Olga Tsareva/iStock via Getty Images

Aurora Cannabis (NASDAQ:ACB) has slipped below Nasdaq’s US$1 minimum listing requirement after nearly two years of its commons declining. The switch from euphoria to dread has come at a high cost for the company, which has seen its market cap fall to US$300 million as cumulative losses get aggregated with a recreational cannabis market in Canada, where illicit sales account for around 40% of total spending. This has meant the creation of two separate regimes. The regulated and highly taxed regime where Edmonton, Alberta-based Aurora operates. The second regime is the buoyant black market, which still accounts for C$4 in every C$10 spent on cannabis in Canada. This has somewhat rendered the Canadian cannabis market a non-starter for long-term value creation, with revenue weakness and unprofitability being inherent in the highly burdensome structure of the first regime.

The company would report revenue of C$61.68 million, up 1.8% from its year-ago comp but with medicinal cannabis sales down 14% during the quarter. But in many ways, the results didn’t matter. Aurora now operates in a zone now highly defined by uncertainty and fears aggregated over many years. The company is past the turnaround stage, with the slow-paced nature of the Canadian cannabis market leaving little room for a breakout performance. This describes the high taxes and centralized mode of distribution with low single-digit sales growth for some years now. Indeed, it’s unlikely there will be a surge in legal cannabis sales in Canada all of a sudden without an extensive redraft of the current laws. The black market won’t disappear, the high tax burden will remain in place, and any increases in the price of the average net selling price of dried cannabis will be short-term and short-lived.

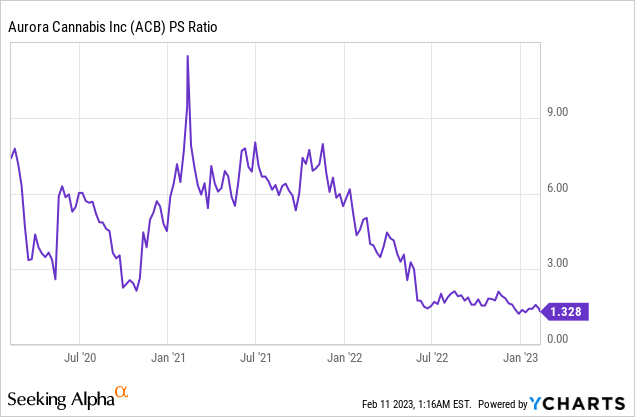

The impact of this is mostly expressed in the compression of Aurora’s retrospective valuation multiple, which has fallen to 1.33x. This in effect encapsulates the level of sentiment attached to each dollar of revenue earned. Higher multiples, which were north of 10x just over 2 years ago, capture periods of time when enthusiasm was more widespread among its shareholder base. The recovery of this in lieu of operational momentum will be the core driver of returns this year.

Cost Savings Progresses But Net Loss Maintains Negative Momentum

Aurora Cannabis reported full revenues of C$61.68 million for its last reported fiscal 2023 second quarter ending December 31, 2022. This was made up of medical cannabis sales of C$39.5 million, down 14% from its year-ago comp, and recreational cannabis revenue that increased by 2% year-over-year to reach C$14.6 million.

The average net selling price of its dried cannabis at C$4.79 was a 6% increase from its year-ago comp and came on the back of a 17% year-over-year increase in kilograms sold to 15,269. Whilst total revenue growth of nearly 2% seems immaterial, its Canadian cannabis peers reported declines in revenue for their most recently reported quarter. Canopy Growth would report a year-over-year revenue decline of 28% and Tilray would report a decline of 7.1%. Aurora’s relative outperformance against its peers was likely due to its growing international medical cannabis business, with sales to the UK, Australia, Poland, and the Cayman Islands being highlighted by management.

There has also been further momentum with the legalization of cannabis sales in Germany and Japan. Hence, with Aurora demonstrating an ability to tap into these highly complex and small but growing international markets, the company could be in a good position to benefit from what now looks like a growing wave of global medical cannabis sales.

A Second Reverse Stock Split In The Cards

This has placed the overall profitability of Aurora in view. The company recorded a gross profit margin of 49%, down from 54% in the year-ago quarter. The 500 basis points decline was partly blamed on growing medical cannabis exports to developing countries, which comes with lower margins than the company’s Canadian and European export markets.

The core takeaway from the earnings report was the fall in SG&A expenses by 33% year-over-year to C$25.43 million. This would drive a positive adjusted EBITDA of C$1.43 million, in line with Aurora’s prior guidance as the company pursues a cost-saving program. However, net loss from operations was still negative at C$67.2 million, an increase from C$51.9 million in the prior quarter but an improvement on the year-ago figure of C$75.1 million.

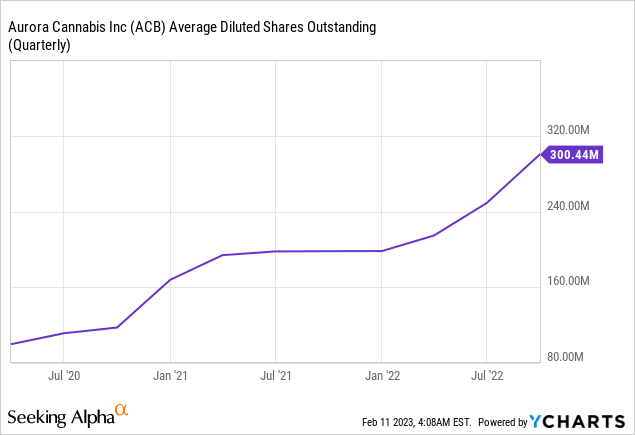

Hence, whilst the company exited the quarter with cash and restricted cash of C$310 million, the underlying business is loss-making and the cash position is being built on the back of material dilution. Cash used in operations was C$60.65 million, a nearly 3x increase from a cash burn of C$21.57 million in the year-ago quarter. Hence, Aurora’s average diluted shares outstanding have been on an unsatiable upward rise, with any rallies seen as an opportunity for the company to issue more shares. Around US$134.4 million in securities remained for sale as of the end of the quarter on the back of their March 2021 base shelf prospectus. The company sold 39,500,341 million shares during the quarter for C$68.8 million in net proceeds.

With continued net losses and dilution on the horizon, we could see the share price get driven lower. This opens up the specter of yet another reverse stock split, which would amount to placing a bandage on a deep cut. Aurora will need to correct this unsustainable situation until it can drive positive returns even as it sees growth.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment