors get to crush the market again.

Now, let me walk you through my thoughts and explain how I would deal with CSX.

2022 Wasn’t Half Bad

Headquartered in Jacksonville, Florida, CSX is the second-largest publicly traded American Class I railroad. With its peer Norfolk Southern (NSC), it services every economic hub and supply chain in the East. After buying the much smaller Pan Am Railroad last year, it also has exposure in Massachusetts, New Hampshire, Vermont, and Maine.

CSX Corp.

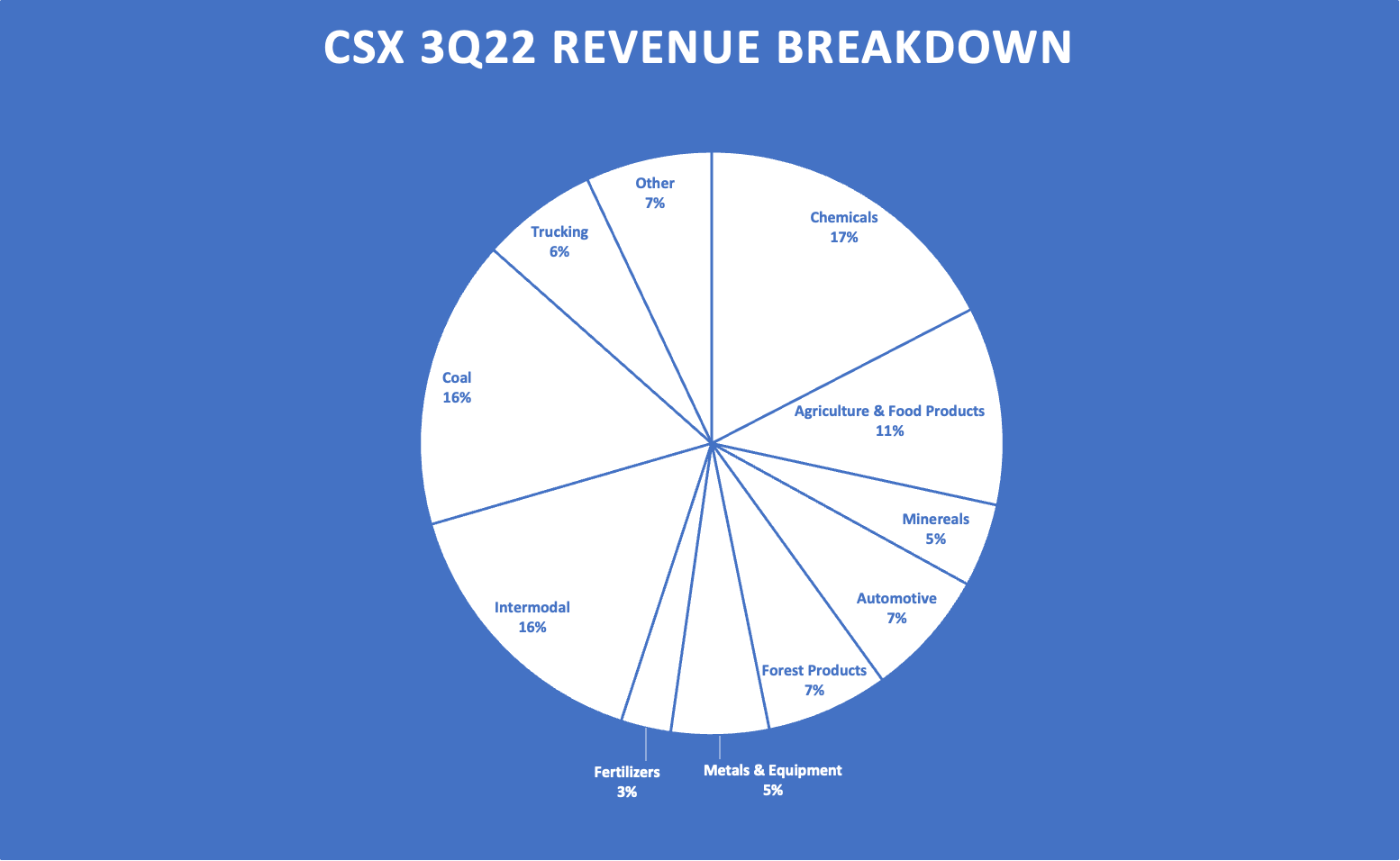

While its peer Norfolk Southern has a huge intermodal footprint, CSX is well-diversified. The company’s biggest revenue segments are chemicals, intermodal, and coal. While many are somewhat “scared” of high coal exposure, I think it’s nothing to worry about. While domestic coal demand is steadily declining, the company benefits from strong pricing and high export demand. While a global recession will damage coal demand, the shift in energy fundamentals, like lasting natural gas shortages in Europe and Asia, will keep a floor under coal demand. Moreover, the long-term decline in coal demand is slow enough to allow the company to diversify. It has done this very successfully over the past few decades.

Author (CSX Corp. Data)

This is what the company commented on coal during its 3Q22 earnings call on October 20:

So optimistic on the production side. There’s clearly a need when you look at the utility coal mines are the utilities that we serve, particularly in the South. They have a lot of inventories; they need to replenish and so we anticipate a lot more consistent deliveries over the next year to really replenish those levels and we continue to see the export market very, very strong and a lot of geopolitical risk out there in Europe and other areas where you probably didn’t see as much demand a year ago, continue to have a lot of demand.

So far, CSX has done a tremendous job in 2022 dealing with operating issues like the surge in post-pandemic demand, which required accelerating hiring efforts and new equipment. In the first three quarters of 2022, the company grew total revenue by 22% with growth in every single segment but fertilizers (1% contraction).

This was mainly due to pricing, including fuel surcharges as total volumes were flat in the first three quarters of 2022.

Unfortunately, railroads (in general) were dealing with high growth in operating expenses. In 3Q22, the operating expenses of CSX grew 25%. This caused operating income to grow by just 10%, despite 18% sales growth.

As a result, the operating ratio (often referred to as “OR”) rose to 59.9%, one of the highest numbers in years.

On a full-year basis, the company expects to deliver double-digit revenue and operating growth.

According to the company:

While there is uncertainty in the global economy, we feel confident in our ability to deliver on this guidance as we look over the remainder of this year. As we mentioned in our earlier remarks, we are pleased with the positive momentum in our service metrics. And we continue our hiring and training efforts to ensure that we have the resources needed to build on these trends and drive improved network fluidity.

Moreover, CSX continues to benefit from demand growth in agriculture, coal, and automotive, as more than 100,000 vehicles are waiting for transportation. This also supports pricing.

With that said, investors are forward-looking, which is bad news for the CSX share price.

