helloabc

Recommendation

Just looking at the earnings results, it certainly seems like a disappointing update, with weaker results vs. consensus estimates and the company’s own guidance across brands. I believe Capri Holdings (NYSE:CPRI) shares fell off the cliff due to this reason. There are a few key things going on here: restructuring of its wholesale strategy, the China reopening, and margin expansion. The former is something that CPRI can control, and they seem to be doing a good job (timeline accelerated), but the latter 2 have quite a bit of uncertainty to them: Are we sure China is the same as the past? Can CPRI benefit as much as expected? How long would it actually take to reach 20% LT EBIT margin? What about the short-term margin pressures?

I am sure management can work their way out of these with better communication, and we will see more concrete data on China sales. Also, the valuation seems to shout cheap at 7x forward earnings. However, till I see answers to these uncertainties, I am not pulling the trigger to buy the stock yet.

Latest earnings highlights

Revenue for the third quarter of FY23 fell by 6% to $1.51 billion, coming in below the $1.53 billion guidance. Adjusted gross margin rose by 120 basis points to 66.3%, while adjusted EBIT profit margin fell by 540 basis points to 16.9%, well below the guided 20.5% target. Michael Kors (MK) was the main culprit for the margin shortfall (MK EBIT margin fell 550bps year-over-year to 22.9%), while global wholesale also played a role. CPRI’s EPS of $1.84 fell short of both consensus estimates and the company’s own target range. Finally, management believes inventory levels will level off this year.

Wholesale update

Managers reaffirmed that CPRI’s long-term target of 20% worldwide wholesale penetration set at its 2022 analyst day remains unchanged, though they did note an accelerated timeline and a different execution path. To put this into perspective, the original execution roadmap predicted a 10pts drop in wholesale by FY27, with D2C outperforming. However, that time frame has been shortened by two years. Specifically, management is cutting shipments to the channel by over $200 million in 1H24, which equates to around a quarter of global wholesale penetration by the end of FY24. Management has also stated that the wholesale channel reset will be finished by the end of 2Q24, putting the company on track to achieve the planned figures of down mid-teens in FY24.

Geographies

Management seems more optimistic today than before. In particular, they pointed to the steady state in North America, the better-than-expected trends in Europe, and the upcoming reopening opportunity in China. Specifically:

- EMEA outperformed, with revenue growth of 19% ex-FX, thanks to robust gains in retail sales that were partially offset by a softening trend in wholesale.

- Asia grew by 8% ex-FX, with strength in Japan and South East Asia offsetting a 40% drop in China. Unfortunately, China had a rough fourth quarter, with more CPRI stores closing than at any other time during the pandemic.

- Sales in the Americas fell by 4%, with retail showing growth in the mid-single digits but wholesale experiencing significant declines.

With regards to China in particular, management anticipates a further drop in 4Q22 due to COVID-related restrictions, followed by an inflection to material growth in FY24 as the reopening quickens. For FY24, management predicts a rise in retail sales in the low double digits.

Others

Also, noteworthy is the fact that all three brands saw an increase in accessories retail sales through CPRI’s own retail channel, indicating continued category strength. In addition, 3Q22 saw the largest growth in customer base. All three brands’ databases have grown every quarter for the past year, indicating enthusiastic consumer response to strategic moves. Although the average purchase price dipped during the holiday season, CPRI found that sales of small leather goods and crossbodies increased rapidly as consumers dressed up for social events. The important trend toward occasion-specific accessories occurred simultaneously with broader Luxury trends seen in both footwear and apparel.

With regards to inventory, it grew by 21.5% sequentially, but management is optimistic about bringing it down to below 4Q22 levels in the coming quarter. Management also noted their satisfaction with stock levels and the wise decision to cut back on wholesale shipments, the latter helped reduce the potential for markdowns and harm to the company’s reputation.

Guidance

FY23:

For FY23, CPRI expects revenue of $5.56 billion, an adjusted EBIT margin of 16.0%, and earnings per share of $6.10. CPRI now anticipates revenue in Michael Kors of $3.83 billion revenue, Versace of $1.1 billion, and Jimmy Choo of $610 million. Notably, the growth of all brands was guided down. Adjusted EBIT margin expectations for each brand are 22%, 15%, and 4% respectively. In 4Q23, management now expects total sales of $1.275 billion, an adjusted EBIT margin of 8.5%, and adjusted EPS of $0.90 to $0.95.

FY24:

Management has guided to an FY24 EPS of $6.40, which is significantly below consensus estimates. This is based on revenue growth in the mid-single digits, which is lower than the high-single-digit growth predicted by consensus. Specifically, the growth will be fueled by low double-digit increases in retail sales, which will be partially offset by a decrease in wholesale sales in the mid-to-high teens, and by a modest increase in GPM, which should be partially offset by expense deleveraging.

Valuation

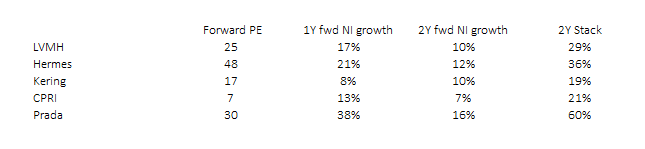

I believe the saving grace for CPRI, from a stock perspective, is that it is trading at a very cheap level compared to other luxury peers. As we can see below, CPRI is the only stock that is trading at the single-digit level (7x forward earnings), compared to the rest that are trading at multiple times CPRI’s levels. There are two arguments that investors could make here to justify the discount:

- CPRI’s portfolio of brands has less brand value than the rest. I do not disagree on this, especially when we compare MK to the likes of Hermes (OTCPK:HESAY), Gucci, etc. And also, CPRI used to have a wholesale segment, so that could be brand dilutive.

- Growth outlook. Using consensus figures, CPRI’s 2-year stack forward earnings growth is 21%, on par with Kering (OTCPK:PPRUY) and 800bps lower than LVMH (OTCPK:LVMUY). If we take the closest peer – Kering – CPRI trades at 10 multiple turns below it but is expected to grow at the same rate over the near term.

Historically, over the past 10 years, CPRI traded at 0.75x Kering on a forward PE basis, and it is 0.43x today. If CPRI were to execute as management guided, there is a good chance for this valuation gap to close, which implicitly suggests CPRI to trade at 12.75x, or 80% upside.

FactSet

Summary

The latest earnings update from CPRI showed disappointing results, with revenue falling below its own guidance and adjusted EBIT margin also falling well below expectations. On strategy, management is cutting back on wholesale shipments by over $200 million in 1H24, and they expect the wholesale channel reset to be finished by 2Q24. Management is also optimistic about the reopening opportunity in China. Despite the company’s cheap valuation, there are still uncertainties regarding China sales and margin expansion, and I would recommend holding off on buying the stock until more concrete data becomes available.

Be the first to comment