Ron Levine/DigitalVision via Getty Images

Just six months ago, I wrote on Centamin (TSX:CEE:CA) (OTCPK:CELTF), noting that the stock would become attractive below US$0.96 with its turnaround thesis intact and a better 2023 ahead from a margin standpoint. While the gold price didn’t provide much help since the article ($1,860/oz vs. $1,790/oz), Centamin PLC (“Centamin”) has outperformed its peer group, finishing the year in positive territory and putting up an impressive ~50% return in H2 2022. This significantly exceeded the GDX’s negative return last year, which can be attributed to the stock becoming attractively valued below US$0.95 and its solid execution and delivery into guidance in a challenging environment. Let’s take a closer look below:

Sukari Mine Operations (Company Presentation)

All figures are in United States Dollars unless otherwise noted.

Q3 Results

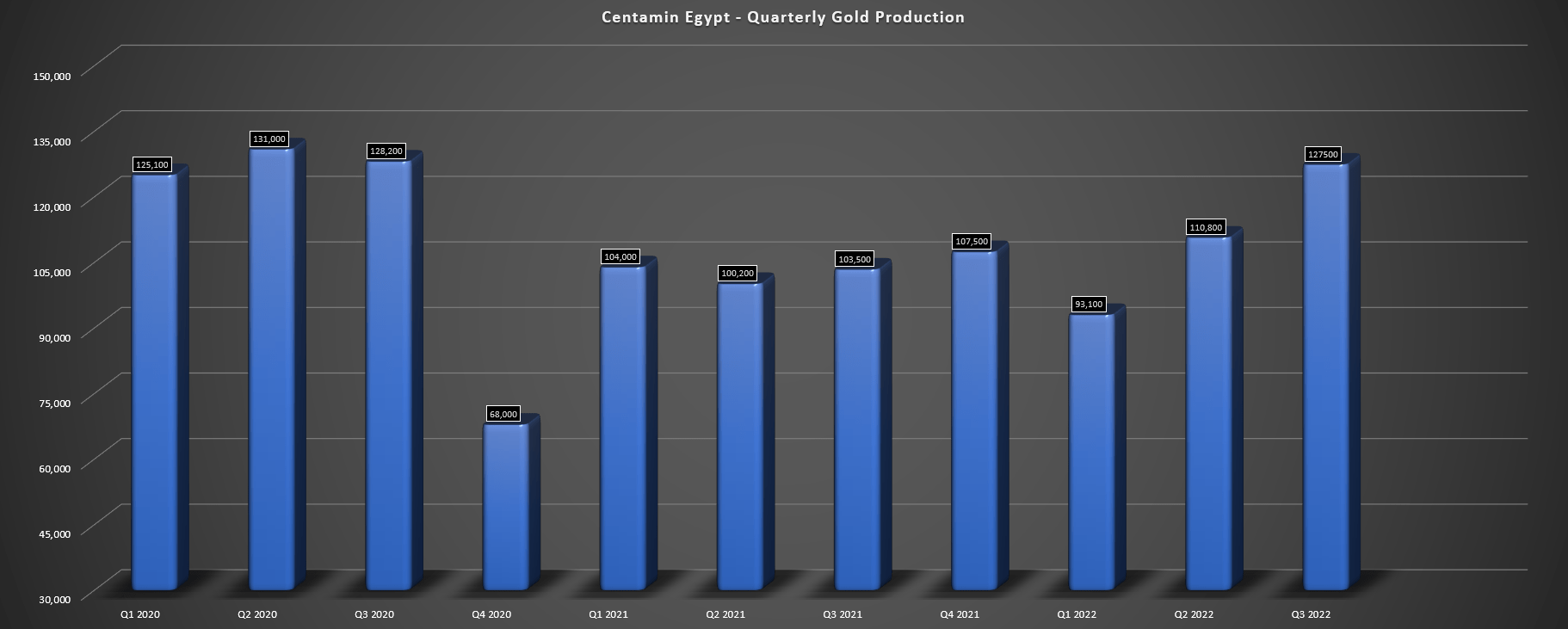

Centamin released its Q3 results in November, reporting quarterly gold production of ~127,500 ounces, a 23% increase from the year-ago period. This solid performance was driven by higher tonnes processed and better grades, with 3.23 million tonnes processed at 1.37 grams per tonne of gold, up from ~2.89 million tonnes at 1.29 grams per tonne of gold in Q3 2021. Notably, it was a record quarter for safety performance (now 5 million hours LTI free), the company’s solar plant was commissioned, and it was a record for total material moved during a quarter (35.6 million tonnes). Plus, the increased investment over the past two years has paved the way for several strong years ahead at its Sukari Mine in Egypt.

