Bet_Noire/iStock via Getty Images

Investment Thesis

Canadian Natural Resources (NYSE:CNQ) is well set up for a strong energy market, with a balance of oil and natural gas production.

I put the focus of my bull case on CNQ’s raising dividends. By my estimates, CNQ’s dividend yield could reach 4.9% next year.

But there are other capital flows that I believe will continue to meaningfully deliver for investors.

Making Sense of Nonsense

There are a few different forces in the market right now. In days that oil stocks do well, the whole energy trade appears to do well. From coal, to natural gas, uranium, and oil, it all appears to move towards energy. Even if some fossil fuels directly compete with each other as a fuel source.

There are just so many algos and capital flows into and out of commodities, that it becomes impossible to make sense of some of the implications afoot. Investors might as well just sit back and get their dividends, rather than having to over-intellectualize anything.

Furthermore, as I’ve stated in the past, I believe that bigger and more fluid companies, with larger market caps, are getting rewarded with a higher multiple, than smaller stocks.

What’s more, I’ve noticed that dividend paying stocks are getting better rewarded than fossil fuel companies that are more predisposed towards buybacks.

Given that CNQ has a market cap of approximately CAD$90 billion, I’m inclined to believe that CNQ will do well at least in the medium term.

Why? Not only are its dividends going up, as we’ll soon discuss, but also, because its valuation is still very compelling.

Capital Allocation Program, Estimated Forward 4.9% Dividend Yield

Before going much further, allow me to highlight a quote from the earnings call,

[…] we have returned approximately $4.9 billion to our shareholders through base dividend and special dividend, an increase of $2.8 billion or 127% from 2021 levels.

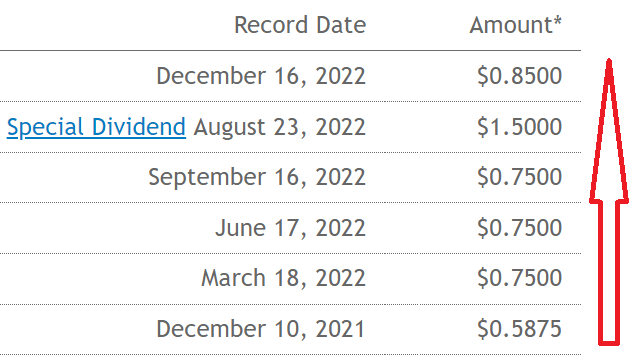

With this in mind, see if you follow a trend in the past twelve months:

CNQ website

Let’s push aside the special dividend of CAD$1.5 per share. Let’s just pretend that didn’t exist. What we see above is that CNQ’s dividend annualizes at CAD$3.4 per share, or 4.2% annualized.

Now, you may contend that getting 4.2% isn’t that great. Yes, the dividend is up 45% y/y, but so what? In fact, let’s assume that next year, the dividend only increases by a more subdued 15% y/y and that there’s no special dividend either.

This would mean CAD$3.91 per share. Translating into a forward dividend yield of 4.9%.

Of course, the big drag on even further increasing CNQ’s dividend payout is that it still holds approximately $12 billion of net debt.

And until that drops below $8 billion of net debt, at some point in the next 18 months, CNQ’s balance sheet will continue to restrict its capital return program.

That being said, keep in mind that CNQ is also repurchasing shares. Recall, that after buying back shares throughout the past 12 months, CNQ has brought down its total number of shares by 4.5%.

What this means, is even by spending similar sums on dividends, the dividend can continue to increase per share, as there are fewer shares available.

CNQ Stock Valuation — 9x 203 Free Cash Flow

For 2022, CNQ is likely to print CAD$10 billion of free cash flow. Yes, oil prices have come down a lot in the past few months. And yes, nobody can predict where oil prices will be in 2023.

Similarly, we don’t know where natural gas prices will be over the next twelve months.

The outlook for these fossil fuels has been very bullish since the summer. And yet, since the summer, these prices have come down. And still, there are all kinds of pontifications about what’s happening and why energy costs will be higher next year. And at the same time why energy costs could also be lower too if there’s a global recession.

And rather than pretend to have any view of where energy prices will be, let’s just settle for 2023 to be similar to 2022.

That implies that CNQ is priced at approximately 9x next year’s free cash flow. Having looked through North American energy company alternatives, I haven’t seen many outside of the biggest names that are priced at this high a multiple.

But there again, as I already discussed, the bigger cap players have been getting a premium in this market. Largely the same as in tech. There’s a run to ”safer” names, with investors eager to pay a premium for big-cap names.

The Bottom Line

Canadian Natural Resources is well positioned for a strong secular growth opportunity in the energy market.

My argument here is that CNQ’s dividends should continue to move higher over the next twelve months. And that’s the best type of setup for investors. Where an investor can get more money back in dividends over time, without having to deploy more capital into the company.

Be the first to comment