RgStudio/E+ via Getty Images

The consumer finance industry is still under pressure amidst macroeconomic volatility. Bread Financial Holdings, Inc. (NYSE: BFH) is not an exemption, but it shows resilience and durability. From its disappointing 2Q results, it picked itself up and bounced back in 3Q 2022. Today, market headwinds and risks are visible, but its capacity to withstand the blows remains high. Its excess liquidity provides it with more flexibility and stability.

Moreover, it remains well-capitalized, allowing it to cover dividends with decent yields. The stock price stays in a downward pattern but may open a potential buy entry point. And even if the target price increases to $50, it still offers a decent yield, which proves its cheapness.

Company Performance

Bread Financial Holdings, Inc., formerly Alliance Data Systems, has been in the business for quite a long time now. Over the years, it has rapidly grown through a series of expansions. Its capitalization on growth through prudent acquisitions has been fruitful. In the last two years, it had the biggest transformation. Although it has always been known as a private-label credit card lender, the addition of Bread led to a massive change. Now, BFH has already streamlined its business processes. The adoption of a new business model has changed the course of its activities. Its buy now/pay later pattern is becoming more popular across the state. However, it has been having a hard time unleashing its potential. After all, 2022 has been a year of macroeconomic disturbances. The high-inflation environment has resulted in cost and interest pressures in the consumer finance industry. And Bread Financial Holdings, Inc. was no exception.

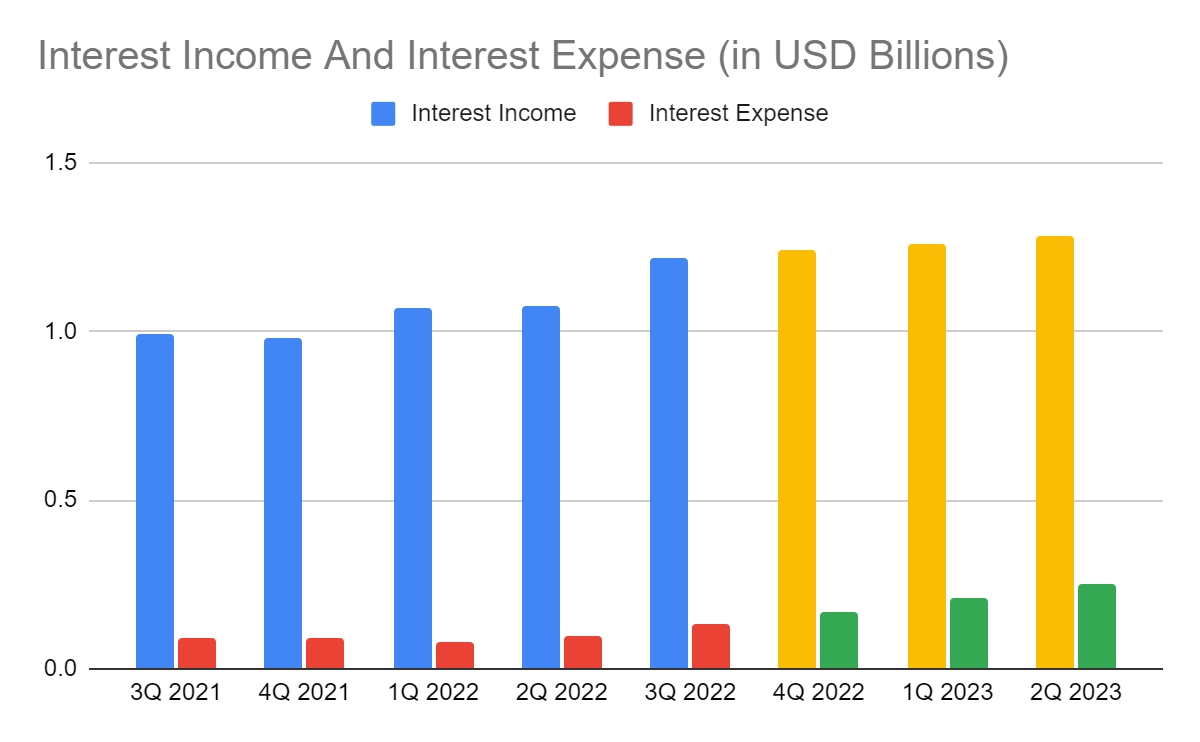

Thankfully, it stays a durable and solid company with its well-balanced revenues and margins. 2Q 2022 was its lowest point, given the sharpest increase in expenses, leading to a very low margin. But today, it continues to prove its resilience as it bounces back and stabilizes revenues and expenses. Its interest income amounts to $1.22 billion, a 24% year-over-year growth. This tremendous growth can be pointed to various factors. First, the acquisition of Bread raised its operating capacity. Second, interest rates keep increasing, making credit loan yields higher. It should not be surprising at all since interest rate hikes match the elevated inflation. Although inflation has maintained its lull, it remains higher than pre-pandemic levels. Consumers have to ensure their capacity to make ends meet amidst the rising prices. And turning to credit cards is one of the swiftest choices to make. As banks become stricter and impose higher borrowing costs, credit cards come in handy. It coincides with the sustained emergence of the digital and fintech revolution. As hybrid work setups and e-commerce prevail, the need for cashless payment methods keeps increasing. In 2020, cash transactions dropped in favor of digital wallets and credit cards. It was most evident in mature economies, such as the US, given the sharp drop from 51% to 22% over the past decade. Even better, many credit card providers now allow the use of virtual credit cards for easier transactions.

Interest Income And Interest Expense (MarketWatch And Author Estimation)

Third, it maintains its deep ties with large companies, such as American Express. With that, it maintains its solid customer base and access to its exclusive offers. Lastly, Bread Financial is doing an excellent job in diversifying its other interest-sensitive portfolio. Its investment securities are relatively a minor interest income component, but its yield is now ten times higher than the comparative quarter. Although their fair value is lower, their yields are firing up as their inflation-lined nature matches with the current market changes.

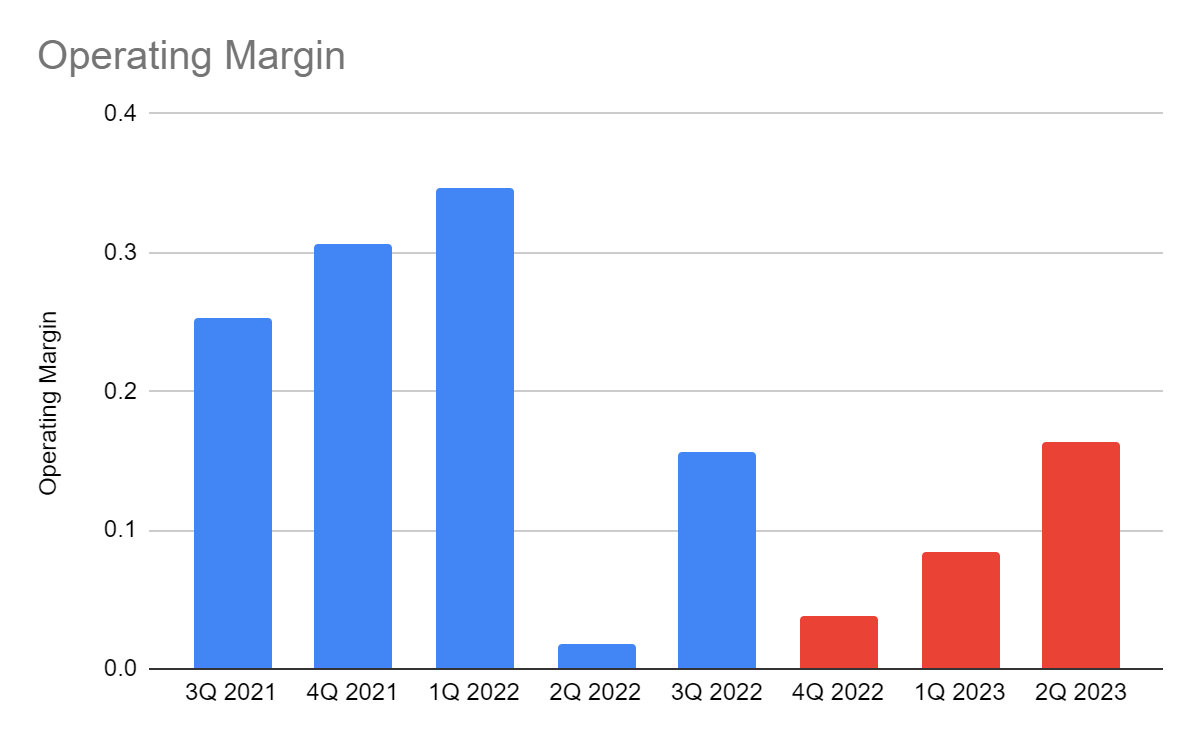

With regard to expenses, BFH does well in stabilizing them. Interest expense is also in an uptrend. That’s a given. It is now 46% higher than its value in 3Q 2021. That’s about twice the increase in interest income, which shows that deposits are more interest-sensitive. Even so, it is logical since the amount of deposits in the Balance Sheet has increased about twice the increase in loans. I will discuss more of them in the next section. It is also logical since higher interest rates entice more deposits due to higher yields. Despite this, net interest margin drops. Meanwhile, non-interest expenses are now more stable. Thanks to the continued inflation lull, helping the company adjust its larger operating capacity better. So, the operating margin is now 16%. Although it is lower than in 3Q 2021 at 25%, it is still a massive rebound from 2Q 2022 at only 2%. The good thing is that the company maintains its viability despite extreme macroeconomic conditions.

As we wait for the 4Q report, I stay optimistic about the stability of its performance. I cling to the positive impact of the continued inflation lull. Interest rate hikes may continue to impact its loan and deposits. It may also capitalize on its excess liquidity to maximize its potential. Of course, it must be more careful as I expect interest rate hikes to intensify and peak in 1Q and 2Q 2023. I will discuss more of these factors in the next section. Hence, interest income and expenses may continue to increase and offset each other’s impact. Provisions may increase further as risks become more evident. Meanwhile, the increased spending on technology and credit card processing system transition may put cost pressures on 4Q margins. But overall, non-interest expenses may become more manageable as the inflation lull continues. Also, its strategic investments may pay off by improving operational efficiency. It can enhance cost-reduction strategies for more stable margins. A rebound may also be expected in the succeeding quarters.

Operating Margin (MarketWatch And Author Estimation)

How Bread Financial Holdings, Inc. May Fare This Year

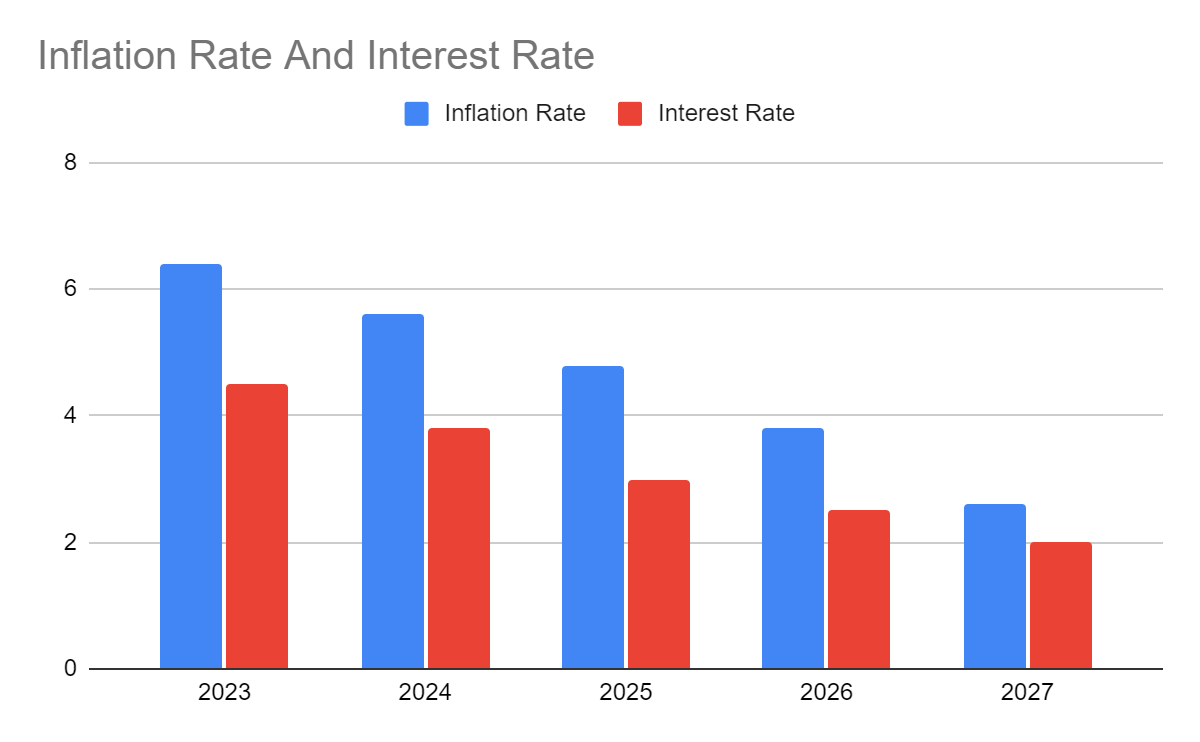

Bread Financial Holdings, Inc. operates in a highly cyclical industry. As such, macroeconomic changes can have a substantial impact on its performance. We already saw it in its recent reports. Despite this, I affirm my optimistic view about its stability this year, given the continued inflation lull. It is now at 6.5%, showing that it has decreased faster than expected. Since it is now 30% lower than its highest point in 2022, managing expenses is easier. The decrease can be sustained, given the improvement in supply chains across industries. Most of them are now seeing the end of their backlogs. Of course, the challenge stays in the real estate sector as inventories cannot still meet the demand despite the skyrocketing prices. But I digress. That is the impact of builders being conservative, and not ramping up since the Global Financial Crisis. That’s quite a different story. Meanwhile, interest rates may increase further since the Fed must not take chances. I expect them to peak in the first half of 2022, raising interest income and expenses. In the second half, we may see it still increasing, but increments may slow down. I set my projection at 4.5-4.8% versus the 5-5.25% consensus estimates. I am also not buying the recession fears, although I don’t discount volatility. Note that the current inflation is caused by demand-pull. It may be more spectacular since there have been supply chain disruptions. But the impact of demand is more prevalent. And we can see now that interest rate hikes are working to stabilize inflation. The unemployment rate also stays stable since it is still a far cry from the labor market situation during The Great Recession. The US economy remains challenged, but it is still doing fine. Macroeconomic prospects may not be robust this year, but stability may improve. The same applies to Bread.

Inflation Rate And Interest Rate (Author Estimation)

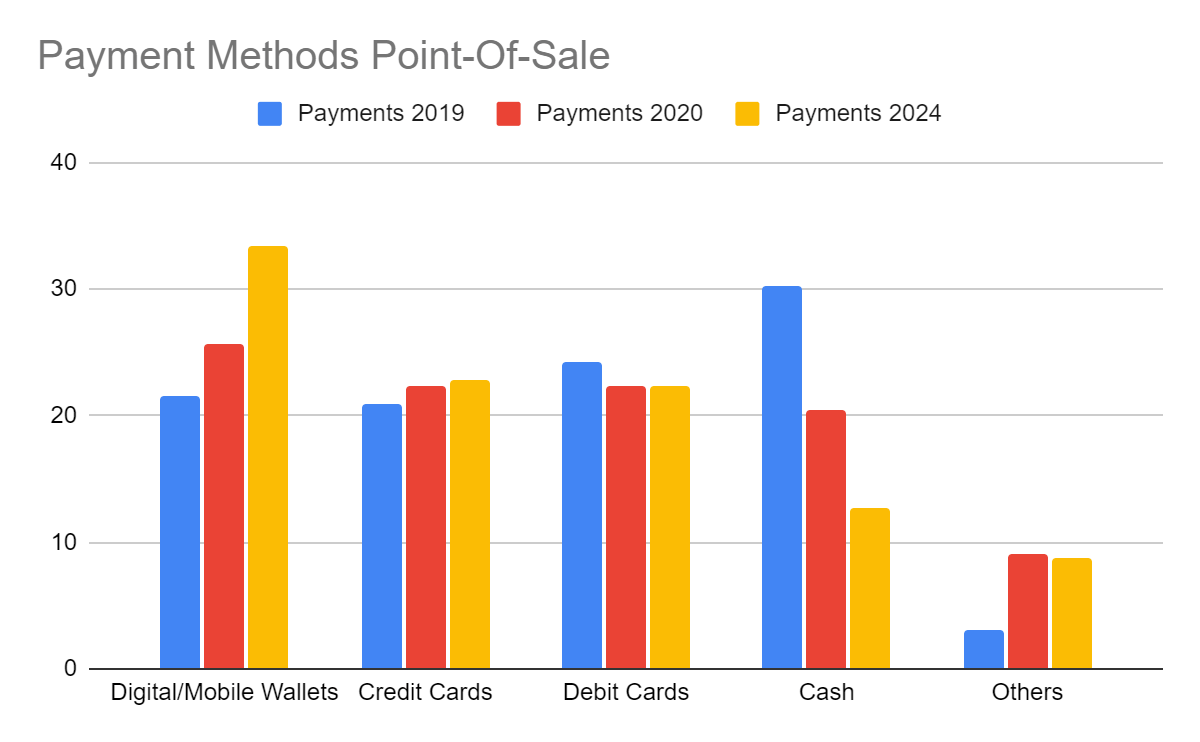

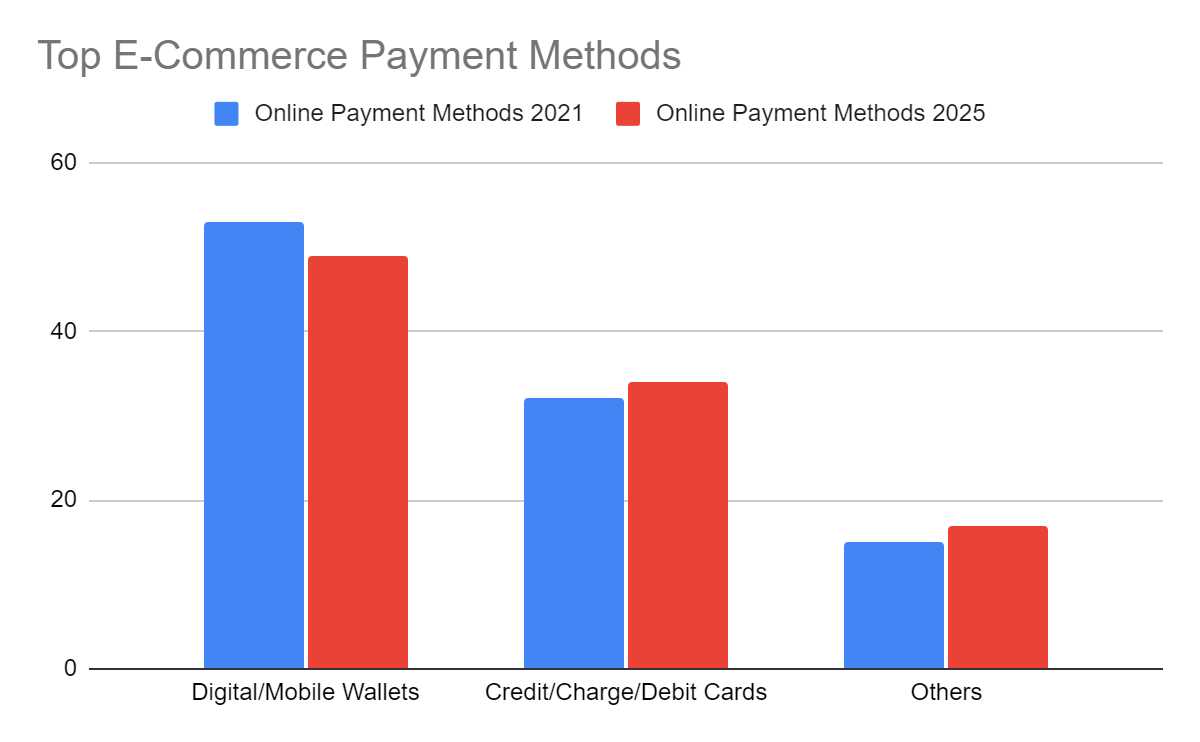

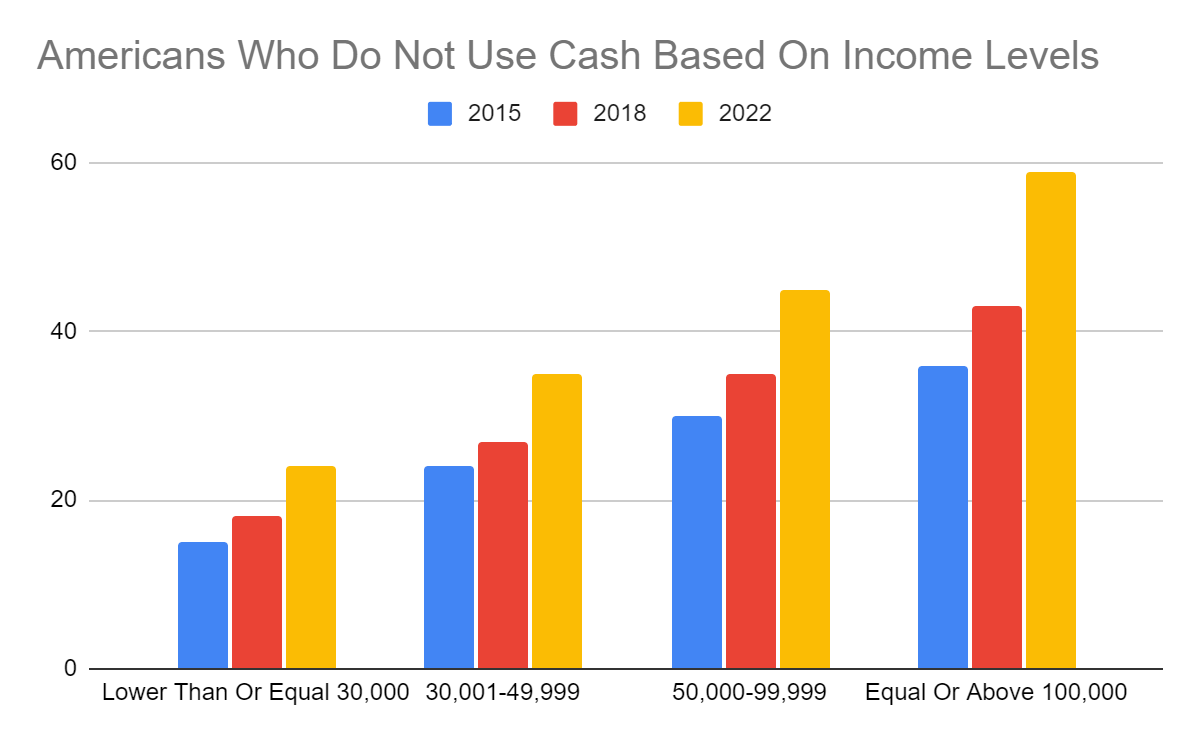

Other potential driving forces are the increased preference for cashless payment methods and the rise of e-commerce. We have already discussed the massive change in cash transactions in the last two years. Since 2022, we have seen a sustained increase in cashless transactions. We will start with the behavioral factor that may drive it before delving into actual statistics. As we all know, remote and hybrid work setups persist as many businesses realize their advantages. In turn, people busy working at home opt to have their food and other items delivered. Also, they opt to browse the internet for personal transactions. Businesses also adapt to automated invoices as they veer away from auditing piles of invoices on their tables. E-commerce becomes more popular as more customers and entrepreneurs go online. Even traditional brick-and-mortar stores are adapting to the fintech revolution. Statistics show that point-of-sale and e-commerce payment methods have increased their preference for digital/mobile wallets. Credit cards take the second spot, followed by debit cards. Even better, many mobile wallets and apps, such as PayPal and Grab accept credit cards for transactions. It is no surprise that credit cards remain a staple and are here to stay. Moreover, many Americans across different income levels are shifting away from cashless transactions. From 2015 to 2022, Americans earning $100,000 and above showed the most massive increase in those not using cash for transactions anymore. Those in lower income brackets moved slower in 2015-2018, but there has been a sharp uptrend in 2022. We can attribute it to pandemic restrictions, e-commerce, and the current macroeconomic changes.

Payment Methods Point-Of-Sale (Statista)

Top E-Commerce Payment Methods (Statista)

Americans Who Do Not Use Cash Based On Income Levels (Pew Research Center)

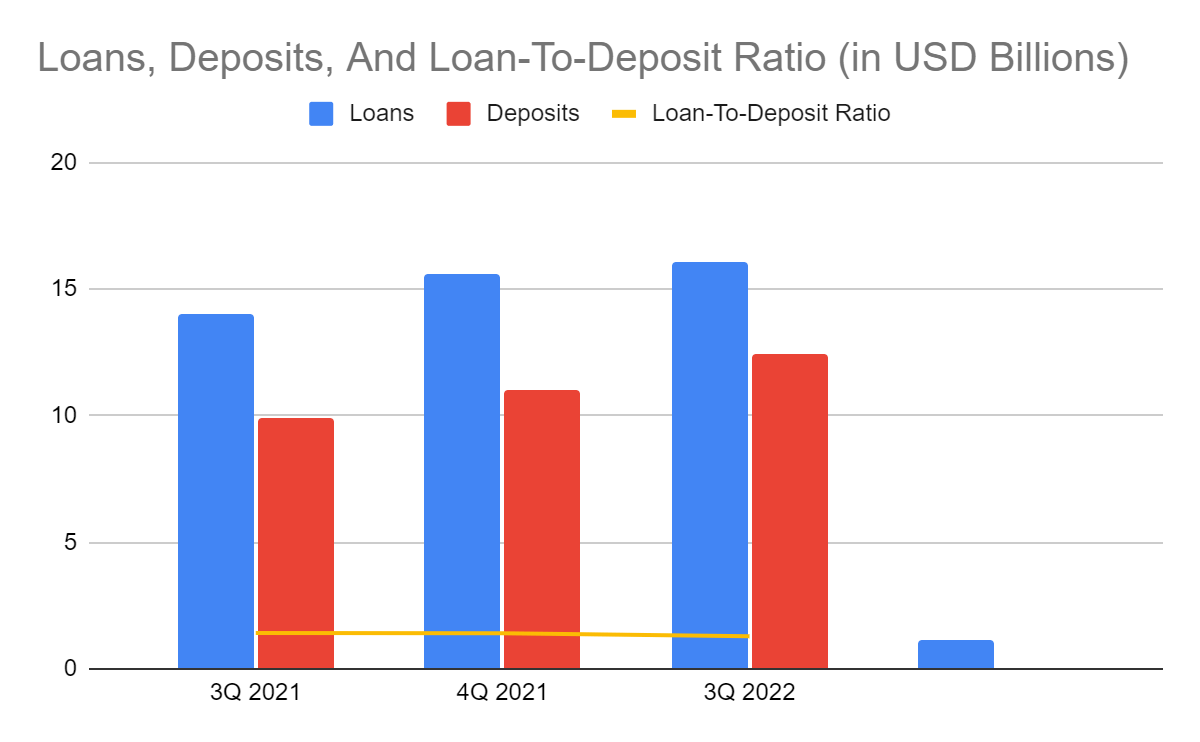

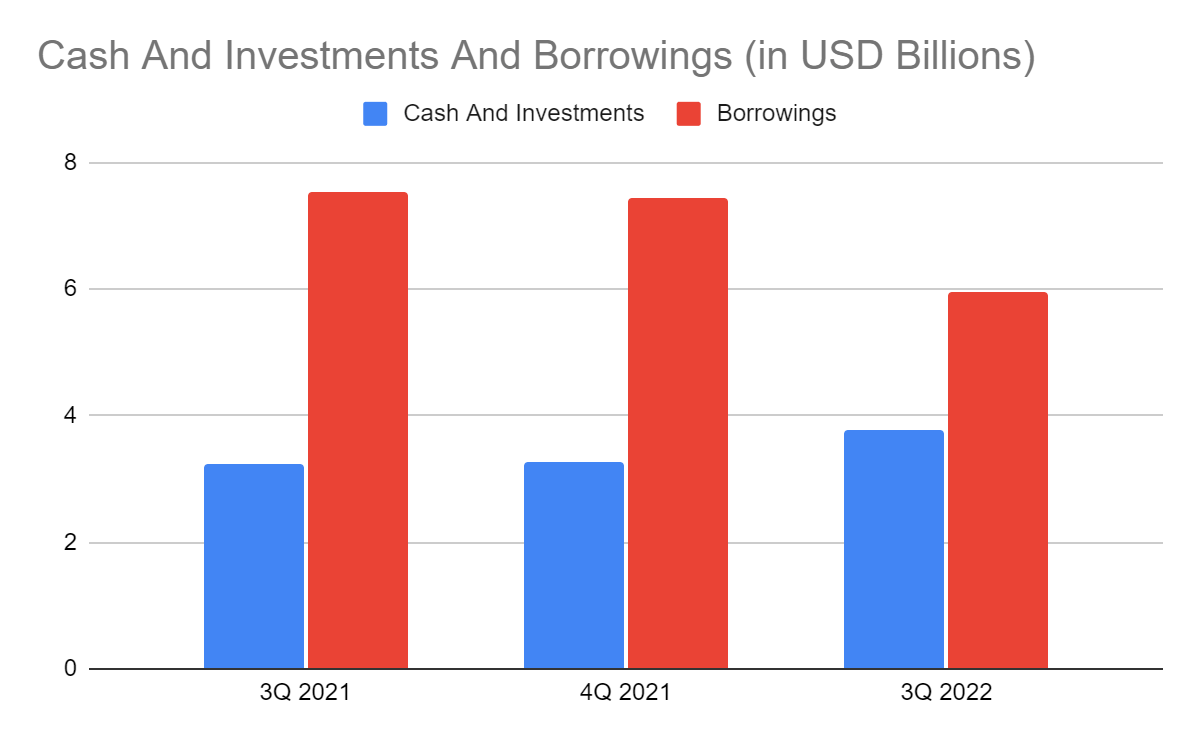

After analyzing these external factors, we must determine what makes Bread a solid company. And it’s not hard because its fundamental stability says it all. It has excess liquidity, which it can capitalize on to maximize its potential or cushion the market blows. Loan growth stays impressive, matched with substantial yields. Despite this, the company must not be too relaxed since delinquencies had a noticeable increase as per its October and November update. The good thing is that it derived higher yields while remaining conservative with its increased credit loss allowances of 12%. Also, the loan-to-deposit ratio has decreased from 142% to 127%. Moreover, its cash reserves are adequate and stable to sustain its operating capacity. The value keeps increasing, which reflects the stable yields and cash inflows. Borrowings keep decreasing, which is a wise move for the company in a high-interest market. Its liquidity is also proven by its Net Debt/EBITDA Ratio of 2.43x, lower than the average 3.5-4x. It shows that BFH has enough core operating earnings to cover borrowings. As such, it has a well-managed balance between its rebound and growth and fundamental stability.

Loans, Deposits, And Loan-To-Deposit Ratio (MarketWatch)

Cash And Investments And Borrowings (MarketWatch)

Stock Price Assessment

The stock price of Bread Financial Holdings, Inc. remains hammered. There has been a slight uptrend in the last few weeks, but the bearish pattern stays prominent. At $40.32, it has been cut by 41% from its value last year. Despite this, the sharp dip may open an opportunity for buying shares. NASDAQ 2022 estimates agree with the current pattern, which shows a negative 4Q 2022 EPS. But for 2023, it anticipates a sharp rebound, given its estimated EPS of $11.2 and the current price-earnings multiple of $4.8. It gives a target price of $53.98. Meanwhile, I estimate the EPS at $8.84, which gives a target price of $42.42. Either way, the stock price may have an upside potential. It is further confirmed by the tangible book value of the company. Its current TBVPS is 38.3, which is lower than its value of 57.2 last year. Indeed, the stock price follows the downtrend in fundamentals. And it is safe to say that it reflects the intrinsic value of the company. However, the decrease appears way sharper than it should be. The current PTBV of 1.1x is way lower than the average of 1.48x. If we use this to find the target price, the value will be $50.74. It shows that the current pricing is undervalued by about 20% and may bounce back.

Moreover, the company remains consistent with its well-covered dividends. Dividend yields are decent at 2.16%, which is way higher than the S&P 600 average of 1.5%. If we match it with the target price of $50, yields will stay higher at 1.68% while the dividend payout ratio is only 12%. To assess the stock price better, we will use the DCF Model.

FCFF $202,000,000

Cash $3,500,000,000

Borrowings $5,900,000,000

Perpetual Growth Rate 4.8%

WACC 9.2%

Common Shares Outstanding 49,800,000

Stock Price $40.32

Derived Value $44.87

The derived value agrees with the supposition of undervaluation. There may be an 11% upside in the next 12-18 months. Investors must use this as an opportunity to buy shares at a discount.

Bottom line

Bread Financial Holdings, Inc. remains challenged but exudes resilience and fundamental stability. It can withstand market blows while sustaining its potential rebound. It also has excess liquidity to cover its capacity, borrowings, and dividends. Meanwhile, the stock price is consistent with fundamentals and appears an ideal entry point to make a position. The recommendation is that Bread Financial Holdings, Inc. is a buy.

Be the first to comment