2023 Might Be Worse

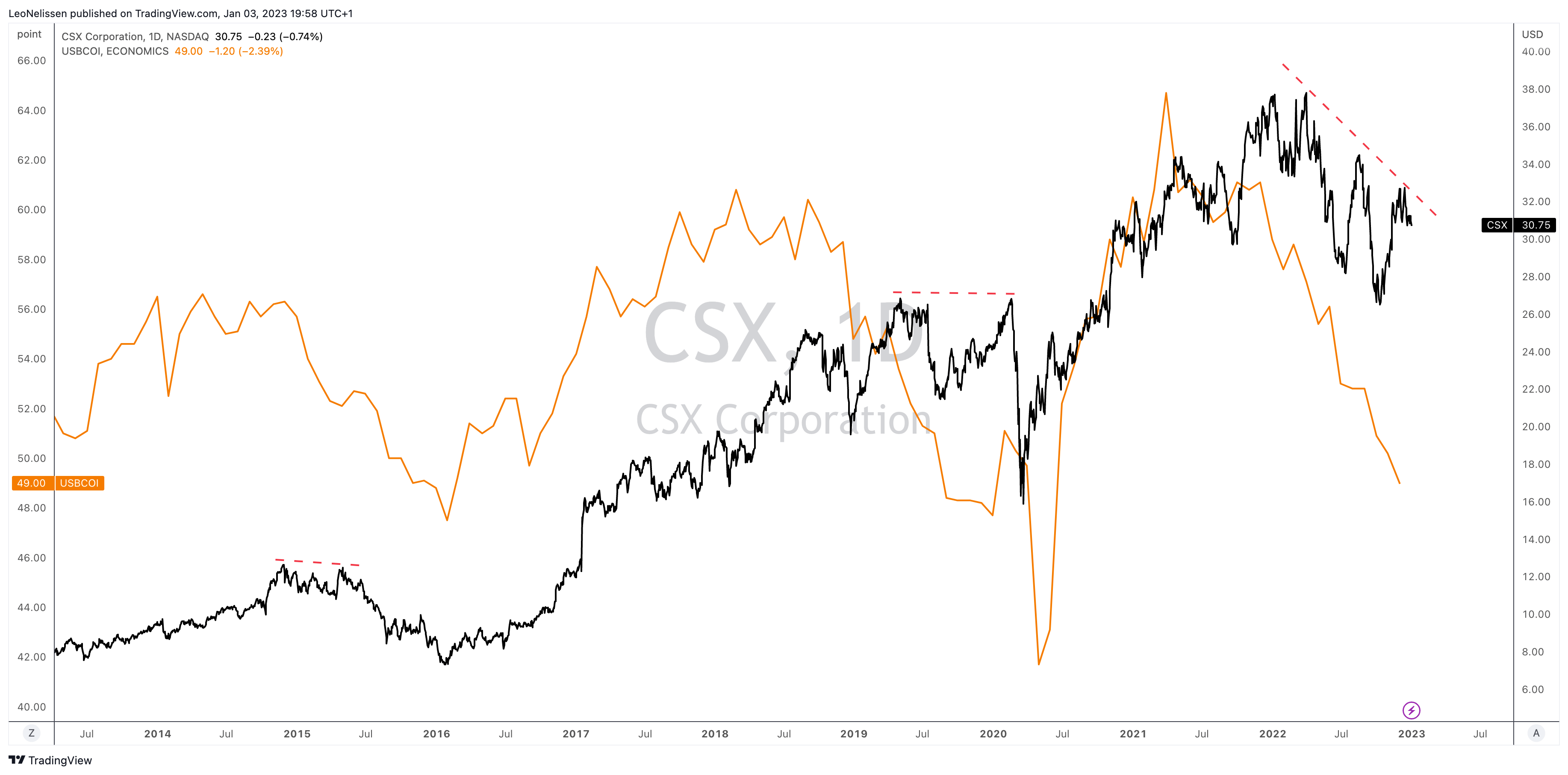

Looking at the chart below, we see that CSX is being dragged down by leading economic indicators. In this case, it’s the ISM Manufacturing Index, which is once again in contraction territory. Just like in 2015 and 2018, cyclical stocks are rolling over, with a high likelihood of more weakness in the months ahead.

TradingView (CSX, ISM Index)

In a recent article, I made the case that a recession is likely. Based on a few bullet points, I explained that the Federal Reserve might have to be more hawkish and faster to fight persistent inflation.

The Fed is feeling tremendous pressure to control inflation. That makes sense as the US economy is consumer-driven. Also, high inflation can quickly turn into lasting above-average inflation once wages and spending habits adjust. That’s a no-go!

Hence, I believe that the Fed will not be afraid to do damage to the US economy to achieve its target of lower inflation. This includes hurting housing demand/prices, unemployment, and consumer spending.

Once the Fed pivots (I still believe it will happen in 2023), the economy will slowly adjust to lower rates. Demand will come back. So will inflation.

Given the aforementioned secular factors, I believe we are in a prolonged period of Fed hikes and cuts at above-average rates (versus 2009-2021).

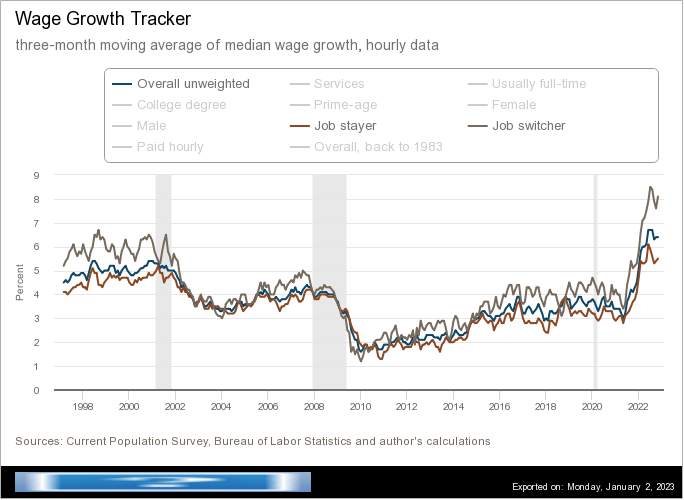

It also doesn’t help that wage inflation remains very persistent.

Faster wage growth is contributing to historically high inflation, as some companies pass along price increases to compensate for their increased labor costs. Prices rose at their fastest pace in 40 years earlier in 2022. Inflation has cooled in recent months but remains high. Federal Reserve officials are closely monitoring wage gains as they consider future interest-rate increases to slow the economy and bring down inflation.

Federal Reserve Bank of Atlanta

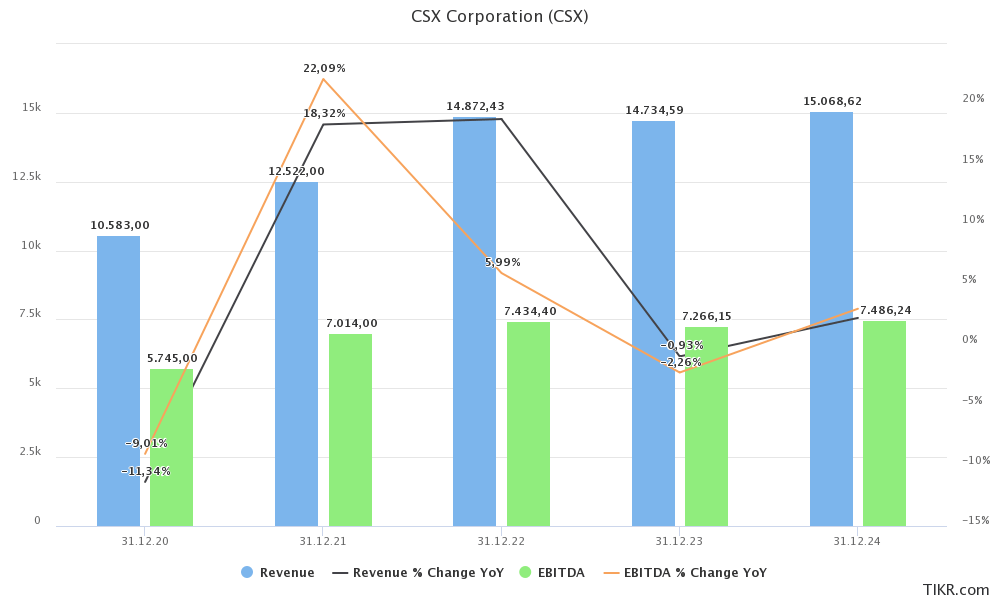

Since October, analyst estimates have come down consistently. In October of 2022, 2023 EPS was expected to come in a penny shy of $2.00. Now, that number is $1.88. Looking at the chart below, 2023 revenues are now expected to decline by 1%, indicating weak volume growth and diminishing pricing power. Adjusted EBITDA is expected to decline by slightly more than 2%. I expect both of these estimates to worsen in the months ahead.

TIKR.com

I also expect the market to drop towards 3,300 points (S&P 500). I think that CSX could retest its lows close to $26.

While that is bad for existing shareholders who cannot stand stock price weakness, I think it’s a terrific opportunity for investors looking to buy (more) CSX shares.

