FG Trade/E+ via Getty Images

Introduction

I’ve mentioned in several articles on SA that I work as an M&A analyst covering Latin America, and I’ve written about several companies from the region. Today, I want to talk about a Peruvian cement producer named Cementos Pacasmayo (NYSE:CPAC) which is currently the only company from Latin America in my portfolio. It has a strong moat in the form of a monopoly in the northern part of the country and the dividend yield is just above 10%. The dividend payments for the past six years of Cementos Pacasmayo account for almost two-thirds of its current market valuation. Let’s review.

Overview of the business and financials

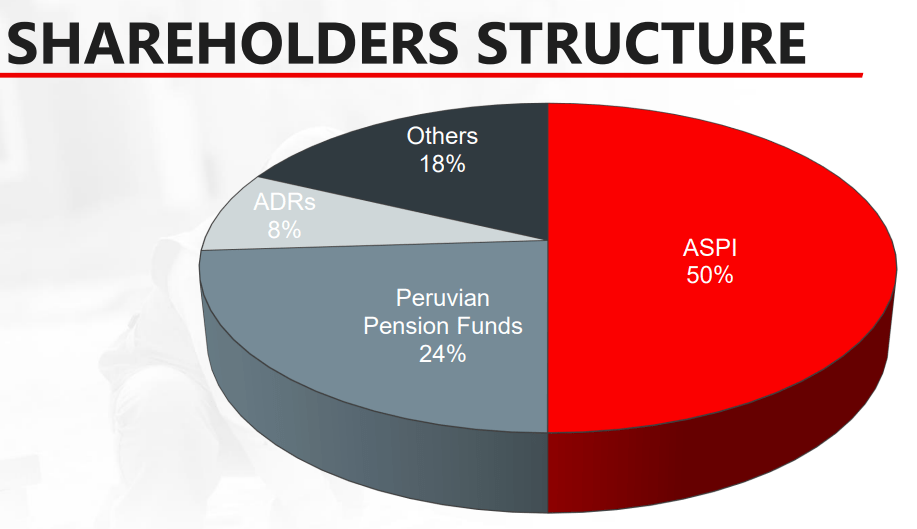

Cementos Pacasmayo was founded in 1949 by Luis Hochschild Plaut, who is the son of Moritz Hochschild, one of the three so-called Bolivian tin barons who is also known as Bolivia’s Schindler for helping save between 9,000 to 22,000 Jews during the Holocaust. When Luis was killed in a kidnapping attempt in 1998, the reigns of the company were passed to his eldest son Eduardo Hochschild Beeck. Eduardo currently holds a 50% stake in Cementos Pacasmayo through a company named Inversiones Aspi and according to Forbes, his net worth stands at $1.1 billion. Cementos Pacasmayo is listed on the Lima Stock Exchange and about 8% of its share capital is trading on the NYSE in the form of American depositary receipts (ADRs).

Cementos Pacasmayo

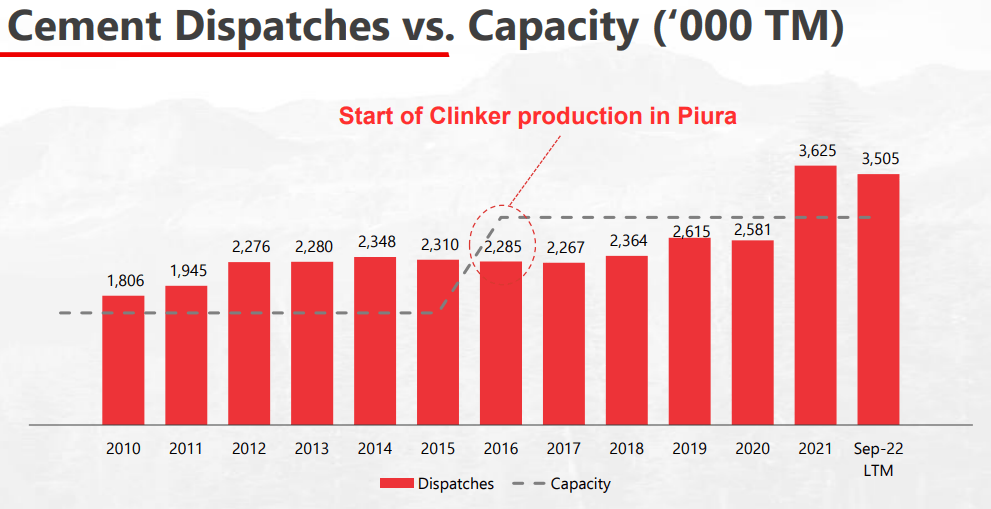

Cementos Pacasmayo owns a total of three production facilities in northern Peru with a combined cement production capacity of 4.9 million MT/year as well as a combined clinker capacity of 2.8 million MT/year. As of September 2022, LTM cement shipments came in at 3.5 million MT so there’s room to improve utilization rates, especially at the Pacasmayo plant.

Cementos Pacasmayo

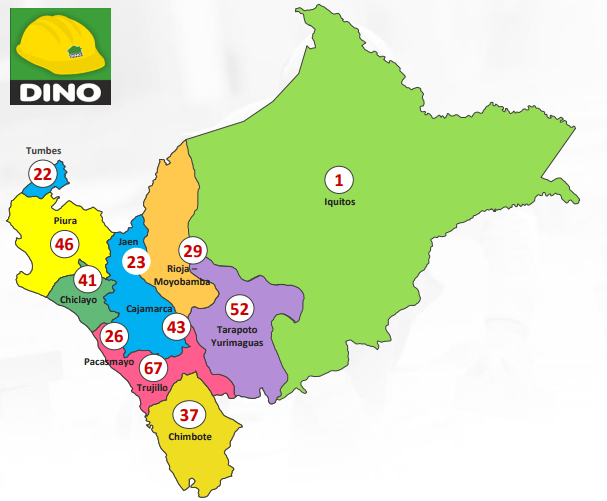

What I find interesting about the Peruvian cement market is that each region of the country is dominated by a separate local company and it’s not economically feasible to open a production facility in a new region due to the competitive advantages enjoyed thanks to their own product distribution networks. Cementos Pacasmayo dominates the northern part of Peru and about 70% of its sales come through around 240 small-scale distributors and 379 points of sale under the DINO brand. These stores offer loyalty programs and incentives for Cementos Pacasmayo products and in my view, each of the three main cement companies in Peru has a great moat in the form of a regional monopoly.

Cementos Pacasmayo Cementos Pacasmayo

Looking at the customer profile of Cementos Pacasmayo, about three-quarters of sales are made to what is locally known as the auto-construction sector. This represents people that buy construction materials to build their own homes and this is very popular in my own country too, especially in the rural areas (note that northern Peru has less densely populated cities compared to the central region). I remember when I was little how all my uncles bought a lot of cement and bricks and built a four-storey home in my village. It’s a cultural thing that is also a bonding experience and also saves a lot of money as they didn’t have to pay for labor. And it’s not that hard, you don’t require a degree to learn how to lay bricks (come to think of it, none of my uncles went to university). Today, it can be learned through a five-minute YouTube video.

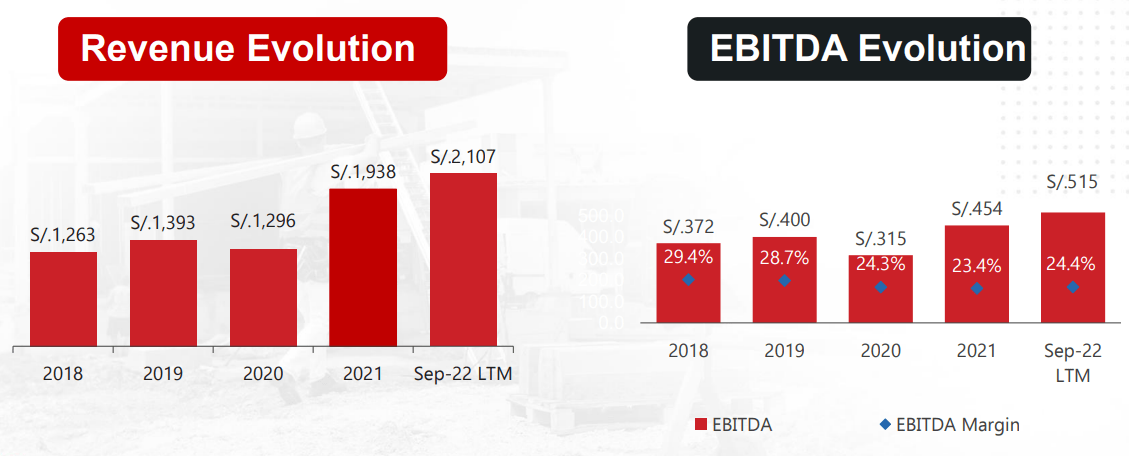

Turning our attention to the financial performance of Cementos Pacasmayo, revenues have increased significantly since the end of COVID-19 lockdowns thanks to pent-up demand and economic recovery in Peru, and they stood at 2.1 billion soles ($538 million) for the 12 months ended September 2022. While EBITDA rose to $515 million soles ($131 million) for the same period, the EBITDA margin is still below pre-pandemic levels.

Cementos Pacasmayo

The main reason for the lower margins seems to be that Cementos Pacasmayo needs to rely on clinker purchases to meet strong demand at the moment. After all, its own clinker capacity is enough for only 2.8 million MT/year of cement production. In order to address this issue, the company is investing $73 million to build kiln #4 at Pacasmayo, which will boost the clinker capacity of that plant by 0.58 million MT/year. The project is expected to be completed in the second half of 2023 and will allow the company to produce about 3.7 million MT/year of cement using its own clinker.

Cementos Pacasmayo

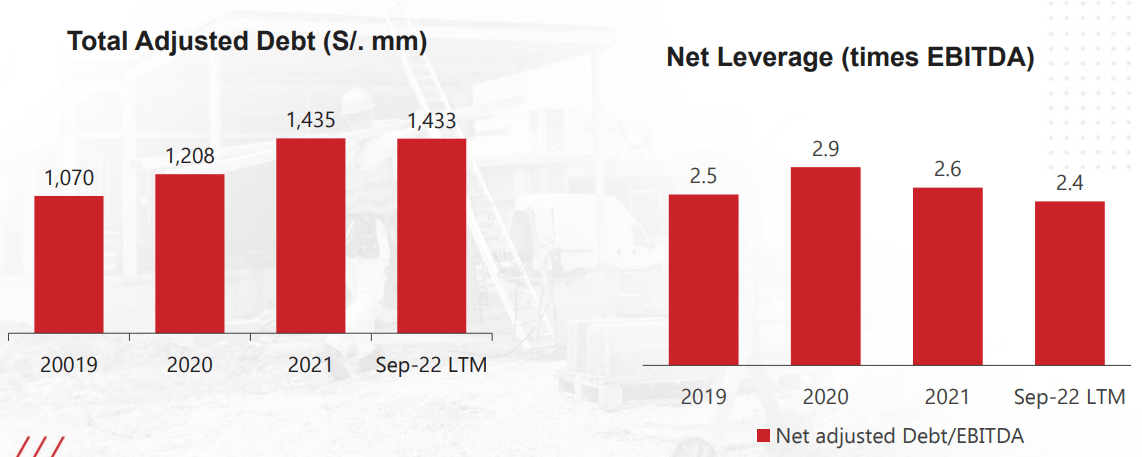

Turning our attention to the balance sheet, the debt load level seems manageable, and Cementos Pacasmayo decided to distribute a $0.54 per ADR extraordinary dividend in December 2022.

Cementos Pacasmayo

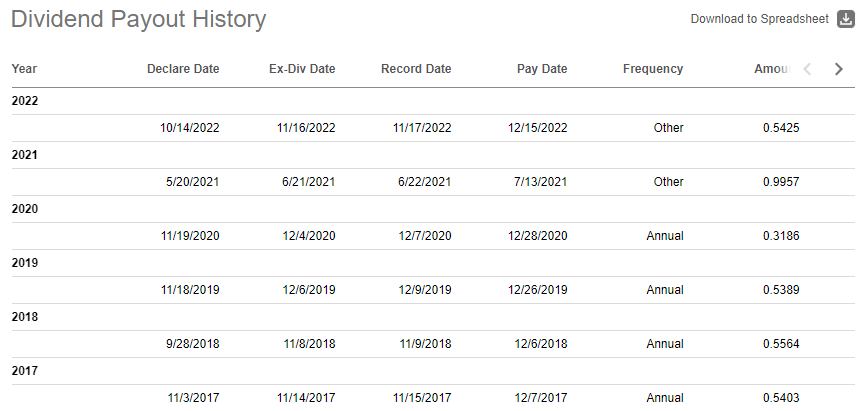

Looking at the dividend payout history, the company has distributed a total of $3.49 per ADR over the past six years.

Seeking Alpha

I think that 2023 is likely to be another strong year as political protests across Peru pushed the government to launch a $1.6 billion economic recovery plan which is expected to keep GDP growth above 3% in 2023. This measure should boost disposable income as it includes a number of social measures such as pensions, soup kitchens, and access to natural gas in homes. In addition, kiln #4 at Pacasmayo should provide a small boost to EBITDA in late 2023. In my view, it’s likely that this year’s dividend will be above $0.50 per ADR again and Cementos Pacasmayo seems cheap at the moment.

Looking at the risks for the bull case, the major one is that change in the government could lead to a scrap of the economic recovery plan or that I’m overestimating its effect on cement demand. It’s also possible that the clinker capacity expansion project is delayed or there are cost overruns. In the long term, I think that the major risk for Cementos Pacasmayo is a potential shift from traditional brick and mortar construction to drywalling and steel framing as the latter is cheaper and faster. Yet, it could take a long time as this shift hasn’t happened in my home country despite significant economic growth since Bulgaria joined the EU in 2007. Sure, drywalling and steel framing may be cheaper, but the insulation provided is bad and it needs more maintenance. Personally, I live in a commie block built in the early ’90s and I’m satisfied with the quality.

Investor takeaway

Cementos Pacasmayo has a dominant market position in northern Peru and this is unlikely to change anytime soon. Its debt level is decent, and I expect sales in 2023 to be strong thanks to Peru’s $1.6 billion economic recovery plan. In addition, EBITDA margins should start returning to around 30% as the company increases its clinker production capacity. In my view, there could be another dividend of above $0.50 per ADR around the end of 2023. The stock looks like a bargain at these levels.

Be the first to comment