Editor’s note: Seeking Alpha is proud to welcome Ryan D’Angelo Raymond as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Ingus Kruklitis/iStock Editorial via Getty Images

Why Upside Remains Intact

The market remains unfazed about BMW’s (OTCPK:BMWYY) prospects due to a broader automotive sell-off and a drop in deliveries in 2022. However, BMW continues to be a quality business with strong economic moats and is well-positioned to benefit from demand in China as well as continued demand for Internal Combustion Engine (ICE) automobiles. Furthermore, I believe BMW’s ownership of the Rolls-Royce automobile line is underappreciated by the market.

Company Overview

BMW is a German premium automaker known for its premium automobile brands such as BMW and Mini as well as ultra-luxury Rolls-Royce. Headquartered in Munich, Germany, BMW was founded in 1916, initially a builder of aircraft engines, eventually entering the automobile business in 1928.

Revenue Segments

BMW’s sales span across geographies – key regions being China (23%), Europe (40%) and USA (19%) – with most of its revenue coming from the sale of automobiles.

BMW Group Annual Reports

Automotive

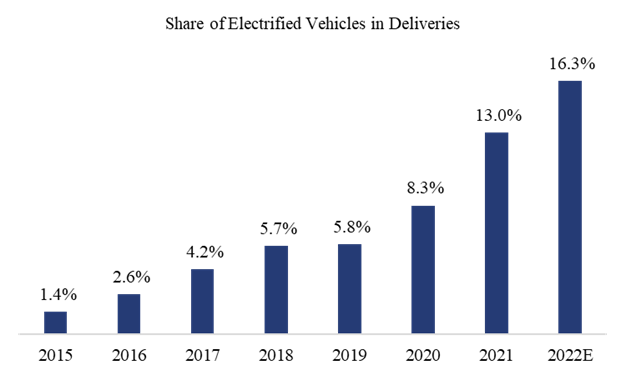

The largest revenue segment, BMW sells its automobiles mostly through dealerships across the world. Deliveries have proven strong in 2021 but have since taken a hit due to supply bottlenecks for vehicle components such as semiconductors, a tough macroeconomic environment, and pandemic-related restrictions in key market China. Management has since guided for a slight decrease in automobile deliveries in FY22.

BMW Group Annual Reports

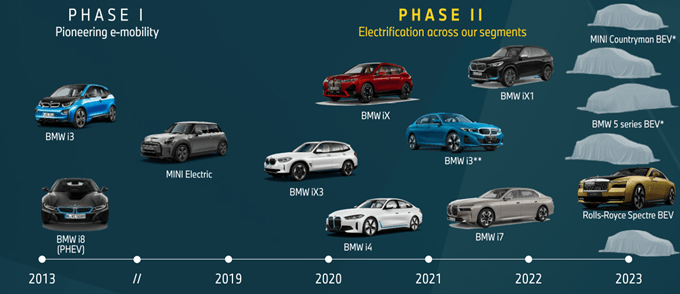

BMW’s Electrification Strategy Is Key

BMW Group Investor Presentation

BMW was one of the early players in the EV space, beginning in 2013 with the BMW i3. However, this fell short of expectations as sales were poor at the time due to the lack of charging infrastructure and hence adoption. BMW has since embarked on a more structured, slow-and-steady approach to electrification. With 3 phases, BMW is currently nearing the end of Phase 2 given that they have Battery Electric Vehicles (BEVs) offered in at least 90% of the markets they operate in.

While other companies have pivoted aggressively towards EVs, BMW CEO Oliver Zipse has chosen to continue building their ICE platforms alongside EVs. At the Q3 FY21 earnings call, he stated:

We still don’t think that the world is separating immediately or very quickly into two completely different phases, the combustion world and the EV world. It’s about an architecture’s competence overall and is not only about EV.

The clearest distinction can be seen in BMW’s target of 25% electrified (BEVs + Plug-In Hybrid Vehicles) by 2025 and 50% or more by 2030 compared with Mercedes-Benz’s (OTCPK:MBGAF) commitment to being 50% electrified in 2025 and up to 100% by 2030.

From 2025 onwards, BMW will launch Phase 3, which it terms Neue Klasse. This will be based on a new vehicle architecture (BEV only) and will be a sixth-generation electric drivetrain to ensure their EVs are on par with vehicles that have “state-of-the-art internal combustion engines”.

BMW Group Annual Reports

Why BMW Is A Quality Business

Economic Moat 1: Technological Strength

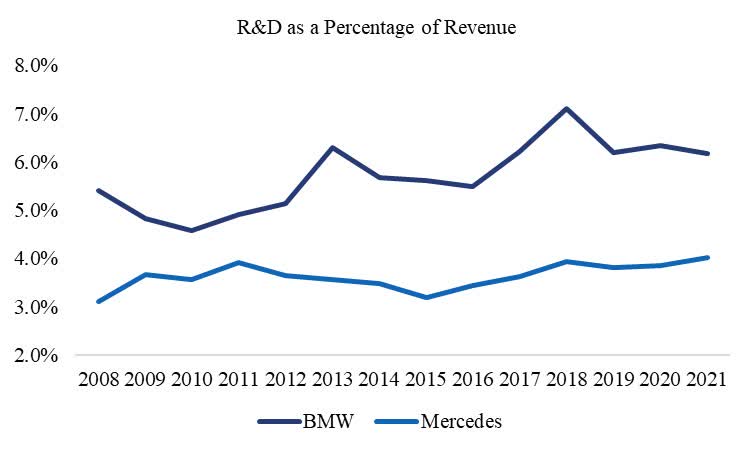

BMW has developed and retained intellectual property with regard to its automotive technologies over the course of its history. BMW boasts R&D locations in 13 countries, close to production plants, in line with their local-for-local strategy.

From the Q1 FY22 earnings call, CEO Oliver Zipse elaborates on BMW’s battery technology:

On the uppermost level, you have the energy module where the different battery cells come together and then goes to the car. That’s fully in-house at BMW, whether that is in Europe or the United States or in China. The battery cell itself, we do everything in-house, R&D, knowledge transfer, production planning, besides the actual manufacturing.

Its technological prowess can be seen from how the BMW i8 hybrid powertrain has been one of the chosen powertrains for International Engine of the Year for 5 of the last competitions, despite the engine first being introduced in 2014. R&D is at BMW’s core – a comparison with closest competitor Mercedes-Benz shows BMW spends more on R&D as a percentage of revenue.

BMW Group Annual Reports, Mercedes-Benz Group Annual Reports

Economic Moat 2: Robust Supplier and Production Networks

BMW’s strength also lies in its local-for-local approach in sourcing and production, which ensures low-cost sourcing, economies of scale and customised production for its markets. BMW has 31 production and assembly plants in 15 countries, allowing BMW to achieve a strong sales footprint in Europe yet a strong presence in Asia, particularly in China, where >80% of deliveries are produced in China.

Using China as an example, BMW has been in China since 2003 and continues to expand its production capabilities there. BMW has had the BMW Brilliance Automotive JV (BBA) in China since 2003, which manufactures BMW brand models, engines and batteries. In early 2022, BMW increased its stake in this JV from 50% to 75%. This will help produce more BEV models in China, now especially the China-only BEV variant of the BMW Series 3 long wheelbase sedan and the long wheelbase X5 Li, specifically tailored for Chinese market tastes.

A Tegus transcript from an expert call with a former Senior Project Manager at Mercedes-Benz reveals the long-term partnership approach that BMW has cultivated which has borne fruit.

BMW, on the other hand, as far as I know, have very long term-oriented contracts, and they secured millions of semiconductor parts and have less problems in this area…They have a very good and positive way of treating other companies, partners and also vendors and suppliers. So this is a huge market advantage at the moment because they are not short with chips.

Economic Moat 3: Strong Brand Portfolio

BMW has curated its premium range of automobiles. They have stuck with their formulaic approach of model identifiers for decades (eg. 3-series, 5-series, X-series, performance-oriented “M”, electric variants “i”) which are familiar to consumers. In terms of reliability and quality, BMW was ranked one of the top 3 most reliable brands by Consumer Reports in 2022, while Mercedes-Benz came last (24th) for the first time.

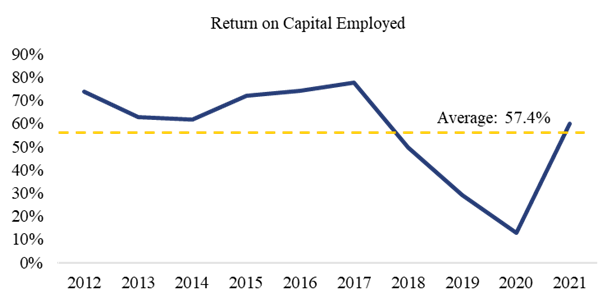

Automotive Return on Capital Employed

BMW Group Annual Reports

These reasons have allowed BMW to achieve a high RoCE for the past decade, with an average of 57.4%, showing that management has been allocating capital well.

Investment Thesis

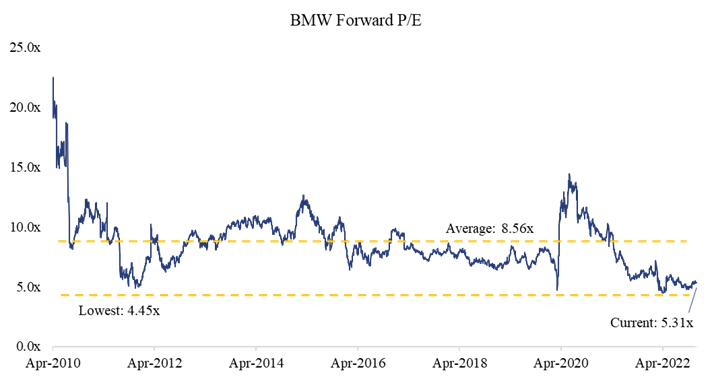

The automotive sector has been sold off in 2022 due to its discretionary nature amidst recession fears and tight consumer budgets. BMW now trades at a Next Twelve Months (NTM) P/E multiple close to the lowest in the past 10 years (4.45x in Apr 2022), with its average being 8.56x in the available data from Capital IQ. I believe this presents a favourable buy opportunity given the theses below.

S&P Capital IQ

Thesis 1: Underestimation of Growth Potential in China

Rising Consuming Class

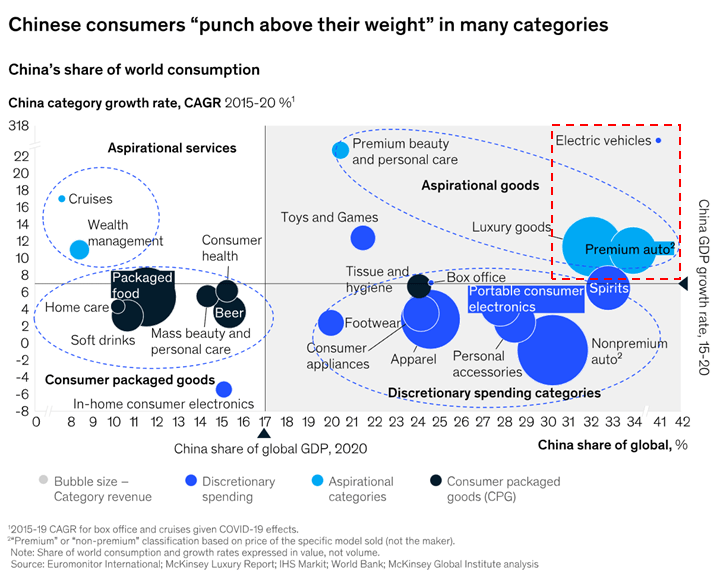

China has become a crucial market for premium automobiles and EVs due to the sheer growth of its middle class.

McKinsey Report on Consumer Trends Shaping Next Decade of Growth in China

From the chart above, premium automobiles have grown at a strong revenue CAGR of ~10% in 2015-2020, with the category size being relatively huge. For EVs, this has grown at a CAGR of >20% in the same period, at a rate >7x faster than the global rate.

McKinsey Report on Consumer Trends Shaping Next Decade of Growth in China

Looking at the Affluent and Mass Affluent income categories, BMW’s target consumers, their share of urban households is expected to grow to ~2x and ~9x their 2020 share respectively by 2030.

These figures show that BMW’s target segment will has significant growth runway and will continue to grow fast.

Additionally, auto finance penetration in China stands at 40%, compared to 70% in USA, providing ample room for growth.

Why BMW Can Capitalise on This Growth

The market remains concerned about the increasing competition from Chinese automakers which threatens BMW’s competitive position.

But I believe BMW’s position in China will continue to remain strong. BMW does not compete with mass-market competitors, since their models are priced relatively high. So it competes with local brands, Tesla (TSLA), Mercedes-Benz and Audi (OTC:AUDVF). BMW is still the only European premium automaker in the top 3 market leaders in China.

