M-A-U/iStock via Getty Images

Climate economy companies are straight up not having a great time, with EV manufacturers, charging infrastructure plays, and battery developers all having suffered marked pullbacks over the last 12 months. The reasons for the fall are multifaceted from rising Fed fund rates to growing recession fears, but none though have to do with the overall trajectory of EV sales. EV sales figures for 2022 are out. They’re strong and point to just how entrenched the transition to the low emission vehicles has become. In the United Kingdom, one of ChargePoint’s (NYSE:CHPT) largest European markets, sales of EVs overtook diesel-powered cars for the first time and accounted for 16.6% of new registrations in 2022. In the United States, EV sales surged to new records with 807,180 EVs sold, around 5.8% of total vehicles, up from 3.2% of all vehicles sold in 2021. This was against an 8% fall in total US auto sales as supply chain bottlenecks and rising Fed fund rates disrupted the economically sensitive auto market.

I’m bullish on the industry, it’s the future of passenger transport and could be a generational opportunity as the global transportation architecture gets redrawn around net-zero lines. EV charging companies occupy a key position in this architecture of the future and ChargePoint, as the largest of such companies, is already playing a significant role in building the most expansive global EV charging network. The company is the largest pure-play EV charging company. Think of it like a gas station at a very rudimentary level, but for the fast-growing number of EVs on the road. This drives a positive relationship with EVs as more charging points address range anxiety, a factor preventing broader EV uptake.

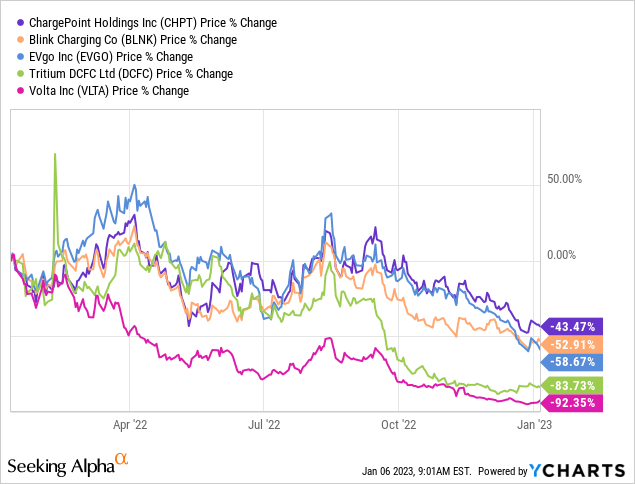

ChargePoint’s dominant status has meant it’s outperformed its peers amidst the retracement seen across its industry over the last 12 months. Its common shares are down around 43.5%, versus 53% for Blink Charging (BLNK) and 92.4% for Volta (VLTA).

The Future Architecture Of Transport

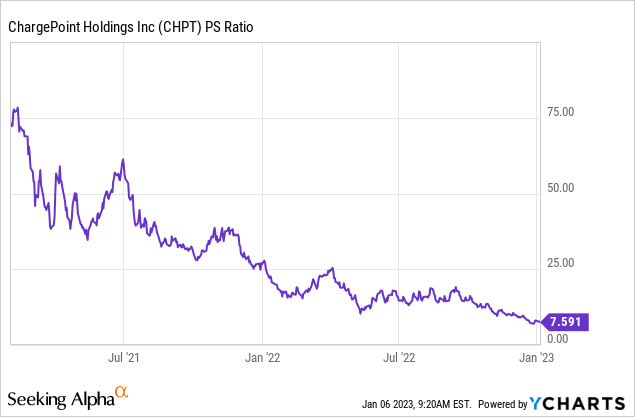

Whilst ChargePoint’s 7.6x trailing 12-month price-to-sales ratio is still materially higher than its peer group median of 1.28x, it’s at its lowest level since the Campbell, California-based EV charging company went public in February 2021.

Further, whilst a 7.6x PS sales multiple looks steep, it’s important to place this in context. The company last reported earnings for its fiscal 2023 third quarter, ending October 2022. This saw revenue come in at $125.34 million, an increase of 92.7% over the year-ago quarter but a miss of $6.78 million on consensus estimates. Revenue is essentially almost doubling on a year-over-year basis.

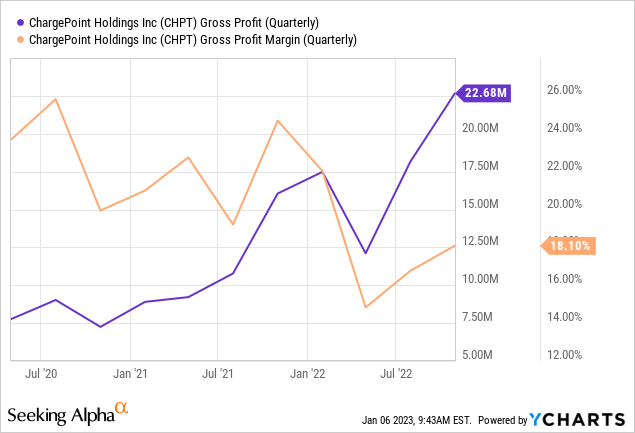

Bears would be right to flag that not only did the company underperform consensus, but it also continues to be intensely unprofitable. The company’s gross profit margin has continued a downtrend, notching 18.1% during the third quarter, down around 650 basis points from 24.7% in the year-ago period. The earnings call was somber, with management stating supply chain constraints and logistics disruptions presented challenges to gross profit that they continue to try to navigate. How much shareholders are willing to pay for unprofitable growth will play a huge role in the direction of the commons this calendar year. This comes against cash burn from operations during the quarter that came in at $83 million, up from $48 million in the year-ago period.

The Bulls Or Bears Could Have Tomorrow

Against $397.6 million in cash and equivalents as of the end of the third quarter, the rate of burn looks unsustainable and places the current expansion roadmap under a level of uncertainty. The cost of raising debt or equity capital has risen materially over the last 12 months and the current run rate, assuming cash burn from operations is constant, is just under 5 full quarters. Hence, the company will likely have to raise more capital this calendar year.

The risk here is a dilutive secondary offering would be against a possible recession and rising Fed fund rates could see an extension of the current market angst around the company’s high multiple. However, with current long-term debt at just less than 10% of their market cap, there is room for this non-dilutive source of funds to be tapped in my view. This comes as the overall number of EVs on the road continues to increase, driving a visceral need for more charging infrastructure.

In the UK, just 23 charging points are being installed daily, a big shortfall of the 100 a day expected to meet ambitious net-zero targets. This shortfall is likely reflected across North America and Europe. More charging points are needed and ChargePoint is building this. In the US, sales of EVs are expected to grow to around 20% of the total cars sold in any single year by the end of the decade, a milestone that would need current charging infrastructure to grow by close to 4x. Hence, there is significant growth ahead, and the bulls could very well see this retracement as an opportunity to expand their position. Fundamentally, the 2023 macro environment will dictate the performance of the commons and could see bears pull off another good year if recession fears come true. I’m bullish on the industry but neutral on ChargePoint here.

Be the first to comment