zorazhuang

Both Enbridge (NYSE:ENB) and TC Energy Corporation (NYSE:TRP) are high-yield investment grade midstream businesses.

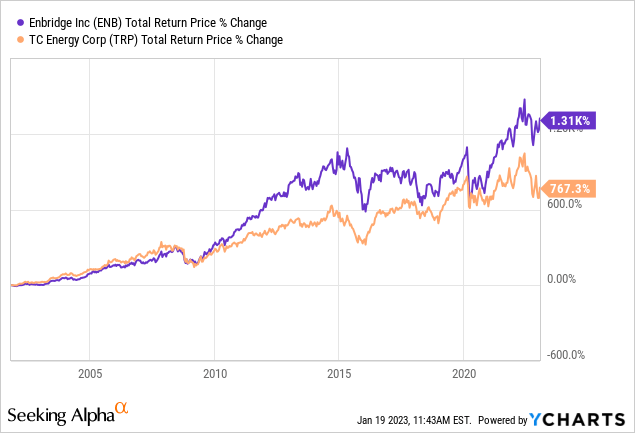

ENB has a vastly superior long-term total return track record:

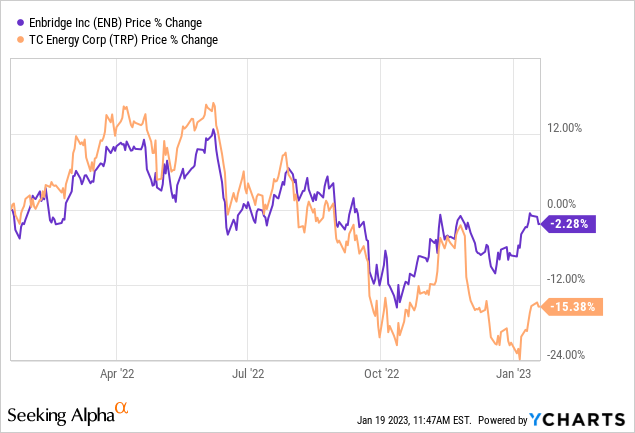

but TRP is down further over the past year, indicating that there could possibly be superior value there:

In this article, we will compare them side by side and offer our take on which one is a better buy right now.

Enbridge Vs. TC Energy: Business Model

TRP’s business model is quite strong, earning it a narrow moat rating from Morningstar. In fact, Morningstar uses rather glowing terms to describe TRP’s asset portfolio:

The combination of top-tier asset and contract quality, regulatory protection on existing pipelines, attractive near- and long-term pipeline projects, and a vast, diverse pipeline network allows TC Energy to generate durable excess returns on invested capital…TC Energy’s assets are some of the highest-quality assets we cover.

Let’s take a closer look: roughly three quarters of TRP’s EBITDA stems from its natural gas pipeline business that spans three countries (the U.S., Canada, and Mexico). The remaining quarter of its EBITDA comes from its liquids pipelines and power and storage assets.

Perhaps its most important assets are its Keystone crude pipeline (the industry’s second-largest crude pipe that delivers crude to the vital Gulf Coast and Midwest markets of the United States) as well as its NGTL and Mainline natural gas pipelines (which transport 75% of the natural gas takeaway capacity from Western Canada). In other words, without TRP’s infrastructure, Canada’s energy export infrastructure would face massive capacity shortfalls and its economy would be significantly damaged.

With its presence across three countries, 35 U.S. states, 12 Mexican states, and seven Canadian provinces, TRP boasts a wide footprint that makes it an extremely important midstream infrastructure player. It owns one of the largest natural gas networks that span North America and connects the lowest cost basins to the largest demand markets.

In addition to its competitively positioned asset portfolio, TRP has a very stable cash flow profile. Its crown jewel NGTL and Mainline pipeline networks are fully contracted at the moment with defensive take-or-pay contracts with 10-year average terms to expiration on them. Meanwhile, its Mexican projects have 25-year take-or-pay contracts backed by Mexican state-owned agencies, making them quite conservative undertakings. The Keystone pipeline is fully contracted as well with a 20-year contract, and its Bruce Power business has 30+ year contracts with the Canadian province of Ontario, once again giving it a very stable cash flow outlook.

ENB’s portfolio of assets is also quite large and well-diversified, providing it with economies of scale, insulation from individual asset, commodity, or geographic concentration risk, numerous growth investment opportunities, and a mission critical role in the North American energy value chain.

