We Are

Data analytics and marketing expert comScore, Inc. (NASDAQ:SCOR) reports a significant number of clients and many patents related to data science. Like other analysts, I believe that future free cash flow would justify a fair price that is significantly higher than the current fair price. I obviously see risks from data regulators and potential failure of acquisitions; however, the current fair price appears too low.

Business Model

Media measurement and analytics company Comscore offers added value to data management and analysis in the field of multimedia platforms in the United States and globally. Clients receive from SCOR a holistic view, which makes them reshape their own products.

Source: Investor Relations

SCOR’s business model is diversified into segments that are always in the field of analysis and improvement of digital information traffic. These include an advertising area, a marketing area, a content tactical programming area, a digital analytics area, and a movie-only segment for box office projections, distribution, and global positioning.

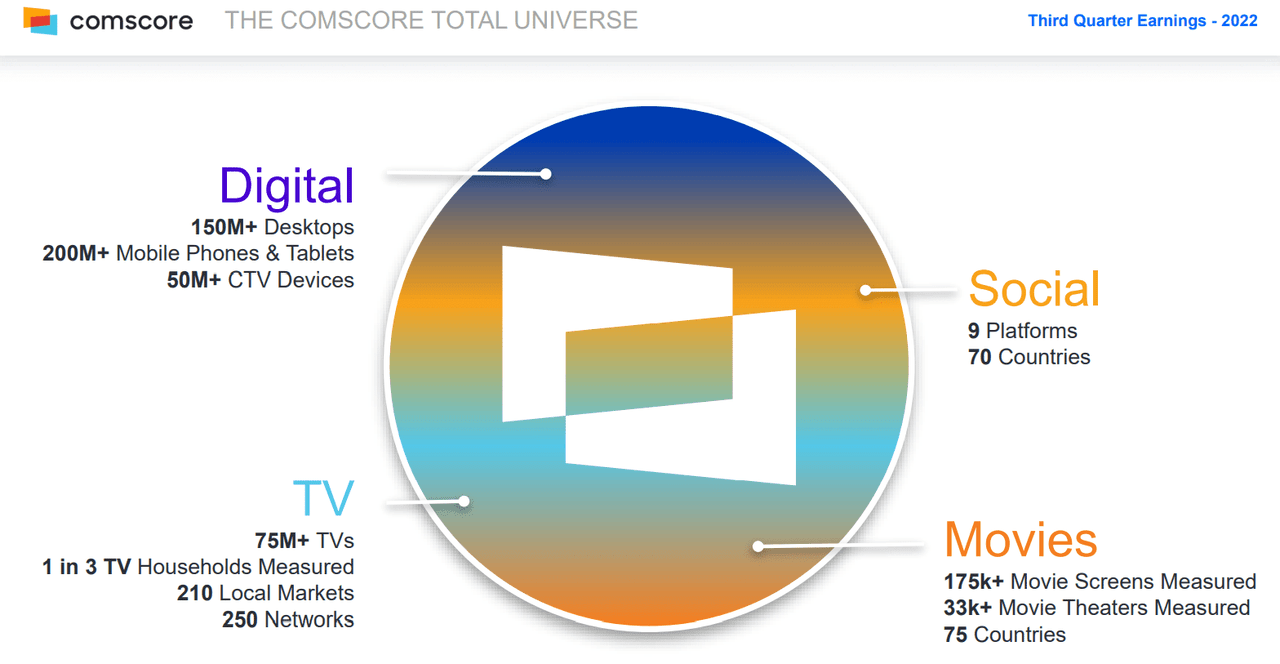

To deliver these services, Comscore has developed a high degree of reliability in its data science and analytics methods, gathering information from audiences ranging from television to digital media, including mobile devices such as tablets, cell phones, and laptops. Video games, electronic commerce, and the advertising market are also added on these elements. This allows Comscore a level of detail and segmentation based on geographic and demographic data that effectively provides localized targets while offering its contracting companies’ products. Currently, the number of social platforms, movies, TVs, mobile phones, desktops, and other devices assessed appears quite impressive.

Source: Investor Relations

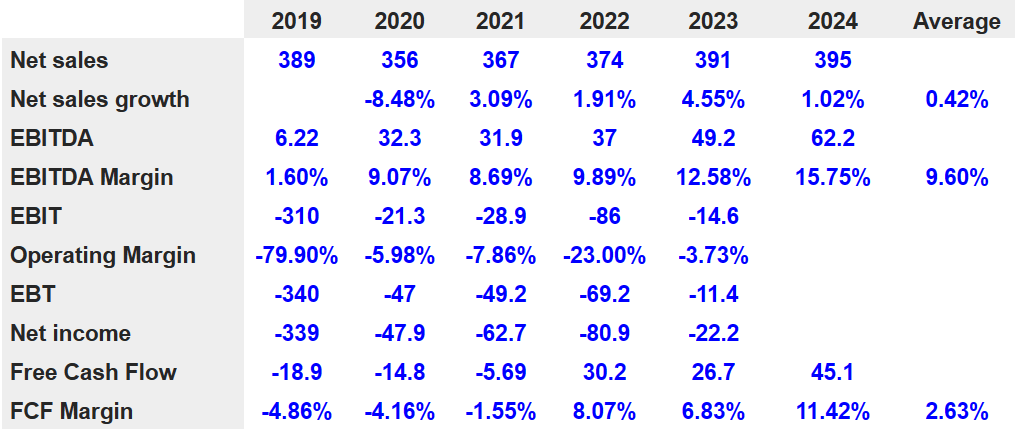

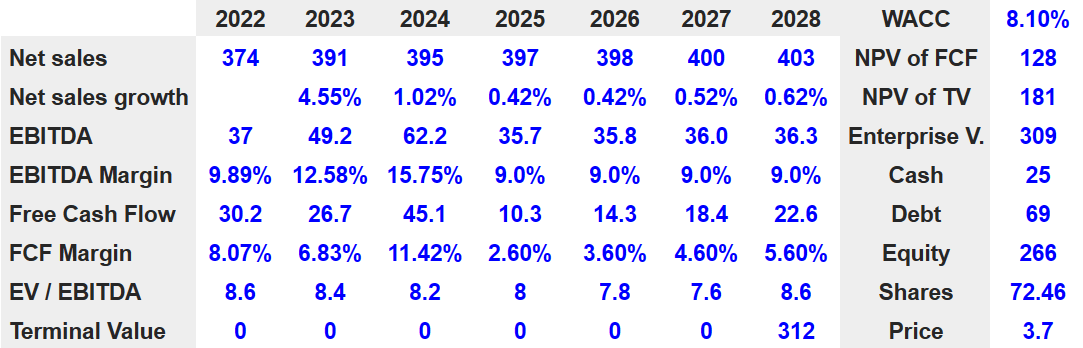

Market Expectations Include An Average EBITDA Margin Of 9% And A FCF Margin Of 2.6%.

I believe that market expectations include very beneficial figures. Guidance includes 2024 net sales of $395 million and 2024 net sales growth of 1.02%. Besides, 2024 EBITDA would stand at $62.2 million with an EBITDA margin of 15.75%. 2024 EBIT would stand at close to -$14.6 million along with an operating margin of -3.73%. With that, the most interesting factor is the cash flow statement because the free cash flow is expected to stand at close to $45.1 million with a free cash flow margin of 11.42%.

Source: marketscreener.com

Balance Sheet

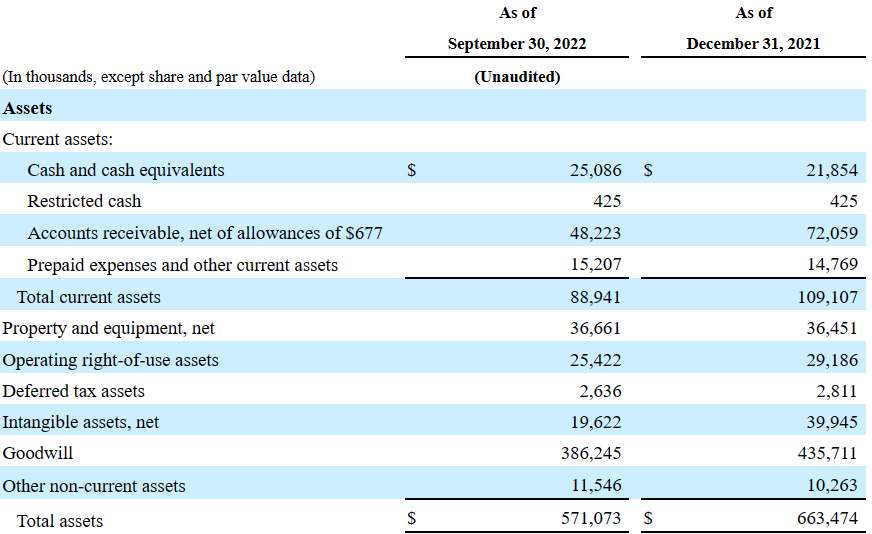

As of September 30, 2022, SCOR reported cash worth $25.086 million with the accounts receivable of $48.223 million, prepaid expenses worth $15.207 million, and total current assets close to $89 million. Current assets are less significant, which may worry certain investors. With that, I am not worried because SCOR appears to generate a relevant amount of liquidity.

Property is worth $36.661 million with operating right of use of $25.422 million, intangible assets worth $19 million, and goodwill of around $386 million. Total assets are close to $571 million, implying close to 2x the total amount of liabilities. Hence, I am not worried about the company’s financial situation as the balance sheet appears in good shape.

Source: 10-Q

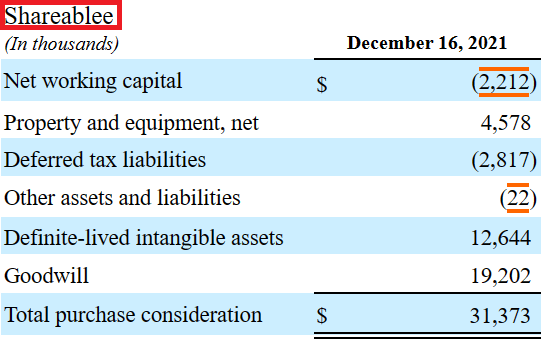

The company appears to acquire a significant number of targets, which explains the total amount of goodwill. The most recent acquisition was that of Shareablee for $31 million including goodwill worth $19 million. I believe that including the assets acquired from Shareablee would help understand the type of transactions made by SCOR. Considering the total amount of goodwill, I believe that impairment risk appears substantial.

Source: 10-k

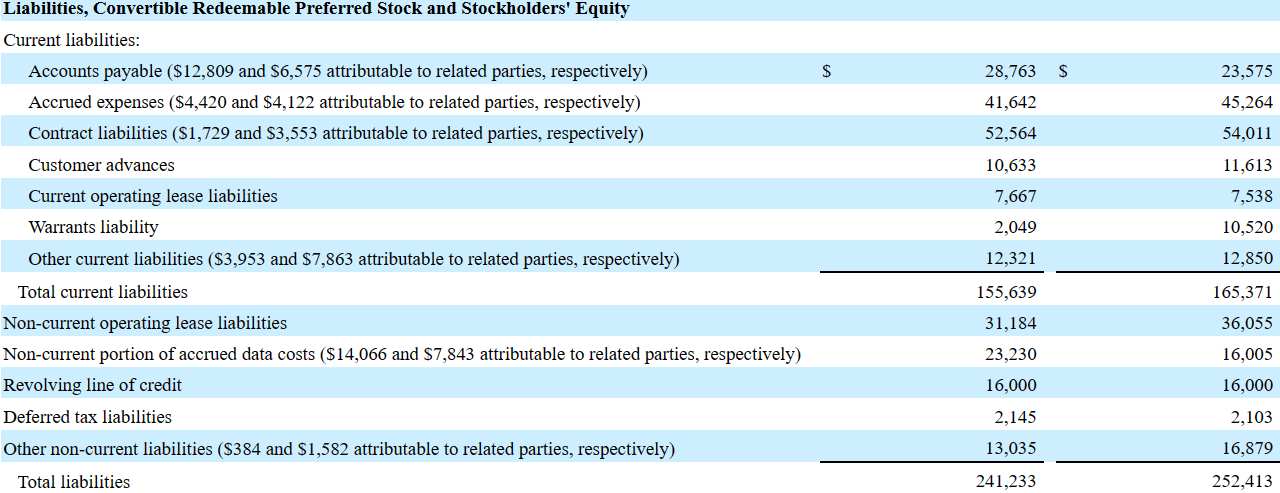

As of September 30, 2022, liabilities included accounts payable worth $28 million, together with accrued expenses of $41.642 million and total current liabilities of $155.639 million. On the other hand, non-current operating lease liabilities stand at $31.184 million. Non-current portion of accrued data costs is worth $23.230 million, and the total liabilities are equal to $241.233 million.

Source: 10-Q

Patents And Intellectual Property Related To Data Science Along With A Significant Number Of Clients Imply a Valuation Of $3.69 Per Share

Among SCOR’s clients we can find marketing agencies, local and regional broadcast television agencies, content creators and companies that provide internet services, film and television studios, parties that organize political campaigns, or companies that offer financial services. The majority of these, although they have offices deployed in more than 18 countries, are located in the United States. Asia and Canada also have active clients and operations for Comscore, but to date they have a low percentage of flow and annual revenue for the company. Considering the number of clients reported by SCOR, I believe that the company’s revenue appears well diversified. As a result, I would expect that the future revenue line will likely not exhibit significant volatility.

Regarding the organization of their products and solutions, SCOR reports three large segments of operations. These are planning and performance, analysis and optimization, and movie reports along with the analysis. Although three segments are integrated and work in the same direction, the company highlights the patents that it has certified in the field of data science, mainly referred to its analysis and optimization segment. Based on these data, the company can offer planning for the marketing of its clients as well as an outstanding report in relation to the distribution of a film. For this reason, we understand that its analysis and optimization segment is currently the core of the company’s operations, without which the other segments of its business model would not be effective or of high quality. Under this case scenario, I assumed that SCOR’s patents and intellectual property will likely enhance future FCF margin and EBITDA margin.

Under the previous conditions, I assumed 2028 net sales of $403 million with a net sales growth of 0.62%. 2028 EBITDA would stand at $36.3 million together with an EBITDA margin of 9%. 2028 free cash flow will likely stay at around $22.6 million, and 2028 FCF margin would be close to 5.60%.

Source: Bersit’s DCF Model

With an EV/EBITDA multiple of 8.6x, 2028 terminal value would be $312 million. Besides, with a WACC of 8.10%, the net present value of future free cash flow would be $128 million, and the NPV of terminal value would be $181 million. The implied enterprise value would be $309 million. Besides, with cash of $25 million and a debt of $69 million, the implied equity would be $266 million, and the fair price would be $3.69 per share.

Competition, Lack Of Innovative Products, Or Goodwill Impairment Could Bring The Fair Price Down To $0.72 Per Share

SCOR is exposed to a highly competitive market, equally made up of other companies with larger budgets for research and analysis to improve operational performance as well as smaller companies that specialize in particular topics, such as distribution of films both nationally and internationally. Under a detrimental case scenario, I believe that new entrants or existing competitors may contribute to a decline in SCOR’s EBITDA margins.

Among the most prominent competitors are Oracle’s (ORCL) Moat, for its digital marketing services, IBM (IBM) Digital Analytics in what corresponds to data analysis, or companies like Nielsen in what concerns market analysis and strategy creation in this regard.

Although these are obviously risky competitors for Comscore’s activities, the company’s success depends primarily on the ability to offer high-quality services and provide its clients with immediate solutions or best-in-class proposals. The industry of data analysis and marketing solutions is still very young, and the possible innovation in the company’s products or services can mark a distinction of value. Under my bearish case scenario, I assumed that SCOR may fail to offer innovative solutions, which would bring lower free cash flow than expected.

Comscore also faces other risks inherent to the industry, in addition to the volatility of the current economy and the lack of predictability about going forward. First of all, the regulations that appear in the field of information traffic and data collection can play a fundamental role in the operations of this company. In the same sense, the direct dependence on third-party services when collecting data is a latent risk in the development of its operations. Since any change in the contracting terms or even the purchase of any of these providers by competing companies can directly affect the analysis and optimization segment of Comscore.

Finally, I am also a bit concerned about the level of goodwill reported by SCOR. If the company’s acquisitions fail to deliver the expected synergies, I believe that accountants may have to diminish SCOR’s goodwill and intangible assets. As a result, the company’s book value per share would diminish, which may bring lower stock demand.

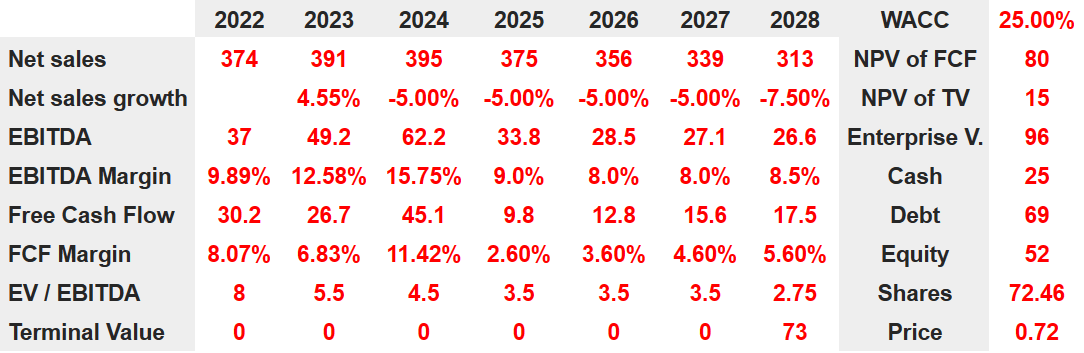

Considering the previous conditions, I forecast that 2028 net sales would be $313 million together with a decrease in sales growth of close to -7.5%. Besides, I expect 2028 EBITDA of $26.6 million together with an EBITDA margin of 8.5%. 2028 free cash flow would be $17.5 million with a FCF margin of 5.60%.

Source: Bersit’s DCF Model

If we assume an EV/EBITDA multiple of 2.75x, 2028 terminal value would be close to $73 million. With a WACC of 25%, the net present value of future FCF would be $80 million, and the NPV of TV would be $15 million.

My results would include an enterprise value of $96 million. Besides, with cash of $25 million and debt of $69 million, I foresee an implied equity of $52 million and a fair price of $0.72.

Takeaway

Comscore offers data management and analysis to a long list of customers in addition to outstanding expertise in the marketing industry. Considering the number of patents in the data science field, expectations from market analysts, and current shareholders, I am optimistic about the company’s future. Even taking into account risks from data regulators, potential M&A failures, or competitors, I believe that SCOR is worth much more than the current market price.

Be the first to comment