Centamin – Quarterly Gold Production (Company Filings, Author’s Chart)

In terms of major investments, the new Sukari solar plant is currently saving up to 70,000 liters of fuel per day or well over 20 million liters per annum, all while Centamin is enjoying lower fuel prices which look to have peaked in Q2/Q3. Meanwhile, the company has seen more underground productivity after switching to owner-operator vs. contract mining. In addition, Centamin expects further productivity gains with the arrival of a new underground fleet last quarter. Finally, all of Centamin’s trucks have been fitted with high-production truck trays; the company is working to boost recovery rates to ~90% at its plant, and it’s working on completing its paste-fill plant.

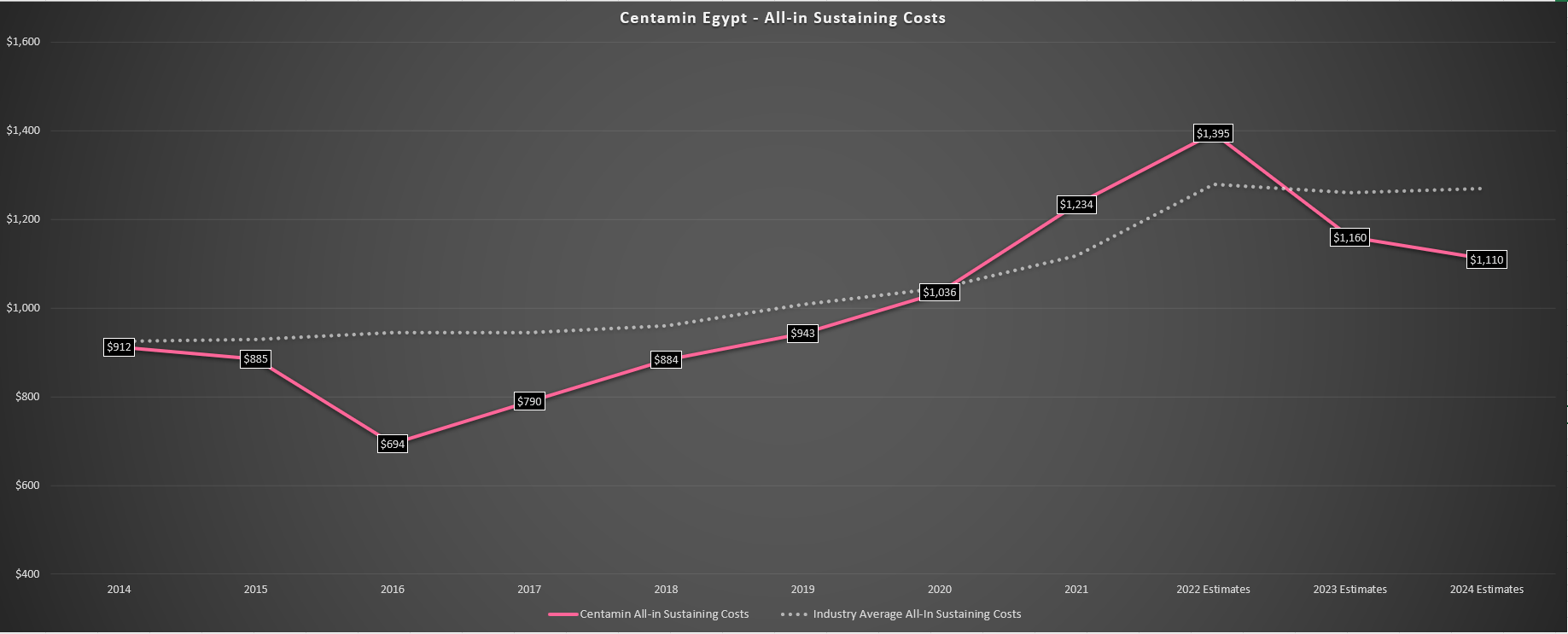

Centamin – All-in Sustaining Costs vs. Industry Average (Company Filings, Author’s Chart)

