Ingus Kruklitis

Dear readers/followers,

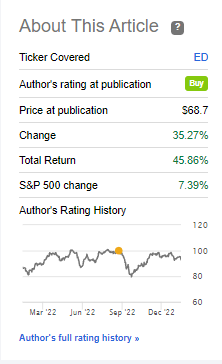

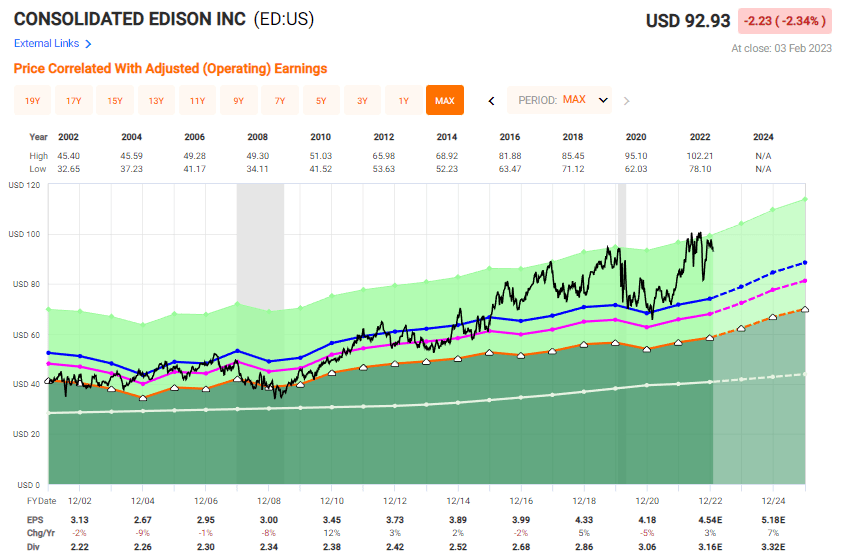

So, Consolidated Edison (NYSE:ED). I would argue that my overall returns and my success with regard to this investment are solid. This is due to my article coverage, which shows exactly how I’ve handled ED, since this, my first article on ED. I first covered ED in January of 2021, when the company was troughing close to $68/share and initiated a position with a bullish outlook.

The returns since then have been better compared to what you see below because I actually sold shortly before and after the neutral article visible on the graph. My RoR for ED has been closer to 50% including dividends.

ED article (Consolidated Edison article)

Because of the beatings the company takes from the political side of things, ED is more volatile than your typical utility stock. This is something we can take advantage of when investing in the company, and that’s exactly what I did when I invested and sold the stock. A simple thesis – it was buyable below $70, but don’t believe it is all that buyable above $90/share.

Let’s revisit ED for 2023.

Consolidated Edison – Revisiting for 2023

The company is a utility owning multiple subsidiaries in the typical fashion for a utility – Holdco and subs – in the eastern areas around New York. The ConEd company of New York, providing electricity and gas service in New York City and Westchester, is the top-tier company in the portfolio. ED also runs steam, which is one of the largest still-in-operation steam systems of its kind.

ED IR (ED IR)

The company has a 200-year old history, a solid dividend to enjoy, and it’s a crucial service covering the needs of 10 million people, which is almost the population of the entire nation of Sweden, where I live.