A New CSX Stock Price Decline Offers Opportunities

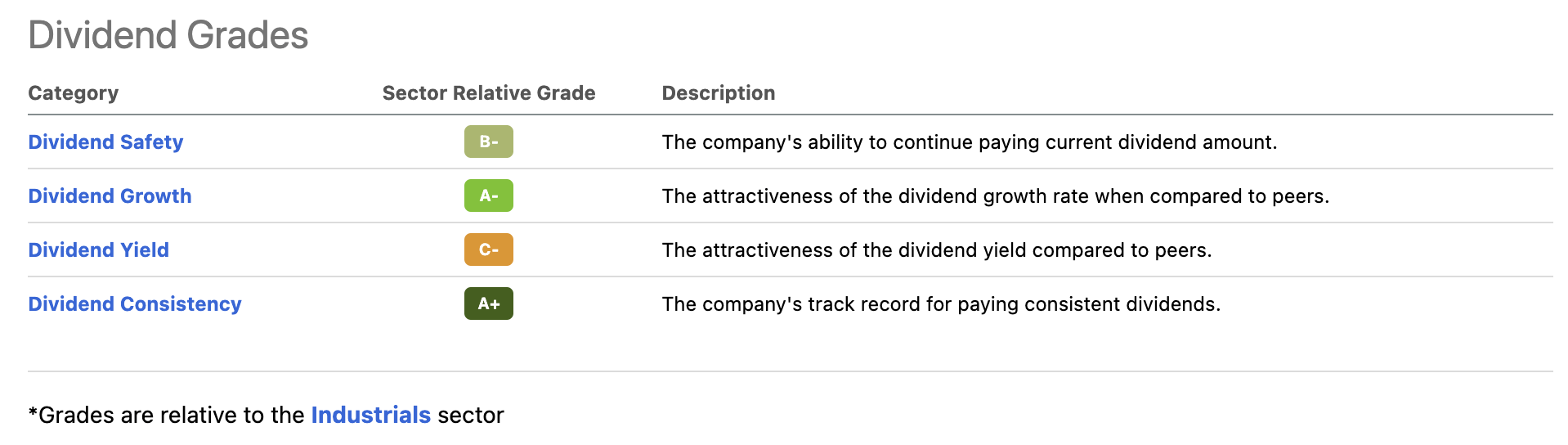

Whenever I discuss dividend growth stocks with a low yield, I get complaints from people who believe that a low yield is a waste of money and time. CSX is in that low-yield category, as it scores low when it comes to comparing its yield to the sector median in the Seeking Alpha dividend scorecard below.

Seeking Alpha

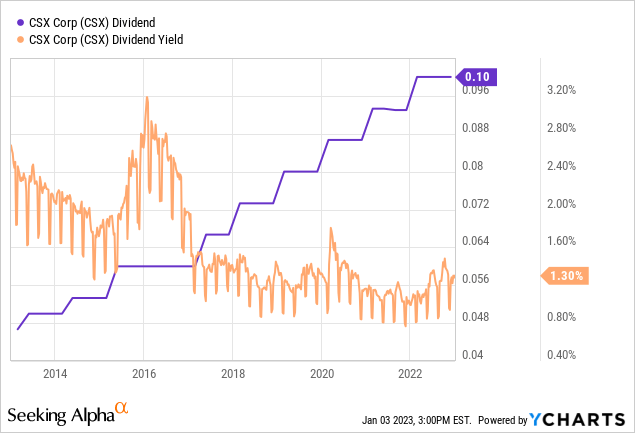

The company currently pays a $0.10 per share per quarter dividend. That translates to $0.40 per year or 1.3% of the current stock price.

There’s no denying that 1.3% is a low yield.

However, there are (at least) four good reasons to still go with CSX.

1. Dividend growth is satisfying

Over the past ten years, the average annual dividend growth rate was 8.3%. That number has risen to 9.0% over the past three years.

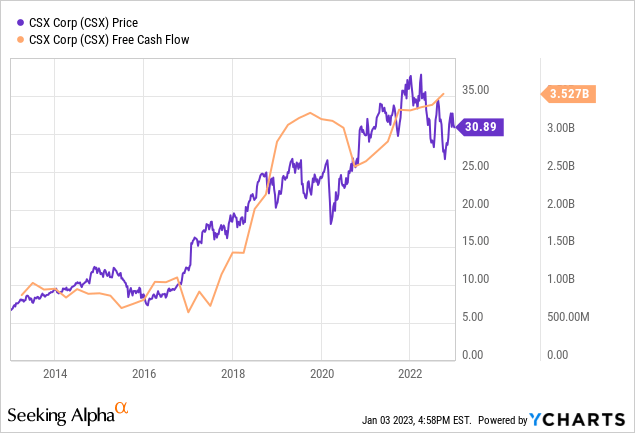

These growth numbers are supported by 16.2% annual compounding free cash flow growth in the 2012-2024E period, which is caused by volume growth, higher operating efficiencies, and strong pricing.