Given that Centamin was working against significant inflationary pressures in 2022 and its cost optimization work has not come to fruition, all-in-sustaining costs [AISC] are expected to spike again in 2022 ($1,395/oz estimates vs. $1,234/oz in FY2021) when combined with elevated sustaining capital. However, with a lower diesel price and diesel savings in 2023 (solar plant), a full year of benefits from improved productivity underground, and slightly lower sustaining capital, we should see significant cost improvements over the next two years. In fact, I would expect Centamin’s AISC to dip below $1,170/oz in FY2023 and potentially below $1,125/oz in FY2024.

There are other potential optimizations that Centamin is looking at currently, including an expansion of Sukari Underground to 1.5 million tonnes per annum for very modest capex ($35 million at the high end). This would involve ventilation upgrades, additional underground development, a larger mining fleet, and a potential expansion to its paste-fill plant. Meanwhile, the company is also looking at a grid power study to deliver grid power to Sukari, which could fully displace diesel fuel at the mine. Egyptian grid power is generated from n natural gas and renewables (hydro, solar, wind), providing further savings, with grid power being lower-cost and one reason that Agnico Eagle (AEM) stands out as a low-cost producer with economies of scale (300,000+ ounce per annum operations) and access to grid power in the Abitibi Region.

Sukari Gold Mine With Potential Grid Connection (Company Presentation)

To summarize, while Centamin was certainly not the most attractive producer from a margin standpoint in FY2021/FY2022, we are seeing costs per tonne and productivity trend in the right direction already, and the future looks bright with considerable success to date on cost optimizations. It’s also worth noting that its Doropo Project, which could head into production by early 2026, is expected to have ~$1,000/oz AISC even after adjusting for inflation, dragging down Centamin’s cost profile even further on a consolidated basis. So, with the potential for a low capex expansion to Sukari Underground, a second even lower-cost mine, and further cost savings, Centamin has a path toward becoming a sub $1,025/oz producer post-2025.