Its assets give ENB ownership of the United States’ second-longest natural gas transmission pipeline network and North America’s largest natural gas distribution business and longest crude oil pipeline network. On top of that, ENB is further ahead of TRP in accommodating environmental mandates from the Canadian government by growing a renewable power business alongside its midstream assets.

ENB’s cash flow profile is exceptionally stable with 98% of its cash flow being linked to commodity price-proof contracts and 95% of its cash flow being backed by investment grade counterparties.

Enbridge Vs. TC Energy: Balance Sheet

Both TRP and ENB enjoy sector-leading BBB+ credit rating from S&P, indicating that they possess significant financial strength.

TRP is currently focused on deleveraging its balance sheet with a goal of achieving a below 4.75x leverage level by 2026. It is employing non-core asset sales to accelerate its efforts to reach this target. In the meantime, its financial flexibility is quite strong thanks to an average term to maturity of 20 years and 85% of its long-term debt at fixed interest rates.

ENB meanwhile also enjoys plenty of liquidity. Furthermore, the vast majority of its debt is at fixed interest rates (90%) and does not mature until the 2030s, 2040s, 2050s, 2060s, and even 2080s, giving it many years of very low-cost debt with which to compound shareholder returns.

Overall, we give ENB the slight edge here given that it is currently at the low end of its target leverage range, whereas TRP is at the high end of its target leverage range. This gives ENB significantly more financial flexibility to pursue accretive acquisitions, growth projects, and/or share buybacks under its current $1.5 billion share repurchase program.

Enbridge Vs. TC Energy: Dividend Outlook

Both businesses have very impressive dividend growth track records. ENB has grown its dividend for 27 consecutive years whereas TRP has 22 consecutive years of dividend per share growth. Both are expected to grow their distributions/dividends at a mid-single digit annualized rate in the years to come.

Given their strong balance sheets and stable cash flow profiles, there is little to no concern about the safety of either dividend and per share dividend growth should continue for the foreseeable future.

Enbridge Vs. TC Energy: Catalysts And Risks

Both businesses are exceptionally well diversified and have very low risk profiles when it comes to navigating future headwinds to the energy industry. As a result, we do not anticipate any near to medium term severe risks facing either business.

That said, long-term if the energy industry experiences strong growth, it will undoubtedly lead to stronger contract fees for both businesses as well as an increase in attractive organic growth opportunities. Both also are positioned to potentially increase growth through accretive acquisitions.

On the other hand, if the energy transition takes place faster than anticipated (which we are skeptical of), then both businesses could suffer from lower contract fees and even increased excess capacity in their networks while suffering from a lack of growth opportunities to invest in.

Enbridge Vs. TC Energy: Valuation

Based on the data below, we see that TRP is cheaper relative to ENB on both a comparative and historical basis:

| Metric | ENB | TRP |

| EV/EBITDA | 12.70x | 11.44x |

| EV/EBITDA (5-Yr Avg) | 12.57x | 11.97x |

| P/2023E DCF | 10.07x | 9.19x |

| Dividend Yield | 6.4% | 6.3% |

That said, ENB does offer a slightly higher dividend yield at the moment.

Investor Takeaway

Both of these businesses enjoy low risk profiles and have very impressive asset portfolios. Both also offer investors an attractive income yield that should be safe for the foreseeable future.

That said, ENB appears to be in a slightly stronger financial position, while TRP’s valuation is cheaper. We view their asset portfolios as being roughly equal and very strong with stable cash flow profiles.

ENB has the stronger track record in terms of:

- longer dividend growth streak

- significantly greater total returns generated

- stronger DCF per share growth CAGR over the past five years (7.8% to 3.2%)

As a result, investors can choose between slightly higher overall quality in ENB or slightly lower valuation in TRP…or they can choose both.

An important final consideration is that they are both based in Canada (so are subject to tax withholding on dividends) and issue 1099 tax forms instead of K-1s, which make them attractive to many investors who otherwise would not be interested. Given the withholding tax on dividends (which can be recovered on your tax return in most circumstances for U.S. investors) and the tax treaty between the U.S. and Canada (which prevents withholding taxes on dividends in retirement accounts like IRAs and 401ks) as well as the 1099 tax form instead of the oftentimes problematic K-1 form (which can result in UBTI and extra taxes inside a retirement account), for many U.S. investors it will make sense to hold ENB and/or TRP in a retirement account.

Given the makeup of our midstream portfolio at High Yield Investor, we think that neither is the best fit for us at the moment and invest in five other midstream businesses instead. That said, we rate both ENB and TRP as Buys at the moment.

High Yield Investor Portfolio

Be the first to comment