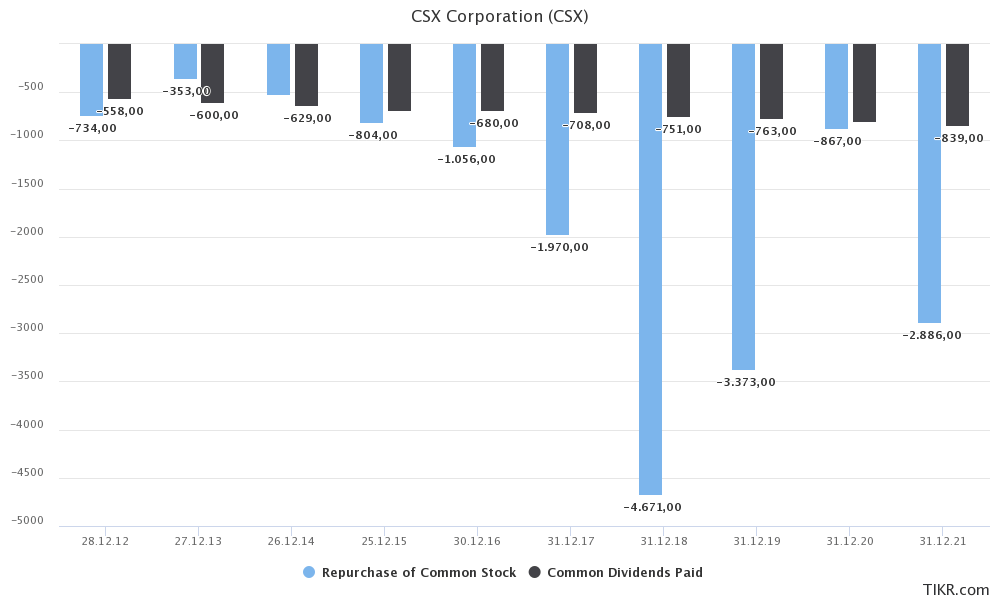

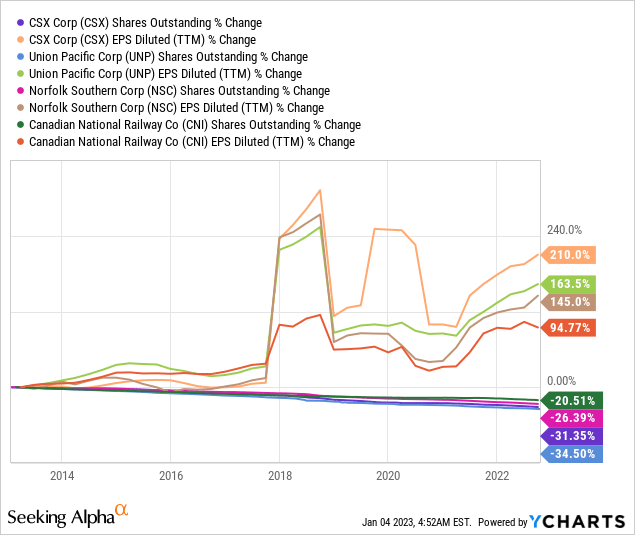

While buybacks are common among Class I railroads, CSX usually takes it to another level as it prioritizes buybacks over dividends. Especially in strong years, the company spends billions on buying back its own shares. Buybacks used to be tax-free. Now they are taxed at 1%, which still makes them a very attractive way to distribute cash to shareholders. However, these distributions are indirect as cash does not end up in shareholders’ pockets. Buybacks lower the share count, which increases the value per existing share.

As the overview below shows, buybacks often exceed dividends. In tough economic years like 2020, buybacks are dialed down. However, as soon as revenue growth improves, buybacks accelerate again.

TIKR.com

Over the past ten years, only Union Pacific (UNP) was able to buy back more shares than CSX. However, CSX outperformed all peers when it comes to earnings PER SHARE growth, which includes buybacks and its ability to grow organically. Please note that I excluded Canadian Pacific (CP) as it has a much higher share count as a result of the pending Kansas City Southern acquisition.

