CHUNYIP WONG

On Tuesday, Blackstone (NYSE:BX) announced a massive $4 billion investment from the University of California Investments (UC) into its non-traded REIT (BREIT). This follows December’s news that Blackstone would limit redemptions due to outsized requests from investors to sell BREIT shares.

To secure the investment from UC, Blackstone provided $1 billion of return support (discussed below) which essentially amounts to a preferential guarantee. In my view, the giant $4 billion allocation from UC coupled with Blackstone’s willingness to provide a guarantee illustrates confidence in the outlook for US residential/multifamily and industrial real estate (which represent the bulk of BREIT assets).

While ordinary investors are unable to invest in BREIT on the same preferential terms as UC, the public market offers what I believe to be a fantastic opportunity to buy similar assets at a large discount to net asset value. As I show below, I believe that the purchase of leading residential/multifamily REITs at current prices will produce low to mid-teens annualized returns to public market investors.

The UC Investment

UC Investment in Blackstone’s BREIT (BREIT / Blackstone )

As shown above, this is a two-part transaction:

- UC acquires $4 billion worth of BREIT shares at its January NAV on the same fee terms as other investors (1.25% management fee with 12.5% incentive fee payable on returns over 5% hurdle). Further, UC has committed to a six-year lock-up (does not have access to redeem monthly like ordinary shareholders).

- In exchange for the giant investment and six-year lock-up, Blackstone pledges $1 billion worth of its own shares in BREIT to provide return support to UC. Essentially this is a limited guarantee of an 11.25% annualized return.

UC’s $4 billion investment and Blackstone providing $1 billion of its own BREIT shares as a limited guarantee has drawn mixed reviews from pundits. On the one hand, this is a gigantic, locked-up commitment from a sophisticated investor. On the other hand, to secure this investment, Blackstone has put $1 billion of its own capital at risk.

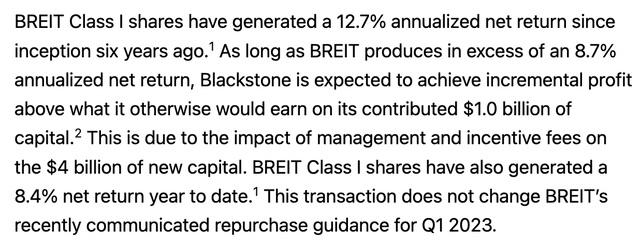

Only time will tell if this transaction is ultimately beneficial to Blackstone shareholders. That said I see this deal as being a bullish sign for the residential/multifamily and industrial real estate sectors. By putting up $1 billion of its own capital to secure UC’s investment/preferred return, Blackstone has clearly said that it expects strong returns from BREIT going forward. As shown below, in the press release announcing the transaction, Blackstone notes that the deal will be financially accretive to Blackstone only if BREIT produces a minimum +8.7% annualized return going forward:

Required return for Accretion to BX (Press Release)

Why is this Bullish for REIT investors?

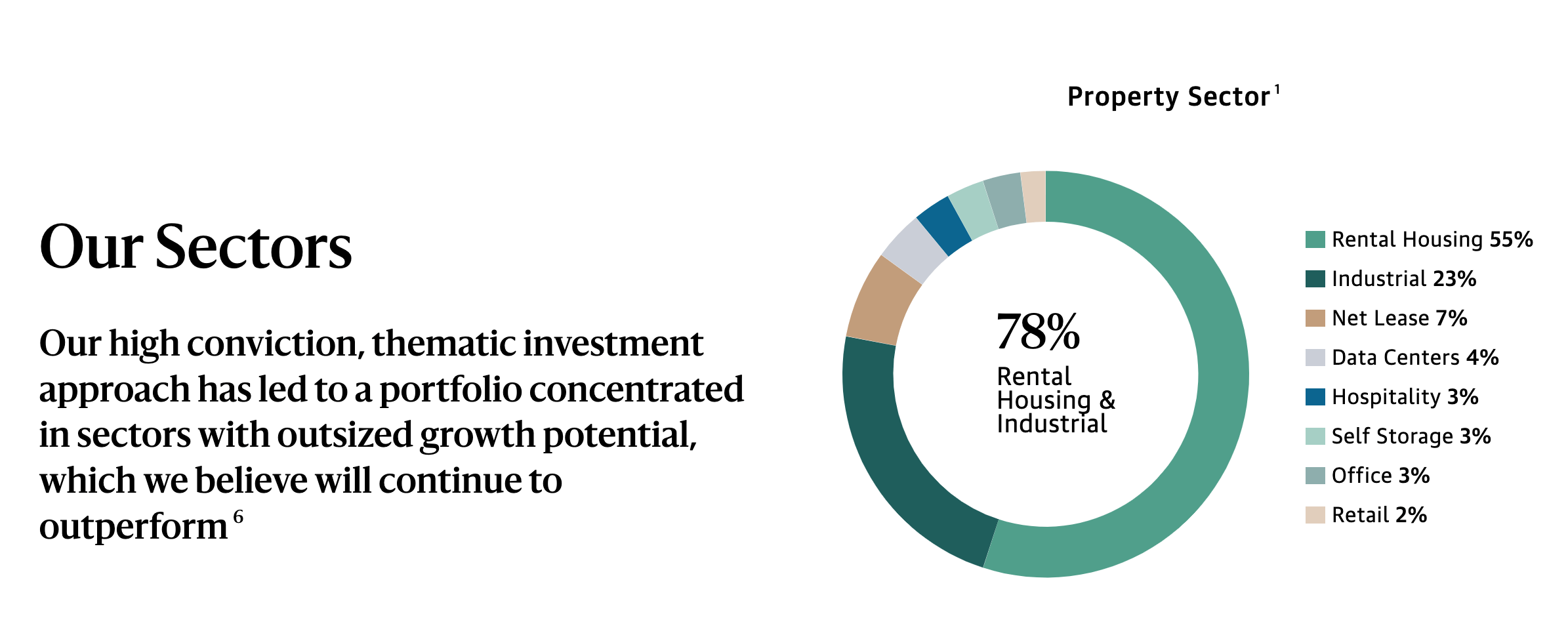

Beyond the obvious size of UC’s investment, which is a clear vote of confidence in the long-term health of the US multifamily and industrial real estate markets, UC being willing to invest at BREIT’s January NAV provides some affirmation of BREIT’s valuation. Similarly, Blackstone using $1 billion to effectively underwrite a limited guarantee signals its confidence in BREIT’s NAV estimate. As shown below, rental housing (mainly apartments) represents the largest component of BREIT’s asset base.

BREIT Assets by Type (BREIT.com)

Below, I show some of the assumptions used by Blackstone to determine BREIT’s NAV estimate:

BREIT NAV Assumptions (BREIT Prospectus)

As shown above, BREIT assumes an exit cap rate of 5.4% for its ‘Rental Housing’ (mainly single-family and multifamily) assets in determining NAV. In the verbiage below the table, Blackstone ‘assumes high single digit net operating income (NOI) growth in the near term’. The assumption of outsized near-term NOI growth suggests that the current implied cap rate of these assets is lower (5% would be my best ‘guesstimate’) than the 5.4% exit cap rate.

On its 2Q22 conference call, Blackstone President/COO Jon Gray noted the attractiveness of public market valuations. Since this time, public market apartment REIT valuations have only become more attractive as share prices have declined.

Jon Gray commentary on public valuations (BX 2Q22 Earnings Transcript from Seeking Alpha)

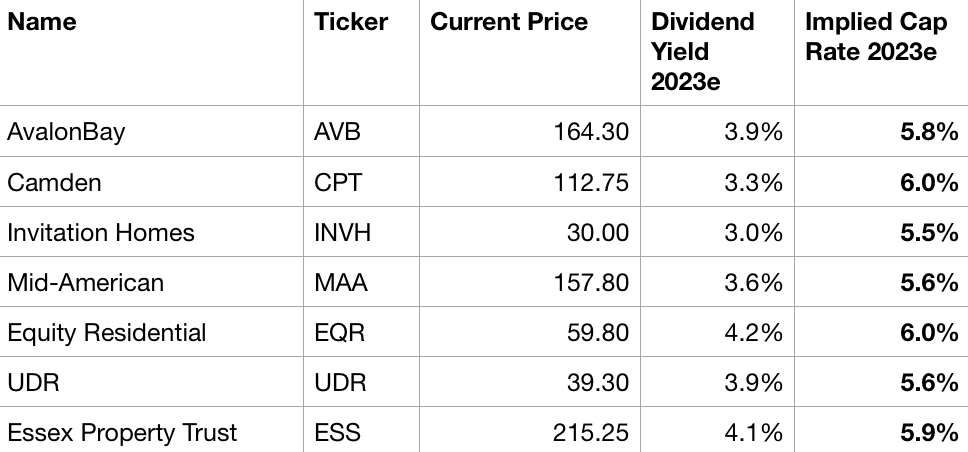

As shown in the table below, the large apartment and single-family rental REITs offer investors the opportunity to invest at lower valuations (higher implied current cap rates):

Rental Housing REIT Implied Cap Rates & Dividend Yields (Company Filings; Author Estimates)

While ordinary investors are not able to invest in BREIT on the same terms as UC, I believe the multifamily REITs offer a superior investment proposition. Rental housing REITs trade at a lower valuation than what is imputed into BREIT’s NAV but they also offer guaranteed daily liquidity (no risk of redemption halt). All of the REITs above have very strong balance sheets with loan to value, or LTV, below 30% (versus ~40% for BREIT) with the benefit of long-term fixed rate financing at favorable borrowing rates.

The combination of a higher initial cap rate, receipt of annual dividends, and eventual convergence to NAV point to low to mid teens annualized returns for investors in the rental housing REITs over the next 4-5 years. See my recent writeup on Equity Residential (EQR) or Camden Property Trust (CPT) for additional color on valuation metrics. Similarly I recently wrote a piece on Rexford Industrial Realty (REXR) which I believe offers low teens returns over a 4-5 year holding period.

Conclusion

I see UC’s large investment into BREIT as a vote of confidence for the rental and industrial housing sectors. While ordinary investors can’t invest in BREIT on the same terms as UC, I believe the opportunity in rental housing REITs at today’s prices will provide even better returns to long-term, conservative investors.

Be the first to comment