Petr Smagin

Published on the Value Lab 25/7/22

BRP Inc. (NASDAQ:DOOO) is an excellent company from an operating and end-market point of view. ROICs are high and the company benefits from a favourable industry structure. However, supply chain issues have been a big problem for the company after the initial powersports boom. Volumes are falling and profitability is taking its consequent decline. The question now is macro. Management believes that their end-market profile is strong enough to withstand the macro headwinds. We think they might be right. But with prices not too discounted from highs we aren’t compelled by valuation even if fundamentals might stay resilient.

Q1 Update

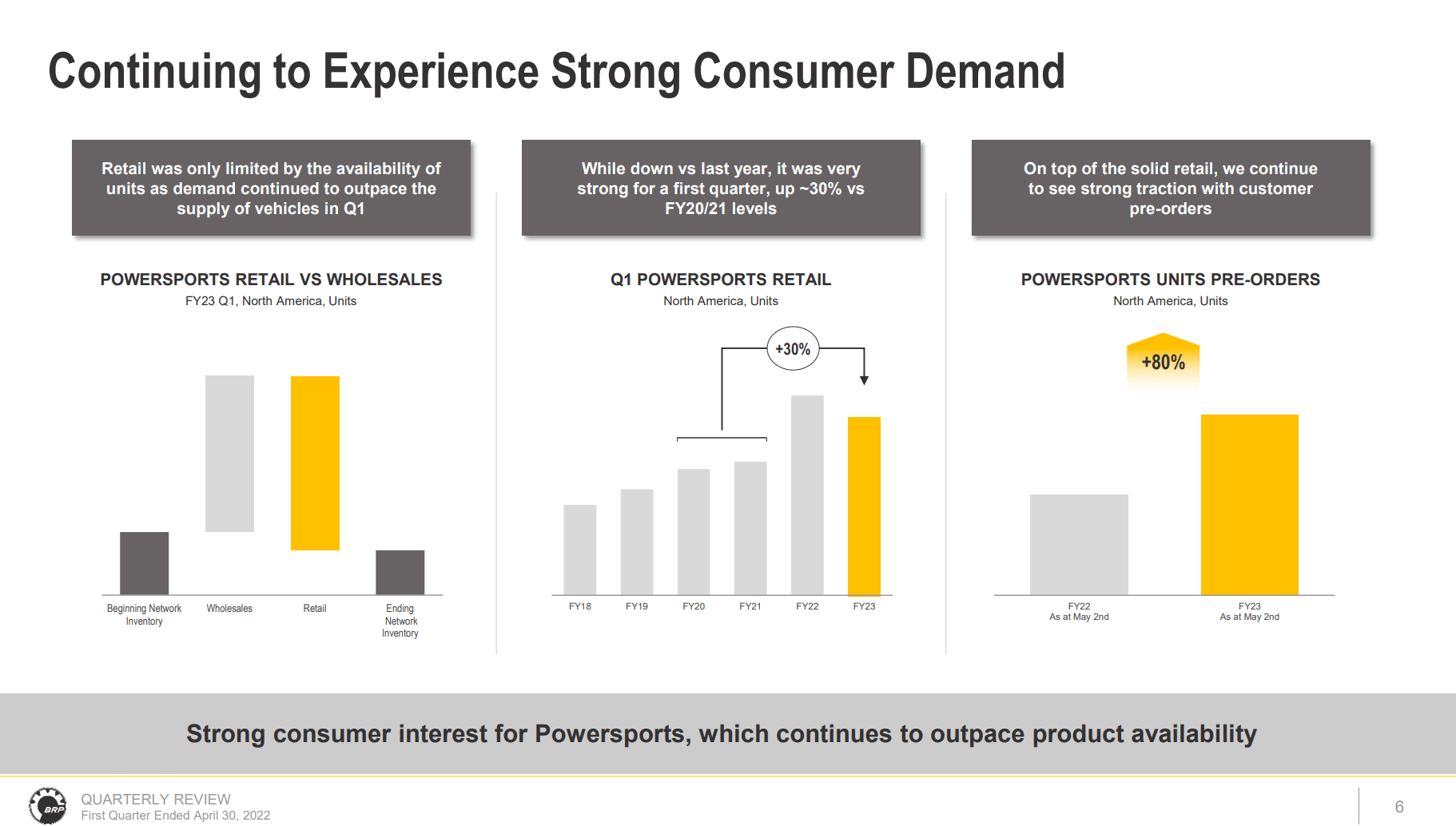

This quarter has been a quarter of declines. While BRP fared better than most in the industry, declines across products that sell this season average to around 9%. The situation with wholesale vendors entirely reflects the situation with them passing their inventory onto retail, almost 1 for 1.

Wholesale to Retail (Q1 2023 Pres)

In the last quarters the company has been relying on retrofit sales in order to keep customers happy. These retrofits continue to be conducted as of this quarter. Ultimately, the demand is pushing hard up against the supply and nothing except for the unleashing of supply chain bottlenecks can solve this problem.

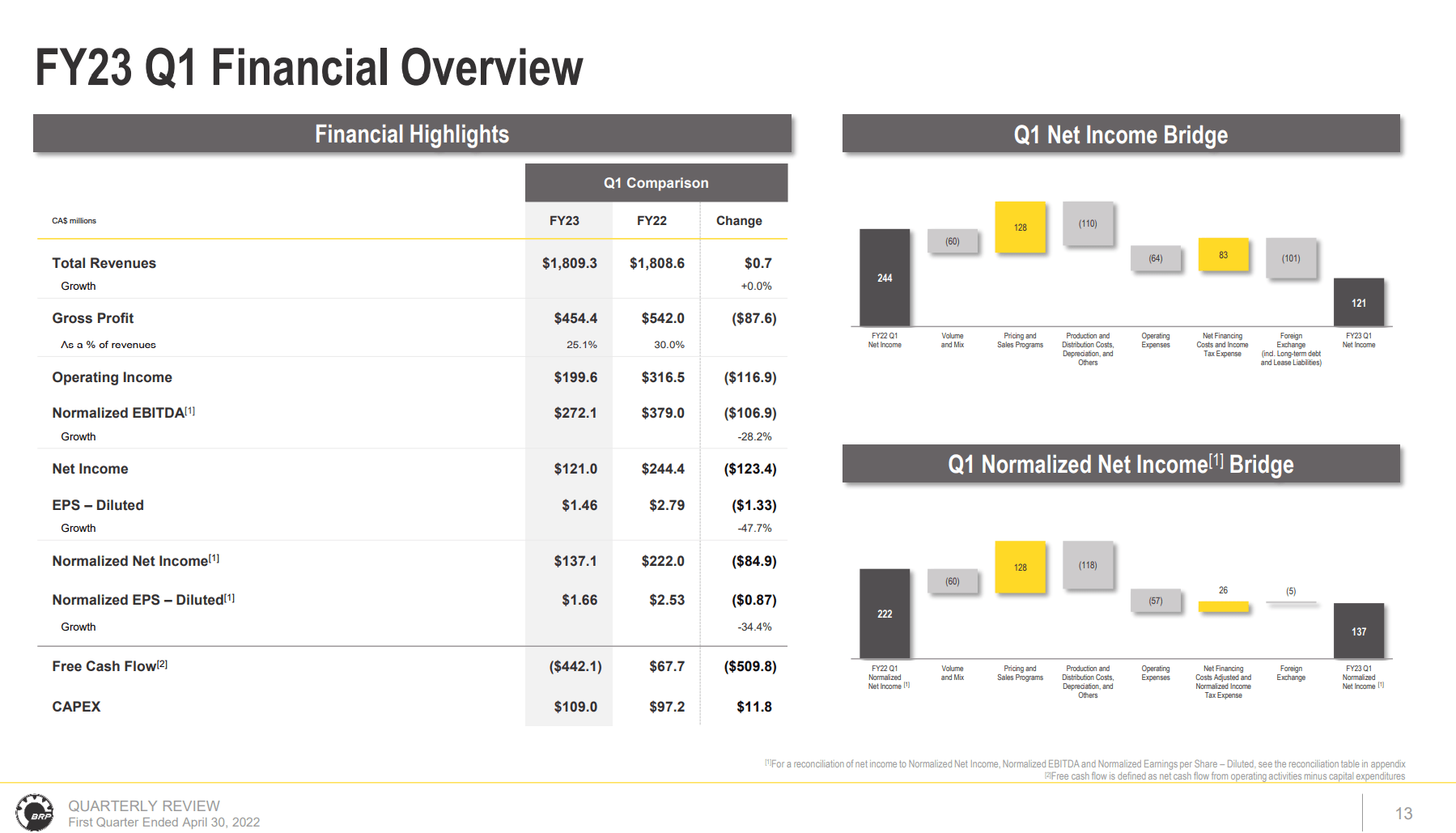

Volume declines are indeed the main feature of this quarter. Sales have remained stable because of pricing increases offsetting volume declines. But the volume declines haven’t been able to smooth over the G&A, and compression of the gross margin due to production inflation have still taken their effect.

DOOO Income Statement (Q1 2023 Pres)

EBITDA declined more than 25%, and gross profit almost 20%. Operating leverage is naturally in effect for an industrial business like BRP’s and the hurt is falling onto shareholders. Aftermarket revenues have been doing pretty well at least growing 14%, and we expect this 20% slice of revenues to be a more resilient element as the larger installed base produces more recurring cash flows through this segment.

Valuation and Conclusions

The company produces very high ROICs and in principle the valuation is quite low at 5.5x EV/EBITDA. In past pieces we’ve used TMA to demonstrate that at least using DCF logic the company is cheap. The problem is that DCF logic usually says companies are cheap. The market reality is that the company still trades quite a bit above pre-COVID levels and not too discounted (about 25%) from highs, about in line with the market. Indeed, sales are ahead of 2019 levels by a decent margin, and profits are ahead too again by at least an expected 20-50% margin, so ahead of pre-COVID probably makes sense. In fact, we agree with management that the company should be pretty resilient to the macro headwinds.

Craig, to be honest, we had our review with all our division before, obviously, our quarterly results and we challenged the team, and we don’t see right now slowing down in demand. Their customers and maybe it’s because our customers, our household income higher than the average, they don’t feel this impact.

Jose Boisjoli, CEO of BRP Inc.

Demand destruction from higher prices is more of a concern, also because it slows the aftermarket turnover if people are more cautious about using their vehicles. But as far as the macro risk goes pre-orders still haven’t fallen yet, and they probably would have if customers were anticipating concerns.

However, the unemployment spiral has yet to start and the economy could turn down a lot more from these levels.

In some respects BRP can be considered a little like the building products companies we cover, where releasing bottlenecks might actually be good for company volumes, with higher income end-markets capable of keeping up spending while the rest of the economy contracts. But a bet like that would be optimistic. While the company has traded down with markets, we still feel that the supply chain situation will persist at least a while longer. Being quite levered to market movements, even if its fundamentals are solid, we’d be wary to invest now. Perfect for the watchlist.

Be the first to comment