Leonid Sorokin

Introduction

I’ve covered telecommunications and electric vehicle (EV) infrastructure company Charge Enterprises (NASDAQ:CRGE), two times on SA so far, the latest of which was in October. Back then, I said that the financial results for Q2 2022 showed that there just aren’t any economies of scale in the telecommunications segment while the income from operations from the infrastructure segment is too low to make a difference.

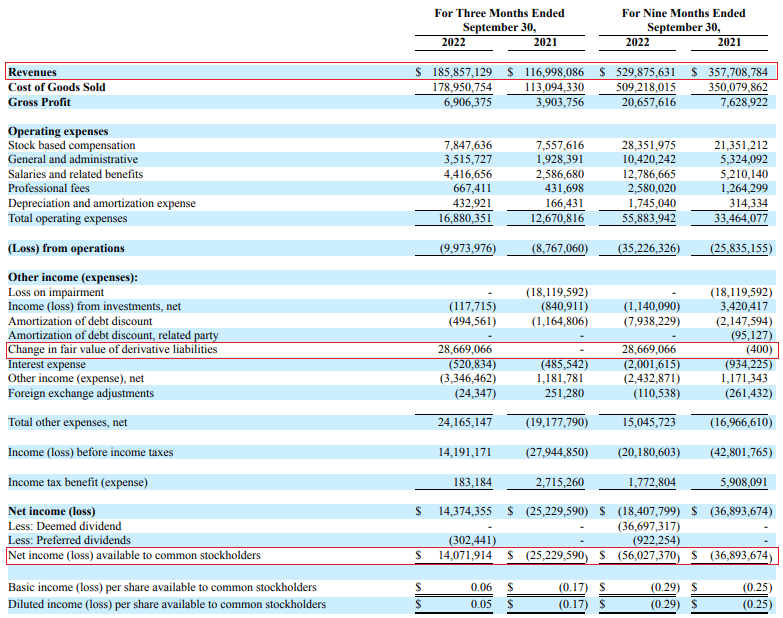

Well, Charge Enterprises posted a $14.1 million net income for Q3 2022 but the reason behind this is a significant change in the fair value of financial liabilities, mainly due to a smaller liability on outstanding warrants as the share price has decreased significantly. The loss from operations was $9.97 million while cash and cash equivalents declined by $10.4 million quarter on quarter. In my view, it’s unlikely that Charge Enterprises manages to avoid significant stock dilution in 2023. Let’s review.

Overview of the Q3 2022 financial results

In case you haven’t read any of my previous articles about Charge Enterprises, here’s a brief description of the business. The company was established in January 2019 and between October 2020 and January 2022 bought several firms involved in telecommunications and wireless telecommunications network and EV charging infrastructure installation. Today, the telecommunications arm of Charge Enterprises provides routing of voice, data, and short message services to carriers and mobile network operators globally, with contractual relationships with service providers across 19 foreign countries. The infrastructure division, in turn, focuses on the construction of wireless network elements such as cell towers as well as the installation and maintenance of EV charging stations and infrastructure.

Charge Enterprises

Turning our attention to the Q3 2022 financial results, we can see that revenues rose by more than 58% year on year to $185.9 million but we’re not comparing apples to apples here as EV Depot was bought in January 2022 while BW was acquired in December 2021. Looking at the net income for the quarter, the reason Charge Enterprises got into the black is a $28.7 million change in the fair value of derivative liabilities, which is tied to the liability on outstanding warrants. As the share price decreases, this gain rises and the past couple of months haven’t been kind to the investors in the company.

Charge Enterprises

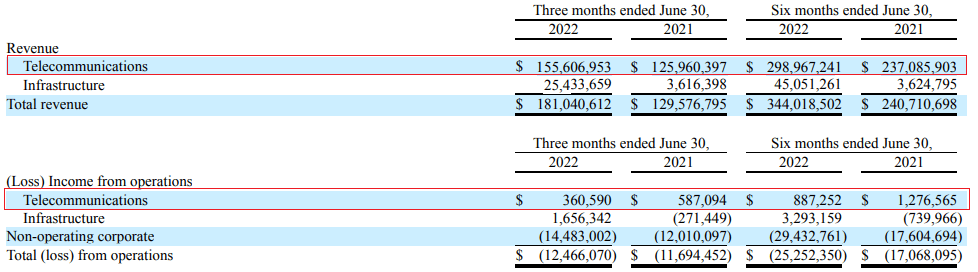

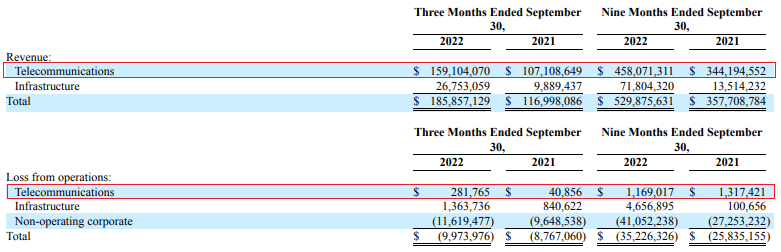

Unfortunately, Charge Enterprises doesn’t provide pro-forma results, but we can compare the Q3 financials to the ones from Q2. Overall, the situation looks grim as revenues inched up by just 2.66% and the majority of the growth came from the low-margin telecommunications business. In addition, the operating income of the infrastructure segment shrank by almost 18%.

Charge Enterprises Charge Enterprises

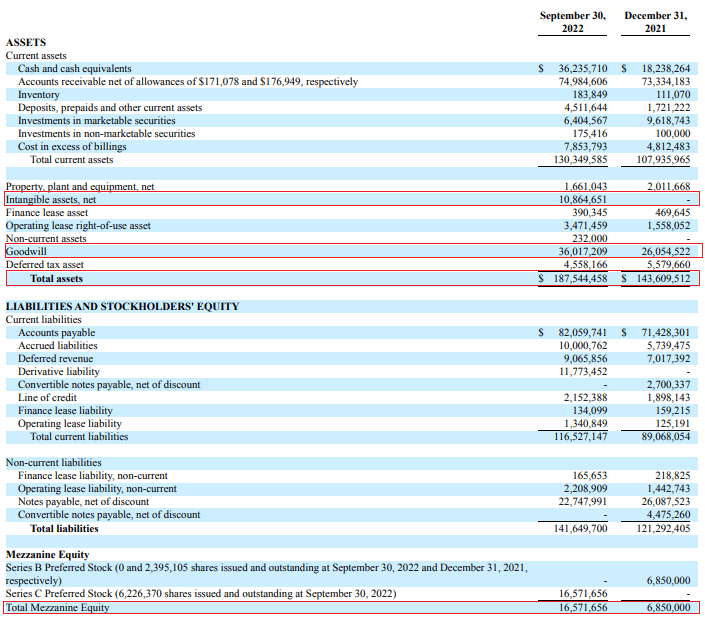

I expect the revenue of the infrastructure division to increase somewhat over the coming months as Charge Enterprises recently inked a deal with New York-focused parking management provider City Parking to provide custom EV charging infrastructure solutions. The latter has a network of 135 owned and operated locations in the New York City Area. However, I doubt that this contract is large enough to put Charge Enterprises within striking distance of becoming profitable as operating expenses have surpassed $11 million per quarter. In my view, this is a major issue as net cash used in operating activities stood at $18.6 million in Q3 2022 alone and cash and cash equivalents declined by $10.4 million quarter on quarter to just $36.2 million. In addition, the tangible book value was negative as of September 2022.

Charge Enterprises

Unless the fundamentals of the business improve drastically in the near future, I think that a significant capital increase to fund operations in 2023 seems inevitable.

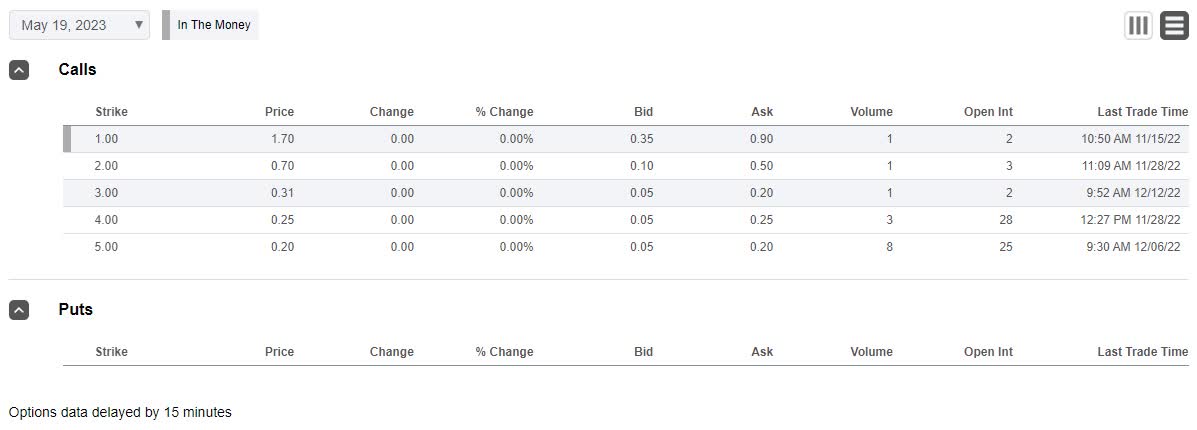

In my view, short selling seems viable as data from Fintel shows that the short borrow fee rate stands at just 6.69% as of the time of writing. The short interest is 4.2% of the float and there are call options available to hedge the risk. However, they are expensive, e.g., $1.70 for call options with a $1.00 strike price in May 2023.

Seeking Alpha

In addition, this is an illiquid stock, and it takes over 11 days to cover. It might be best to avoid Charge Enterprises.

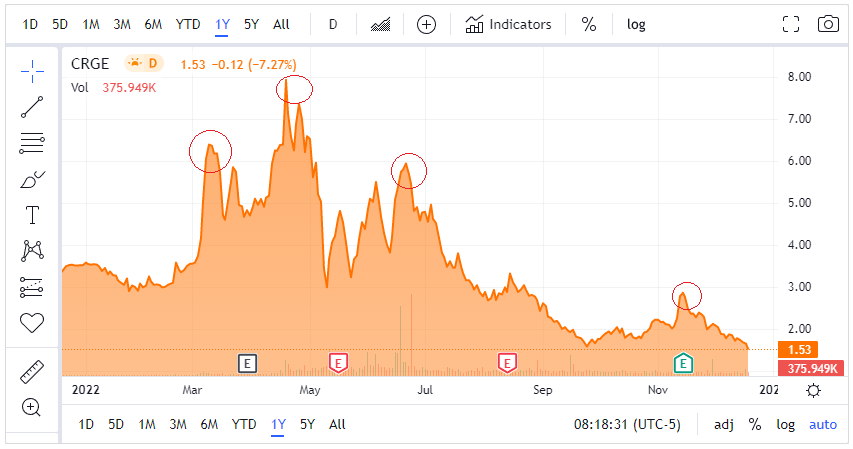

Looking at the risks for the bear case, I think that there are two major ones. First, I could be wrong about the small size of the City Parking deal and that this contract enables Charge Enterprises to turn its business around. Even if this is a small deal, it’s possible that several similar ones will be inked in the coming months. Second, the share prices of microcap companies can sometimes increase for spurious and unknown reasons, and this has already happened several times here in the past year alone. It’s possible that it will happen again in the near future.

Seeking Alpha

Investor takeaway

Charge Enterprises rapidly grew its annual revenues above $700 million thanks to several acquisitions since late 2020 but I think that there is little value in the business at the moment. Revenues barely grew in Q3 2022 and most of them seem to be coming from voice and data termination services, which is a notoriously low-margin business. Cash is starting to run out and I think that significant stock dilution is likely to take place in the next few months.

The short borrow fee rate seems low enough to make opening a small short position viable. However, call options are expensive and it takes over 11 days to cover. I think it’s best for risk-averse investors to avoid this stock.

Be the first to comment