Financial Results & Forward Outlook

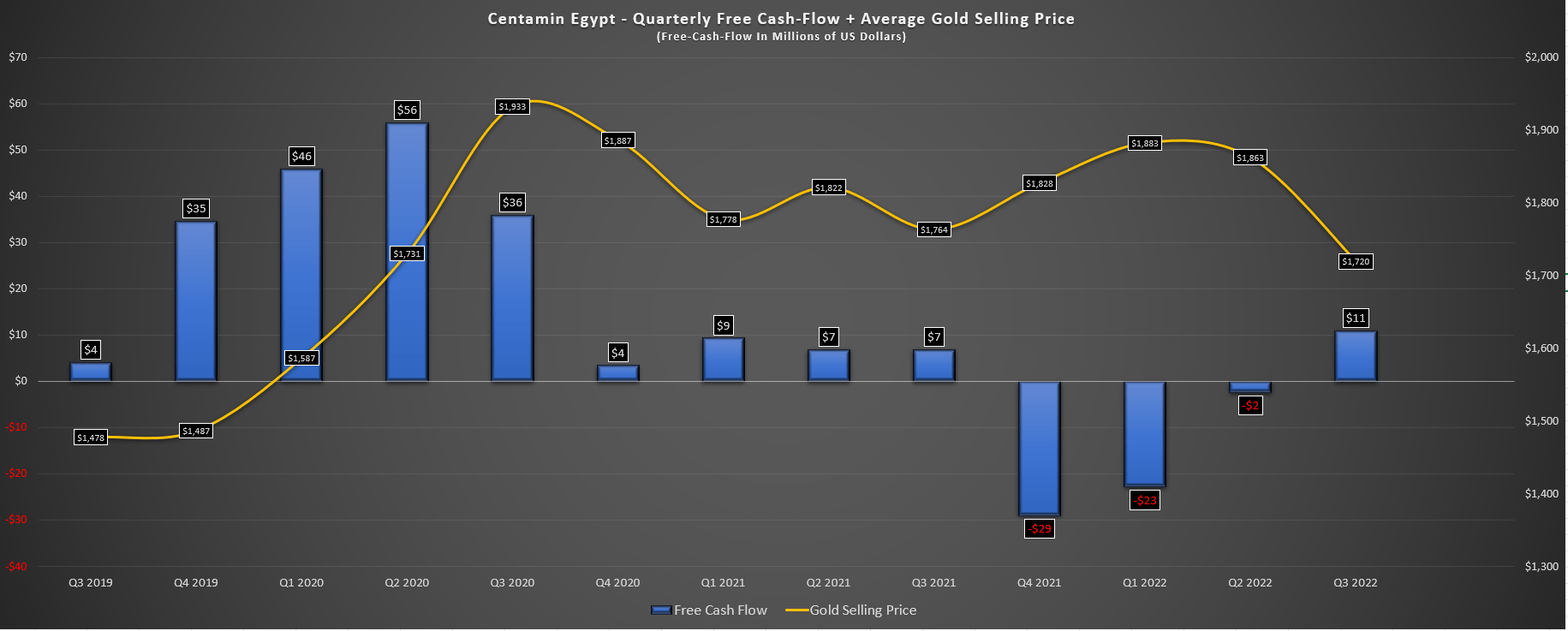

Digging into the financial results, Centamin reported revenue of $218.1 million in Q3, with ~126,600 ounces sold at an average realized price of $1,720/oz. This increased from the year-ago period, given the increased sales volume despite the weaker gold price, and I would expect a much stronger Q4 and Q1, given the recovery in the gold price since Q3. Meanwhile, cash flow moved back into positive territory (Q3 2022: $11 million) despite the elevated capital spending and the softness in the gold price. I would expect further improvements in free cash flow given the combination of better cost performance, the benefit of a $1,800/oz average realized gold price if the metal continues to cooperate, and much lower capex in 2023.

Centamin – Quarterly Free Cash Flow & Average Realized Gold Price (Company Filings, Author’s Chart) Centamin – Capex Outlook (Company Presentation)

