ImagineGolf/iStock via Getty Images

Introduction

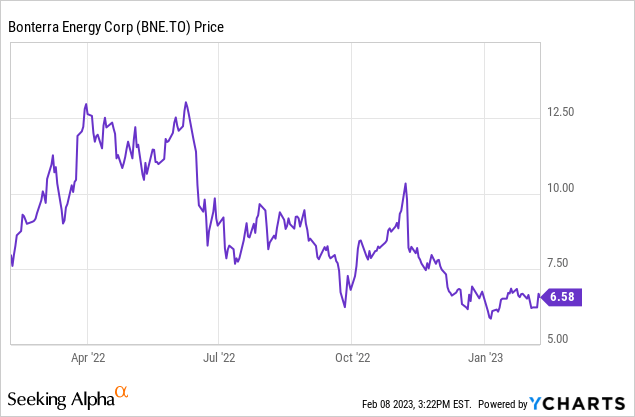

Bonterra Energy (OTCPK:BNEFF) (TSX:BNE:CA) initially reacted well to the higher oil price as the company started 2021 at a share price below C$3 to see it spike to almost C$14 per share June 2022. Since recording that multi-year high, the share price has lost about 50% again and I think the current share price level makes Bonterra pretty attractive if you believe in a future with US$70+ oil and C$3.5 natural gas.

The 2023 guidance looks interesting

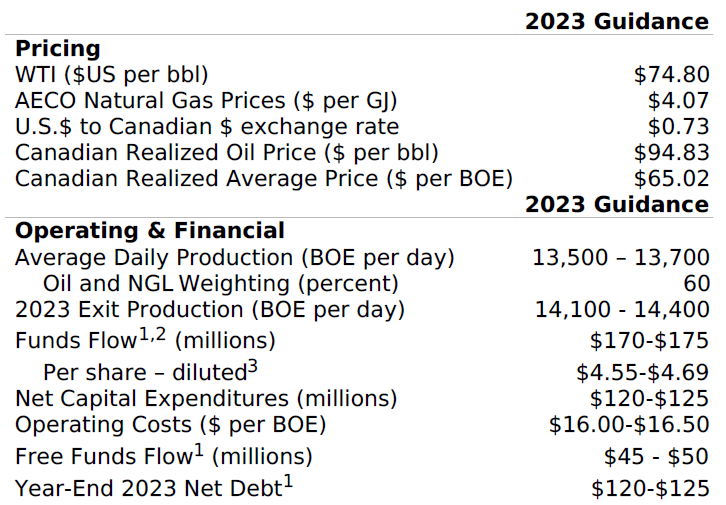

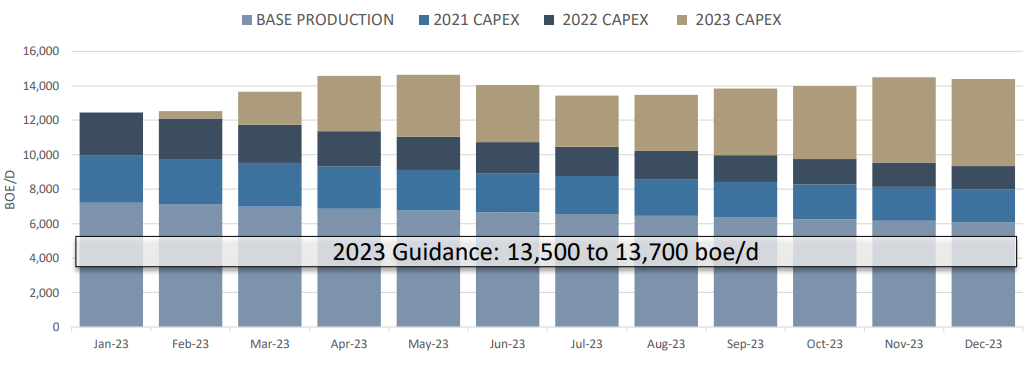

Bonterra plans to spend C$120-125M on capital expenditures in 2023, which should be sufficient to generate a total output of 13,500-13,700 barrels of oil-equivalent per day. The exit rate should be slightly higher at 14,100-14,400 barrels of oil-equivalent per day due to the timing of these investments.

The company obviously wants to focus on its free cash flow generation, and based on its own guidance, it expects to generate about C$170-175M in funds flow.

Bonterra Energy Investor Relations

That’s based on an average oil price of US$74.80 and a natural gas price of C$4.07 per GJ. The current natural gas price is trading below that level (at approximately C$3/GJ) but the oil price is trading a few dollars higher so based on the current oil and gas prices the base case scenario appears to be pretty realistic.

The sensitivity analysis also helps to figure out how the cash flow will change as the oil and gas prices change. For every (Canadian) dollar the oil price comes in higher, the funds flow will increase by C$2.15M. Meanwhile for every C$0.10 decrease in the natural gas price, Bonterra’s funds flow will be C$1.05M lower. So applying a C$1 decrease in natural gas price and a C$4 increase in the oil price on a per barrel basis would have a negative impact of just C$2M on the funds flow and the free funds flow.

Based on the aforementioned data, Bonterra anticipates to generate C$45-50M in free cash flow. Divided over the 36 million shares that are currently outstanding, the free cash flow per share will likely come in between C$1.25 and C$1.40 per share. As Bonterra is currently trading at approximately C$6.6 per share, the stock is trading at a free cash flow yield of approximately 20% based on the base case scenario.

Bonterra Energy Investor Relations

Bonterra should remain focused on its balance sheet

The free cash flow will be used to reduce the net debt toward C$120M by the end of this year. That’s the only right decision, especially in a climate of increasing interest rates and thus interest expenses. Right now, Bonterra is paying approximately C$15M per year on interest expenses. Given the production profile of roughly 5 million barrels of oil-equivalent per day, Bonterra needs to spend about C$3 per barrel of its operating margin on making the interest payments.

Bonterra also recently refinanced its credit facilities It entered into a C$110M first lien secured credit facility and a C$95M second lien secured term debt facility. The term facility is pretty expensive with a fixed interest rate of 11.70% on a portion of the loan with Canadian Prime + 625 basis points on a second tranche. The prime rate is currently 6.70% which means that second tranche of the C$95M term debt currently has an effective interest rate of almost 13%. This means that although the gross debt and net debt will decrease we likely won’t see a noticeable impact on the total interest expenses which will remain high and will likely even increase. As the Bank of Canada has indicated there may be no more rate hikes, we will likely start to see the quarterly interest payments decrease throughout the year, but the total interest expense in Q1 2023 will likely be pretty high.

Investment thesis

As of the end of 2021, Bonterra had about 97.4 million barrels of oil-equivalent in its 2P reserves. Based on an average production rate of 13,500 boe/day, this represents a reserve life index of just under 20 years. As of the time of writing this update, the YE2022 reserves hadn’t been published yet but I expect the company to have ended the year close to 100 million barrels of oil-equivalent for a 2P reserve life of approximately 20 years.

I’m also looking forward to seeing the new PV10 calculation and the oil and gas prices used by the consultants to have reached that value.

I recently initiated a small long position in Bonterra and may be looking to further expand this position throughout this year as the balance sheet gets derisked.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment