David Tran/iStock Editorial via Getty Images

Clear Secure, Inc. (NYSE:YOU) offers a secure identity verification platform. If you’ve recently traveled through one of 46 major airports, you’ll likely have seen the “Clear” checkpoints as a separate lane in the security process. Clear Plus members enrolled in the company’s private biometric system bypass the initial step where TSA agents typically confirm travelers’ government-issued ID and boarding pass.

The service is particularly valuable to frequent travelers for the convenience of saving time and avoiding long lines. The platform is also featured in a growing number of sports arenas that have welcomed Clear as a security partner while also receiving a revenue share.

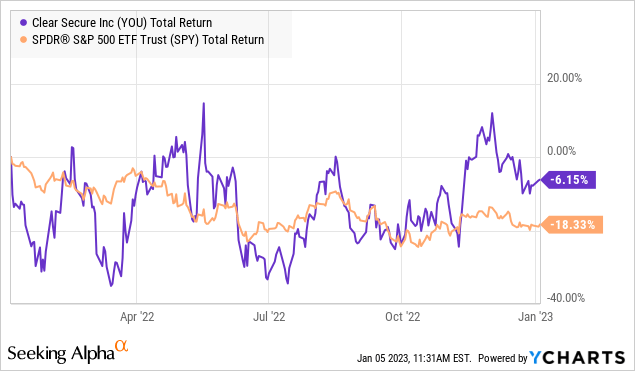

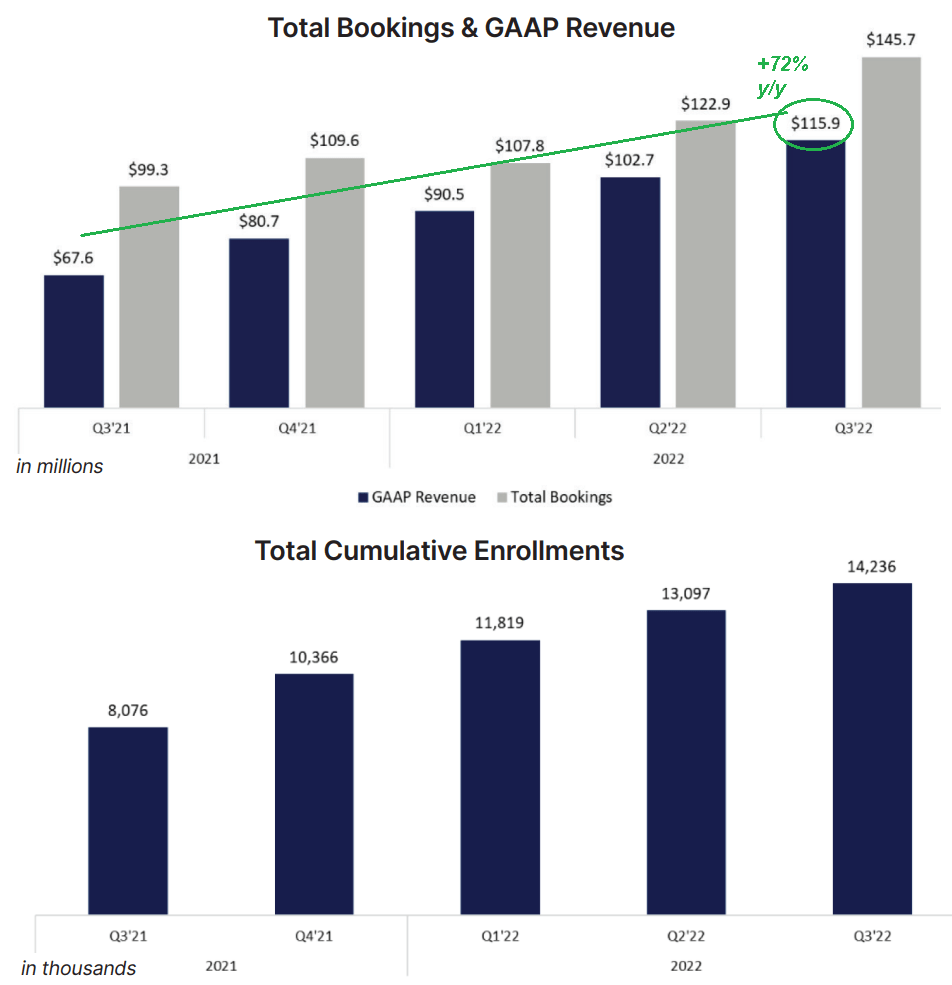

Following the company’s 2021 IPO, shares have been volatile amid the broader market selloff, although the setup here has seen some relative strength in the stock reflecting impressive growth and earnings trends. Indeed, the company last reported quarterly results marking the first quarter of positive EPS while the number of enrollments at 14.2 million climbed 76% from last year.

We like the stock with a sense that the business model benefits from several competitive advantages including a powerful network effect where growth snowballs as the program scales. We highlight ongoing initiatives to expand the company’s reach and customer value proposition which can represent a catalyst for firming earnings going forward.

YOU Key Metrics

YOU released its Q3 earnings in mid-November with EPS of $0.05, which beat estimates by $0.05 as consensus was looking for a flat result. Revenue of $116 million climbed by 72% year-over-year, with the strength largely driven by the recovery of the airline industry compared to pandemic disruptions at the start of 2021. Management notes success with in-airport and various partner channels driving memberships captured in a climbing number of bookings along with retention of customers.

On the financial side, keep in mind that there was a GAAP loss of -$65.6 million although this mostly reflected share-based compensation and the timing of the vesting from previously issued warrants. More favorably, the underlying shift towards profitability is evidenced by the adjusted EBITDA measure which reached $11.9 million compared to negative -$14.5 million in the period last year. The company also reported a positive free cash flow of $5.3 million.

The expectation is that earnings will maintain this more positive momentum going forward. For Q4, management is guiding for revenue of around $124 million, implying a growth rate of 54% compared to Q4 2021, and up 7% on a quarter-over-quarter basis.

Finally, we can mention Clear Secure maintains a solid balance sheet, ending the quarter with $700 million in cash and cash equivalents against effectively zero long-term financial debt. The position is strong enough that the Board of Directors declared a special $0.25 dividend which was paid in December.

source: company IR

Clear Secure’s TSA PreCheck Bundle

We mentioned Clear Pass focuses on the ID verification side of the airport screening process. The other step is the actual security area where travelers and carry-on luggage are checked for contraband.

In this case, the Department of Homeland Security (DHS) offers the “TSA PreCheck” option which is a separate paid program for passengers deemed a low risk to go through an expedited process by avoiding the removal of belts, shoes, clothing layers, and even leave a laptop store in a bag through the screening machines. The idea here is that the Clear Pass is complementary to TSA PreCheck with the attraction of having both being the fastest method of entering the airport boarding area.

Notably, Clear Secure is now offering a “bundle” of both services with a soft launch started in Q4 through an agreement with DHS which is likely to work as a boost to its marketing and tailwind for new enrollments. The airport operators benefit by essentially outsourcing an important part of the critical security functions while the TSA also benefits by reducing its headcount requirements helping to improve speed and efficiencies overall.

In many ways, Clear Pass is a win-win for all involved which we view as a strong point in the company’s outlook and investment profile. On this point, airlines like United Airlines Holdings, Inc. (UAL) and Delta Air Lines, Inc. (DAL) have partnered with Clear to promote the service as an option for travelers.

United directly invested in the company back in 2019 with the latest update being the option to sign up to Clear directly from the airline app since November. Clear Secure also works with American Express Co (AXP) where the Pass is offered as a perk on premium credit cards.

Clear’s Economic Moat

With the company’s history going back more than a decade, the game changer now is a belief that the operation has finally reached a critical mass with enough locations where the service can make sense to a wide range of travelers. This concept is related to the network effect where the value of the service grows as its user base expands.

The relationship with airports, the TSA, and commercial partners also creates a sort of barrier to entry as an intangible asset making it difficult for a competitor to attempt an alternative service. A high retention rate above 92% in the last quarter indicates customers are finding value in Clear Pass which represents a high switching cost of giving up the perks.

Furthermore, the platform is being utilized in other applications where security screening is a requirement and there is room to capture efficiencies in the process. Members of Clear Plus also have the option to use the features at entertainment venues and stadiums where a security line often forms.

Clear also offers a Health Pass which gained prominence during the pandemic with validation of COVID testing results and digitization of vaccine status that many types of business in certain areas embrace. Notably, this feature now integrates with Apple Inc.’s (AAPL) “Health App“.

What’s Next For Clear Secure?

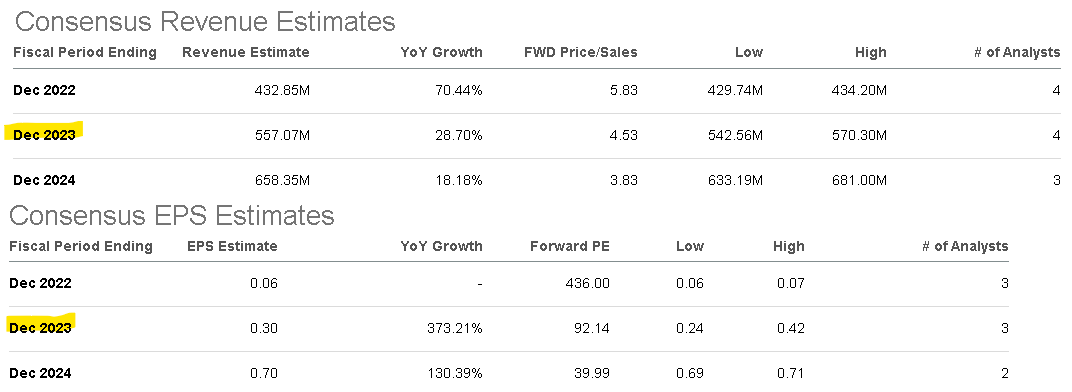

In truth, there are many companies with a good story and one of the lessons from 2022 is that operational momentum is often not enough to push a stock higher. That said, the most encouraging trend for YOU is its earnings trajectory is expected to accelerate. From a current consensus EPS of $0.06 for 2022 with the yet-to-be-reported Q4 results, the market is forecasting EPS to reach $0.30 in 2023, and more than double again towards $0.70 in 2024.

Beyond the higher base of enrolled members, the company should capture higher margins as operating expenses decline as a percentage of revenue. An ongoing international expansion is still in the early stages with the company regularly announcing new launches in various countries. Even at existing U.S. airports, availability at additional concourses and terminals also works as a growth driver.

By this measure, while the forward P/E of 92x highlights a lofty premium for any stock, the forecast for the top-line growth to average over 20% between 2023 and 2024, while EPS possibly increases more than 10 fold, can justify some of the optimism.

Seeking Alpha

Are There Risks?

The key for the company will be to maintain the pace of signups for new members while finding success in international markets. Longer-term, Clear Secure will need to become the global standard for secure identity verification not just in travel, but also leisure, and other industries with a visible presence in more and more countries as part of the bullish case.

The other side to the discussion would be the risk that growth simply begins to disappoint while the expected earnings fail to materialize. One concern is that the company may have already captured the “low-hanging fruit” of hard-core heavy business travelers where the Clear Pass makes the most sense, at least from the U.S. market. By this measure, doubling the number of cumulative platform users from here will be more difficult.

There is also an argument that if “everyone” is using Clear/TSA PreCheck, it begins to defeat the purpose of a priority security lane membership. It’s not there yet but could become a problem at certain airports if the platform is too successful. Going further, a skeptic would also point to the regulatory risks where the service no longer becomes viable based on changing laws in the future or even in a scenario of a headline-making failure in the system that would undermine confidence in the company’s security protocol.

YOU Stock Price Forecast

There’s a lot to like about YOU. We’re bullish, and see shares trading higher going forward with a buy rating and price target at $35.00, representing a 50x multiple on the current consensus EPS for 2024 at $0.70. Naturally, stronger-than-expected earnings would support a revision higher to market estimates and make shares appear even more compelling.

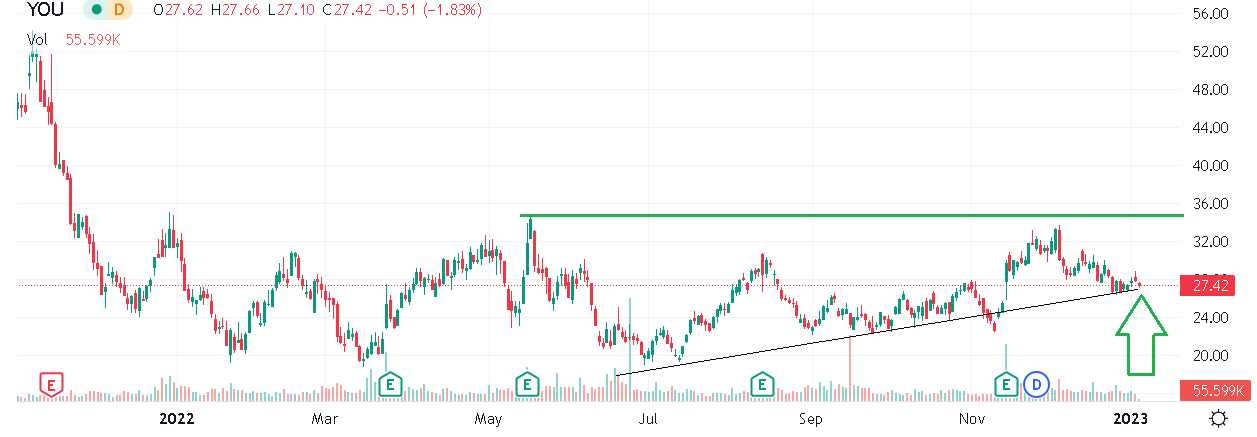

Our otherwise “modest” price target of 25% higher from the current level takes it one step at a time with a base case that shares will likely remain volatile in the near term against ongoing macro headwinds. We also recognize that expectations are high with the stock hardly a secret, which adds to downside risks in a scenario where the company misses estimates. Monitoring points during the Q4 earnings report, set to be released in late March, include margin trends and the pace of new signups.

Seeking Alpha

Be the first to comment