BING-JHEN HONG/iStock Editorial via Getty Images

Investment Thesis

Recently I detailed how Intel (INTC) is not executing as strongly as investors may have been starting to expect given the changes (especially increased funding) under new CEO Pat Gelsinger. So instead of (or in addition to) buying Intel for the turnaround in half a decade perhaps, here I will recommend a company that is executing in the present: Taiwan Semiconductor Manufacturing Company Limited (NYSE:TSM) (“TSMC”).

The combination of a comprehensive foundry chip manufacturing process technology portfolio, wafer price increases, and an ongoing record period of investments in more manufacturing capacity should bode well for continued growth into the future. Nevertheless, despite this compelling growth profile, TSMC is valued not much higher than Intel, and lower even than many no-growth companies. Buy the dip on overblown recession, inflation, and interest rate hikes concerns, none of which will impact TSMC long-term.

Analysis

TSMC achieved a $75B run rate in May, which means that after a few years of torrid growth that was accelerated due to COVID-19, TSMC is finally about to overtake Intel in revenue. Given that TSMC is spending this year about 4 times more in capex (to further increase its manufacturing capacity) than just a few years ago, TSMC is prudently preparing to accommodate even higher demand (and hence further growth) into the future.

However, as just alluded to, the crucial point is that TSMC isn’t just an investment that was successful at the onset of COVID-19, which has now (at least from the point of view of investors, looking at the stock price trend) become out of favor due to issues such as inflation, recession fears, and interest rate hikes. Instead, investors should be reminded that semiconductors are still a growth industry, as it has been since every decade since its inception.

To illustrate this, the semiconductor industry became over $500B in size in 2020, and is widely expected to approach or reach $1T by 2030. In other words, while investors often describe semiconductors as cyclical, this is simply false, or misleading at best.

While it is true that building fabs takes years, which could lead to periods of overcapacity or undersupply, the only real part of this sector that is really influenced by such trends is the memory industry, since those are the most commoditized parts. However, TSMC has no significant memory business. So in contrast, chips (whether analog or digital) tend to be based on proprietary IP, which makes them the opposite of a commodity, and hence they are not influenced by cyclical trends, and hence neither is TSMC. QED.

Of course, TSMC will still be influenced by factors such as a recession that can influence (soften) demand, but the long-term trend as noted above is clearly up. So, since TSMC has over 50% market share in the foundry (outsourced chip manufacturing for often fabless companies) space, as the manufacturer for most of the largest chip companies such as Intel (INTC), Apple (AAPL), AMD (AMD), Qualcomm (QCOM) and Nvidia (NVDA), I would argue that this makes TSMC one of the safest and easiest investments to get exposure to the long-term growth of semiconductors.

Looking ahead, as the world’s largest reliable and effective capacity provider with our technology leadership, manufacturing excellence and customer trust, we are well positioned to capture the growth from the favorable industry megatrend with our differentiated technologies. We expect our long-term revenue to be between 15% and 20% CAGR over the next several years in U.S. dollar terms, of course, fueled by all four growth platform, which are smartphone, HPC, IoT and automotive.

