Andrii Chagovets/iStock via Getty Images

It’s been just under four months since I bought some more FreightCar America Inc (NASDAQ:RAIL), and in that time, the shares are down about 4.5% against a gain of about 15.26% for the S&P 500. On the one hand, this is bad news, but I do like to buy cheap stocks, so it may also present an opportunity. After all, a stock trading at $3.64 is, by definition, a less risky investment than the same stock when it’s trading at $3.86. I’ll decide whether or not I want to buy more, hold, or take my lumps here by looking at the most recent financial results and comparing those to the valuation. I also want to offer an update on my options trade, as I was just exercised on some short puts. Finally, I’m champing at the bit to write about insider activity here.

We’re all busy people, and for that reason I want to give you the chance to save some time by offering my “thesis statement” paragraph. This is a short, hopefully pithy summary of my thinking in one paragraph, which gives you the chance to get in, and get out, and thus avoid the emotional pain associated with reading 1,700 of my words. You’re welcome. I’ll be nibbling on some shares of FreightCar again this morning, because I think the valuation is compelling. I think the most recent financial results were fine, and that the company remains in an uptrend. I particularly like the explosion in revenue from this time last year. Additionally, I like the fact that insiders who know this business better than anyone else continue to put their own capital to work in it. Finally, I generated a 30% yield on puts previously, and I consider that to be a reasonable return given the risks here. Unfortunately, it’s not possible to make much from selling short puts at the moment, so I can’t recommend that strategy. I’ll simply buy shares as I think that makes the most sense at the moment.

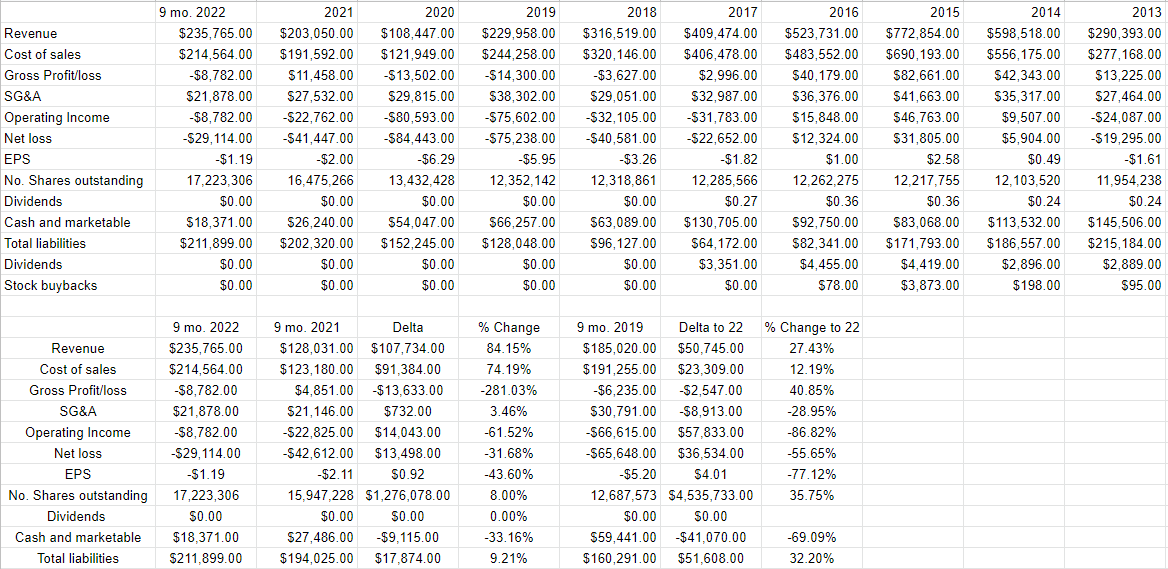

Financial Snapshot

I think the most recent financial results out of FreightCar have been generally good in my view. Not unexpectedly, revenue is up massively when compared to both the previous year and the pre-pandemic era. Specifically, sales during the quarter just ended were 27.4% higher than they were in 2019 and were up a massive 84.5% when compared to the same period in 2021. I can’t overstate how much I like the fact that sales for the quarter were $107 million higher than the nine months of 2021 and $50.7 million higher than the same period in 2019. In fairness, the cost of sales was also higher, but by only $91.4 million over the previous year. The reason gross profits dropped relates to a loss on pension adjustment of $8.1 million. This accounts for about 92% of the gross profit loss, so I’m not too worried about it. Lastly, net loss shrunk by $13.5 million, which is fairly impressive in light of the increase in input costs in 2022. When I review the income statement, I’m impressed.

It’s not all sunshine and lollipops over at FreightCar, though. Specifically, interest expense has jumped massively by $8.3 million, or 89% relative to the same period a year ago. Additionally, the debt load has increased to $91.96 million, up from $79.5 million previously. On the bright side, the company has cash of $18.4 million, or 20% of this debt level. I don’t like the increase in indebtedness, but I’m not as concerned about this balance sheet as I am about a few others. Finally, some might fret about the secured term loan FreightCar entered into in 2020. The purpose of which was to acquire the then unowned portion of the Castanos manufacturing operation. Even the most vociferous critics of this deal would have to admit that some portion of the $12 million annualized reduction in SG&A expenses, for instance, are the result of this deal.

Given the above, I’d be happy to add to my stake at the right price.

FreightCar America Financials (FreightCar America investor relations)

The Stock

My regulars know that I consider the business and the stock to be distinctly different things. If you’re one of my new followers, first, welcome, I guess. Second, I consider the business and the stock to be distinctly different things. This is because the business generates revenue by selling freight cars to lessors and the Class 1 railroads. The stock is a scrap of virtual paper that gets traded around based on a host of factors having little to do with the business. The company’s decision to buy some shares, for instance, may drive the stock higher in price. The stock price may go up and down depending on what an analyst says about the future price of steel, or the state of the freight car fleet in North America. The stock is also affected by the crowd’s demand for “stocks” as an asset class. There’s no way to prove it definitively, but I think a reasonable case could be made to suggest that my investment in FreightCar would have done even worse had the overall market not risen by about 15.26% since then. Given that the financial statement valuation of the business is “backward-looking” and the stock is the crowd’s forecast about the distant future, there’s an inevitable tension between the two.

So, to sum up, the business generates revenue and net income, while the stock bounces up and down based on the crowd’s ever-changing views about the future. In my view, the only way to successfully trade stocks is to spot the discrepancies between what the crowd is assuming about a given company and subsequent results. I like to buy stocks when the crowd is particularly down in the dumps about a given stock, because those expectations are easier to beat.

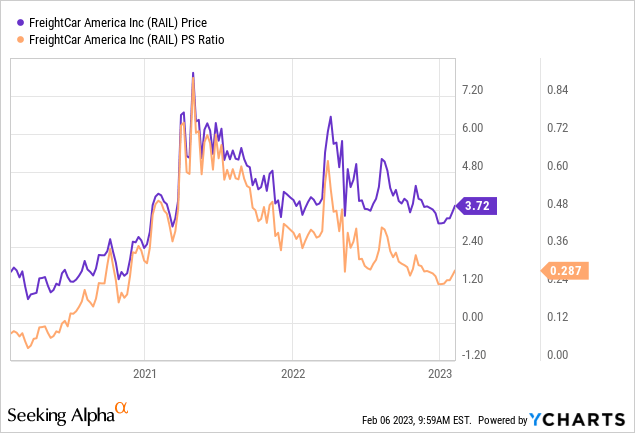

Another way of writing “down in the dumps about a given stock” is “cheap.” I like to buy cheap stocks because they tend to have more upside potential than downside. As my regulars know, I measure the cheapness of a stock in a few ways, ranging from the simple to the more complex. On the simple side, I look at the relationship of price to some measure of economic value, like sales, earnings, and the like. I like to see a stock trading at a discount to both its own history and the overall market. When I last reviewed FreightCar America, the market was paying about $.326 for $1 of sales, which I considered to be fairly cheap. At the moment, the shares are about 12% cheaper on that basis, per the following:

I’d note that the shares are relatively cheap by historical standards.

One more thing my regulars know is that I want to try to understand what the crowd is currently “assuming” about the future of a given company, and in order to do this, I rely on the work of Professor Stephen Penman and his book “Accounting for Value.” In this book, Penman walks investors through how they can apply the magic of high school algebra to a standard finance formula in order to work out what the market is “thinking” about a given company’s future growth. This involves isolating the “g” (growth) variable in this formula. In case you find Penman’s writing a bit dense, you might want to try “Expectations Investing” by Mauboussin and Rappaport. These two have also introduced the idea of using the stock price itself as a source of information, and then infer what the market is currently “expecting” about the future.

Anyway, applying this approach to FreightCar America at the moment suggests the market is assuming that this company will grow profits at a rate of about ½% from here. In my view, that is a pretty pessimistic forecast, especially given what the analyst community seems to think at the moment. For the reasons above, I’m going to nibble on shares again this morning.

Options Update

Those who read my stuff regularly know that I’m a sucker for the idea of selling puts on companies I like. Way back in March of 2022 I sold 10 January 2023 puts with a strike of $5 for $1.50 each, because I just couldn’t say “no” to that 30% yield. Not surprisingly I was recently exercised on these at a net price of $3.50. Although the position thus acquired remains barely profitable at the moment, I’m nearly at a maximum position size for FreightCar stock.

Although I like the strategy, I can’t recommend it at the moment because the premia on offer at the moment is too thin. For instance, the January 2024 puts with a strike of $2.50 are only bid at $.25 at the moment. I consider this to be too paltry a bid to make the exercise worthwhile. That written, I’ll remain on the lookout for better premia.

Insider Buys

After investing for decades, I’ve come to the conclusion that all investors are equal, but some are more equal than others. Some investors are just better at investing because they have the emotional temperament for it. Also, some are better because they have access to teams of talented analysts. One group of people I like to pay attention to are company insiders. Because they live and breathe a particular company, these people know more about a given company than any Wall Street analyst ever will. When they put their capital to work, I want to be on the same side of the table as them. With that written, I would like to point out that two insiders purchased 16,300 shares at the end of 2022 at an average price of $3.50. When the people who know this business best put their own capital to work in the stock, that fills me with some confidence. I like being on the same side of the table as these more knowledgeable investors.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment