bjdlzx

(Note: This article appeared in the newsletter on July 19, 2022 and is updated as needed.)

(Note: This NYSE listed company is a Canadian company that reports in Canadian Dollars unless otherwise noted).

Cenovus Energy Inc. (NYSE:CVE) has been rapidly growing cash flow beginning with the acquisition of the partnership interest from ConocoPhillips (COP). The company is far larger now, so growth is likely to slow. But a well-run thermal business tends to generate a lot of free cash flow. For all the supposed market emphasis on free cash flow, the valuation does not come close to taking into account what this business will generate on average throughout the business cycle.

Safety

A side issue is that the refinery in Toledo had an accident that killed 2 workers and has caused a shutdown. This has caused me to tell my newsletter subscribers that BP p.l.c. (BP) appears to be heading back towards its safety record before the big oil spill. Therefore, the stock for me is an avoid.

Cenovus has a relatively good safety record. I would, therefore, expect that once BP is bought out that safety will not be in the headlines in the future.

Some have asked about the effects of a refinery shutdown. First of all, most if not all of this will be covered by insurance. Gulf oil spills that exceed insurance like a few years back are a relatively rare event in the industry. Secondly, Cenovus will be bringing online a brand-new Superior refinery in Wisconsin, probably in the first quarter. Progress there will be updated in the third quarter report. Therefore, any capacity decreases from the accident and fire will likely be mitigated relatively fast.

That makes the current price action responding to the headlines way overdone. The concentration should be on the overall picture which remains unchanged.

Thermal Business

The thermal business often has a large initial cash requirement that then provides a depreciation charge to cover the cash flow generated. It is only recently that companies like Cenovus have gotten costs low enough to successfully compete with the unconventional sector, even though thermal oil is a discounted product. Previously, this sector of the oil and gas business generated a lot of depreciation to protect cash flow. But profits “hit the skids” after the large product price decline in 2015. Now, higher commodity prices combined with lower costs are a fantastic combination for shareholders.

Thermal Growth From Acquisition

So far, actual growth from acquisitions has gone back to small opportunistic acquisitions. Management announced the acquisition of the 50% interest in Sunrise that they do not own. Since Cenovus took this operation over after the merger with Husky (OTCPK:HUSKF), management believes that they can bring costs in line with their other projects. The partner probably got tired of consistently high costs and was wary of cash needed to bring costs to competitive levels.

The acquisition of the Sunrise interest combined with the acquisition of the refining interest gets a partner (BP) that has a less than stellar safety record and an equally mixed management record “out of the way” to allow for an efficient management of the assets going forward.

What is becoming apparent is that when I first covered Cenovus Energy, management was literally “tied up” by partnerships. Now the unhelpful partners are being dismantled so that management can run things by themselves. The changes over the last five years or so as this has happened have been a real eye-opener.

Refining Growth

This is one of the few companies actually building a brand-new refinery.