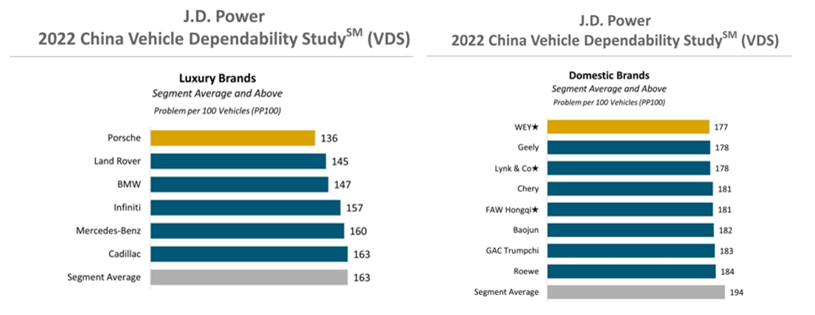

I believe this stems from a technological advantage and brand equity that BMW possesses. A study by J.D. Power shows the quality advantage that BMW has over the Chinese brands, with lower Problem per 100 Vehicles by a decent margin.

J.D. Power 2022 China Vehicle Dependability Study Strategy& Digital Auto Report 2021

A Strategy & report highlights the emphasis Chinese consumers have on safety, higher than those in Germany and USA.

I believe this is what underpins BMW’s leading position in deliveries in China compared to other European counterparts.

BMW Group, Mercedes-Benz Group, Volkswagen Group Annual Reports

Thesis 2: Overlooked Market Demand for ICE Segment

The market has focused very heavily on EV transitions which I believe to be myopic given that serving ICE demand during the transition is still crucial.

Cautious Approach to ICE Phase-Out

BMW’s electrification strategy stands in stark contrast to its competitors, with slower phasing out of ICE automobiles to be able to continuously capture market demand for both ICE and electrified automobiles. While competitors like Mercedes-Benz have hopped on the bandwagon and pursued a more aggressive electrification strategy – which will be virtually irreversible since it requires a large upfront investment, BMW has taken a cautious approach, instead developing mixed platforms that can develop both ICE and electrified automobiles. At the same time, BMW is ensuring their production plants can easily pivot from one to the other.

| Features of Mixed Platform Approach | Commentary |

| Flexibility to respond to ICE / PHEV / BEV demand | Building out a platform that is highly flexible (eg. New 7-series comes as i7, but PHEV and ICE also available) allows BMW to respond to market demand well. Although the focus may be high demand for i7, the flexibility to respond to PHEV and ICE demand will allow BMW to capture market sales in these other automobile types. This also saves BMW from being stuck on a dedicated platform when there are design breakthroughs. |

| Production and supply chain flexibility | This also allows BMW to recalibrate their production plants towards being able to produce ICE and electrified automobiles for swift response to market demand. |

| Geographic responsiveness | With the EU 2035 ICE Phase-Out, the UK 2030 ICE Ban etc., BMW can respond in these respective markets as they already produce BEVs in 90% of their markets. |

| Economies of scale | Spreading the upfront development cost across a larger volume of automobiles reduces unit costs. |

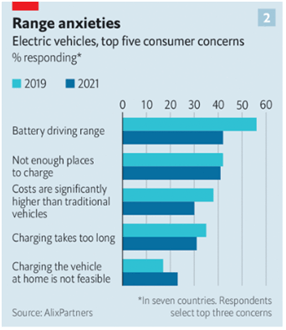

Why This Strategy Is Superior – The Future Is Not EVs Yet

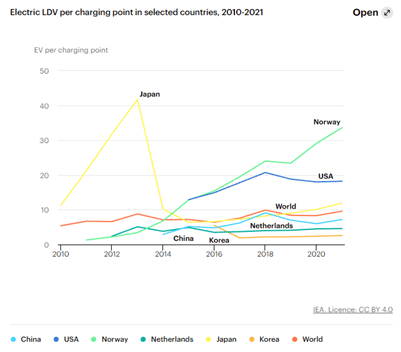

The answer is simple – range anxiety and charging infrastructure continue to hold back EV adoption.

The Economist – “A Lack of Chargers Could Stall The Electric-Vehicle Revolution”

The EV per charging point ratio has remained relatively flat for China in the past decade, suggesting that charging infrastructure deployment has matched EV stock growth, while in USA, EV stock growth has exceeded charging infrastructure deployment.

International Energy Agency International Energy Agency

To put this into perspective, the EU 2014 Alternative Fuel Infrastructure Directive that regulates the deployment of public EV infrastructure recommended that EU member states reach 10 EV per charger. The figures are far from this: Europe (15), USA (18), UK (21).

Strategy& Digital Auto Report 2021

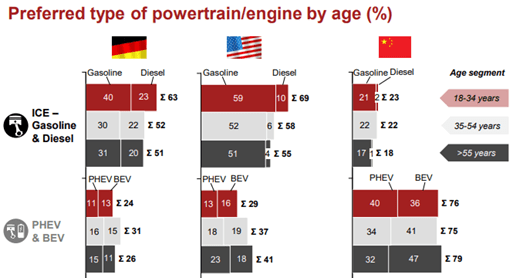

It is hence not surprising that consumers across age segments in key BMW markets still prefer ICE automobiles. As its competitors accelerate their transition towards electrification, I believe BMW’s cautious approach will allow it to capitalise on overlooked market demand for ICE.

Thesis 3: Underappreciation of Rolls-Royce

Gem In A Great Business

With 7% revenue contribution and 0.3% of deliveries share, ultra-luxury brand Rolls-Royce is BMW’s hidden gem.

BMW Group Annual Reports

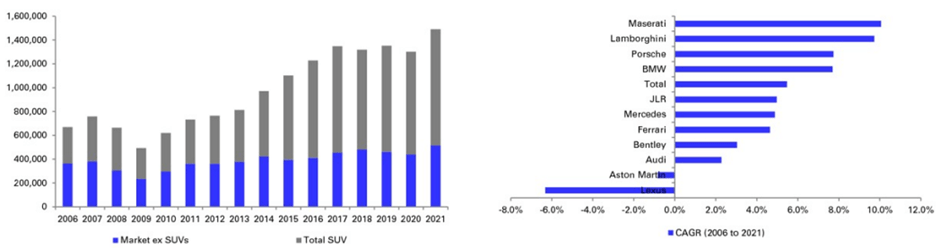

Rolls-Royce has steadily grown in deliveries since 2010, with outstanding results in 2021 (49% growth YoY) and the SUV Cullinan becoming its most important model. SUVs are a fast-growing market segment with most automakers experiencing growth in the last 15 years. Rolls-Royce has successfully leapfrogged this trend and revived its Ghost model.

Deutsche Bank Equity Research Reports

In terms of electrification, Rolls-Royce is at the forefront – aiming for 100% BEVs by 2030 (similar to Bentley) compared to Ferrari’s 40% BEV, 60% EV target.

I believe the Rolls-Royce line is an attractive business within BMW because it has strong brand value (we can’t build an ultra-luxury brand in a month, a year or even several years), robust deliveries performance and pricing power. Moreover, there is exposure to the high-growth SUV market and protection from a recessionary environment due to low income elasticity.

Supercars.net, Ferrari and Volkswagen Group Annual Reports

Compared to ultra-luxury brands like Ferrari and comparable Bentley, Rolls-Royce is growing the fastest (2x their CAGRs), is the most expensive (hence greater status symbol) and produces significantly fewer models (hence more exclusivity).

Where The Value Lies

S&P Capital IQ

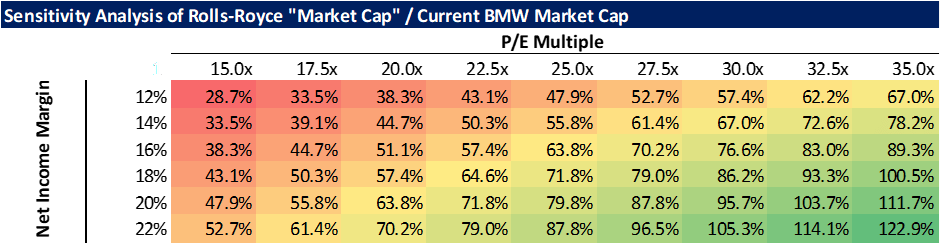

Using the P/E multiples of luxury comparables, a quick analysis below reveals a Rolls-Royce “Market Cap” that makes up 97% of BMW’s current market cap. Even a 20% haircut to the Rolls-Royce “Market Cap” still implies that it takes up 78% of BMW’s market cap.

S&P Capital IQ, Deutsche Bank Equity Research Reports

BMW has one of the highest cash/market cap ratios amongst automakers, such that stripping out cash from its market cap suggests that Rolls-Royce takes up the entire value of BMW (and even more). We get to purchase the BMW Automobile (Ex. Rolls-Royce), Motorcycles and Financial Services businesses for free.

I believe this is an incredible undervaluation of BMW as its competitors simply do not own an ultra-luxury brand like Rolls-Royce.

A sensitivity analysis further underscores Rolls-Royce hidden value.

DCF Estimates

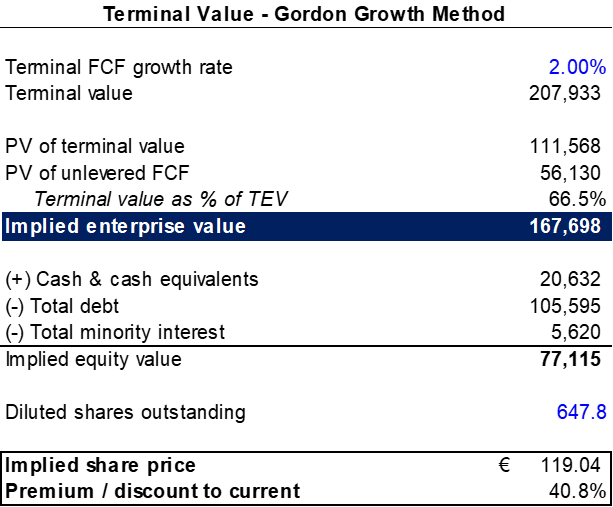

Valuation

Using a WACC of 6.7% and the Gordon Growth method for calculation of terminal value, I arrive at a target price of €119.04, with an upside of 40.8%.

DCF Estimates

DCF Estimates

Below are my key assumptions.

DCF Estimates

Catalysts

The first catalyst would be a strong sales recovery in China in Q4 FY22 and beyond driven by growth in deliveries, particularly EVs. Such strong performance in China will give the market confidence that BMW’s position in China is still robust despite tough competition from domestic players.

The second catalyst would be a rebound in the ICE automobiles’ sales and a subsequent rise in market share. This would lead to the market’s realisation that BMW’s approach of building flexible architecture for its automobiles is superior for the transition towards EVs.

The third catalyst would be robust Rolls-Royce sales in a recessionary environment, which I believe will further cement its brand image as an ultra-luxury brand, but now with EVs.

Risks

There are several investment risks that I have identified that I believe to be sufficiently mitigated.

Decline in China Sales

China sales are largely driven by EVs, so a decline could stem from consumer shifts towards domestic players. This would be possible if domestic players improve their dependability, but consumer perception should still take time to change. I have also taken a more conservative approach to modelling BMW’s revenue growth, growing at about 3% CAGR for a business that has grown at about 5% CAGR for the past 14 years.

Quicker ICE Phase-Out

The timelines of national ICE phase-outs have largely been set and will take time to achieve, such as the EU 2035 ICE Phase-Out and UK 2030 ICE Ban. BMW’s flexible architecture approach will also allow it to pivot to EVs when required, and its high R&D spending shows no signs of BMW falling back in terms of its EV rollout.

Shift of Consumer Taste to EVs instead of ICE Automobiles

Even if this happens, there will still be markets that have a slower transition away from ICE automobiles in the next 5 years. The previous points about BMW’s flexible architecture approach and EV rollout also apply here.

Decline in Rolls-Royce’s Brand Value

I believe this is unlikely given the strength of Rolls-Royce’s brand which has been built over decades. Management has also taken the right steps in limiting production and maintaining Rolls-Royce’s selling price to upkeep the brand’s ultra-luxury image.

Prolonged Depressed Margins

This could be due to continued shortages of vehicle components, high raw material costs and mix shift towards EVs. I believe management’s excellent management of the semiconductor shortage provides comfort that they can navigate future problems. Furthermore, I modelled a gradual EBIT recovery to 10.6% only in 2026, when the full effects of technological improvements can offset the negative effect of mix shift towards EVs, and when short-term headwinds are likely to be abated.

Conclusion

BMW is trading at an attractive price today, presenting an opportunity to invest in a company with strong economic moats in an industry that is undergoing transformation. BMW is in a pivotal position to leverage demand in China along with demand for ICE automobiles. Furthermore, BMW’s ownership of Rolls-Royce provides substantial value that I believe the market has not fully appreciated.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment