Pgiam/iStock via Getty Images

Almost four months ago, I recommended purchasing Brandywine Realty Trust (NYSE:BDN) for its attractive dividend, which was well-covered by cash flows, and its 10-year low valuation level. Since my article, the stock has declined 25%, to a fresh 10-year low, mostly due to the impact of high interest rates on the interest expense of the REIT. Nevertheless, Brandywine recently refinanced its debt and thus its next debt maturity is in late 2024. In addition, the trust is likely to recover strongly whenever inflation moderates. Thanks to its exceptionally low price-to-FFO ratio of 4.5, Brandywine is likely to highly reward patient investors when inflation reverts towards its normal range.

Why the stock has slumped

Brandywine has plunged 55% over the last 12 months due to the triple impact of inflation on the stock. First of all, the surge of inflation to a 40-year high has greatly increased the operating expenses of most REITs. However, Brandywine has proved superior in this aspect so far, as it has protection from increases in operating expenses on 81% of its leases. This has been prominent in the performance of the REIT. In the third quarter, its operating expenses dipped 2% over the prior year’s quarter.

Another effect of inflation is on the interest expense of Brandywine. The Fed has raised interest rates aggressively in order to restore inflation to its long-term target of 2%. Higher interest rates significantly increase the interest expense of most REITs, which carry an appreciable amount of debt. Brandywine is not an exception to this rule. In the third quarter, its interest expense grew 12% over the prior year’s quarter, from $15.9 million to $17.8 million.

As long as interest rates remain on the rise, they are likely to exert pressure on the results of Brandywine. The trust has an interest coverage ratio of 1.1 right now. It is also important to note that the REIT has a material debt load, with a leverage ratio (Net Debt to EBITDA) of 7.2 and net debt (as per Buffett, net debt = total liabilities – cash – receivables) of $2.1 billion. This amount is approximately 9 times the annual funds from operations [FFO] and hence it is not low by any means. However, Brandywine expects to post an improved leverage ratio of less than 6.9 for the end of 2022.

Investors should also realize that the Fed has slowed its pace of interest rate hikes and expects to end its cycle of interest rate hikes at some point in the first half of the year. In addition, the REIT is doing its best to manage its debt as efficiently as possible. It has cancelled some acquisitions while it has put some future developments on hold until the properties are fully pre-leased.

Moreover, in December, Brandywine issued $350 million of 5-year notes and announced that it will use the proceeds to redeem the bonds that would mature in February. In other words, the REIT managed to refinance its debt even under the adverse business conditions prevailing right now. As a result, the trust will not face another debt maturity until October 2024. This is undoubtedly a strong relief for the REIT, as inflation and interest rates are likely to revert towards normal levels over the next two years thanks to the aggressive stance of the Fed.

Apart from its effect on operating expenses and interest expense, inflation also has another effect on the stock of Brandywine. High inflation significantly reduces the present value of future cash flows and hence it tends to compress the valuation level of most stocks. In fact, the impact of inflation on the price-to-earnings ratio of stocks is a key factor behind the ongoing bear market of the S&P 500.

Indeed, inflation has greatly compressed the valuation of Brandywine. The stock is currently trading at a 10-year low price-to-FFO ratio of 4.5, which is much lower than the 10-year average price-to-FFO ratio of 10.9 of the stock. Brandywine was trading at a price-to-FFO ratio of 9.8 only in 2021. In other words, whenever inflation subsides, the stock may double merely thanks to the normalization of its valuation level.

Resilience

Brandywine enjoys resilient cash flows thanks to some key characteristics of its markets. The trust generates 74% of its operating income in Philadelphia, which offers several advantages to the REIT. 80% of all pharmaceutical and biotechnology companies have offices in Greater Philadelphia.

Brandywine business model (Investor Presentation)

Moreover, 87% of all the cell and gene therapy treatments approved by the FDA in 2020 originated in Philadelphia. Overall, Philadelphia is an exceptionally strong market for a REIT like Brandywine, given the strong demand for high-quality properties in this state.

Analysts seem to agree on the resilience of Brandywine to the ongoing downturn in its business caused by inflation. They expect the REIT to incur just a 9% decrease in its FFO per unit in 2023, mostly due to higher interest expense, and expect a 7% recovery in 2024. Overall, Brandywine is likely to achieve essentially flat FFO per unit in 2024.

Flat performance is usually not exciting for the unitholders but the stock is trading at only 4.6 times its expected FFO in 2024, an extremely cheap valuation level. If the REIT posts essentially flat FFO per unit in 2024 and inflation reverts towards normal levels, the stock will probably trade much higher than its current price.

Dividend

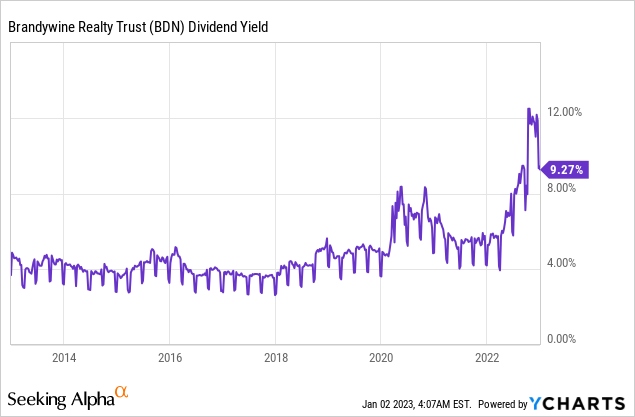

Due to its 55% plunge in the last 12 months, Brandywine is currently offering a 10-year high dividend yield of 12.4%.

When a stock offers such a high yield, it usually signals that the dividend is on the verge of being slashed. However, the dividend of Brandywine is an exception to the rule. The stock has a healthy FFO payout ratio of 56%, which provides a meaningful margin of safety for the dividend. As analysts expect nearly flat FFO per unit over the next two years, the payout ratio is likely to remain solid for the foreseeable future.

Moreover, Brandywine has repeatedly stated that the dividend is well covered by cash flows. Of course, there have been instances in which a dividend was cut despite management’s reassurance, but the sustained confidence of the REIT bodes well for the safety of its dividend. Even if the dividend is cut by 50%, the stock will still be offering an above-average yield of 6.2%. Overall, Brandywine is offering an attractive dividend, which makes it easier for the shareholders to wait for the recovery of the business from the highly inflationary environment prevailing right now.

Risks

Due to its material debt load, Brandywine will probably come under pressure in the adverse scenario of persistent inflation. If inflation remains abnormally high for years, it will exert pressure on the stock due to high interest expense and a suppressed price-to-FFO ratio. However, such a scenario is highly unlikely. The Fed has made it clear that it has prioritized restoring inflation to its normal range. As a result, inflation has begun to subside in recent months and is likely to decline further this year.

Final thoughts

Brandywine is trading at an extremely low price-to-FFO ratio and is offering a 10-year high dividend yield of 12.4% due to the impact of inflation on the stock. Those who are confident that inflation will revert towards its normal range in the upcoming years should purchase the stock at its current price. However, as the stock is highly volatile, only the investors who can tolerate stock price pressure for an extended period and remain focused on the long term should consider purchasing Brandywine.

Be the first to comment