gremlin

Airlines (represented by the U.S. Global Jets ETF (JETS)) are notoriously cyclical, and their profitability is highly sensitive to a range of macro and idiosyncratic events, for example, extreme weather, oil prices, terrorism, pandemics, etc. As an investor, I find it hard to sleep well at night investing in airlines. I appreciate trading airlines can be very profitable for the experts, but for me, I am always more concerned with the risks of permanent loss of capital.

I much prefer indirect exposure to the industry. AerCap (NYSE:AER) exactly fits the bill for me.

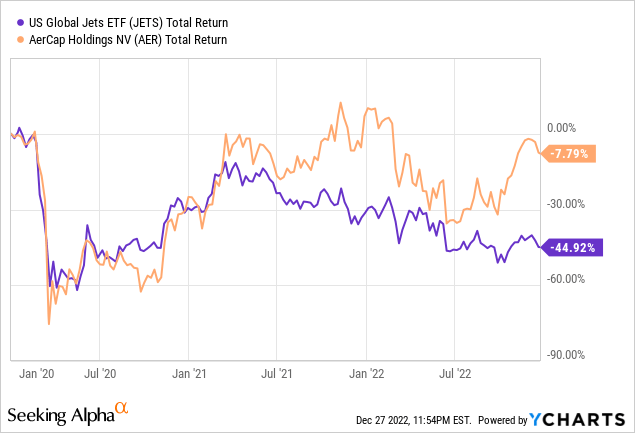

Consider the relative performance of AER and JETS during and after the pandemic:

The relative outperformance of AerCap reflects the fact that its profitability is secured by contracted cashflows that are collateralized. As such, the exposure to risk events affecting the industry is indirect and somewhat buffered by their aviation partners (some of which are government-owned or sponsored). Unlike some of the other airlines, there was no permanent loss of capital, equity issuance, operational losses, or otherwise debt raised to keep it afloat.

The Business Model

AerCap is by far the largest lessor of aircraft, helicopters, and engines. It enters into operating leases (unlike finance leases which are akin to vanilla lending), hence the economic and legal ownership of the assets remains with the lessor. In other words, at the end of the lease (say 8 to 12 years), the lessor is exposed to the residual value of the aircraft. As such, during the lease tenor, the lessor (i.e., AerCap) depreciates the asset in its books. The lessor may also impair the asset if there is a need to (e.g., the market value of the aircraft type decreases materially).

As such, the main direct expenses of the lessor are depreciation and interest expenses. Revenue is predominantly the lease payments. AerCap largely neutralizes interest rate risk by incorporating it in the lease agreement and/or utilizing fixed debt funding as well as derivatives to hedge the interest rate risk.

At the end of the lease, AerCap may extend the lease, redeploy to another lessee or sell the aircraft. AerCap routinely sells assets at a premium to book value, which is a testament to its robust depreciation policy. In the recent quarter, it generated a gain of 23% over book value. However, the long-term average gain is in the range of a high single-digit percentage.

In substance, AerCap’s business should be seen as a structured funding business. The credit risk is mitigated by the following lines of defense:

- The creditworthiness of the lessee/airlines (many of which are government-owned)

- The value of the asset. If the lessee breaches the lease agreement (e.g., does not pay), AerCap may repossess the aircraft and redeploy elsewhere

- Cash/credit collaterals posted by the lessee

- Insurance (e.g., act of war, aircraft destruction, etc.)

So in short, both credit and interest rates are generally well managed.

The Russia Seizures

The seizures of 113 planes and 11 jet engines by Russian authorities in response to sanctions triggered by the Ukraine war were clearly an exception to the above. Consequently, AerCap had to take a $2.7 billion pre-tax charge during the first half of 2022. AerCap may recover some (or all of it) through insurance, and this is currently still in litigation. Any recoveries from insurance would be a pure upside for AerCap.

In spite of this rare event (and material financial costs involved), AerCap was able to absorb this and still reach its targeted leverage ratio of 2.7x ahead of schedule, which demonstrates the resilience of its organic cash generation.

The Unit Economics

AerCap’s earnings can be thought of as comprising (1) a spread on leasing and (2) gains on disposal of assets (aircraft, helicopters, and engines). The current environment for aircraft leasing is strong given the significant delivery delays on new aircraft from the OEMs. This is primarily due to a shortage of engines available to service both new aircraft deliveries as well as repairing engines in a timely manner.

This translates to strong demand for the leasing product, aircraft disposals, and higher lease amounts. AerCap is, by far (at least a factor of 2), the biggest player in this space and is benefiting from the scale and diversification of product offerings. In the most recent earnings call, the CEO highlighted the data advantage for nimble portfolio decision-making:

The amount of data emanating from this level of transaction activity data is unparalleled and gives AerCap unique insights into the market allowing us to make meaningful decisions earlier, and with more conviction. Today, it’s the reason we are considerably more optimistic about global widebody demand than many others. We believe that the shortages we are currently experiencing in the narrowbody market will be replicated in the widebody market.

Naturally, the reopening of China, which is a huge aviation market, will tighten the supply in the market further and present significant opportunities for incremental growth.

On the expense side, AerCap is benefiting from having raised fixed debt funds during the pandemic at low rates and thus maintaining a low cost of funds of ~3.3%. Incremental debt at increased rates relating to new lease agreements is compensated by the lease agreement.

Gains on sale in the current environment have been very high (23% gain in the 3Q’2022) and possibly due to beneficial asset mix as well. A going-forward assumption of ~10% gains on disposals would be more in line with historical trends.

Importantly, AerCap maintains an investment grade rating with a positive outlook from both Moody’s and Fitch Ratings. The low cost of funds and ability to tap the market for liquidity is a key competitive advantage, especially in times of stress as seen during the pandemic.

Finally, as a result of the GE Capital Aviation Services acquisition, AerCap is guiding for significant synergies (~$150m) over time. This is another benefit of its scale and should ensure, together with competitively low cost of funds that it maintains the highest cost efficiency in the industry.

To sum it all up, based on its normalized earnings power, I expect AerCap to be able to sustainably generate 10% to 15% ROE throughout the cycle.

Capital Allocation And Valuation

Whilst AerCap does not pay a dividend, it has a shareholders’ friendly capital allocation framework. AerCap is arbitraging its capital structure by selling assets at a premium to book value and utilizing the proceeds to buy back shares at well below book. This is exceptionally accretive and helps to grow the book value per share rapidly.

AerCap is currently trading at slightly less than 0.8x book value. Given that it just reached its target leverage ratio in Q3’2022, I expect it to restart its share buyback program imminently.

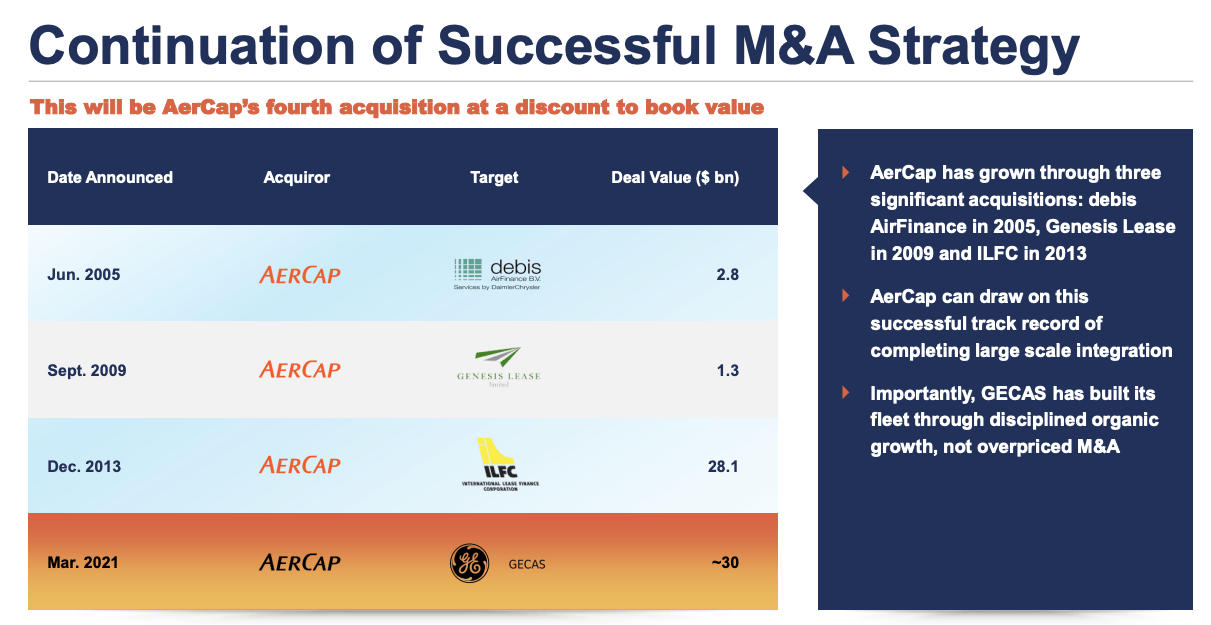

Disciplined Acquisitions At Discount To Book

AerCap has a strong discipline when it comes to M&A transactions. Whilst it did execute a number of transformational M&A transactions, all of these, have been concluded at a material discount to book value.

AerCap Investor Relations

The latest GECAS transaction was completed at a massive discount of >30%.

Once again, an opportunistic but transformational transaction completed at a distressed valuation. Under normal market circumstances, aircraft lease portfolios are typically consumed at 1.1x to 1.3x book value.

Final Thoughts

I see AerCap as having a superior risk/return investment profile compared to the airlines. I expect AerCap to compound its book value (and shareholders’ returns) at a double-digit clip in the next several years, driven by earnings and accretive share buybacks.

The CEO has a significant part of his net wealth (over 2 million shares) in the stock, so management’s interests and shareholders are very much aligned.

AerCap managed to survive both the pandemic and the Russia-Ukraine war and still thrive. This is probably one of the toughest stress tests someone could have envisioned for this firm, and it passed with flying colors.

I remain very bullish, especially given the industry tailwinds discussed in this article. This could very well be a Goldilocks period for AerCap even if a recession ensues.

Be the first to comment