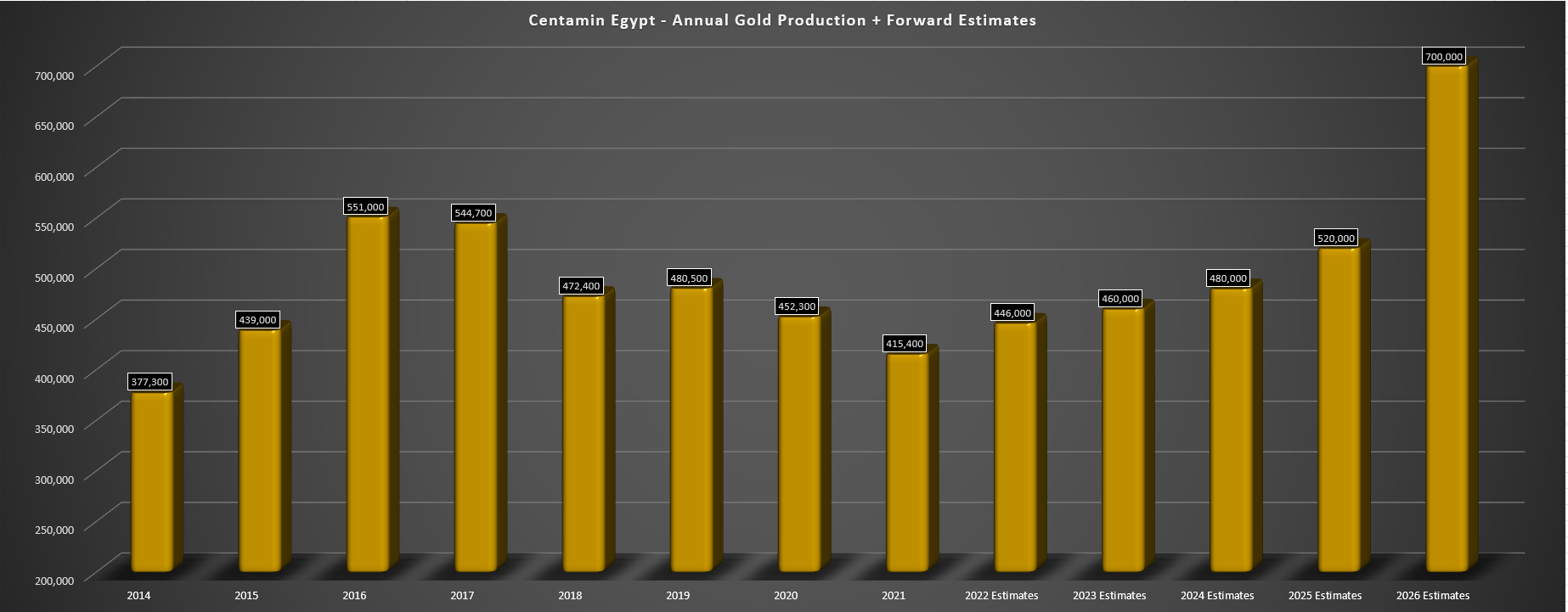

In terms of Centamin’s future and the big picture, we can see that the combination of two years of elevated waste stripping and optimized underground operations has set Sukari up to a ~460,000-ounce per annum producer, with a potential lift towards 500,000 ounces with the benefit of another 40,000+ ounces each year from the Sukari Underground Expansion (~400,000 tonnes at 4.0+ grams per tonne gold). However, Centamin’s Doropo Project in Cote d’Ivoire could transform Centamin into a 670,000-ounce producer post-2025, with production closer to 700,000 ounces in 2026/2027 as Doropo benefits from peak production. For now, the project has yet to be green-lighted, but with a PFS in H1 2023, it’s possible we could see a construction decision by mid-2024, with a lat 2025 first gold pour.

Centamin – Annual Production & Forward Estimates (Company Filings, Author’s Chart & Estimates)

Although this would provide a significant boost to cash flow given that Doropo is expected to be a cash cow with ~170,000+ ounces per annum at sub $1,000/oz AISC, this would also help Centamin to shed its less attractive single-asset producer status. The good news is that Centamin should generate a decent amount of free cash flow this year to further pad an already strong balance sheet ($160 million net cash), suggesting that this growth would translate to production growth per share with the ability to fund this with debt and cash vs. equity. Let’s take a look at Centamin’s valuation:

Valuation

Based on ~1.60 billion shares outstanding and a share price of US$1.50, Centamin trades at a market cap of $2.4 billion and an enterprise value of ~$2.24 billion. This is not a cheap valuation by any means for a single-asset producer in Egypt, even if the company does operate a Tier-1 scale operation(~500,000 ounces per annum). The reason is that Centamin has a 50/50 profit share on its Sukari Gold Mine with the Egyptian Mineral Resource Authority [EMRA], with over $800 million paid to the government to date over its mine life from royalties and profit share. Even if we assign $500 million in fair value to Doropo and its additional Egyptian concessions, this places a value of ~$1.74 billion on its share of Sukari. Even after accounting for the Underground Expansion, I would argue that the valuation is no longer attractive.