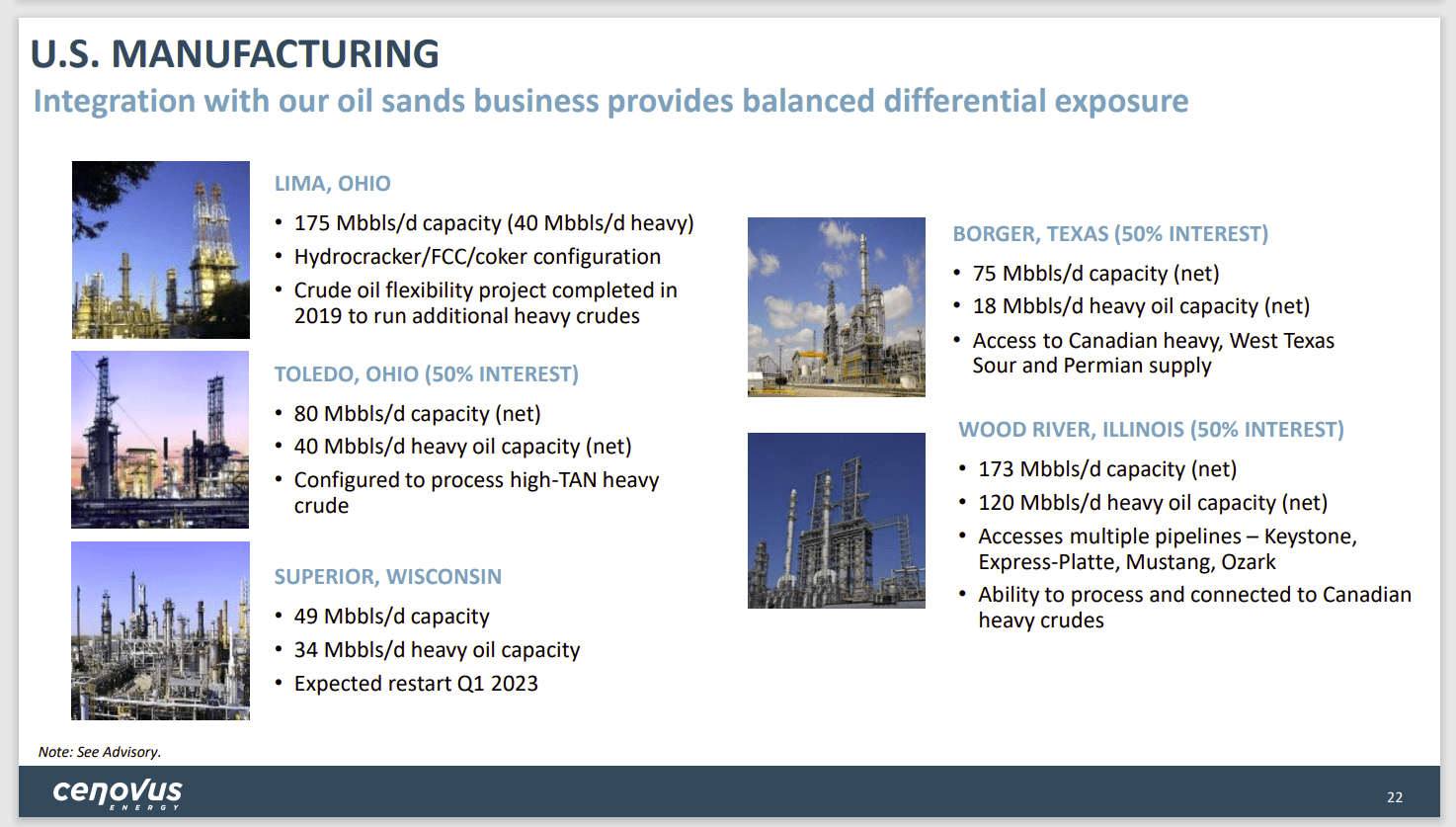

Cenovus Energy Summary Of Refining Business In The United States (Cenovus Energy First Quarter 2022, Investor Presentation)

The other growth project is the startup of the Superior, Wisconsin, Refinery. That refinery burned to the ground in the past and took a fair amount of time to rebuild. But the insurance money allows the company to replace the old refinery with modern equipment at a nominal cost to the company. Shareholders are likely to gain a margin advantage as well as overall refining profitability from the most modern refinery in North America.

Notice that the Superior refinery has a heavy oil capacity similar to the Toledo refinery. What will be delayed, of course, is the ability to use both refineries for more total capacity. But any capacity shrinkage will be temporary, as shown in the slide above.

It should also be noted that this company, like many others, will increase capacity by means of “debottlenecking” and other small projects that allow for production capacity increases. There are also refineries out there doing outright expansions to handle more production. The whole industry overall is expected to add enough capacity equivalent to several medium-sized refineries.

While the press blares that “no new refineries were built since a long time ago” the fact remains that refinery capacity is being significantly increased. It will likely decrease during the next industry downturn as the industry closes down outmoded high-cost capacity. Of course, the next recovery would likely mean more expansions involving modern technology to expand capacity. This process has gone on for a long time. It should be expected to continue in the future.

Growth Through Merger Synergies

This one is going to be a little harder for shareholders to determine. So many times, rising oil prices make management look like geniuses when it comes to acquisition benefits. I happen to believe that this particular merger with Husky was a good one. However, the actual company performance during the next cyclical downturn should make the benefits of the merger far more obvious to shareholders.

Cash Generation

By most measures, Husky was a high-cost thermal producer while Cenovus was low cost. Replacing at least some of that high-cost production to Husky refineries with lower cost production combined with less necessary outside purchases for the refining system should materially benefit the combined company. Rising commodity prices will likely magnify that benefit.

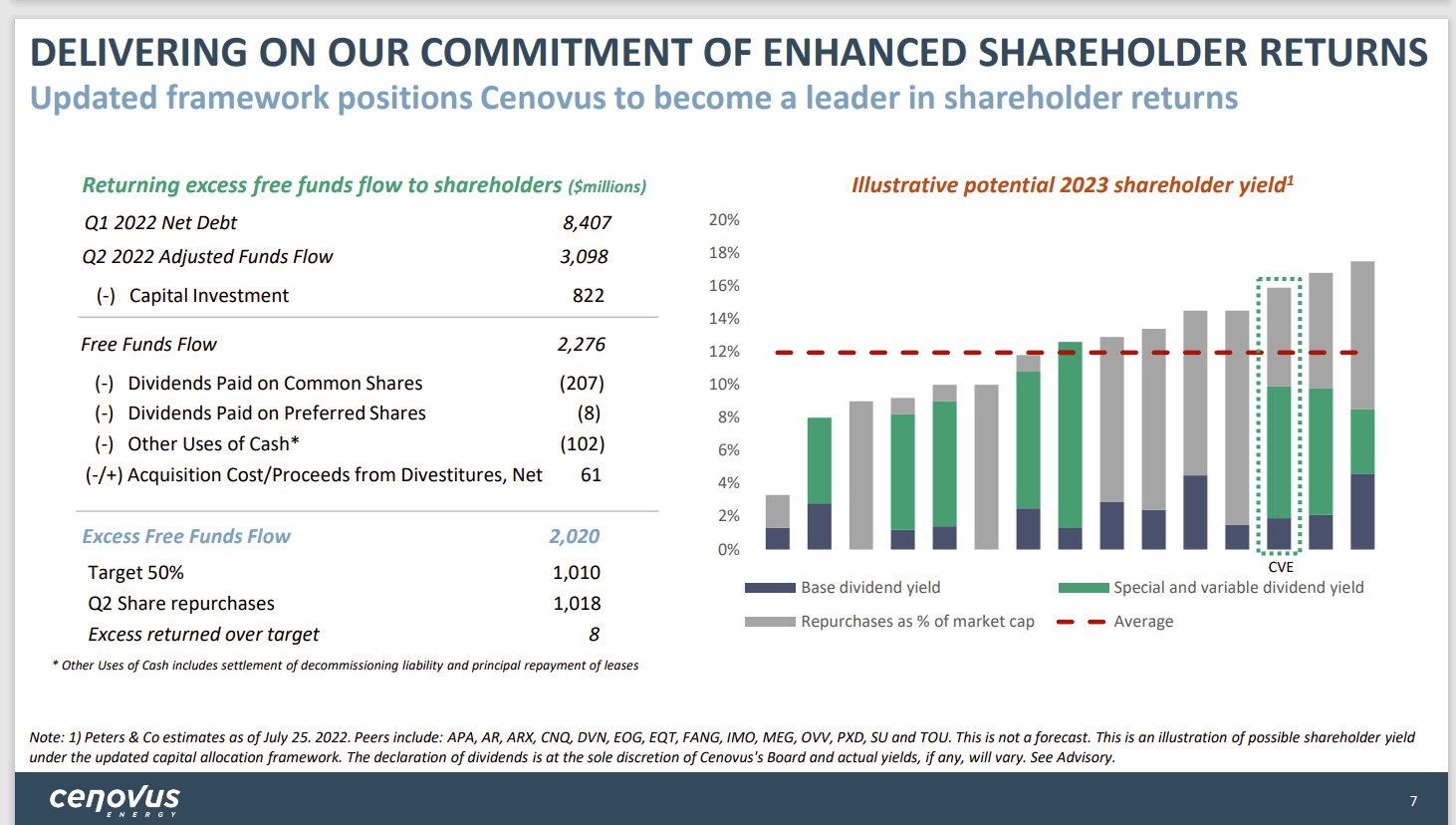

Cenovus Energy Plans To Return Profits When Compared To Competitors’ Plans (Cenovus Energy Second Quarter 2022, Earnings Conference Call Slides)

Management plans to initiate a variable distribution that will produce quite a yield during periods of high prices. Management also plans to continue reducing debt. As was mentioned previously, thermal producers (especially low-cost ones like this one) usually cash flow generously even when they are not profitable. The refining and upgrading capacity will help to insulate the company from losses during periods of weak commodity prices.

In the meantime, shareholders can expect a period of relatively large variable distributions as long as commodity prices remain strong. The difference here is management intends to continue to grow the company. Therefore, that growth will provide some distribution downside protection during times of weak commodity prices.

This company is best looked at as a variable distribution entity. Here, that growth will likely mean that the distribution will cycle as they do with similar companies. But the overall cycle of distributions will keep rising.

Most likely, growth will happen at a single-digit pace, with an occasional acquisition to bump up the average over the long term. That may be enough for some investors to consider this as a variable income investment proposition for the long term.

This management has done wonders for the company since taking over. Debt is already at a low level by most accounts. That debt will likely decline for this company to achieve an investment grade rating within the next few years (at the most).

There is another potential profit enhancement for the company in the conventional business. That business has been mostly natural gas in the past. But any thermal producer has an interest in finding condensate to mix with the thermal oil, so it flows through pipelines. Management had indicated an interest in changing the focus of drilling conventional wells to emphasize more liquids. Success in this endeavor would enable a long-term profitability to increase because less condensate would have to be purchased.

Summary

This company has been growing rapidly ever since the buyout of the ConocoPhillips partnership interest. That growth will likely slow now that the company is far larger. But decent single-digit production growth, combined with some profitability enhancements from merger synergies and some organic profitability increases, provide an attractive investment proposition. Combined returns from all of the above in the teens would probably be a reasonable expectation.

There is also the dividend and the variable dividend to add to the potential returns. The company is now diversified enough to be a far safer investment than was the case a few years back. Management still has to establish a combined company record of superior performance. But that does not take an extraordinary effort when a company is this vertically integrated.

That means there is a fair amount of potential appreciation ahead as the market recognizes the benefits of the new company configuration. For years, the market ignored the ever-present improvements. Now, it is catch-up time.

Be the first to comment