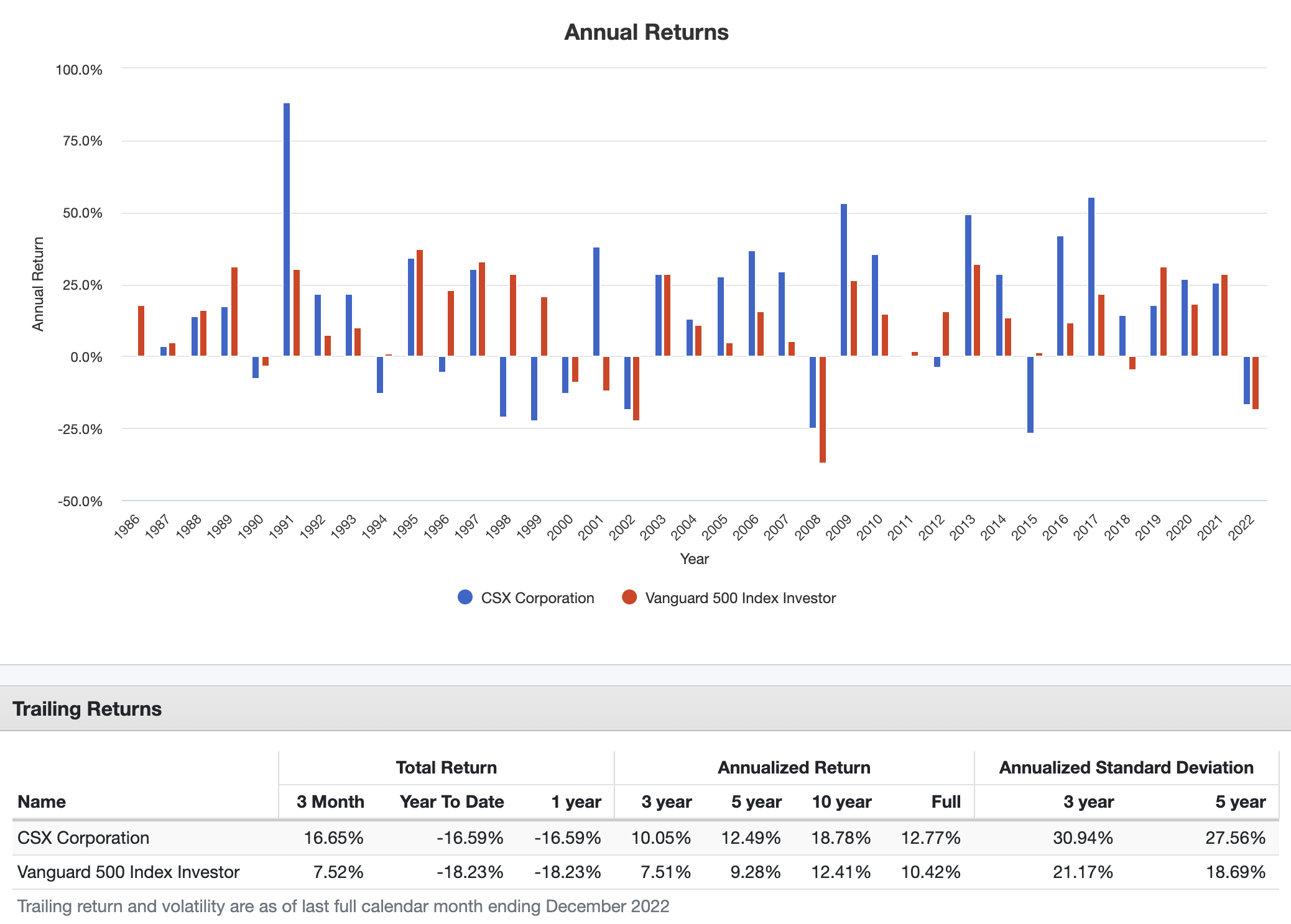

Going back to 1985, CSX has returned 12.8% per year, including dividends. This beats the market by more than 200 basis points per year. This outperformance is consistent as the 3/5/10-year periods show.

These outperforming returns come with a somewhat elevated standard deviation, which is caused by the company’s cyclical business model. After all, the moment economic growth slows, transportation volumes drop.

The upper part of the overview below shows that CSX tends to sell off more than the market in years of poor economic growth, or even contraction.

Portfolio Visualizer

30% drawdowns are not uncommon. It happened three times over the past ten years.

However, as I already said, that’s a characteristic we can use to our advantage, given the other qualities the stock brings to the table.

This brings me to reason 4.

4. Supply chain re-shoring

One of the topics we started to discuss a bit more last year is supply chain re-shoring. For example, on December 5, I wrote an article covering my view on supply chain re-shoring and several dividend picks that benefit from that. In that article, I covered Canadian Pacific, a Canadian peer of CSX. However, CSX is also impacted by this.

Essentially, the pandemic triggered supply chain de-risking. Companies saw that modern supply chains were, in fact, not as resilient as initially expected. The pandemic opened a lot of eyes, which includes awareness of the risks that come when dealing with governments like the one in China.

Companies wanted to move supply chains closer to their end-customer. Meanwhile, high energy prices and structural changes in Europe are triggering the same, which is great news for manufacturing in the United States.

CSX benefits from that. After all, it is the backbone of manufacturing in the Eastern part of the United States, connecting companies to supply and demand.

On November 15, CSX commented on this during the Stephens Annual Investment Conference.

I still am a believer that you’re seeing more and more activity on the on-shoring side with uncertainty in China, with some of the things that have been created with the Russia conflict, that’s going to be more and more of a driver for companies as they look at their supply chain as a competitive advantage, and how can they have the reliability to their customers that others can’t deliver.

Moreover, the company highlighted the strength of the US consumer, and the need to shorten supply chains.

[…] the best way to create reliability is have your production closer to the end consumer and we touch the most valuable consumers in the world, 2/3 of them here in the U.S. And I think you’re really seeing that. I know there’s been debates before of whether we’re going to see onshoring. I remember when we had Chief Energy, everybody said a big way that onshoring is going to happen and never materialize. But I think this time, we are seeing the numbers come through on real capital being spent on that. So that’s — that’s a big opportunity for us going forward.

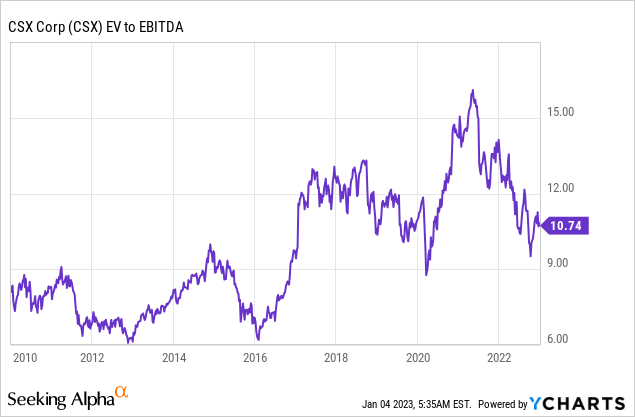

Valuation

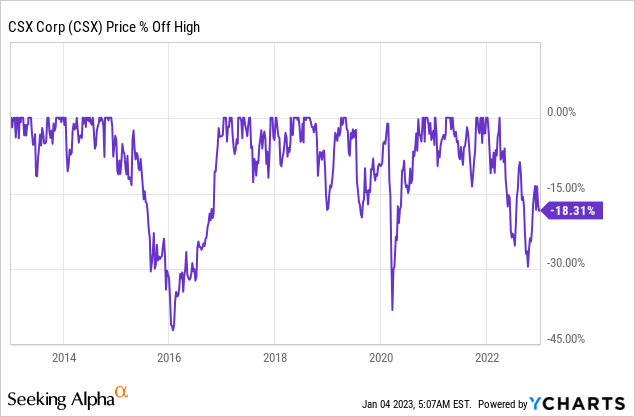

CSX is trading 20% below its 52-week high. This is resulting in an EBITDA multiple of 10.8x, using a 2023E EBITDA of $7.3 billion. It’s also based on its $79.2 billion enterprise value, consisting of its $64.9 billion market cap, $14.0 billion in 2023E net debt, and just $300 million in pension liabilities.

FINVIZ

This valuation is attractive as it is now below the five-year median.

However, the problem is that EBITDA estimates are likely to come down, as we discussed in the first part of this article. This could push the stock down to $26 without making it look any cheaper.

Hence, investors who like the long-term value CSX brings to the table should keep a close eye on CSX. I think a move lower toward $26 opens up fantastic long-term investing opportunities.

Takeaway

In this article, we discussed one of America’s largest railroads. CSX Corporation is a terrific dividend growth stock, despite offering a low yield. The company uses strong free cash flow to maintain consistent and strong dividend growth, while aggressively engaging in buybacks.

Moreover, the company is poised to be a big winner in a long-term supply chain re-shoring trend, benefiting domestic manufacturing production and everything related.

However, economic circumstances are getting worse by the day. It looks highly likely that CSX shares work their way to $26 again.

While that isn’t fun for existing shareholders, I think it’s a terrific opportunity for investors to buy (more) CSX exposure at attractive prices. On a long-term basis, I have little doubt that the company will continue to outperform the market by a wide margin.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment