Alphotographic

Citigroup Inc. (NYSE:C) is scheduled to release its fourth quarter’s financial results on Friday morning (January 13). Although we’re always wary of what Friday the 13th might offer, we think the bank could beat its earnings estimates or, at the very least, showcase robust quarterly growth.

The American banking giant operates in a highly cyclical industry, meaning its earnings releases are usually eventful. However, we anticipate a more sustainable quarter than some of the firm’s preceding fiscal periods; here’s why.

Citigroup Earnings Estimates

Consensus

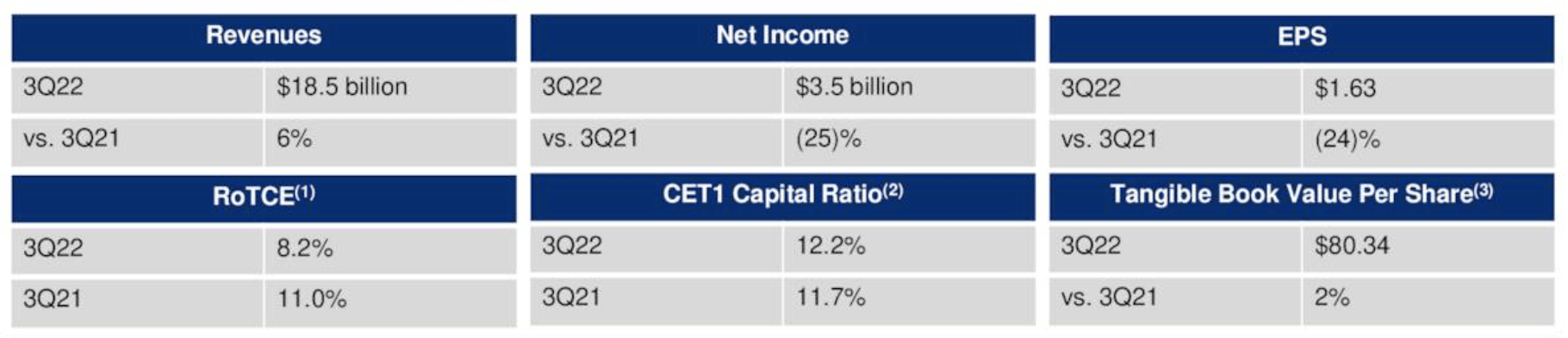

Citigroup crushed its third-quarter financial estimates, as it beat its revenue target by $230.60 million and its earnings-per-share midpoint by 20 cents. The firm’s earnings were assisted by an improved debt market and the divestiture of its Philippines consumer business for a profit of $256 million (which can be backed out of core earnings).

Despite the bank’s solid third quarter, analysts expect Citi’s fourth-quarter earnings to settle lower with revenue and EPS targets of $17.39 billion and $1.20, respectively.

Will the estimates materialize? Let’s do a deeper dive to find out.

Citi’s Earnings Estimates (Seeking Alpha)

Operational Discussion

Baseline

As previously mentioned, Citi posted better-than-anticipated results in its third quarter; however, input costs and impairments (from divestments) remained a concern as its earnings-per-share slumped by 25% year-over-year.

3rd Quarter Earnings (Citigroup)

We anticipate an alternative outlook going into the company’s fourth-quarter results. Interest rates have remained supportive of the enterprise’s debt portfolio, which makes up approximately 65% of its revenue mix. In addition to supportive interest rates and credit spreads, leading indicators such as improved credit card metrics are a positive sign.

As per its third quarter, Citi’s interest-based income rose by 12% year-over-year. But will this be sustained in the bank’s fourth quarter? We think Citi experienced additional income-based growth amid continued interest-rate hikes. In addition, inflation growth has moderated, which likely slowed its loan debt portfolio’s value decay. Thus, we won’t be surprised if another 12%+ year-over-year growth is reported.

Furthermore, Citigroup could report a marginal improvement in non-interest income. The bank’s third-quarter non-interest revenues dropped by 5% year-over-year. Although we think M&A activity has remained subdued, Citi could report a significant increase in other non-interest activities. For instance, the Bank’s CEO, Jane Fraser, recently mentioned that trading revenues could settle nearly 10% higher in Q4. Moreover, services revenue is generally less cyclical than a bank’s trading and debt segments; thus, we could easily see the segment’s 15% year-over-year in Q4 resume.

Non-Core Events – China Divestment

In other developments, Citigroup has closed its consumer banking business in China as part of its restructuring process, which will see it lend its resources to wealth management. Although the firm’s Q4 report might reveal significant restructuring charges, we consider this a non-core element, which should be added back to expenses for valuation purposes. Moreover, it’s anticipated that the pivot would bring about improved long-term results. Thus, market participants could see the announcement as positive.

Quantitative Analysis

The Beneish M-Score tracks a company’s accruals recognition, which conveys whether its earnings are being recognized prematurely or whether they’re lagged. Citigroup’s Beneish M-Score of -2.18 suggests it has recently been a conservative earnings recognizer, which limits the risk of downside earnings surprises.

Beneish M-Score (Gurufocus)

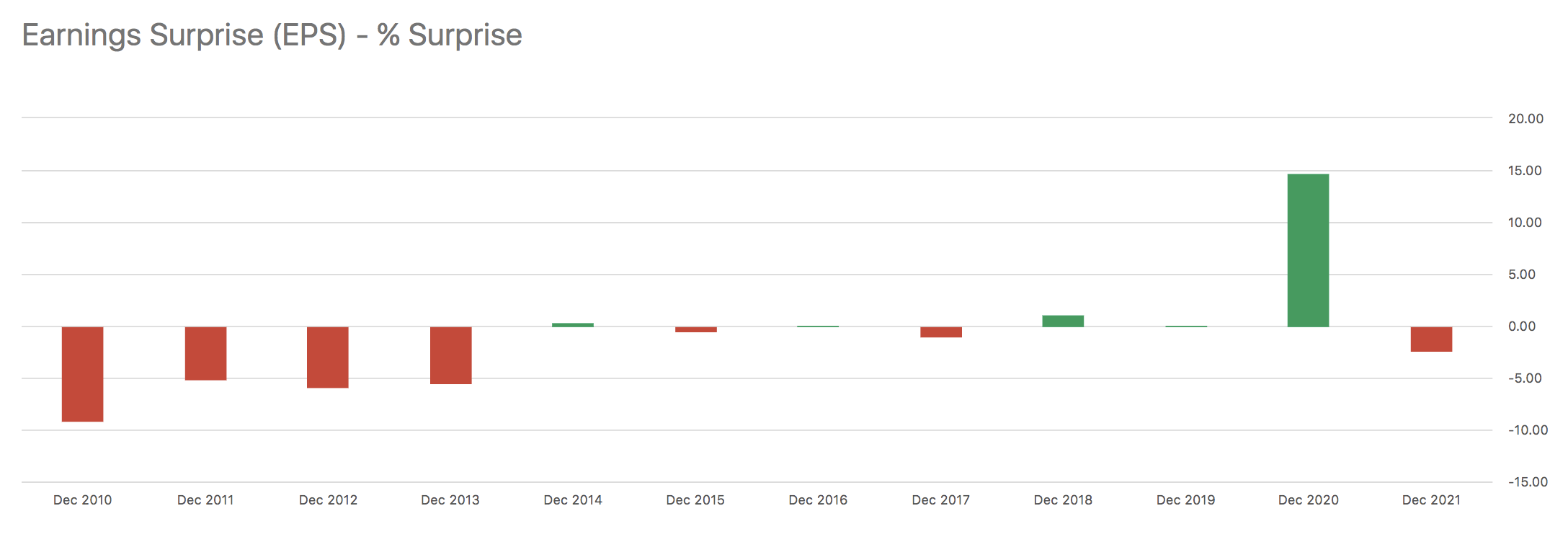

Even though the bank’s Beneish M-score is on solid grounds, Citi possesses a history of earnings crash risk as it has missed seven of its last 12 earnings-per-share targets. Earnings crash risk is a significant obstacle for a stock, as many investors consider the feature in cohesion with stock momentum crash risk.

EPS Surprises (Seeking Alpha)

Valuation & Return Prospects

Residual Income Model

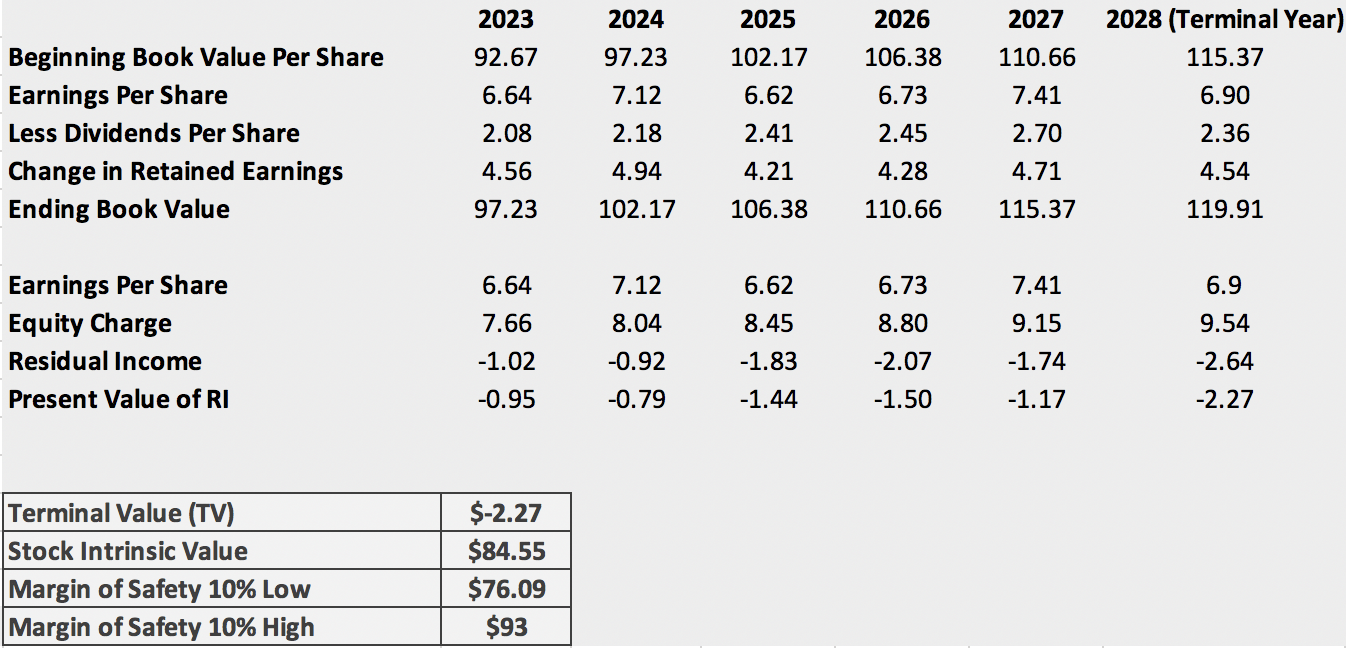

Our multistage residual income valuation model suggests that Citigroup’s stock is undervalued. Even if a margin of safety and possible restructuring EPS depletion are considered, Citigroup’s stock is trading well below its intrinsic value, which is parsimoniously communicated by its current price-to-book ratio of 0.55x.

Multistage Residual Income Model (Author’s Calculations)

Here’s how the model’s inputs were decided upon.

- The stock’s current market price was divided by its price-to-book ratio to establish a ballpark book value per share.

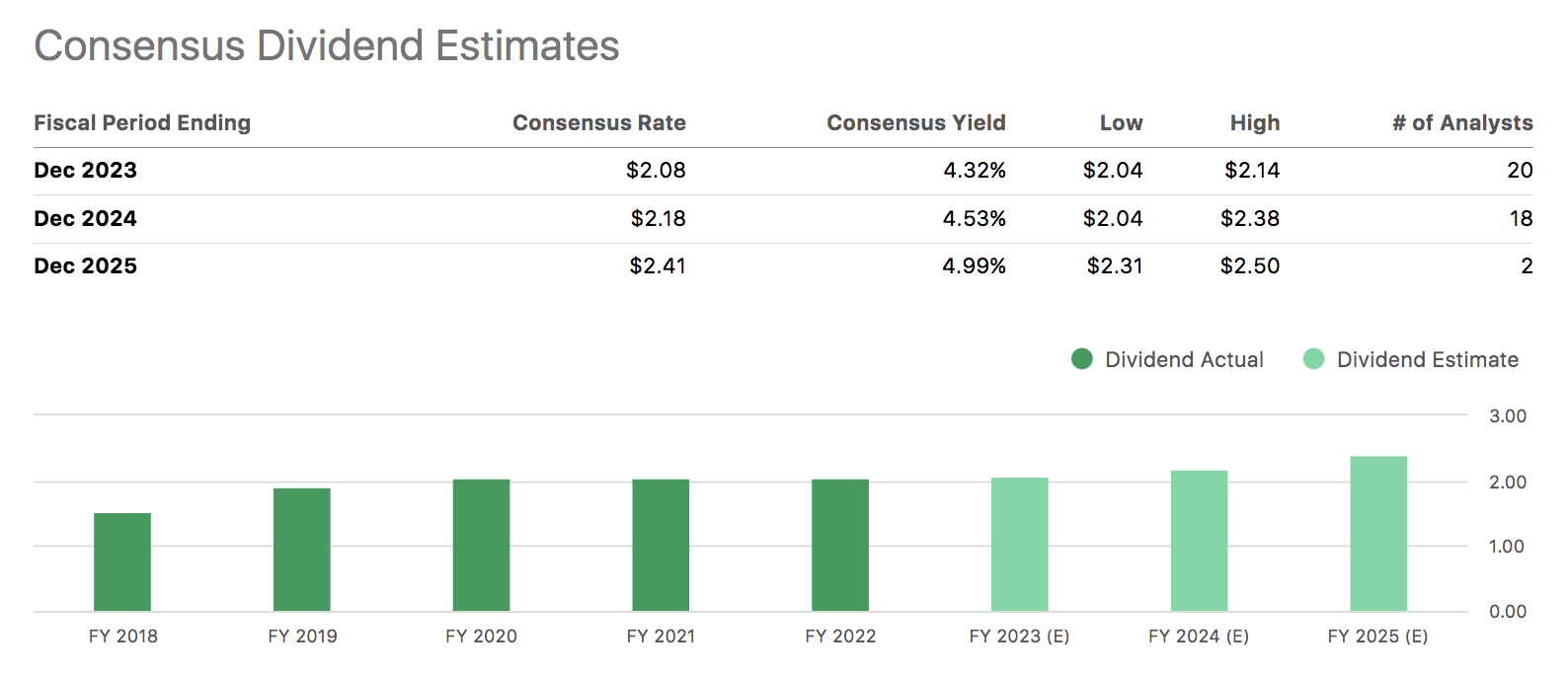

- Seeking Alpha’s database was utilized to discover analysts’ sample EPS and dividend estimates. Dividend estimates only stretch until 2024 (year-end); thus, ex-ante dividends were assumed to be in line with earnings-per-share growth.

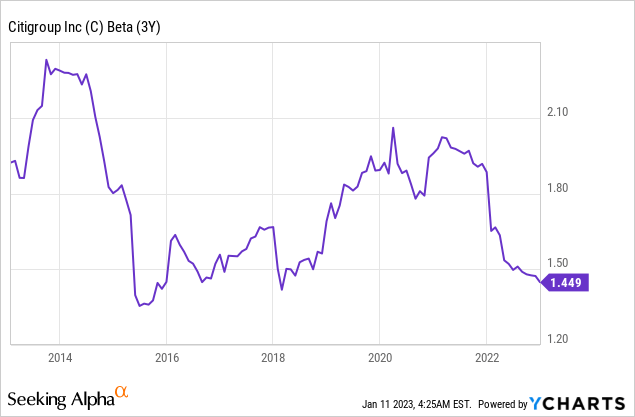

- The implied U.S. market risk premium was combined with the stock’s current beta coefficient to determine the cost of equity. The result was multiplied by each year’s beginning book value to estimate an equity charge.

- Lastly, the terminal year’s EPS and dividends were set to normalized averages. In addition, a persistence factor of 0.3 was added to the TV computation to account for Citigroup’s substantial market share.

Dividends

Citigroup’s historical shareholder compensation profile is robust. The stock’s current and forecasted dividend yield/s are “best-in-class” Therefore, investors have access to carry return, which phases out reliance on price returns.

However, keep in mind that Citigroup’s current restructuring process could diminish the stock’s dividend prospects to a certain extent.

Seeking Alpha

Concluding Thoughts

Citigroup’s fourth-quarter earnings report looms, and we believe the bank’s results will be favorable. Although risks such as investment banking depletion and restructurings persist, continued interest rate support and better trading profits might lead the way to an impressive Q4 report.

Forensic metrics provide an even contest; however, the bank’s stock is undervalued, and a marginal earnings beat could send Citigroup Inc. into stardom.

Be the first to comment