US Dollar, Singapore Dollar, Thai Baht, Indonesian Rupiah, Philippine Peso, Indian Rupee, ASEAN, Fundamental Analysis – Talking Points

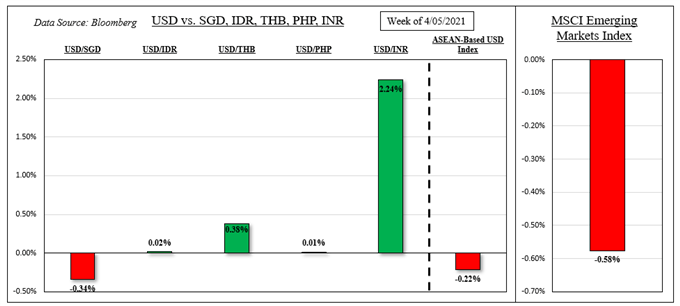

- US Dollar was mixed against SGD, THB, IDR and PHP this past week

- Weakness in Emerging Market stocks offset by falling Treasury yields

- Key event risk: Chinese GDP, US CPI, Fed Powell speaks, MAS policy

Discover what kind of forex trader you are

US Dollar ASEAN Weekly Recap

The haven-linked US Dollar netted little changed against its ASEAN counterparts this past week. The Singapore Dollar strengthened while the Thai Baht weakened. This is as the Indonesian Rupiah and Philippine Peso were relatively flat. This is despite a 0.6% decline in the MSCI Emerging Markets Index (EEM). ASEAN currencies can be quite sensitive to capital flows and risk aversion.

Weakness in the Thai Baht may have been due to rising global Covid cases. That is denting local tourism prospects, a key segment of Thailand’s economy. A notable standout in the developing Asia-Pacific region was the Indian Rupee. USD/INR gained the most in 6 weeks after a dovish Reserve Bank of India monetary policy announcement. The currency pair appears to have overturned the dominant downtrend since last March.

US Dollar, MSCI Emerging Markets Index– Last Week’s Performance

*ASEAN-Based US Dollar Index averages USD/SGD, USD/IDR, USD/THB and USD/PHP

External Event Risk – Chinese GDP, US CPI & Retail Sales, Fed Chair Jerome Powell Speaks

All things considered, it could have been a worse week for ASEAN and Emerging Market currencies. That is because dovish rhetoric from the Federal Reserve helped to cool hawkish monetary policy expectations. The outlook for a rate hike by the end of 2022 dramatically shifted lower. As such, falling Treasury yields and a weaker US Dollar offered some relief to Emerging Markets.

Rising rates in the world’s largest economy can make it harder for developing markets to pay off dollar-denominated debt, particularly as their currencies depreciate. The decline in EEM last week may have also been largely due to concerns about the outlook for risk-taking in China. A stronger-than-expected PPI report bolstered inflation woes in the world’s second-largest economy, hinting at PBOC dovish unwinding efforts.

It should be noted that China is a key trading partner for most ASEAN countries, so if the PBOC wants to slow inflation to prevent the economy from overheating, that risks reverberating outwards. As such, all eyes are on Chinese GDP ahead. The economy is expected to expand 18.3% y/y in the first quarter. Much like with the PPI report, a stronger reading could further raise inflation woes, denting EEM.

But, the broader focus will likely remain on the US. The world’s largest economy will release the next CPI and retail sales report ahead. Similar to China, beats here may rekindle longer-term Treasury yields. That would be a prominent downside risk for ASEAN currencies. But, Fed Chair Jerome Powell could reiterate fairly dovish rhetoric during his moderated Q&A at the Economic Club of Washington on Wednesday.

Recommended by Daniel Dubrovsky

How can you overcome common pitfalls in FX trading?

ASEAN, South Asia Event Risk – Monetary Authority of Singapore, Indian CPI & Industrial Output

Focusing on the ASEAN economic docket, USD/SGD is eyeing the Monetary Authority of Singapore’s (MAS) semiannual policy announcement on the 14th. The MAS is widely anticipated to leave its FX policy band, midpoint and width unchanged. So the focus for the Singapore Dollar may be oriented outwards. But, due to the city-state’s reliance on trade, the central bank’s outlook will likely be a reflection of global growth prospects. Singapore’s benchmark stock index, the Straits Times (STI), has been on a tear as of late amid an improving outlook for world GDP, recently underscored by the IMF. So a rosy outlook from the MAS could propel the STI higher. Meanwhile, USD/INR will be eyeing local CPI and industrial output data on Monday.

Check out the DailyFX Economic Calendar for ASEAN and global data updates!

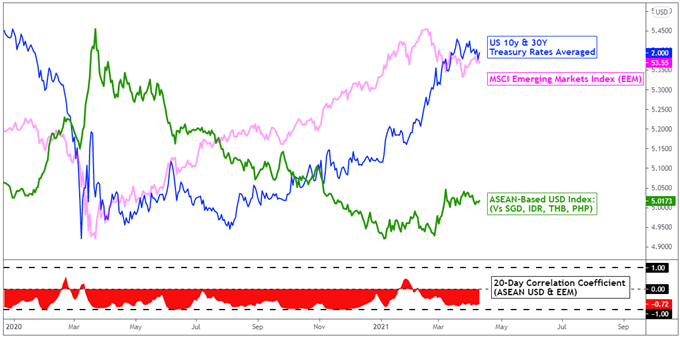

On April 10th, the 20-day rolling correlation coefficient between my ASEAN-based US Dollar index and the MSCI Emerging Markets index changed to -0.72 from -0.75 one week ago. Values closer to –1 indicate an increasingly inverse relationship, though it is important to recognize that correlation does not imply causation.

ASEAN-Based USD Index Versus EEM and Treasury Yields – Daily Chart

Chart Created Using TradingView

*ASEAN-Based US Dollar Index averages USD/SGD, USD/IDR, USD/THB and USD/PHP

— Written by Daniel Dubrovsky, Strategist for DailyFX.com

To contact Daniel, use the comments section below or @ddubrovskyFX on Twitter

Be the first to comment