Niall_Majury/iStock Unreleased via Getty Images

[Please note that all currency references are to the U.S. dollar except if indicated otherwise.]

Brookfield Asset Management $47.00 (Toronto and NYSE symbol NYSE:BAM; Investment Management; Shares outstanding: 1.65 billion; Market cap: $80.1 billion; www.bam.brookfield.com) is a global manager of alternative assets headquartered in Toronto, Canada. The company commenced trading on the NYSE and Toronto stock exchanges under its current name in November 2005 but its origins date back more than 100 years.

Brookfield (“BAM”) has a solid track record of growing its asset management franchise and generating acceptable investment returns – both on behalf of its clients and the corporation’s proprietary capital. Nevertheless, considerable tailwinds in the form of low-interest rates, and strong public and private markets helped alternative asset managers, including Brookfield over the past decade. However, the environment is changing rapidly – the party is over.

Understanding the Brookfield business

Brookfield has two separate business operations. The first is the asset management business which generates fees in various formats. The second is the investment business which holds the company’s proprietary investments – these investments generate dividends and (hopefully) increase in value over time. There is also a complementary feedback loop between the two businesses – competitive investment returns in the investment portfolios attract more external client money which in turn generates more fee income for the asset management business.

The Asset Management Business

Brookfield is a global manager of alternative assets -the main categories are real estate, infrastructure, renewable energy, private equity, and credit. The total assets under management at the end of March 2022 were $730 billion while fee-bearing capital amounted to $379 billion. The bulk of the assets are located in the U.S. (62%), followed by Europe and the Middle East (19%), Asia Pacific (12%), and South America (6%).

Brookfield offers a large number of investment avenues for its investors, including public vehicles, segregated accounts, and private funds covering all these asset classes.

The management of these investments generates fee income for the company. The fee income consists of base management fees, incentive distribution fees, performance fees, and carried interest. Brookfield also earns transaction and advisory fees related to the closing of transactions.

Key profit drivers of this part of the business are the quantum of fee-bearing assets under management that can generate fee income, as well as the investment returns which can trigger performance fees and carried interest.

At the end of March 2022, the largest portion of the fee-bearing capital resided in the credit business (35%), followed by real estate (22%), infrastructure (20%), renewables (14%), and private equity (9%).

The credit business falls under Oaktree, a global manager of credit, private equity, real assets, and listed equities. Brookfield paid $5.0 billion for a 61.2% interest in 2019. Assets under management amount to $164 billion, up from $120 billion at the time of the acquisition.

The Investments

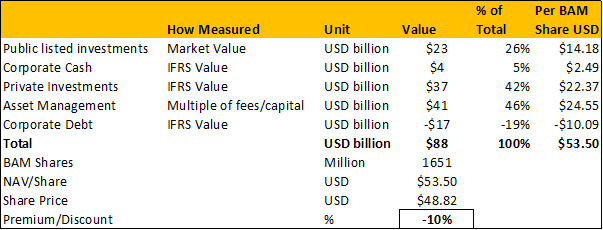

Brookfield is a co-investor in most of its endeavors with $65 billion of invested capital at the end of March 2022. Control of this portfolio of investments holds significant benefits to BAM – first, it allows BAM to extract various fees for the management of the assets. Second – the investments provide a regular and substantial cash flow in the form of distributions.

The bulk of the capital is invested in real estate assets, with an IFRS balance sheet value of $32.7 billion by the end of March 2022. A large portion of these assets used to be housed in a listed vehicle, Brookfield Properties Partners which was privatized in mid-2021. The real estate portfolio is split into 3 segments, namely a core portfolio of “trophy” properties, a development or redevelopment segment, and finally a group of properties held for sale.

Also, under the real estate umbrella falls a residential development arm that operates mainly in North America and Brazil. The equity value of this unit is $2.2 billion.

Renewable power falls mainly under the umbrella of the listed Brookfield Renewable Partners (New York symbol BEP). The current market value of BAM’s 48% economic interest in BEP is $11.4 billion. BEP owns a global-scale renewable power portfolio which includes 8,133 megawatts of installed hydroelectric capacity, 5,411 megawatts of installed wind capacity, and 2,633 megawatts of installed solar capacity.

Infrastructure investments are housed in the listed Brookfield Infrastructure Partners (New York symbol BIP). The current market value of BAM’s 27% economic interest in BIP is $8.6 billion. This portfolio includes electricity transmission lines, toll roads, LNG terminals, oil and gas pipelines, and telecom towers.

Private equity investments are owned and operated mainly through the listed Brookfield Business Partners (New York symbol BBU). BAM owns an economic interest of 64% in this business which currently has a market value of $3.4 billion. This segment is active in a wide range of activities, including residential mortgage insurance, offshore oil services, modular building leasing, energy storage, and solar power solutions.

Other minor holdings include the listed Brookfield Asset Management Reinsurance Partners (New York symbol BAMR) in which BAM holds a 63% economic interest. Notably, the CEO of Brookfield, Bruce Flatt also holds a 10% interest directly in this entity. Together, these smaller investments have a book value of $2.1 billion. There is also corporate cash of $4.1 billion.

A reasonable track record

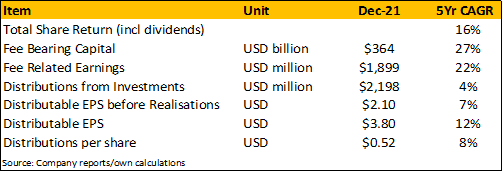

The share price of BAM performed well over the past 5 years, generating a total return of 16.2% per year. This was ahead of the S&P 500 and the MSCI All Country Equity Index but well below the returns of other leading alternative asset managers, Blackstone (BX), KKR (KKR), and Apollo (APO).

In the table, we highlight some of the key metrics that indicate the performance of the BAM asset management business.

Fee Bearing Capital: This is all the invested and committed capital held in the perpetual affiliates, private funds, segregated accounts, and liquid strategies, that can earn a fee. It is a key performance measure for BAM and has shown strong growth over the past 5 years. However, the acquisition of Oaktree in 2019 added $120 billion; excluding this, the annual growth was somewhat less impressive at 17%.

Fee-Related Earnings: This includes the base management fee, incentive distributions, performance fees, and transaction and advisory fees adjusted for direct costs and minority interests. The base management fee normally makes up more than 80% of the total fees and is more consistent from year to year than any other fee income.

Distributions from Investments: This represents all distributions received from the proprietary investments held by BAM, including BEP, BIP, and the real estate portfolio. These distributions form an important part of the BAM cash flow.

Distributable Earnings before Realizations: This is all fee revenues plus distributions from investments adjusted for corporate expenses and preferred share costs. It excludes the highly variable realized carried interest and gains from dispositions and presents the best measure of sustainable performance.

Distributable Earnings: All realized carried interest and disposition gains are added to the fee revenues and income from distributions to arrive at this measure.

Distributions per Share: This is the quarterly distribution paid by BAM to its shareholders. It should be noted that BAM also pays an infrequent special distribution not included in the calculations below.

Company/Analyst’s own calculations

The overall picture based on these key performance measures is one of solid but not outstanding growth, especially at the per-share level.

Optimistic growth expectations

At the investor day in September 2021 (and confirmed again at the June 2022, AGM), top management laid out aggressive growth plans for the next 5 years. Forecasts were based on strong expected growth in fee bearing capital, fee-related earnings, distributions from investments, and realized carried interest.

Growth Forecasts: 5-Year Plan

Item |

Measure |

Level 2021 |

Expected 2026 |

5Yr CAGR |

Fee Bearing Capital |

USD billion |

$364 |

$830 |

18% |

Fee-Related Earnings |

USD million |

$1,899 |

$3,200 |

11% |

Distributions from Investments |

USD million |

$2,198 |

$4,100 |

13% |

Distributable Earnings before Realisations |

USD million |

$3,348 |

$8,200 |

20% |

Realised Carried Interest |

USD million |

$715 |

$2,900 |

32% |

Source: Company documents

In some respects, these forecasts seem optimistic, but it is worth pointing out that management has a good track record of meeting their longer-term forecasts.

New development segments such as insurance and technology hold potential for future growth and may support the efforts to achieve the growth targets. The BAM CEO is on record seeing a $100 billion opportunity for the technology team (“software is the new infrastructure” he says) and a $200-$300 billion opportunity for the insurance solutions team.

The Brookfield Transition Fund is another area that may provide impetus to the growth plans. Brookfield hired Mark Carney (ex-Governor of the Bank of Canada and Bank of England) in 2020 to promote this fund. The first tranche of the fund is expected to raise $15 billion but the CEO sees a $200 billion investment opportunity in this market. Capital raised will be invested in renewable energy projects, and projects to help industrial companies to decarbonize their production processes.

Asia is another area of growth targeted by Brookfield. The company has already invested capital in Australia, China, India, and South Korea. A regional head office was established in Shanghai, and a total of $13 billion of assets are held across renewable energy projects and real estate. In India, the company has invested in real estate, telecom towers, toll roads, and renewable energy projects.

Still, we would consider these forecasts as very optimistic and specifically point to the high growth expectations for the distributions from investments and carried interest. It is difficult to foresee an environment where stable, long-term assets such as those that form the bulk of the investment portfolio can grow their distributions by 13% per year.

Also of concern is the 4-fold increase in realized carried interest. The monetization of carried interest depends on the performance of assets subject to meeting minimum return hurdles; this leaves the eventual outcome uncertain until such time that the fee is realized.

The party is over

The macro-environment has been exceptionally favorable for leveraged, long-life investments in real assets over the past decade. Low-interest rates, combined with reasonable economic growth and booming stock markets provided the backdrop for these types of assets to perform well.

Institutional investors, especially those with conservative mandates and long-term liabilities such as pension funds and faced with low yields on fixed-income products, routed large amounts of capital to real asset experts such as Brookfield. According to the Willis Tower Watson Global Pension Assets Study, 2022, investments in real assets and alternatives now form 19% of pension fund portfolios, a four-fold increase over the past 2 decades.

And 2021 was an absolute blow-out year for dealing in private assets. The consulting firm Bain & Company stated in its 2022 report on Global Private Equity that the value of global buyout deals broke all previous records and was more than double the 2019 and 2020 levels.

Higher interest rates may curb this enthusiasm as yields offered by government bonds and investment-grade corporate bonds become more attractive. Higher interest rates also may continue to lower public market equity valuations; this message will eventually depress valuations in the private markets as well and lower the returns generated by private market investments. This will curb the base management fees, carry fees, and incentive fees that BAM can earn from its pool of assets.

BAM holds a limited amount of debt on the corporate balance sheet. However, the pooled investment vehicles are highly leveraged. Of particular concern would be the private equity and real estate portfolios that carry large amounts of debt with relatively short durations on average. In a higher interest rate environment, these investments may struggle.

Asset Management spin-out

Brookfield intends to list its asset management business separately in both New York and Toronto and will distribute a 25% interest to shareholders of BAM later in 2022. The justification is that a separation will make it easier for investors to understand and value the asset management business and possibly attract new investors that are interested in a “pure-play” alternative asset manager.

After the separation, BAM will hold a 75% interest in the asset management business plus all the other proprietary investments that it currently holds. On a stand-alone basis, BAM estimates that the asset management business could be worth $80 billion or $48 per share. If this proves to be correct, the distribution will be worth $12 per BAM share. This seems optimistic – see our estimates below under “Valuation.”

At the end of March 2022, the unconsolidated BAM corporate balance sheet showed shareholders’ equity of $43.3 billion, preference shares of $4.2 billion, and total debt of $11.2 billion.

The debt to capital ratio was 17%. Brookfield generally received favorable credit ratings from all the major rating agencies, including an S&P A- rating for the long-term senior unsecured debt.

Fair corporate governance but management is in absolute control

Frank McKenna is the independent chair of the board of directors, a position held since 2010. Bruce Flatt is the CEO of Brookfield. He was appointed as the CEO of Brascan (the previous name of Brookfield) in 2002 and remained in this position post the name change in 2005.

The directors, executive officers, and other partners own directly and indirectly over 300 million (or 18%) of the Class A and Exchangeable Class A shares. Class B shares are owned exclusively by BAM Partners Trusts, representing a group of current and former senior executives.

Class A & B shares allow shareholders to vote on matters that need to be approved by shareholders. All ordinary resolutions must be approved by a simple majority of Class A and Class B voting shareholders. Special resolutions must be approved by a two-thirds majority. This effectively provides a veto on all decisions to the holders of the Class B shares, i.e., the BAM Partners Trust or senior executives.

Executive compensation is aligned with the board’s objective of building a global asset management business focused on sustainable cash flows over the long term. A large portion of management rewards is therefore linked to the value of Brookfield’s shares. Over the past 5 years, the main executives received 85% of their compensation in long-term share ownership awards. The balance came in the form of a base salary and annual incentive plan.

Valuation…the market is spot on

The valuation of BAM is a nebulous exercise given the consolidation of the controlled proprietary investments as well as the asset management business in the financial statements.

Nevertheless, we follow an approach of valuing the listed investments at market value, the real estate business, and other assets at the balance sheet values and then estimate a value for the asset management business.

We place a value of $41 billion on the asset management business, which is the average of two valuation methods. First, a multiple of fee income – we apply a 17.5 times multiple on the fairly stable fee-related earnings and 7.5 times multiple on the highly variable realized carried interest. A second method applies a proportional value on the fee-bearing capital of the asset management business (11% of fee-bearing assets which is similar to Apollo and KKR); this yields a slightly higher value.

A fair value range, applying higher and lower valuation multiples- yield a value for the asset management business between $30 billion and $50 billion – still a long way off from management’s estimate of $80 billion.

On our estimate, BAM is trading at a 10% discount to its asset value – which seems about right – given the portfolio holding structure and the opaque balance sheet.

Key value metrics (Company/analyst own calculations)

Bottom line …solid business but wait for a better entry point

Brookfield has built a solid business against a very favorable macro backdrop. In a higher interest rate environment, slower economic growth, and less favorable public market conditions, gains will be harder to come by. Capital inflows may also slow down as pension funds and other institutional managers find less risky alternatives in their traditional hunting ground of investment-grade fixed income.

Written by Deon Vernooy, CFA, for TSI Wealth Network

Be the first to comment