Rost-9D/iStock via Getty Images

Introduction

Constellation Software Inc. (OTCPK:CNSWF) reported earnings on Friday. Headline numbers were impressive, but many more positive things lie under the surface. We’ll go over all of these things in this article. The market was prepared for the worst after seeing the company’s stock price performance on Friday, but results were better than we personally expected, especially when it comes to organic growth.

Without further ado, let’s dig directly into the numbers.

The numbers

Constellation’s headline numbers were excellent. However, as is always the case for the company, the KPIs go far beyond revenue and earnings.

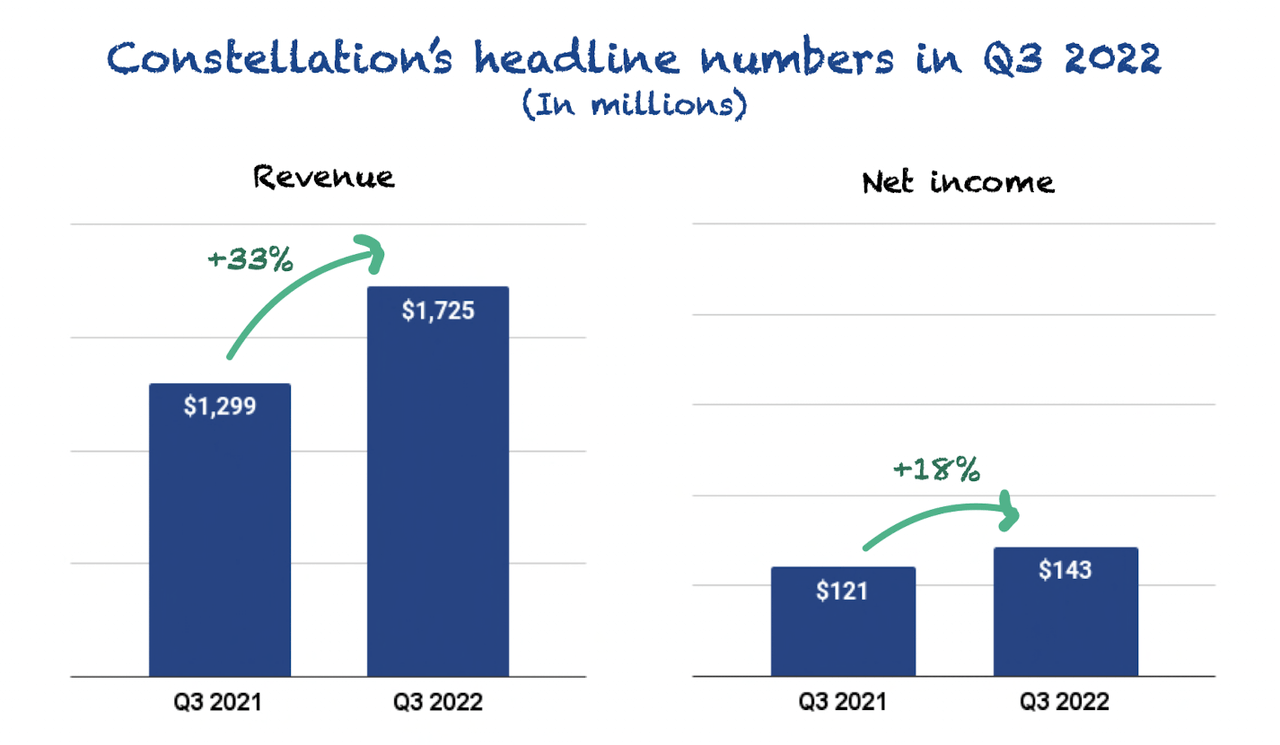

Revenue grew 33% year-over-year to $1.73 billion, and net income increased 18% year-over-year to $148 million (consolidated):

Made by Best Anchor Stocks

Without including non-controlling interests, net income grew 28% to $138 million. The fact that revenue grew faster than net income means there was some margin contraction, but as we’ll see later on, one of the expenses that created this contraction is excellent news for Constellation.

Revenue accelerated from the previous quarter (+30% year-over-year) and showed why we shouldn’t focus on quarters when looking at Constellation. The company has made a significant acquisition (Altera) this year, which has helped boost revenue growth. Without considering revenue from this large acquisition, revenue growth would’ve been 16%.

Let’s dig a bit deeper into revenue and its components.

Digging deeper into revenue

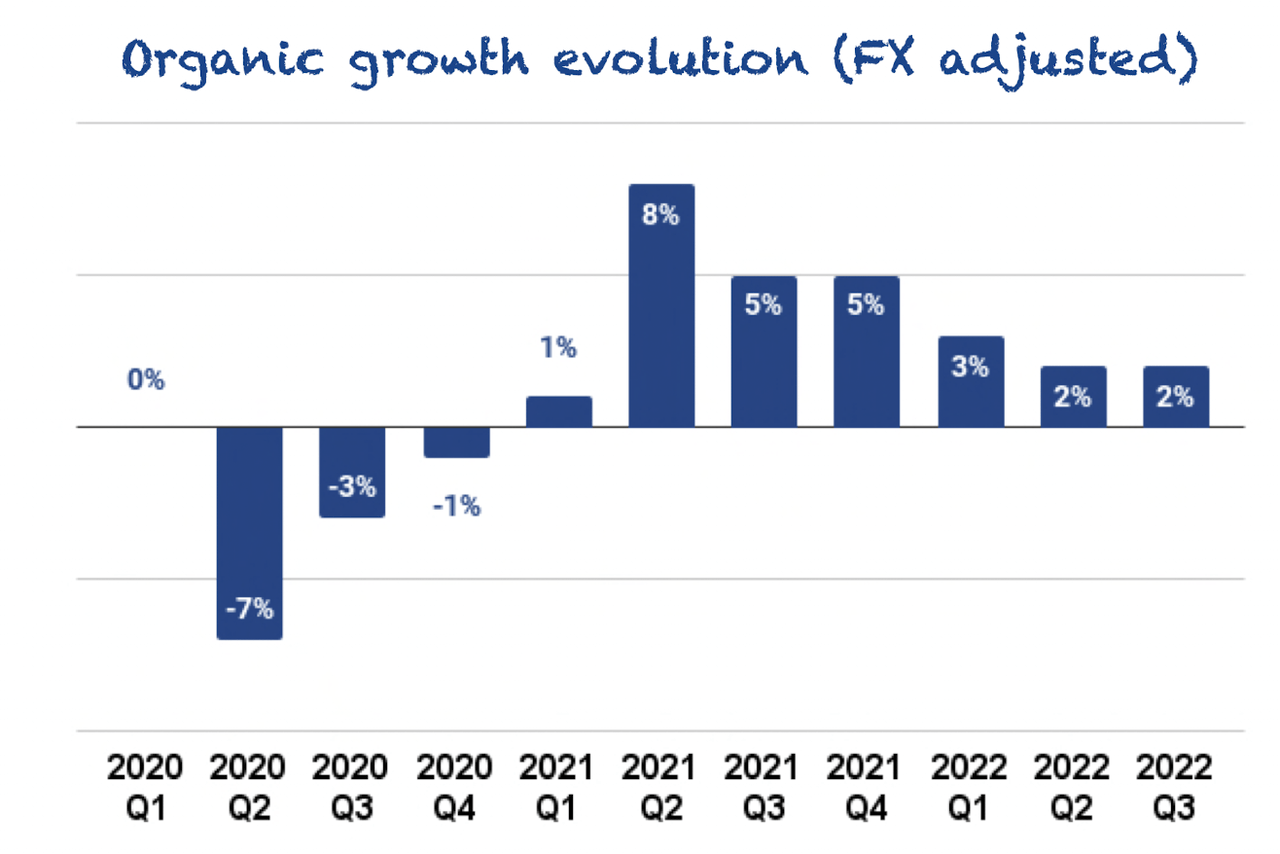

Constellation has two sources of revenue growth: acquisitions and organic growth. As per usual, revenue growth was primarily driven by acquisitions, but there is good news on the organic growth front.

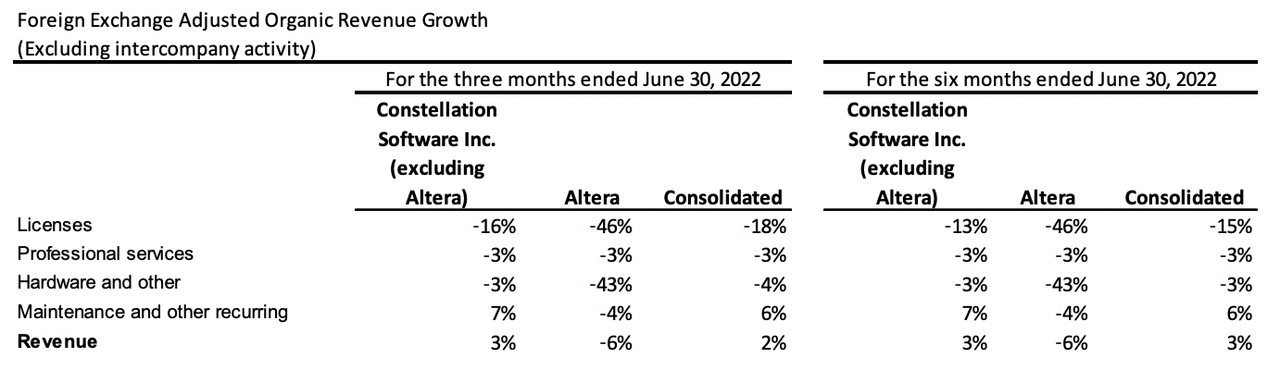

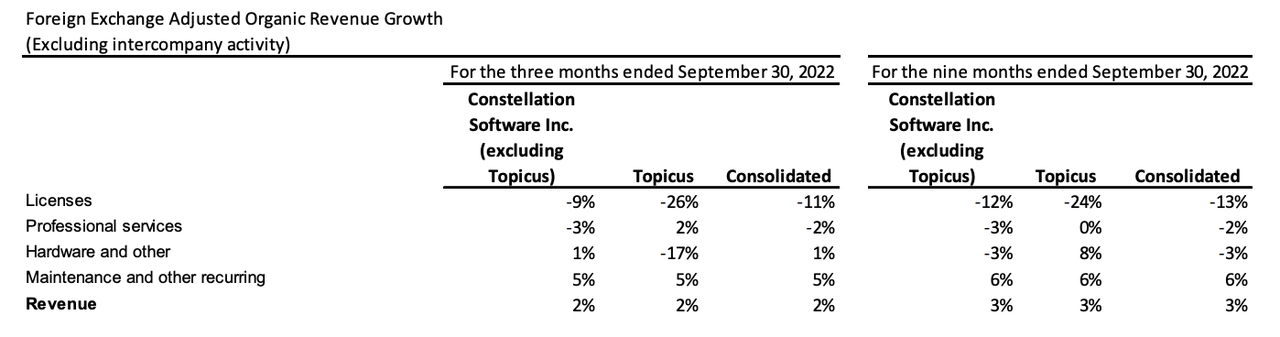

Organic growth was still severely impacted by foreign exchange headwinds, so we’ll focus on FX-adjusted metrics. FX-adjusted organic growth was the same as last quarter, 2%:

