gorodenkoff

A Quick Take On Bentley Systems

Bentley Systems (NASDAQ:BSY) reported its Q3 2022 financial results on November 12, 2022, missing revenue but beating EPS estimates.

The firm provides a large number of software applications for infrastructure and building design analysis and related information management.

Given the company’s substantial debt load in a growing cost of capital environment and apparently full stock valuation in present conditions, my outlook for BSY is Hold.

Bentley Systems Overview

Exton, Pennsylvania-based Bentley was founded to develop workflow software for infrastructure engineering for public works, industrial and commercial facilities globally.

Management is headed by President, Chairman and CEO Mr. Gregory Bentley, who has been with the firm since August 2000 and was previously founder and CEO of Devon Systems.

In addition, the firm was co-founded by Chief Technology Officer/EVP Keith Bentley and Director and EVP Barry Bentley.

Bentley offers a portfolio of software and services for the design, construction and operations of infrastructure. Their offerings include:

- Asset Performance software to improve asset management and performance

- Applications for 3D modeling, engineering analysis, surveying, mapping, and visualization

- Software for simulation, design coordination, and collaboration

- Software for plant engineering and operations

- ProjectWise for project information sharing

- Connected Data Environment to increase interoperability between systems

- Digital twins to enable real-time monitoring of physical assets

- OpenRoads technology for civil engineering design and construction.

The firm sells primarily through the direct sales channel, generating the vast majority of its revenues through this channel.

In geographic regions where it does not have a physical presence, BSY relies upon local specialist channel partners.

Bentley Systems’ Market & Competition

According to a 2018 market research report by The Business Research Company, the global market for infrastructure software was estimated at $231 billion in 2017, with Western Europe as the largest region accounting for $83 billion (36%) and the U.S. representing $49 billion (21.4%) of global demand.

The main drivers for expected growth are the continued development of infrastructure in both the developed and developing regions of the world.

Also, the delivery of software through cloud, whether public, private or hybrid, has gained acceptance from customers.

Major competitive or other industry participants include:

-

Autodesk

-

Trimble

-

Hexagon

-

Dassault Systèmes

-

AVEVA Group

-

Nemetschek

-

Oracle

-

Aspen Technology

-

Environmental Systems Research Institute

-

General Electric

Bentley Systems’ Recent Financial Performance

-

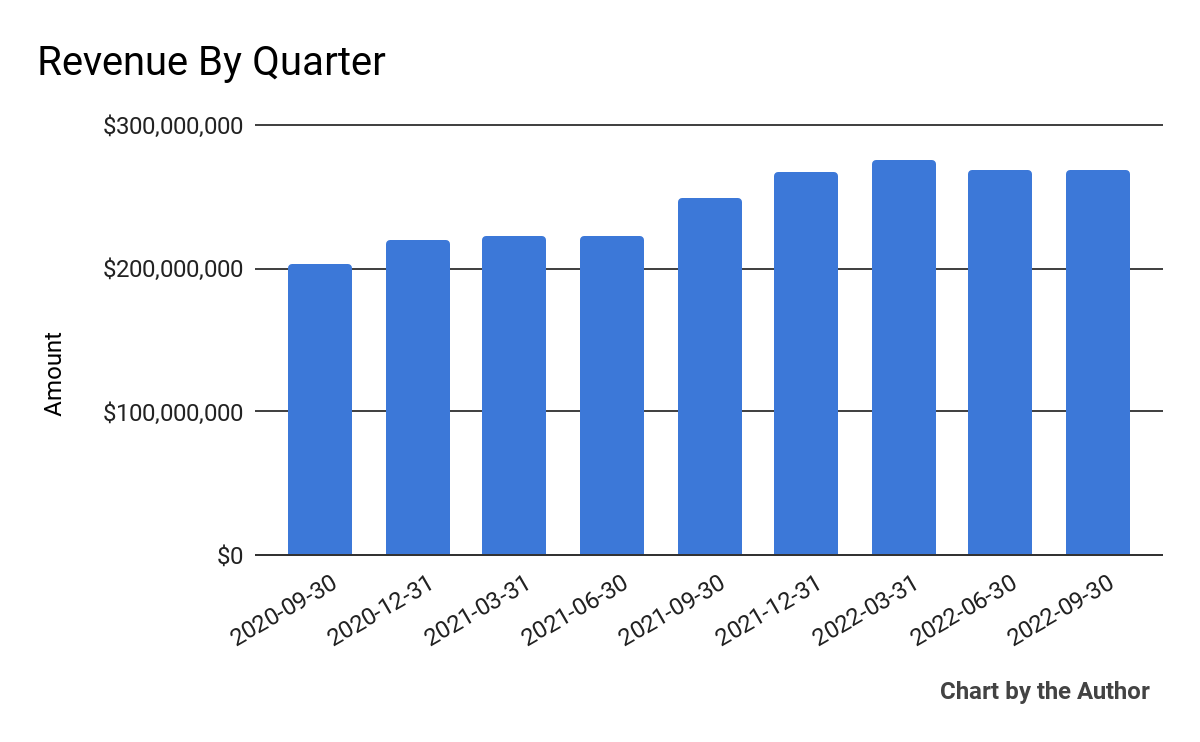

Total revenue by quarter has risen per the following chart:

Total Revenue (Financial Modeling Prep)

-

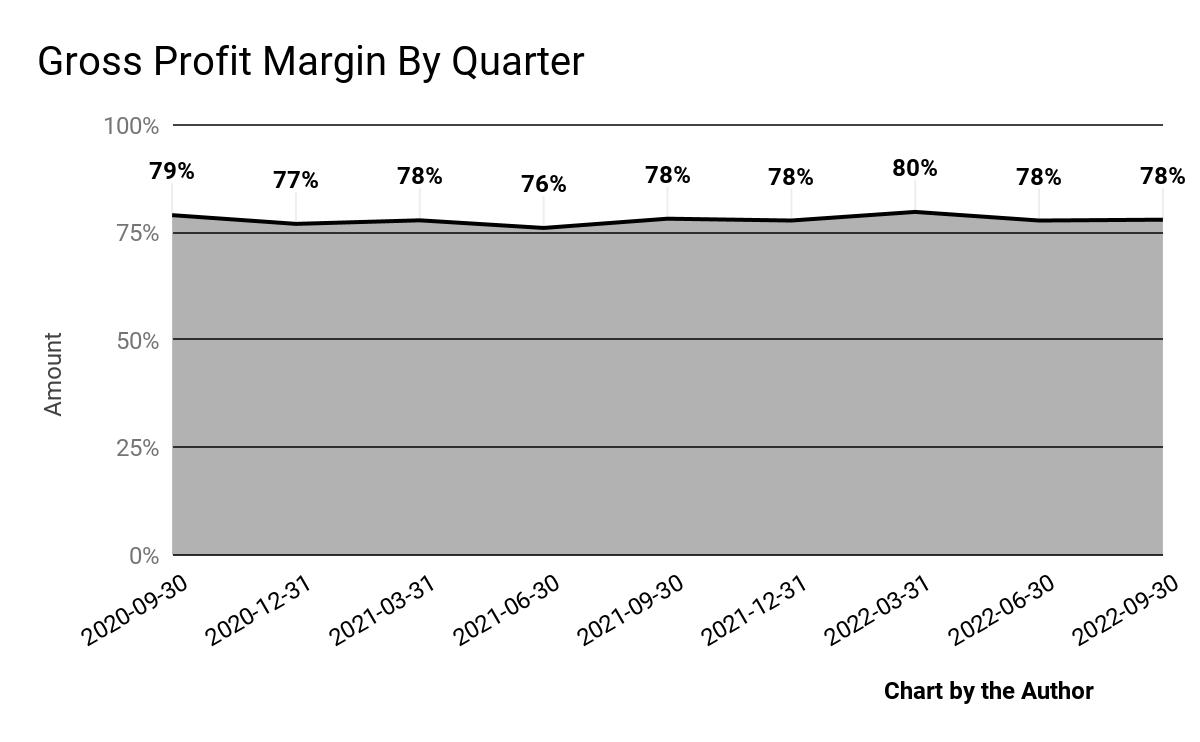

Gross profit margin by quarter has trended slightly higher in recent quarters:

Gross Profit Margin (Financial Modeling Prep)

-

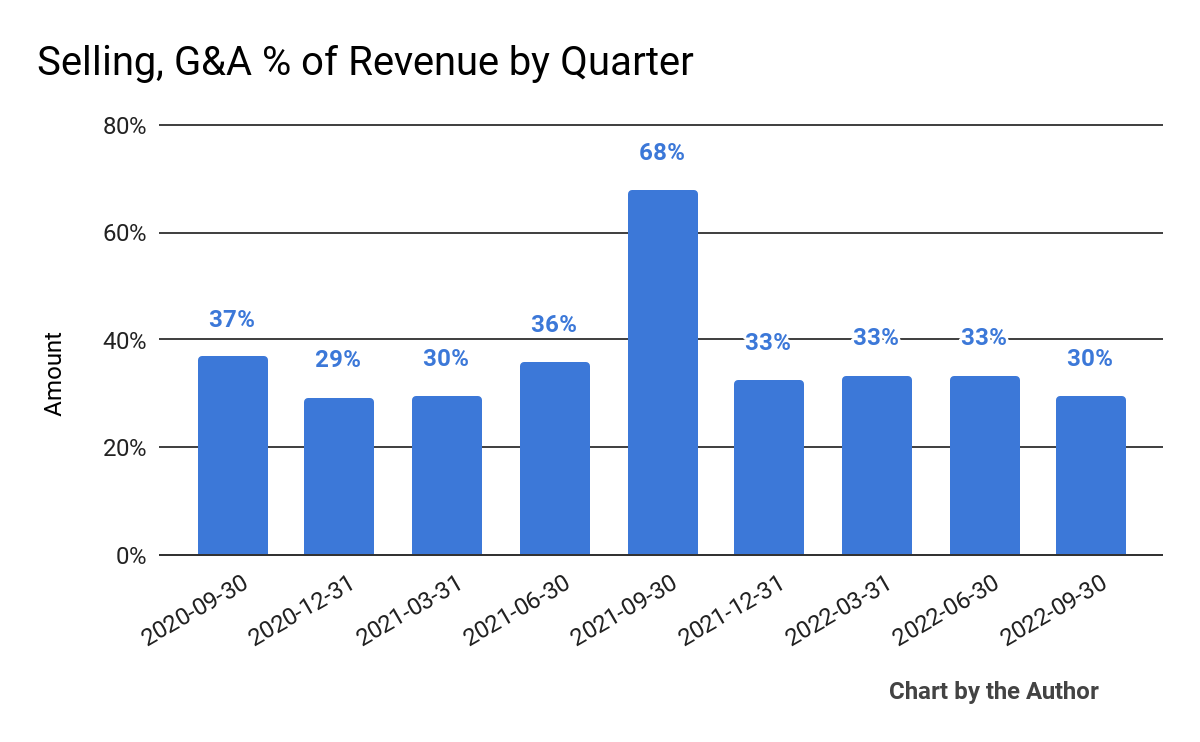

Selling, G&A expenses as a percentage of total revenue by quarter have largely remained within a tight range, except for Q3 2021:

Selling, G&A % Of Revenue (Financial Modeling Prep)

-

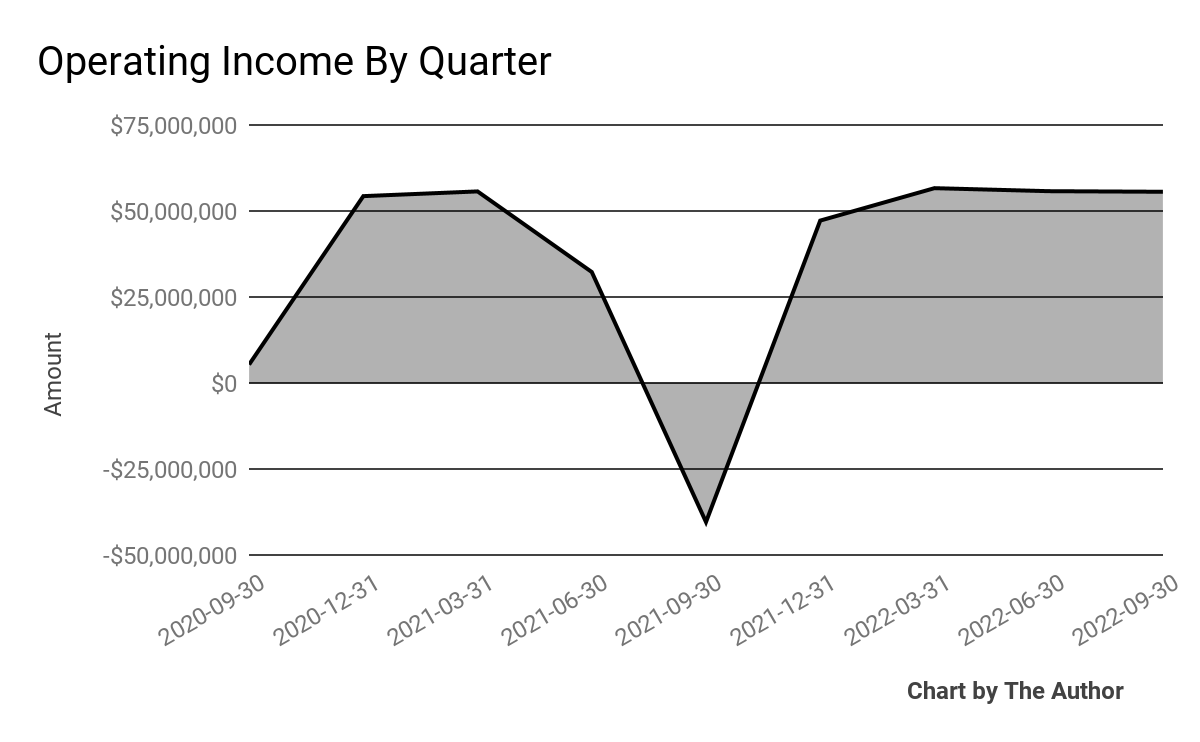

Operating income by quarter has shown the following results:

Operating Income (Financial Modeling Prep)

-

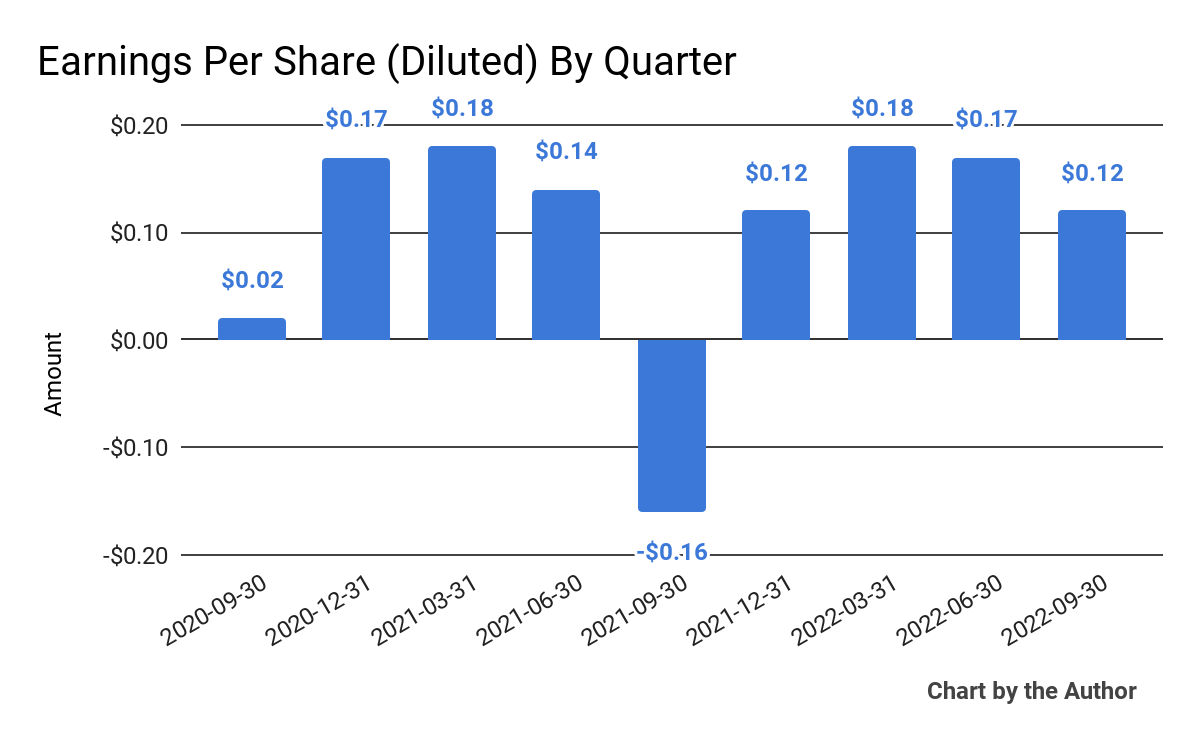

Earnings per share (Diluted) have produced the results shown below:

Earnings Per Share (Financial Modeling Prep)

(All data in the above charts is GAAP)

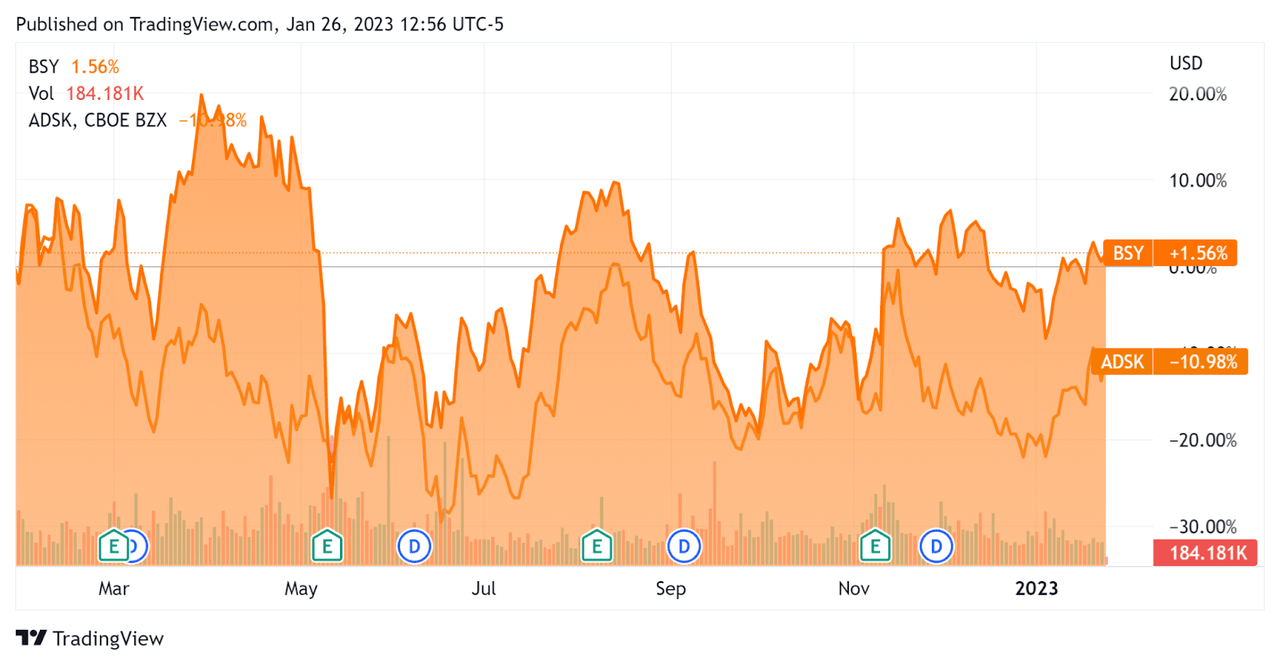

In the past 12 months, BSY’s stock price has risen 1.6% vs. that of Autodesk’s, which has dropped 11%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For Bentley Systems

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

12.6 |

|

Enterprise Value / EBITDA |

49.3 |

|

Revenue Growth Rate |

18.3% |

|

Net Income Margin |

17.4% |

|

GAAP EBITDA % |

25.5% |

|

Market Capitalization |

$10,976,237,568 |

|

Enterprise Value |

$13,555,626,918 |

|

Operating Cash Flow |

$318,805,000 |

|

Earnings Per Share (Fully Diluted) |

$0.59 |

(Source – Financial Modeling Prep)

As a reference, a relevant partial public comparable would be Autodesk (ADSK); shown below is a comparison of their primary valuation metrics:

|

Metric [TTM] |

Autodesk |

Bentley Systems |

Variance |

|

Enterprise Value / Sales |

9.2 |

12.7 |

38.5% |

|

Enterprise Value / EBITDA |

43.4 |

49.8 |

14.9% |

|

Revenue Growth Rate |

16.2% |

18.3% |

12.6% |

|

Net Income Margin |

12.6% |

17.4% |

37.5% |

|

Operating Cash Flow |

$1,880,000,000 |

$318,805,000 |

-83.0% |

(Source – Seeking Alpha and Financial Modeling Prep)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

BSY’s most recent GAAP Rule of 40 calculation was 43.7% as of Q3 2022, so the firm has performed well in this regard, per the table below:

|

Rule of 40 – GAAP [TTM] |

Calculation |

|

Recent Rev. Growth % |

18.3% |

|

GAAP EBITDA % |

25.5% |

|

Total |

43.7% |

(Source – Financial Modeling Prep)

Commentary On Bentley Systems

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted a ‘rebalanced business’ after its exit from Russia in Q2 2022 and the resulting negative financial impact on its business.

Leadership is seeing an ‘incremental uptick’ in its annual recurring revenue when compared with an ‘aberrantly high ’21 Q3 growth.’

The firm expects to benefit from the current ‘bulge’ in a backlog of projects per a survey of U.S. civil and other engineering companies. As to its financial results, total revenue rose 7% year-over-year on an as-reported basis, or 15% on a constant currency basis.

The company’s net retention rate was 110%, indicating reasonably good negative net churn from its customer base.

The firm’s Rule of 40 results have been excellent, with a moderate revenue growth result combined with a strong operating result contributing to a good figure for this metric.

Operating income in the past three quarters has been relatively flat while earnings per share has dropped in recent quarters.

For the balance sheet, the firm finished the quarter with $72.9 million in cash and $1.78 billion in debt.

Over the trailing twelve months, free cash flow was $299.4 million, of which capital expenditures accounted for $19.4 million. The company paid $43.6 million in stock-based compensation, much of which was to senior executives.

Looking ahead, management reaffirmed its previous guidance for full-year 2022, expressed in constant currency terms, to an adjusted EBITDA margin of 33%.

Regarding valuation, compared to competitor Autodesk, Bentley is being valued at higher EV/Sales and EV/EBITDA multiples, which is reasonable given its higher growth rate and net income margin.

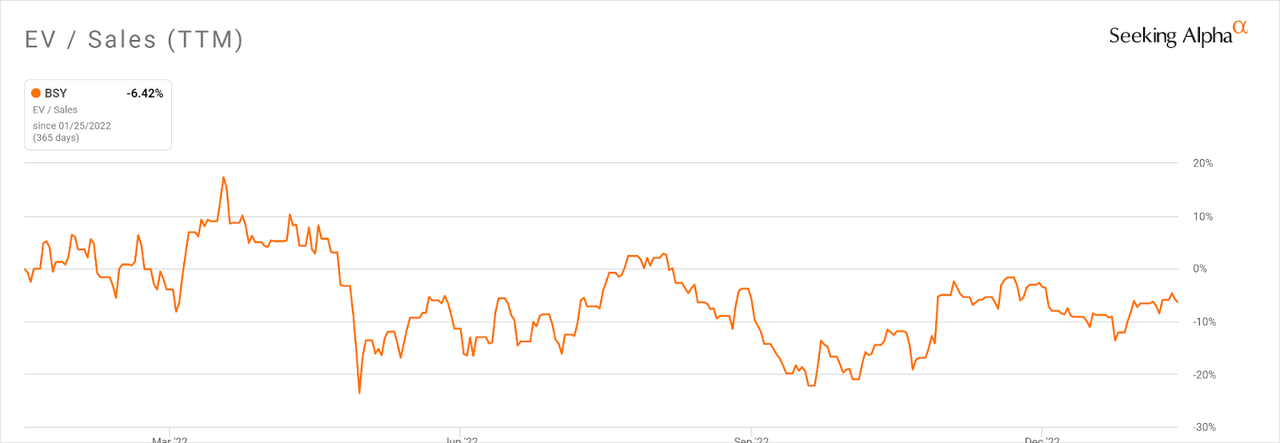

Notably, BSY’s EV/Sales multiple has compressed by only 6.4% in the past twelve months though it was as low as 22% down, as the chart shows below:

EV / Sales Multiple History (Seeking Alpha)

BSY management appears to be cautiously optimistic about the near-term future, but the stock looks to be fairly valued, at least in comparison to competitor Autodesk.

Given the firm’s substantial debt load in a growing cost of capital environment, my outlook for BSY is Hold.

Be the first to comment