Orhan Turan

Cloudflare (NYSE:NET) remains one of the most richly valued stocks I own in my portfolio, and that’s saying a lot considering that beaten-down tech stocks make up the bulk of my investment holdings. The rich valuation is offset by the company’s continued strong execution even in spite of a tough macro backdrop. The stock initially dropped hard after the latest earnings report, as the company’s forward outlook appeared to disappoint investors who wanted more. The stock might not look cheap relative to peers based on today’s multiples, but if the company can deliver against projected targets, then the valuation quickly becomes more and more compelling.

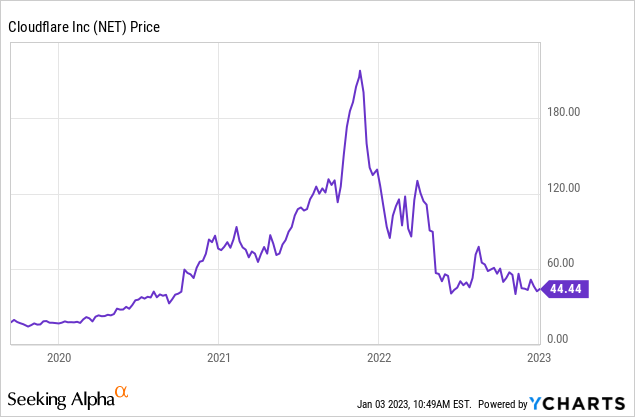

NET Stock Price

After the pandemic, NET saw its valuation bid up to astronomical levels.

I warned on the valuation multiple times, including in September of 2021 and March of this year. The stock had already fallen considerably from highs at those points but remained pricey nonetheless. After the stock fell by another large amount from there, I began buying. I last covered NET in October where I rated the stock a buy on account of the more reasonable valuation and resilient fundamentals. The stock is down 18%, offering long-term investors a prolonged opportunity to invest alongside a top-tier tech operator.

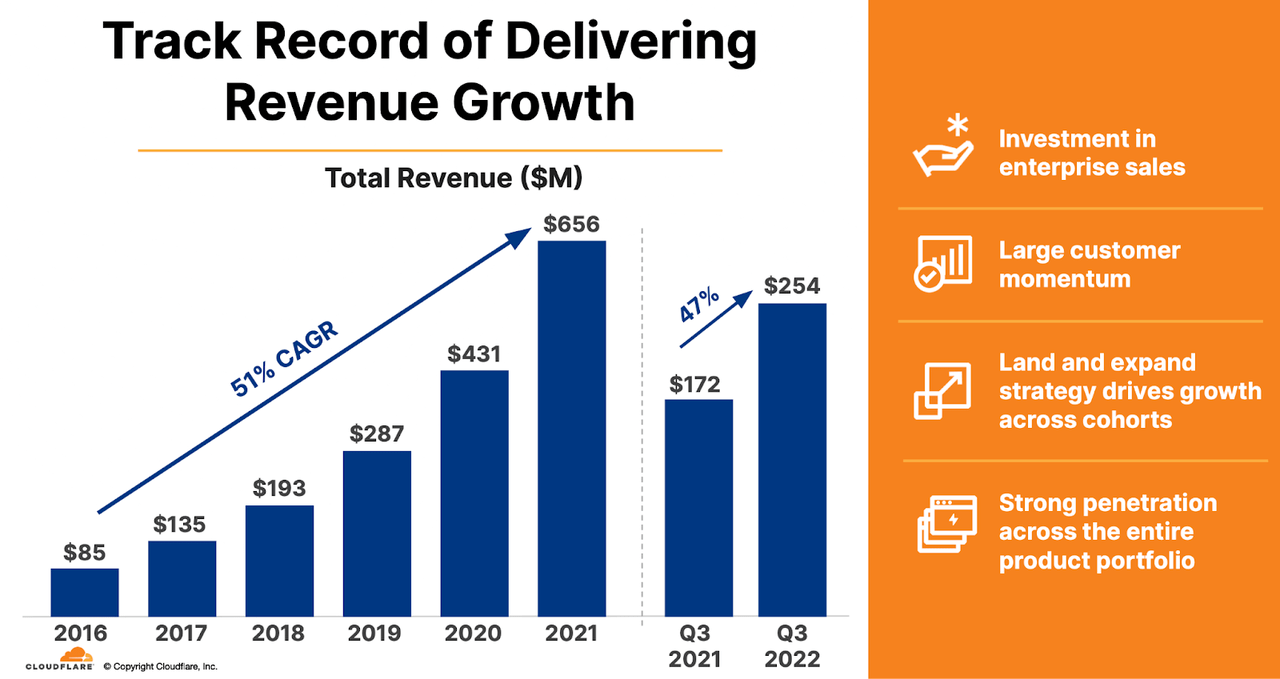

NET Stock Key Metrics

The latest quarter saw NET deliver 47% YOY revenue growth to $254 million. That is an astounding achievement considering that revenue grew by 52.2% in 2021 (and that’s on top of 50.2% growth in 2020). This is an environment in which many tech companies are taking advantage of tough pandemic comparables and a tough macro environment to justify decelerating growth rates, yet NET has somehow managed to sustain top-tier growth.

2022 Q3 Presentation

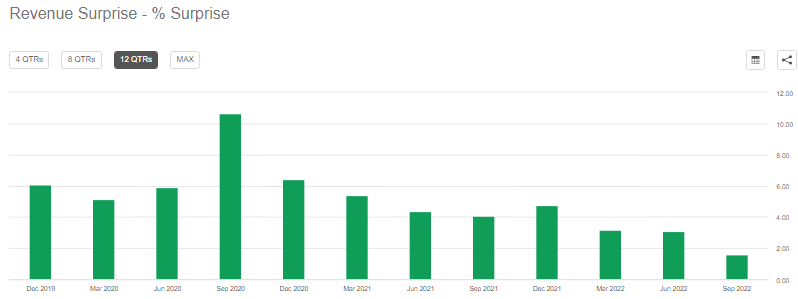

That’s not to say that the tough macro backdrop has had no effect on the company – the revenue beat represented the smallest beat over the last 3 years.

Seeking Alpha

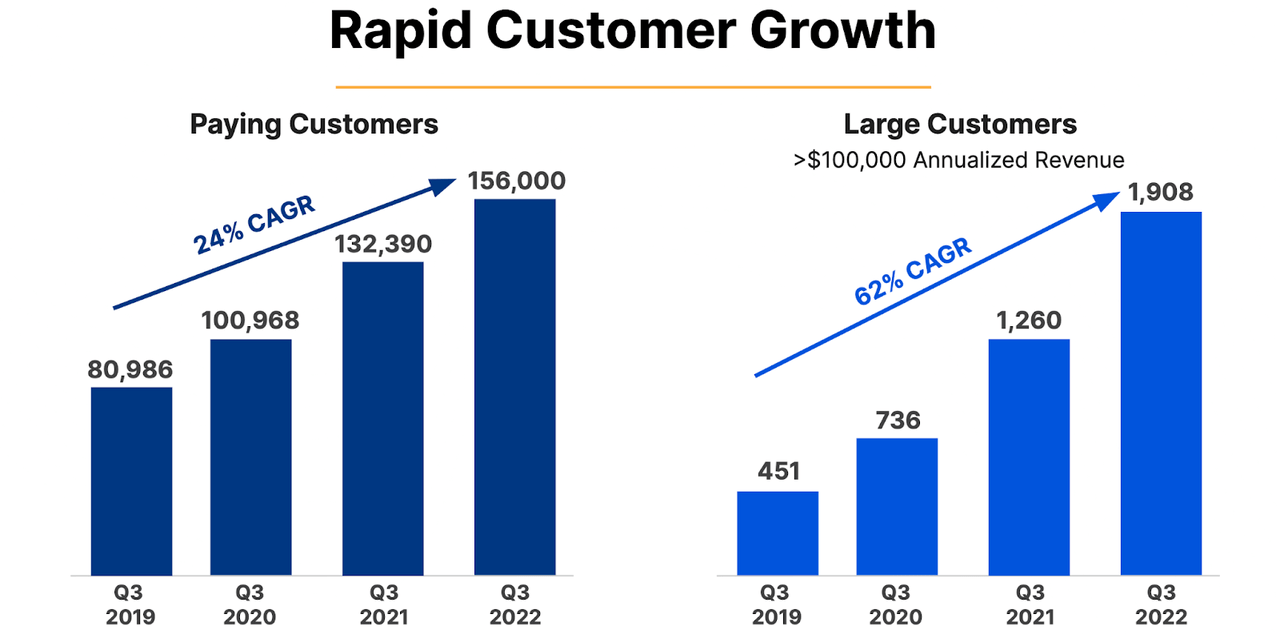

NET continued to grow its customer base, including 62% growth in its large customers.

2022 Q3 Presentation

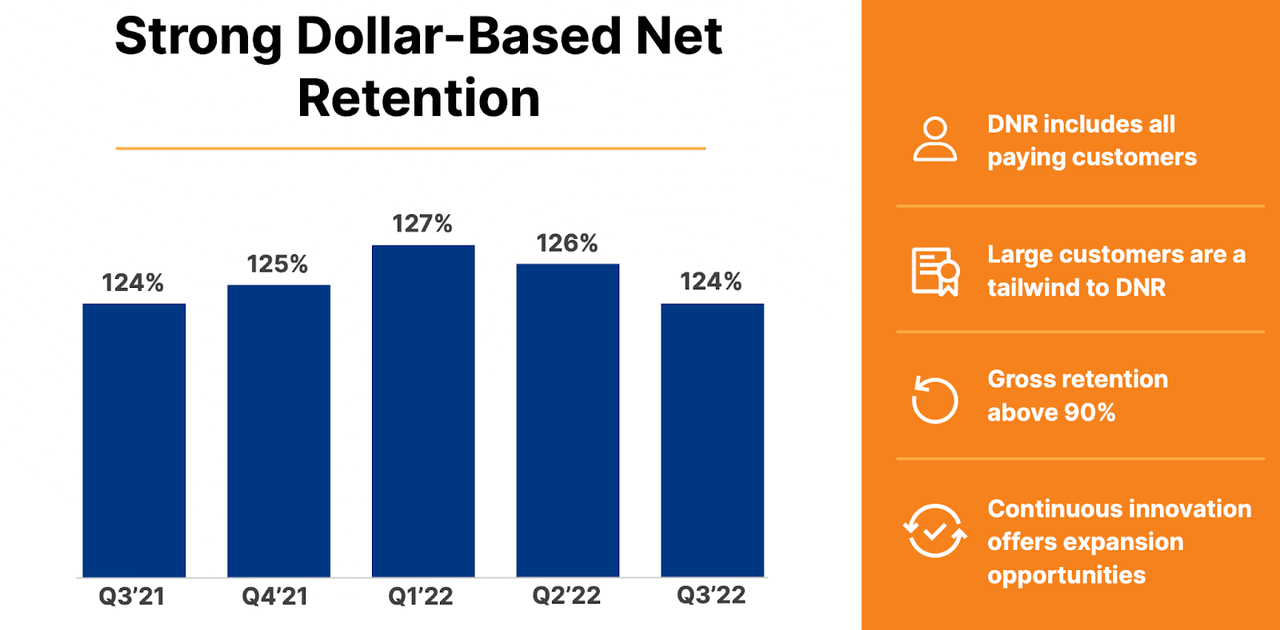

The most appealing draw of the stock is the high dollar-based net retention rate, which remained at 124%. Investors have focused on tech companies which can sustain strong growth rates even amidst difficult macro conditions – NET’s high dollar-based net retention rate should help it continue growing rapidly even now.

2022 Q3 Presentation

On the conference call, management noted that they will not be satisfied until the net expansion rate is over 130%, viewing that as being “very achievable” due to their storage-based products like Zero Trust and R2. The sequential decline in the net expansion rate was driven by less net expansion and not due to elevated churn.

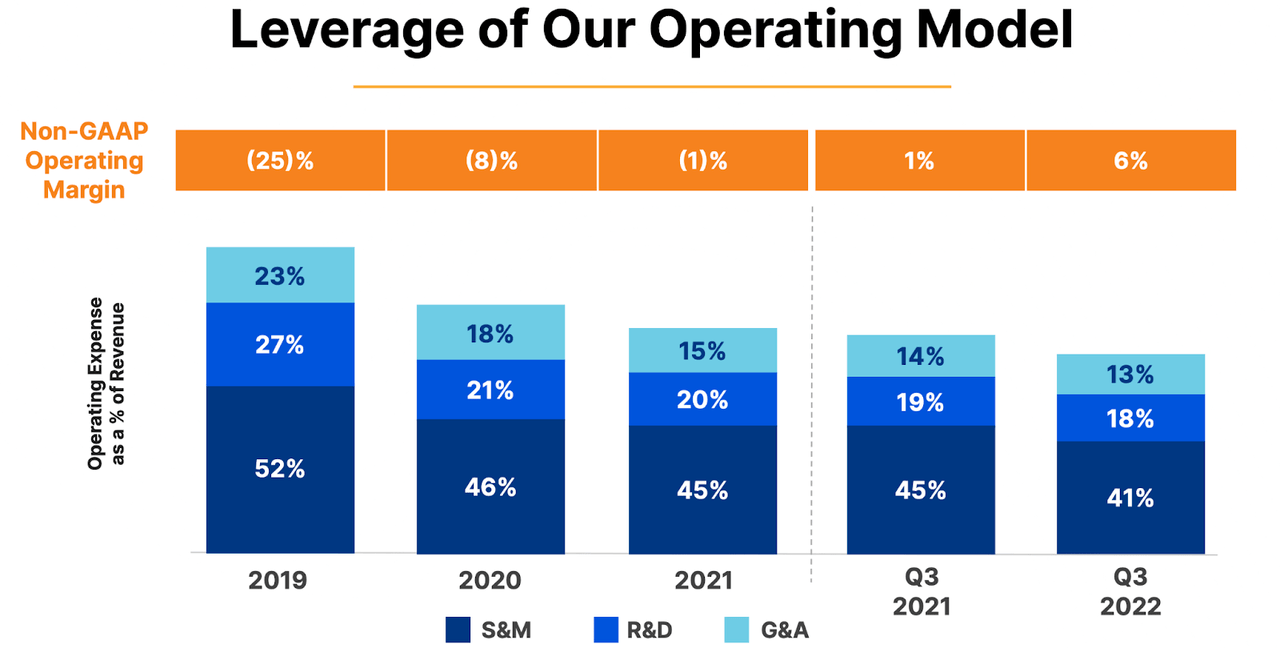

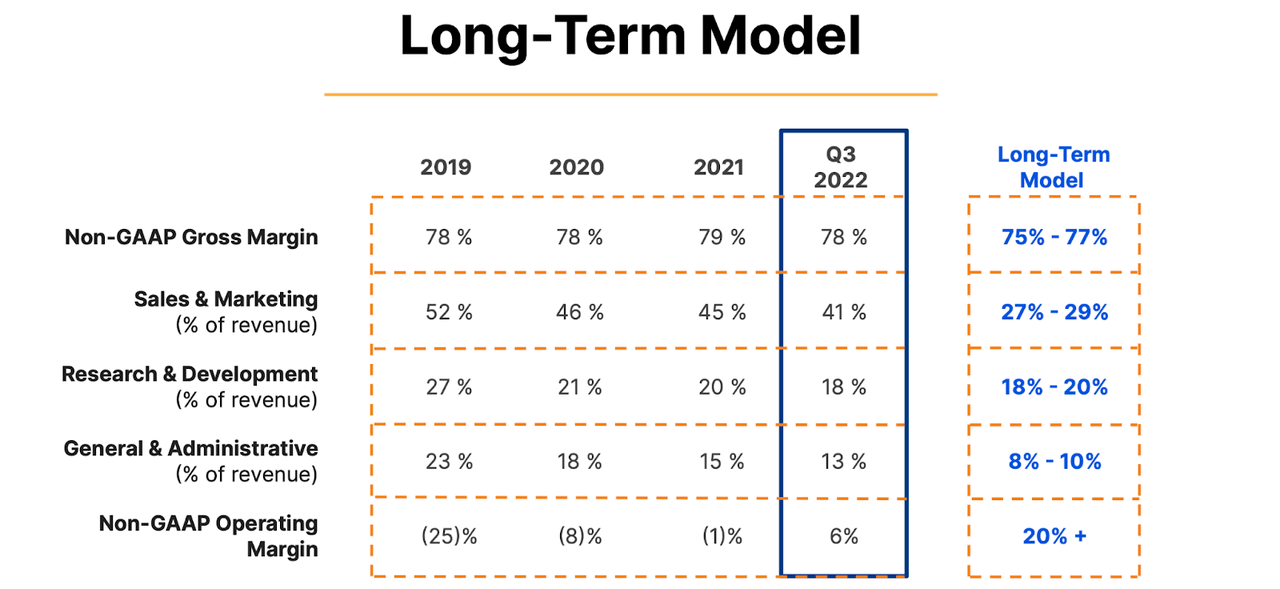

NET continued to see operating leverage, with non-GAAP operating margins expanding to 6%.

2022 Q3 Presentation

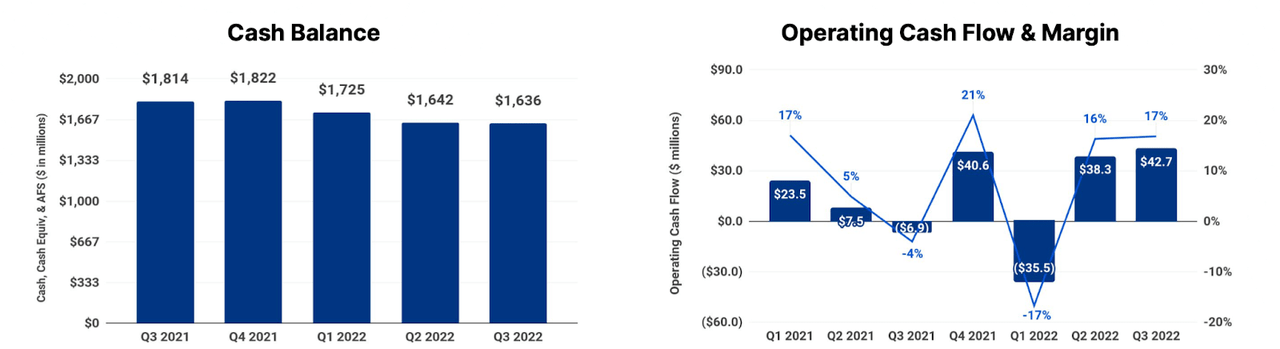

NET ended the quarter with $1.6 billion of cash versus $1.4 billion in convertible notes. That is a solid balance sheet position considering that NET is already operating near cash flow breakeven.

2022 Q3 Presentation

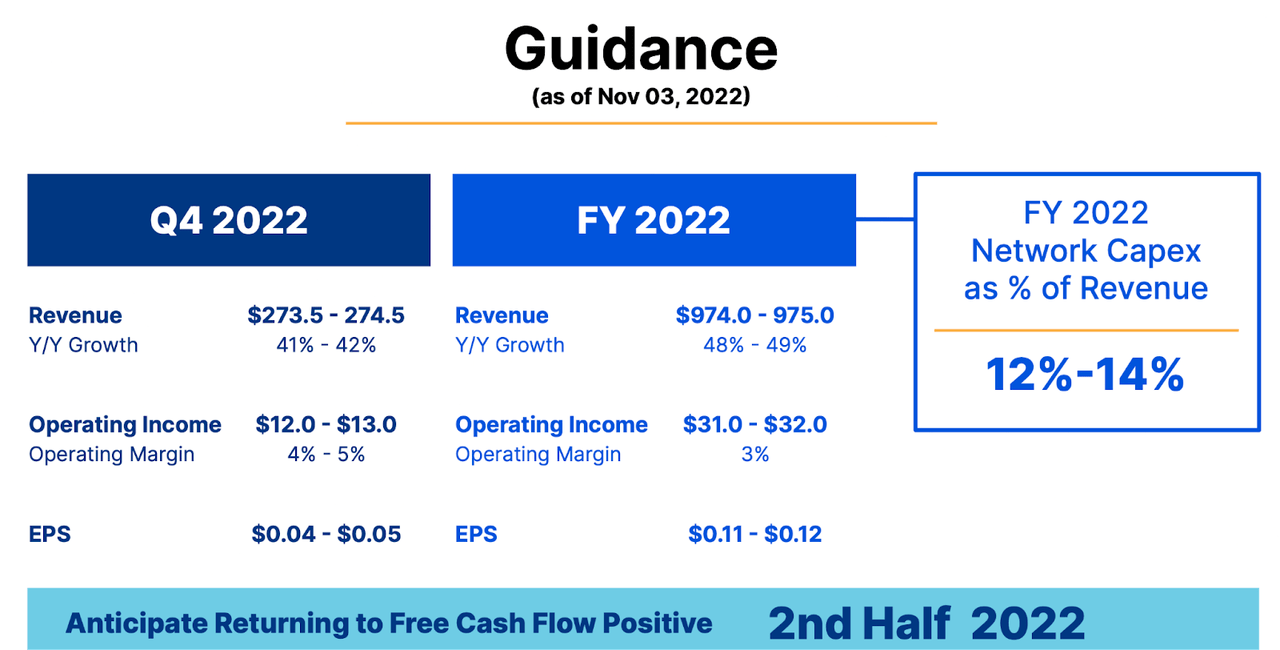

Looking ahead, NET guided to 42% revenue growth and for a return to positive free cash flow.

2022 Q3 Presentation

On the call, management also initiated long-term guidance, expecting to organically achieve $5 billion in annualized revenue over the next 5 years. That represents an approximate 39% CAGR over the next 5 years based on FY2022 guidance.

Is NET Stock A Buy, Sell, or Hold?

Before discussing valuation, we should remind ourselves of the compelling investment thesis. NET is a dominant content delivery network (‘CDN’) which has used its dominant position to offer additional services such as cybersecurity. NET is helping to power a faster – and safer – internet.

2022 Q3 Presentation

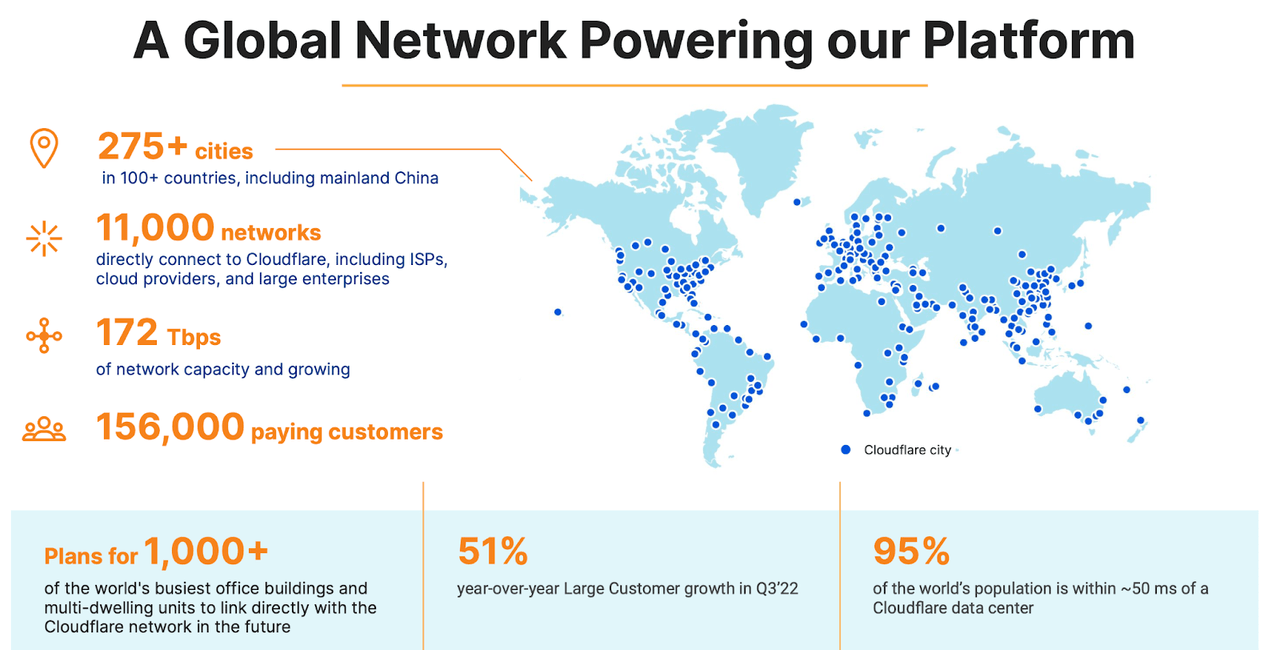

NET has built a large global network spread across over 275 cities and 11,000 networks. The large reach helps NET compete effectively against smaller operators.

2022 Q3 Presentation

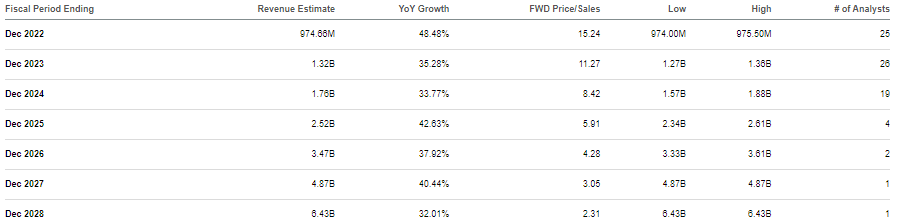

The stock might not look obviously cheap here. NET is trading at around 17x this year’s sales. Yet that multiple gets more reasonable quite quickly as NET works towards its goal of $5 billion in annual revenues by 2027. We can see below that consensus estimates call for NET to come just short of that target.

Seeking Alpha

Management has guided for at least 20% non-GAAP operating margins over the long term.

2022 Q3 Presentation

Assuming 20% long-term net margins, 30% growth, and a 1.5x price to earnings growth ratio (‘PEG ratio’), I could see NET trading at 9x sales in 2027, representing a stock price of $139 per share. That represents around 26% compounded annual returns over the next 5 years. Upside risks to that estimate include the possibility that NET trades at a higher 2x to 2.5x PEG ratio and downside risks include the possibilities that NET does not hit that target and/or does not continue to grow at 30% by then. Key risks to consider is that the current valuation is quite rich relative to more beaten-down tech peers and that is driven largely by sentiment as Wall Street has more confidence in the long-term growth story. If that sentiment turns sour, then I could see NET declining as much as 30% just to trade in-line with peers. NET faces stiff competition including from the likes of Akamai (AKAM) as well as mega-cap tech titans Microsoft (MSFT) and Alphabet (GOOGL). It is possible that as the market becomes more saturated, NET may see pricing pressure and difficulty sustaining rapid growth rates. I have discussed with subscribers to Best of Breed Growth Stocks that a carefully chosen portfolio of undervalued quality tech stocks is my preferred way to take advantage of the crash in tech stocks. NET fits right into such a basket as a higher quality allocation, as the valuation still makes sense for this top-tier operator. I rate the stock a strong buy for long-term tech investors.

Be the first to comment