Valuation

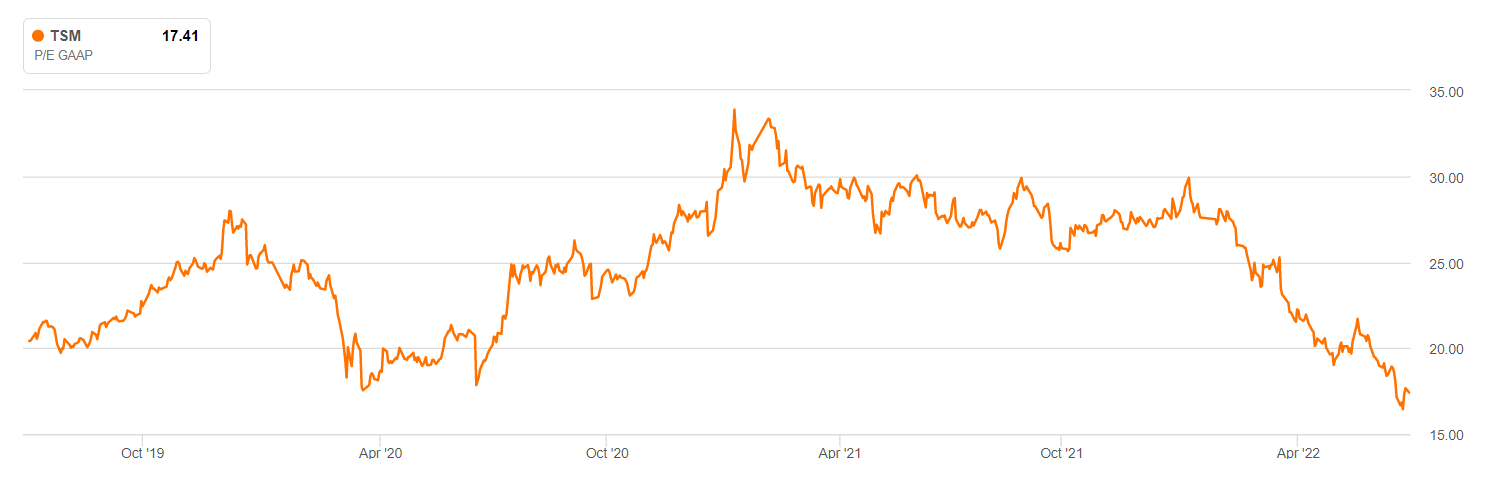

It gets even more beautiful once one looks at the valuation one has to pay for TSMC currently. TSMC was rewarded with a premium valuation over the course of the second half of 2020, but TSMC has not been spared from the broad-based stock decline in the last half a year. This means TSMC is now valued the same as it was two years ago, despite that quarterly revenue has almost doubled from a bit over $10B to a bit below $20B. Such a fierce growth rate (at very high scale) is usually what one would rather expect from best-in-class software companies.

In numbers, with $1.4 EPS in Q1, this implies a 14 P/E ratio. While investors may argue that the time of high valuations is over (at least for the time being), given TSMC’s growth, which as argued is likely to continue for the next decade, the company arguably deserves a premium valuation. Instead, the valuation has declined to a multi-year low. For comparison, even a no-growth company like PepsiCo (PEP) sports a 26 P/E. This means that the risk-reward ratio and the potential shareholder return from a position at the current price has significantly shifted in favor of long-term investors.

Seeking Alpha

In conclusion, the stock price may arguably double based on multiple expansion alone, and this is before any future increase in earnings, as investors expect TSMC to grow revenue by double digits through 2026.

Risks

The primary risk is a geopolitical one, as people often question what would happen if China invades Taiwan. Even if this is an irrational risk, it may nevertheless continue to weigh on the valuation.

Secondly, the next risk will arise in the next 5-10 years, which is the rise of Intel Foundry Services in conjunction with TSMC’s loss of process leadership to Intel. Nevertheless, as mentioned this risk is still far out, as Intel is only just starting to build the fabs that will one day build foundry chips. In addition, as noted the semiconductor industry is not a zero-sum game, as the overall pie is getting bigger over time. Lastly, in the short-term, Intel increasing its own reliance on foundry capacity for a variety of businesses (such as graphics) actually benefits TSMC.

Investor Takeaway

Simply put, TSMC is the Microsoft (MSFT) of semiconductors given its reliable and meaningful growth over time that, per TSMC’s guidance which is based on customer input, is set to continue well into the future. Nevertheless, at the time of writing, the shares are being sold for just 14x P/E. Given the trends discussed, the current price will more likely than not end up being seen as a very nice opportunity several years down the road, which means investors with the prescience to act now may be nicely rewarded.

Of course, there are still risks, but the most material one, which is the rise of Intel Foundry Services, fueled by Intel retaking process leadership, is at least half a decade away from becoming material in even the slightest way, as Intel is still waiting for the U.S. to fund the CHIPS act in order to build out its Ohio fabs. In Europe, production of the Germany fab is only planned to start in 2027 (!). In both cases, the timeline concerns the first one or two fabs at each location, not the potential $100B buildout (6-8 fabs) Intel has talked about. For some concrete numbers, even if Intel manages to grow IFS from scratch into a $10-20B business over the next 5-10 years, during the same time period the foundry industry may grow from on the order of $100B to $200B, which hence still leaves $180-190B for TSMC.

Be the first to comment