Made by Best Anchor Stocks

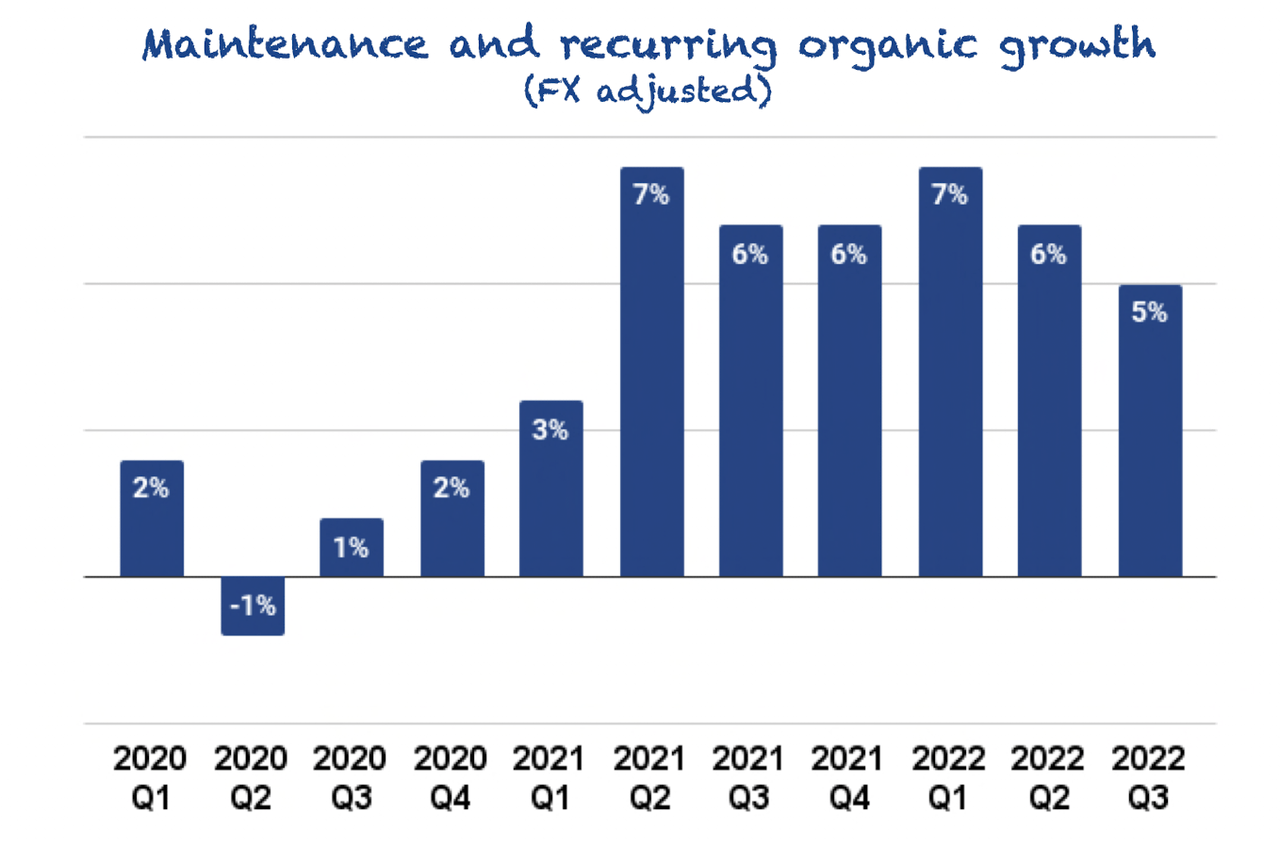

The bright spot of organic growth was once again in management’s preferred revenue source: maintenance and recurring. This revenue source grew 5% organically, at a significantly faster pace than overall organic revenue:

Made by Best Anchor Stocks

It was the 9th consecutive quarter of maintenance and recurring organic growth, despite the last two quarters being negatively impacted by the Altera acquisition. For the last two quarters, management has provided the organic growth metric excluding Altera, and we can see how Altera “shaved off” organic growth from maintenance and recurring:

Constellation Q3 MD&A

Altera had negative organic growth this quarter, but it has improved sequentially:

Constellation Q2 MD&A

Impacts on organic growth from acquisitions (both positive and negative) are something we must live with, but as Altera was such a large acquisition, we get a clearer picture by excluding it. Of course, this doesn’t mean Altera will always contribute negatively to organic growth, but it probably will until Constellation effectively integrates it into its VMS portfolio and realizes all the synergies.

We believe there are many synergies to be realized across the Altera acquisition, but signs are encouraging. The company reported a positive net income margin of 6% in Q3, which is a significant improvement with respect to Altera’s negative net income margin of 3.6% last quarter.

Regarding Topicus’ impact on organic growth, last quarter, we saw how it contributed positively. This quarter it did not impact it at all:

Constellation Q3 MD&A

We believe there is still room for Constellation to improve its organic growth, but this quarter’s performance excluding Altera was very good. Moreover, it was even better after considering Topicus’ organic growth, which typically excels in this metric. It’s true, though, that Topicus operates in Europe, where the macro landscape is a bit more problematic than in the U.S. and might be negatively weighing on growth.

Looking at the expense side – Growing for the right reasons

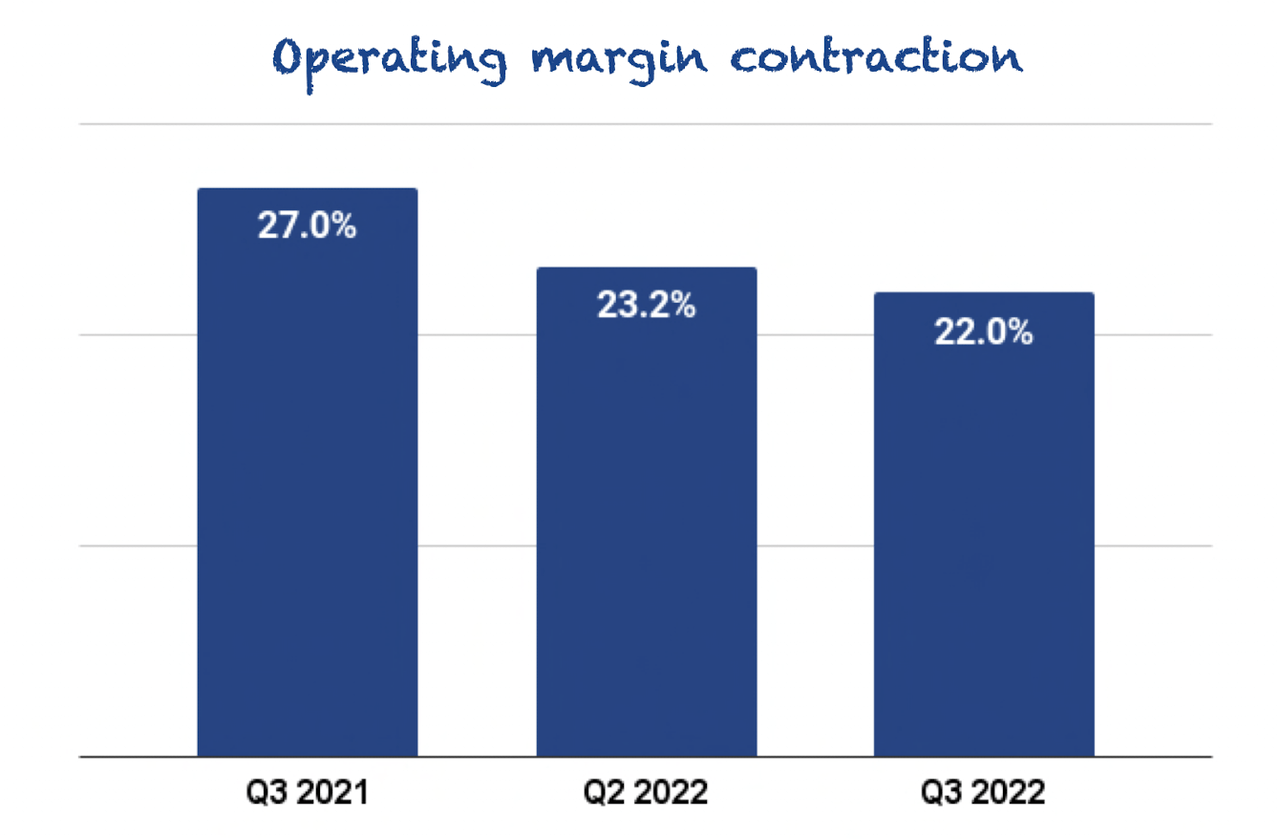

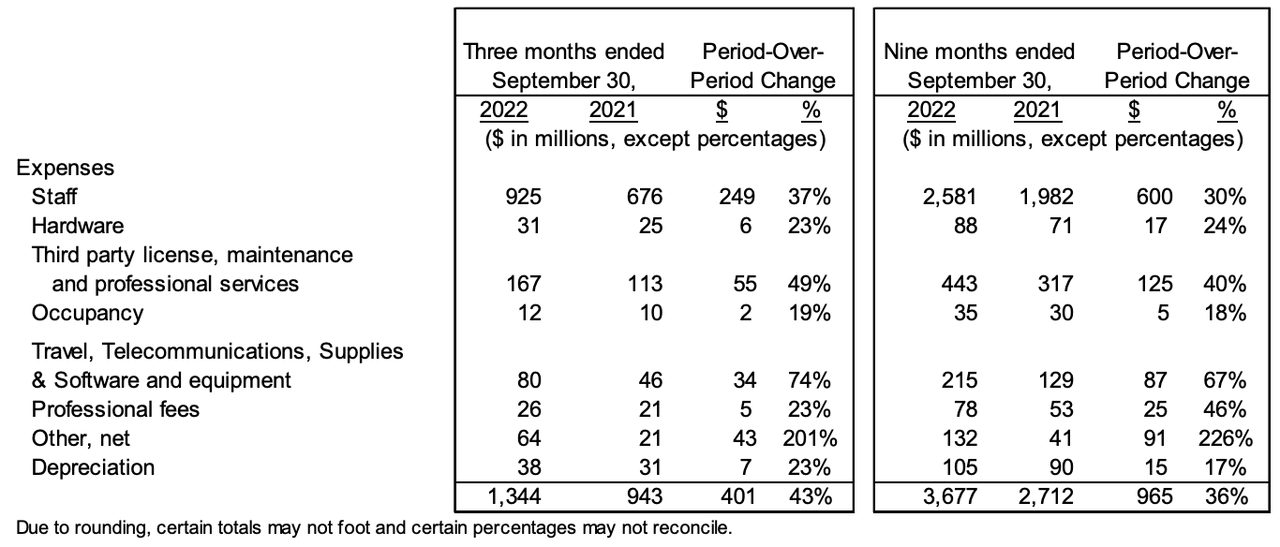

As we discussed before, operating expenses grew faster (+43% year-over-year) than revenue, so there was a slight margin contraction:

Made by Best Anchor Stocks

There were no worrying signs in these increased expenses. In fact, there was positive news. Yes, you read that right. There was good news about increased expenses. That doesn’t often happen, right?

Contrary to organic growth, margins benefited from a strong dollar as it reduced expenses by approximately 6%. The company is “hedged” against currency risk because a strong dollar reduces organic growth but protects margins through lower expenses.

Constellation Q3 MD&A

The increased expenses came from various sources:

Constellation Q3 MD&A

Several of these stand out because they grew faster than revenue. Namely:

-

Staff

-

Third-party license, maintenance, and professional fees

-

Travel, Telecommunications, Supplies, & Software, and equipment

-

Other, net.

The first two grew faster than revenue as a result of acquisitions. Constellation constantly acquires businesses, so its staff expenses are rarely entirely optimized. What we mean by this is that there’s a lag between when an acquisition is made and when the company manages to optimize its operations through several initiatives, like sharing central services, for example.

The third expense grew as a result of the lifting of the COVID restrictions. Last year, travel was muted because many countries had restrictions in place, but this year it’s going back to normal and thus creating a natural lift in this kind of expense. It’s a return to normal more than anything else.

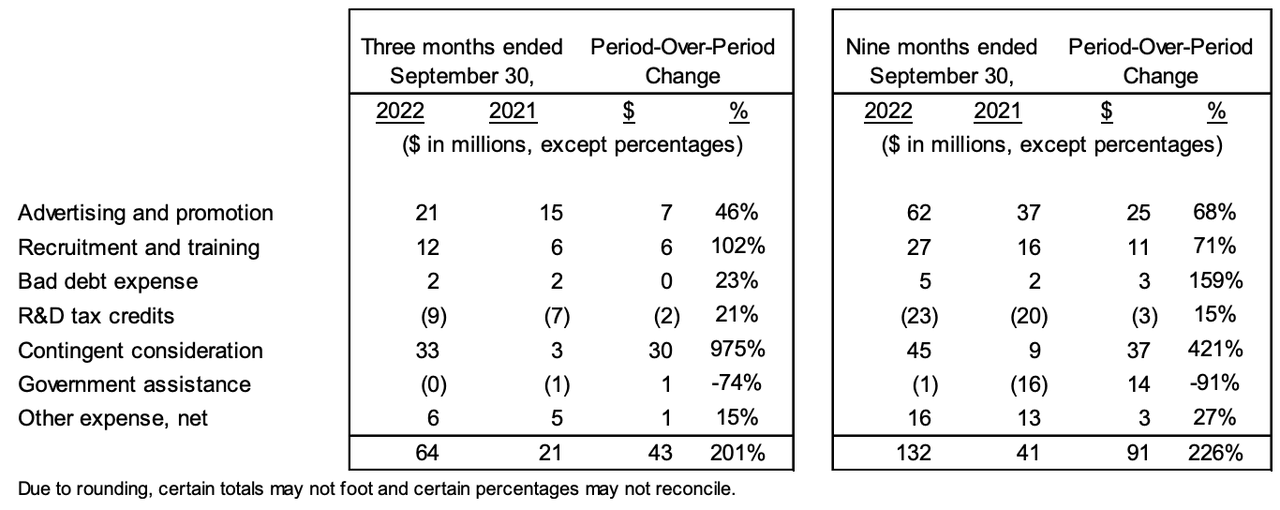

Number 4 is where we find the good news. “Other, net” has the following expense lines included:

Constellation Q3 MD&A

The outlier in this list was contingent consideration. We’ve talked about this expense item in other earnings digests, but we’ll bring here the description:

The contingent consideration expense amounts recorded for the three and nine months ended September 30, 2022 related to an increase in anticipated acquisition earnout payment accruals primarily as a result of increases to revenue forecasts for the associated acquisitions.

Source: Constellation MD&A

Simply put, if an acquisition does better than management expected, they have to pay a bit more for it, and this increased payment goes into contingent consideration. A higher contingent consideration expense is indeed a higher expense, regardless of how we interpret it. Still, in this case, a higher expense means that the company’s acquisitions are doing better than expected, which is great to see.

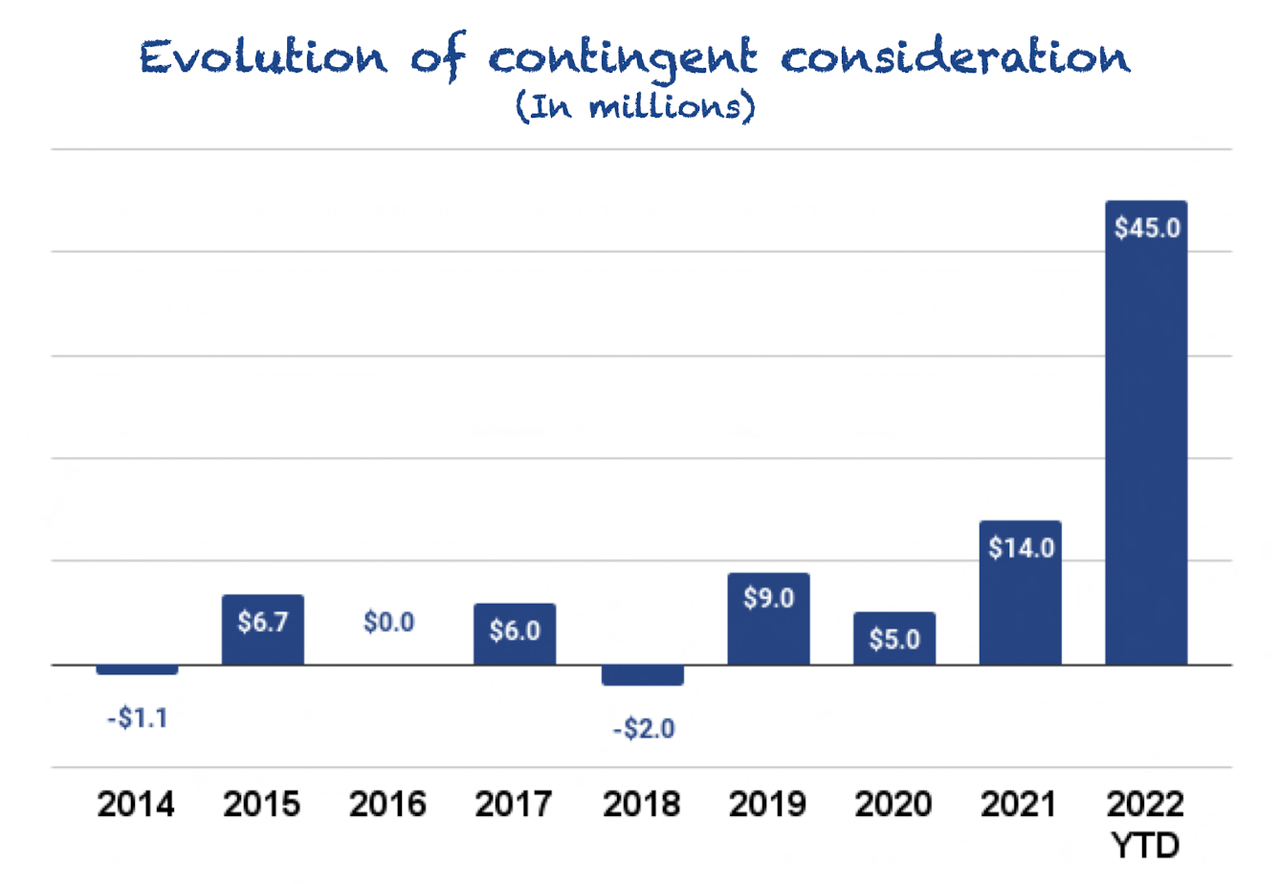

A $33 million contingent consideration expense is significant compared to other quarters. The contingent consideration expense for this quarter was higher than this expense for 2021, 2020, and 2019, combined!

Made by Best Anchor Stocks

There’s a limitation to interpreting a higher contingent consideration as “acquisitions are going better than expected,” though. Why? Because this expense only considers those acquisitions that explicitly note in the acquisition terms that the price will increase if specific targets are met. For those acquisitions that don’t have these considerations included, we don’t have a way of knowing how they are performing.

If we adjust operating expenses for contingent consideration, we can see that Constellation’s operating margin was significantly better. However, it wouldn’t really be entirely “fair” to do this because it’s also true that this expense comes from higher-than-expected revenues, so we should adjust those too in that case.

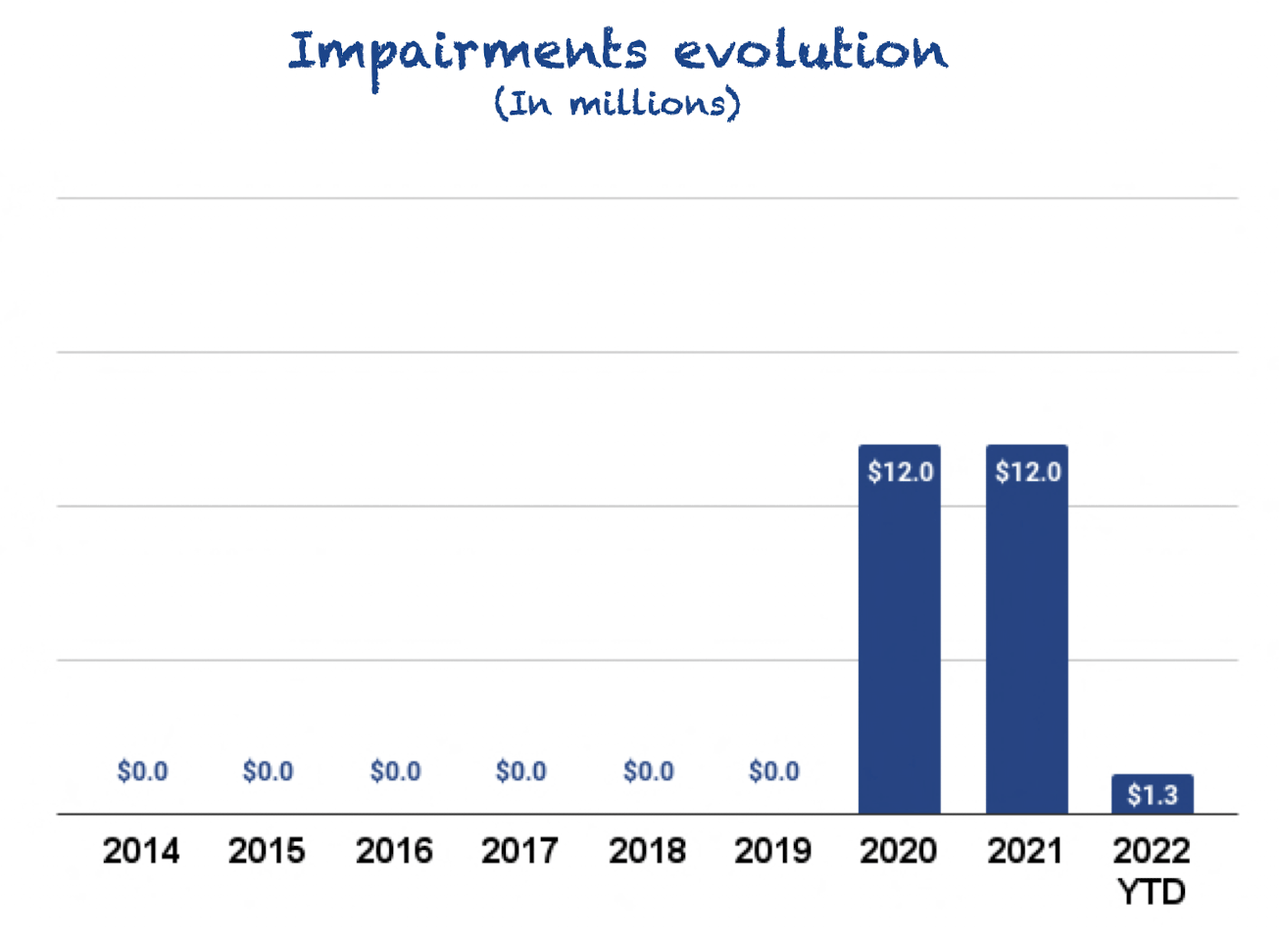

There’s an opposing part to the story. Constellation also incurs impairments when acquisitions go worse than expected. Fortunately, no impairments were incurred this quarter, and the YTD impairments remain very low compared to 2020 and 2021. Of course, we don’t know what Q4 will bring:

Made by Best Anchor Stocks

Constellation focuses quite a bit on price when making acquisitions, which is reflected in reduced impairments.

There seems to be quite a significant margin of safety in the company’s acquisitions. Another metric to understand the type of acquisitions that Constellation makes is the bargain purchase gain. The company describes this metric as follows:

Results from the fact that the fair value of the separately identifiable assets and liabilities acquired exceeded the total consideration paid, principally due to the acquisition of certain assets that will benefit the Company that had limited value to the sellers.

Source: Constellation MD&A

The company recorded a $3 million bargain purchase gain this quarter, which despite being insignificant, is not something you would typically see in other companies. Some companies’ assets are automatically worth more just by being part of Constellation’s broad VMS portfolio.

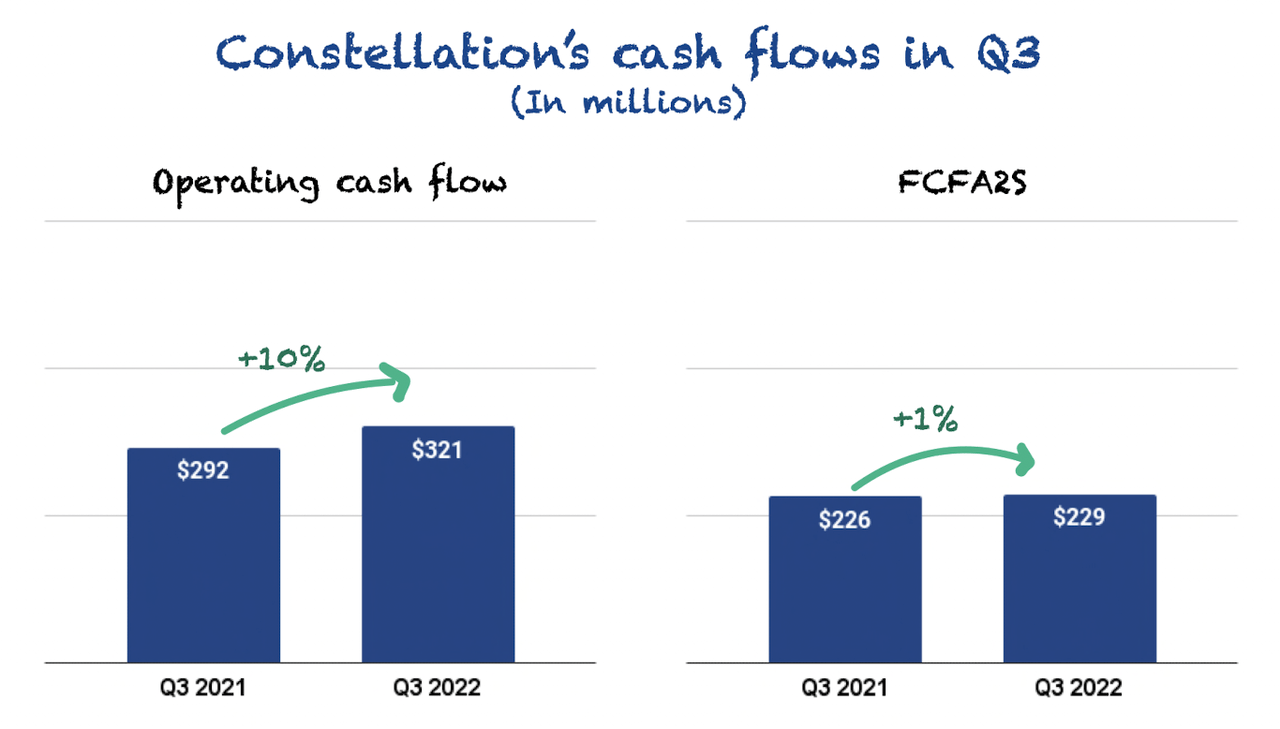

Looking at cash flows – Still impacted by a tax change

In the previous quarter, we saw how cash flows decreased significantly, mainly due to a non-cash operating working capital hit. This quarter, cash flows went back to a more normal trajectory, but they were still impacted by other events.

Operating Cash Flow increased 10% year-over-year while FCFA2S increased 1% year-over-year:

Made by Best Anchor Stocks

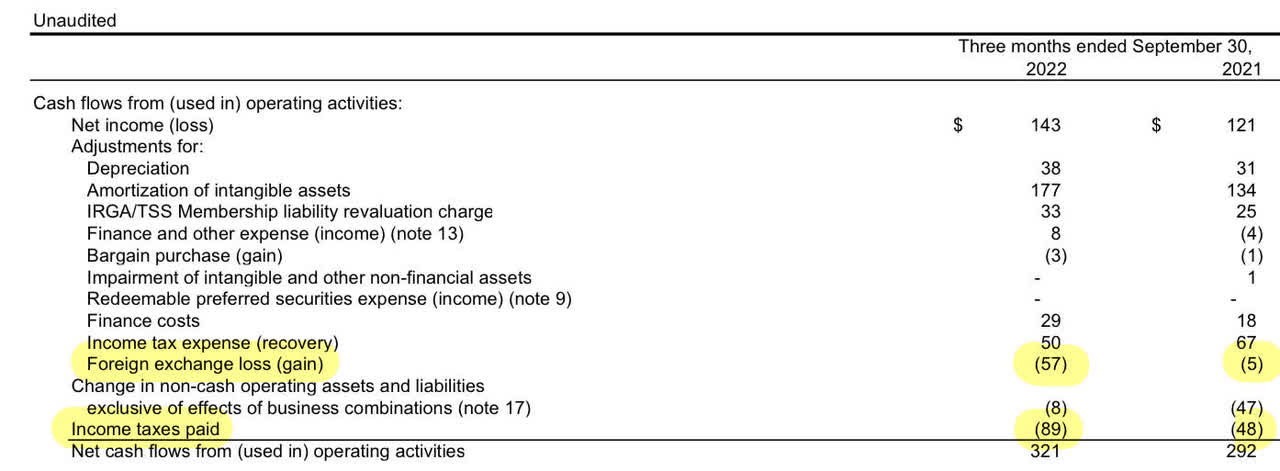

Operating cash flow did not grow as fast as net income due to a higher foreign exchange gain and higher taxes:

Constellation Q3 Financial Statements

Taxes were significantly higher due to the change in the Tax Cuts and Jobs act that already impacted cash flows last quarter:

Effective for 2022, research and experimentation (R&E) expenditures are no longer allowed to be deducted as incurred for US entities. The Tax Cuts and Jobs act mandates that, for tax years beginning after December 31, 2021, R&E expenditures be deferred and amortized.

Source: Constellation MD&A

As Constellation has to spread the deduction of these expenses over a longer period, taxes go up due to higher net income. This new legislation was not in place in 2021, so higher taxes are weighing on cash flow growth this year. As soon as we unlap these “tough” comps, we should see a return to more normal growth in 2023.

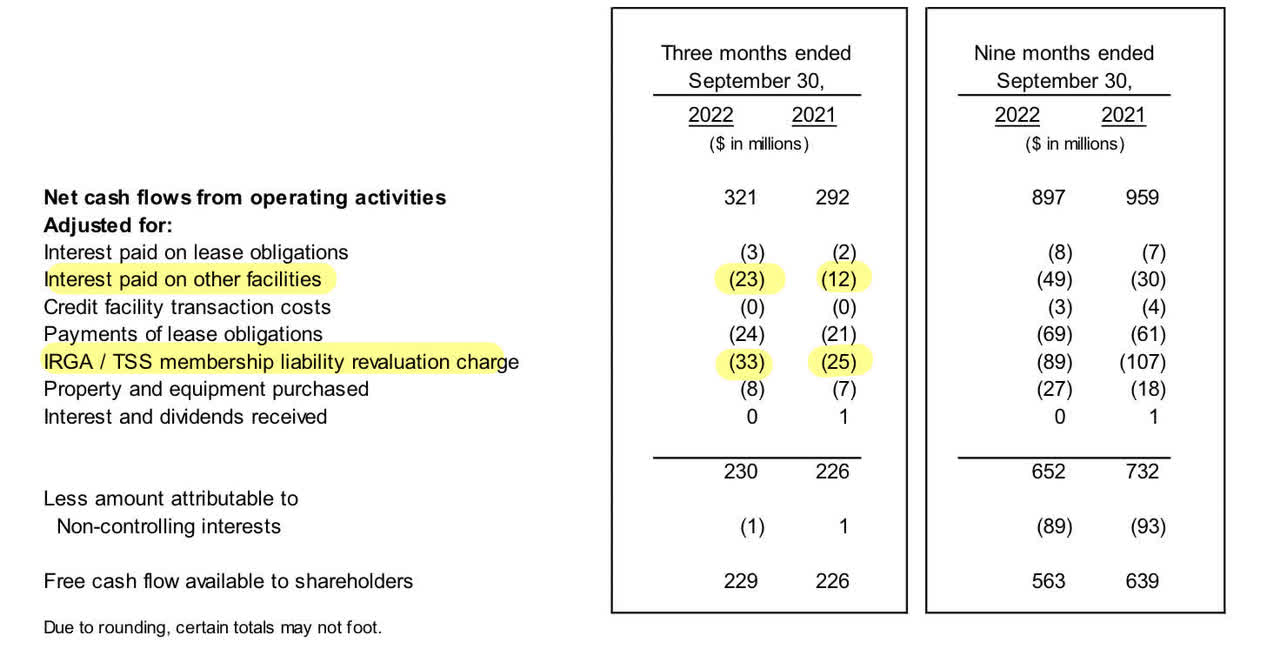

Regarding FCFA2S, it was impacted by the same things as operating cash flow and also from higher interest paid and an increase in IRGA revaluation charges:

Constellation Q3 MD&A

We have explained the IRGA/TSS membership liability in prior articles, and it’s pretty complex. Simply put, some Topicus equity holders can sell their shares to Constellation at a predetermined price set in the IRGA if they wish to. Constellation views this as a liability and records the increases in this liability as a reduction in FCFA2S.

All in all, some positive developments in cash flows. There’s little the company can do to “solve” the two things holding cash flow back. The foreign exchange gain will most likely correct going forward, whereas taxes should enjoy easier comps next year.

If we look at the first 9 months, cash flows are still significantly down due to the impact that Constellation suffered in non-cash operating working capital in Q2.

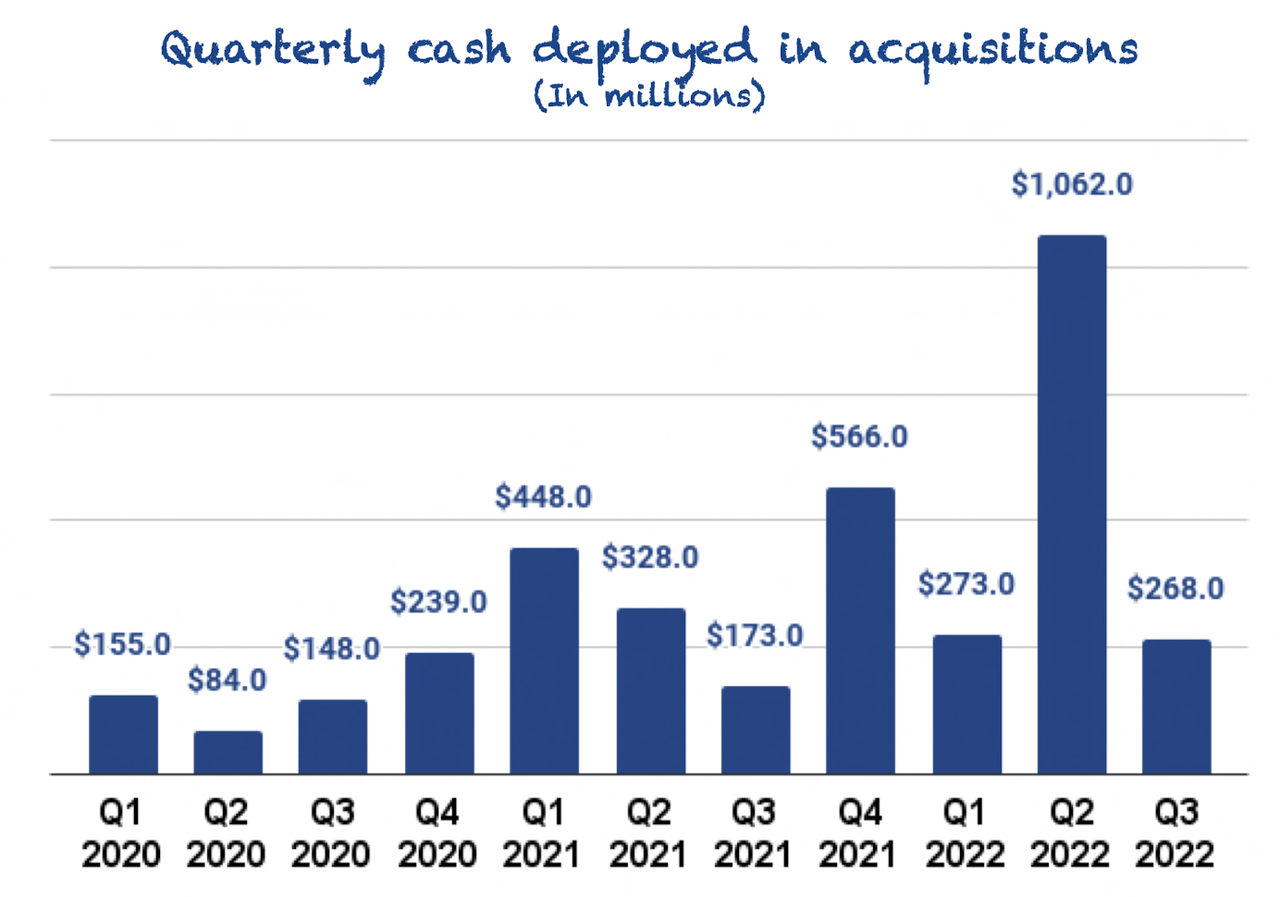

Acquisitions – An average quarter

Constellation had an average quarter regarding capital deployment. The company deployed $268 million into acquisitions in the quarter:

Made by Best Anchor Stocks

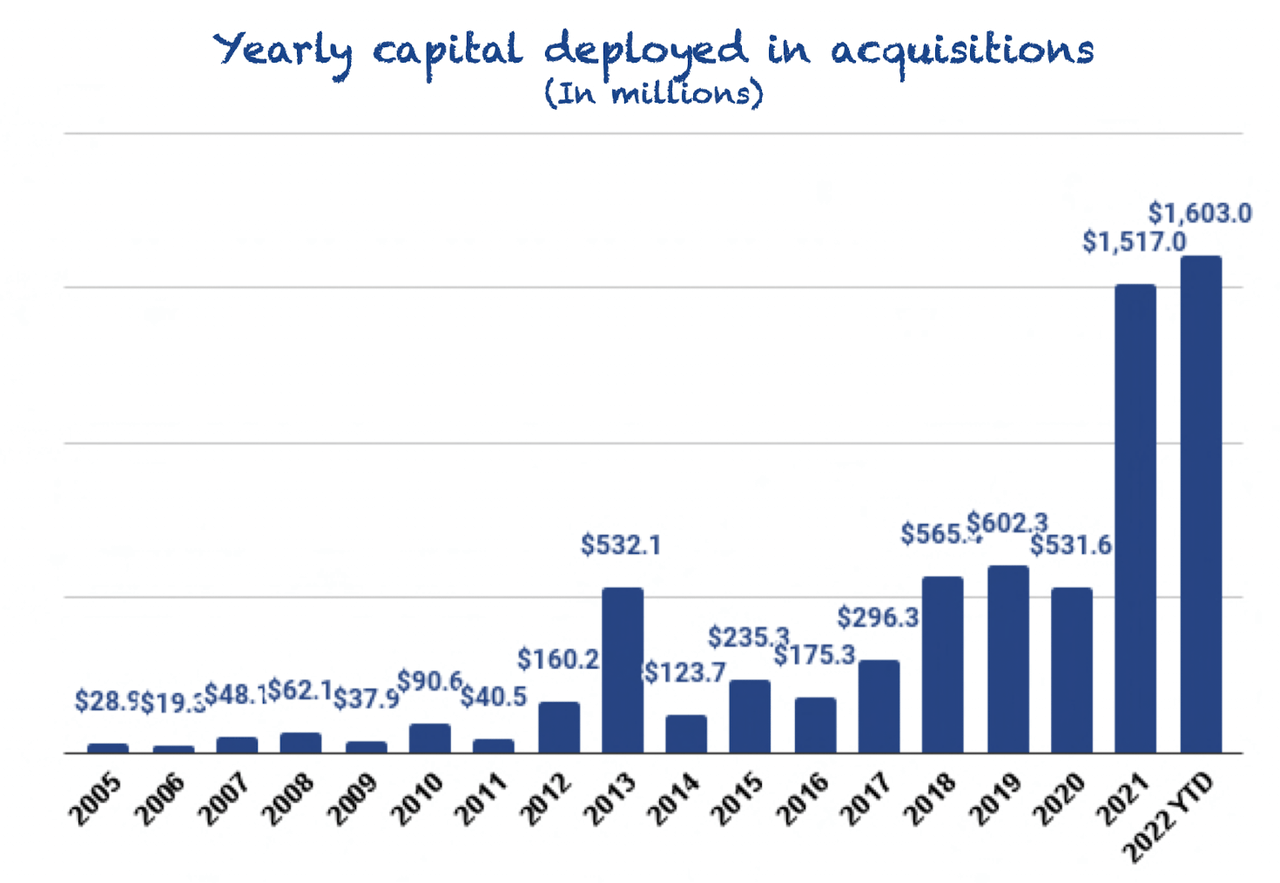

Of course, capital deployment was much more muted than in Q2, but that was because the Allscripts (now Altera) acquisition had an outsized contribution in that quarter. If we zoom out and see what Constellation has deployed this year, we can see that it has been the best year in this regard by a wide margin, and there’s still one quarter to go:

Made by Best Anchor Stocks

Capital deployment is volatile because management can’t predict when opportunities will arise, but it remains at a healthy level. Constellation’s bread and butter is making plenty of small acquisitions, but as the company scales, it must look to larger acquisitions to continue to add value through inorganic ventures. It’s impossible to know when these large acquisitions will come, but Constellation’s management is looking at them more in-depth than it did in the past.

There’s been a bit of criticism regarding the shift to large acquisitions, but its largest acquisition ever seems to be playing out just fine. If Constellation manages to crack the code with large acquisitions the runway ahead to scale capital deployment remains significant.

Management is leveraging the balance sheet

Constellation’s management has historically run a very conservative balance sheet compared to other serial acquirers. However, it’s leveraging it a bit now to conduct larger acquisitions.

The company ended the quarter with a net debt position of $561 million, comprised of $665 million in cash and $1.2 billion in debt. From this amount of debt, $939 million is held by subsidiaries and is not guaranteed by Constellation.

All in all, the company’s financial position remains strong despite its higher debt. Let’s not forget the company has generated almost $900 million in operating cash flow during the first 9 months.

The company’s solid financial position might turn out to be an advantage compared to other more leveraged competitors going into a higher-rate environment.

Conclusion

Constellation Software reported a solid quarter. Revenue growth was strong, aided by the Altera acquisition, and the cash deployed was decent. Expenses grew faster than revenue due in part to outsized contingent considerations, which is great because it shows that Constellation’s acquisitions are going better than expected.

In the meantime, keep growing!

Be the first to comment