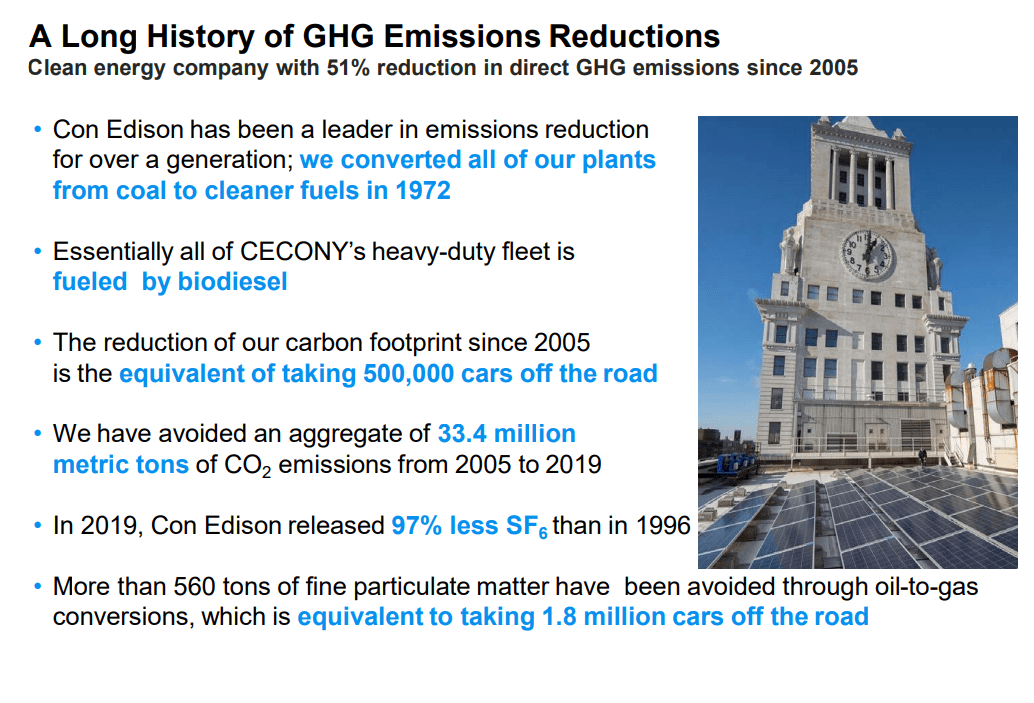

The company has been through the first steps of its “change” program, which has seen ED become one of the cleanest US utilities in existence. It’s not up there with companies like Ørsted A/S (OTCPK:DNNGY), which I own and cover extensively as well, but it’s solid nonetheless (and not really all that comparable to Ørsted A/S either, truth be told). The company has a history of such ESG reductions, and its current goal is to go 100% clean by 2040, which is in line with some of the EU targets here.

ED IR (ED IR)

This is also mostly in line with the goals of the State of New York. The market has obviously “bought” the way the company has been performing and these goals, given how the stock has performed over the past few years – for the most part at least.

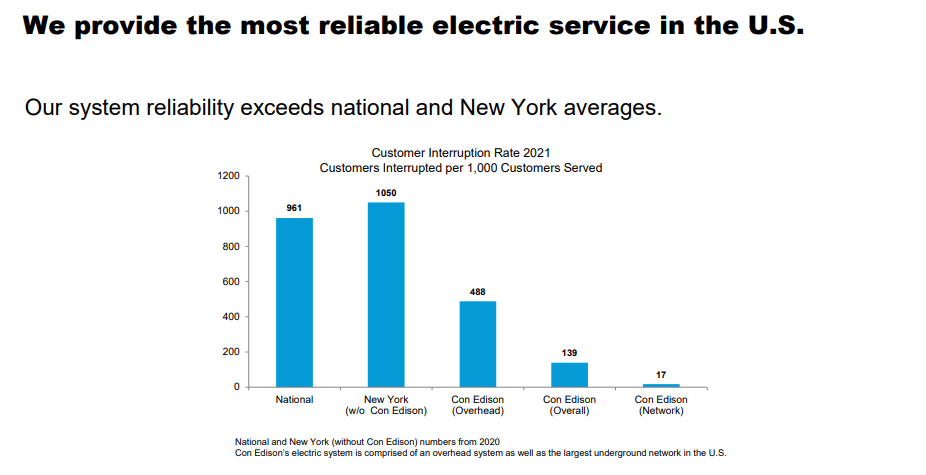

And the company certainly has arguments going for it, being one of the most reliable services all across the nation.

ED IR (ED IR)

I do not believe it an exaggeration to say that ConEd is probably leading the charge for ESG and green energy across the US. I find no company that’s going as “all-in” in terms of meeting climate goals, having their customers meet climate goals, and pushing for utility-owned renewables and utility-owned energy storage projects – many of which are already operational. The company is also one of few to host an annual “ESG presentation” with a corresponding call, which I do not believe any other utility on earth is currently doing – ED did this for the third consecutive year back in November.

I also believe it fair to say that if you don’t believe in the green energy push, then ConEd is not the investment for you, as their entire mission objective and operations are centered around this ambition.

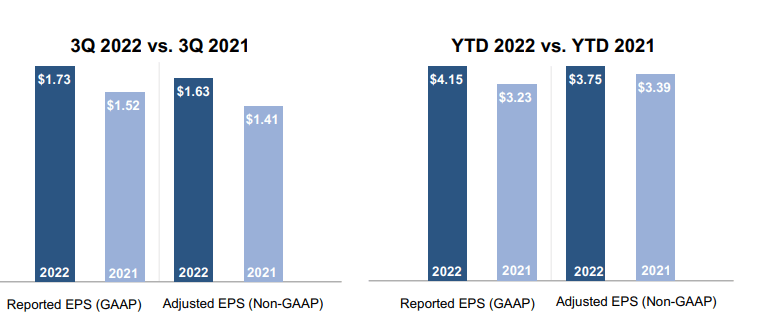

The company’s most recent earnings, the 3Q22, are good, enjoying a beat in earnings of over $0.15/share. since that report, the company has climbed somewhat, as one could expect given that these, in part, confirm the upside for what the company has been saying.

A few milestones are worth mentioning in 3Q. The company has decided to sell off CEBs to an RWE subsidiary.

ED IR (ED IR)

I have adjusted my own price targets and estimates accordingly in line with this push. It’s also a very important time for CECONY, with a 10-year total investment plan coming up to $68B between Clean energy, Core Service, and Climate Resilience. CECONY has also filed a rate case for its Electric/Gas services, and this is something to keep a very close eye on. The company wanted a 10% RoE and a 50% equity ratio – not outlandish by any means, but we need to remember that NY is a relatively complex political landscape – so these things are often clear. ED has plenty of investments that it needs to do, and there are up-costs of Pensions, remediations, storm costs, hardening costs, and other CapEx/OPex considerations. The rate base/corresponding numbers and earnings from the case for 2023 is currently showing lower than forecast for 2023, with an annualized increase in electricity of $867M, and $299M for Gas. The big push is in 2023, with smaller changes in the years 2024-2025. As you can see, the rate case response is not going the way the company wants, and 8.8% RoE is quite a bit lower than I personally forecasted here (9-9.5%), but reflecting the operating environment and the realities of where the company operates.

Still, the core of the company’s operations remains solid. Dividends and earnings are up, and the company relatively recently upped its dividend by a few percent. While the company share price is far from as stable as we would expect from a utility, the company’s underlying earnings are actually fairly stable.

ED IR (ED IR)

We can move on to valuation to see where 2023 finds ConEd, and what we should be doing in terms of investing, selling, or considering.

Consolidated Edison Valuation

With the latest results solid, the rate case is mostly acceptable – at least not thesis-breaking, we can review ED and state with clarity that this business remains one of the most premiumized utilities out there that you can invest in.

F.A.S.T Graphs ED (F.A.S.T graphs)

This company is pushing up at a premium of 20.37x, well above its average over time of 16.3x. Remember, the last time I bought, we were close to that discount of around 15-16x, and the company yielded above 4%. Now that yield is less than 3.5%, and even with a 5% annualized forecasted growth rate until 2025E, the returns here are dictated by the valuation you invest in, and how high the company goes.

ED’s premium has been rising for the past few years, growing higher and higher. While 16.3x is for the 20-year, the 5-year average premium is around 19x. The company is still overvalued here, just not as much. However, looking at what ED may generate in returns, grows tricky.

on a 19x forecasted P/E basis, we have no more than 7% annualized RoR, and that’s inclusive of dividends. Without dividends, it’s below 4%. Even forecasted to a 20-21x P/E forecast, the RoR here doesn’t crack double digits – nor 7% without dividends.

This is one of the core reasons why I would consider ED to be an absolute “HOLD” here. In fact, if you own it, I believe you should consider trimming at this point. The company has been this expensive, but it hasn’t been this expensive often, and for long.

ED Valuation Upside (F.A.S.T graphs)

The core of my thesis for ED here is the simple fact that I don’t see anything that could cause ED to be justified for a higher valuation. In terms of trends, and looking beyond further premiumization, I only see one direction that the company can go from here – down.

The sale proceeds from CEB are likely to be used to pay down debt and provide the company with the capital needed not to issue any more equity for its ESG plans in the near term. They will also probably buy back shares to fill the EPS gap that the asset sale creates – but all of this is already priced into the current valuation.

In simple wording, the way the company trades above $90/share already provides us with the most bullish of case outlooks for 2023 and the next few years. That means that ED, as I see it, is a “HOLD”.

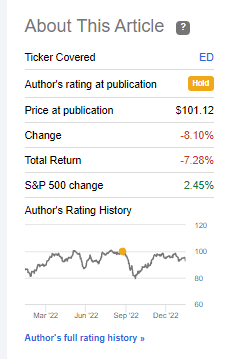

I call your attention to my last article on this company, and how you would have performed compared to listening to the ED bulls at that time.

Seeking Alpha ED article (Seeking Alpha)

My PT was $88/share. The company is still above that target, and my update with the new rate case the way it seems likely to go, and EPS forecasts as well as the sale of CEBs cause me to negatively adjust this PT slightly. I’m at $85/share at this point.

S&P Global analysts give the company an average starting at $70/share and going to triple digits – $100/share. However, almost 100% of the analysts agree with my stance here now. 14 analysts, with only 1 at a “BUY” with an average PT of $89.5, and 10 at “HOLD” with 3 Underperforms or “SELL”. That’s a sobering picture for this high-quality utility, and one I 100% happen to agree with.

At a 3.4% yield for a 20-21x P/E, I can easily, comparatively, get a far better upside, and far better yield at the same sort of fundamentals that ED offers me. There are utilities around the world that will take care of your capital equally well, but pay you better dividends, and are trading far cheaper.

I did not “BUY” back during the dip, unfortunately, that almost immediately followed my article. This was a mistake on my part, but I simply did not have the capital to spare at the time. Instead, we’re back to “HOLD” without seeing that dip-induced “BUY” here.

My initial 2023E thesis for Consolidated Edison is therefore as follows:

Thesis

My thesis for Consolidated Edison Is as follows:

- Consolidated Edison is a top-quality utility with a great set of assets and a good set of fundamentals. At the right valuation, the assets here are backed by incredible safety and a good geographical population base.

- However, unless the valuation is right, you’re at risk of putting your capital to “work” at below-7% annualized RoR even with yield.

- At the current valuation, I would consider this company to be a “HOLD” and a rotation target due to overvaluation. I trimmed it and sold it off to watchlist status, and I believe you can consider the same.

- I consider ED a “HOLD”. PT is $85/share.

- Selling put options is not valid either – the company is too expensive for that to be of interest.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- The company is currently cheap

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Due to not fulfilling my valuation-related criteria, this company warrants only a “HOLD”, and I believe you can rotate it here.

Be the first to comment