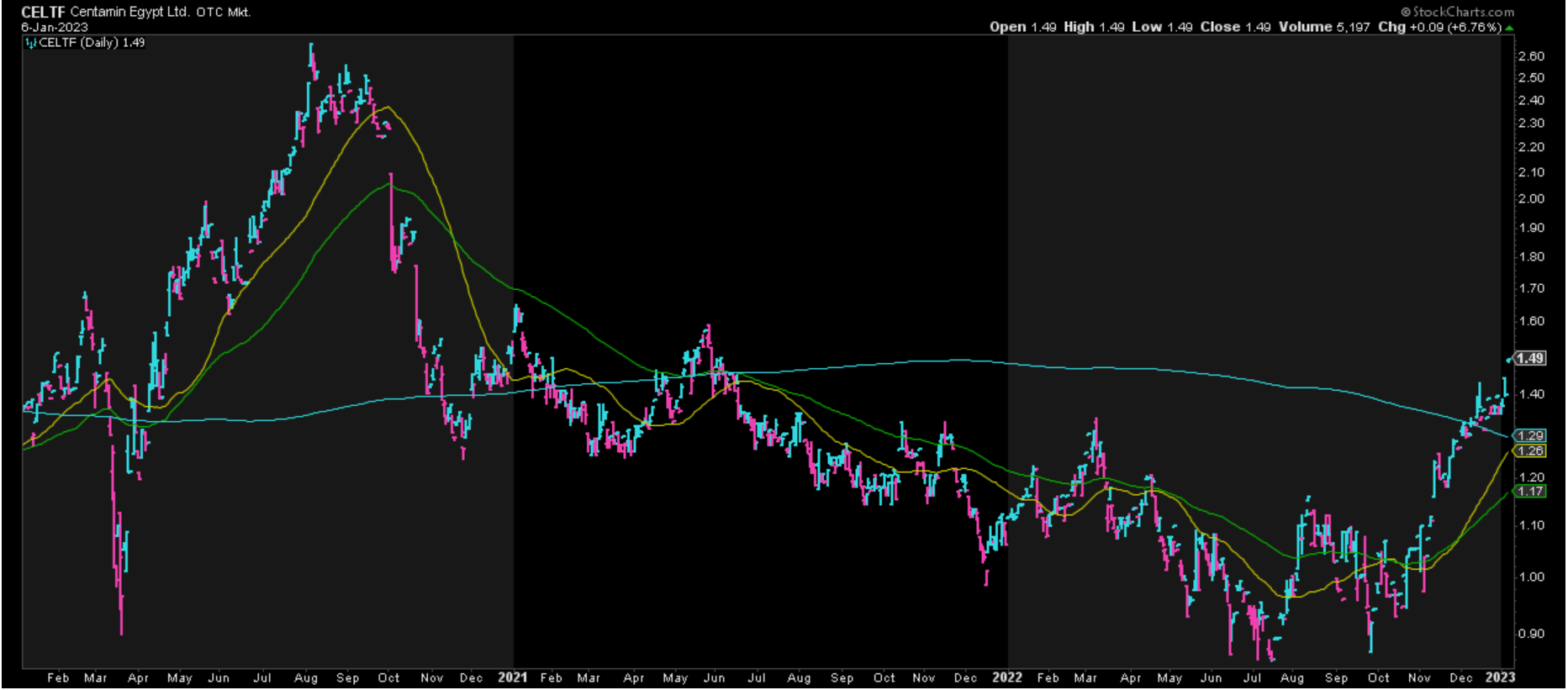

Centamin 3-Year Chart (StockCharts.com)

Looking at Centamin from a technical standpoint, the setup is less attractive here as well, even if momentum is back to the upside. This is because Centamin’s next strong support level doesn’t come in until US$1.10, while it has resistance expected at US$1.71. If we measure from a current share price of US$1.49, this translates to a reward/risk ratio of 0.55 to 1.0, with $0.22 in potential upside to resistance and $0.40 in potential downside to support. Generally, I prefer a minimum reward/risk ratio of 6.0 to 1.0 for mid-cap names, meaning that even from a technical standpoint and ignoring the less attractive valuation, Centamin would need to dip below US$1.18 to become more attractive.

Summary

Centamin had an excellent year in 2022 while many of its peers struggled, and the turnaround thesis remains intact here. Importantly, Centamin is expected to see a steady trend higher in production as the decade progresses, and costs at Sukari should continue to improve and dip back below the industry average after two years of elevated investments, translating to steady margin expansion vs. 2022 levels. Still, the goal is to buy cyclical names when they’re deeply out of favor and sitting near support. In Centamin’s case, the stock is neither cheap nor near support after a 70% rally in 15 weeks. Hence, I don’t see any way to justify chasing the stock here, and I would view any rallies above US$1.60 before April as a profit-taking opportunity.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment