Business on Wall Street in Manhattan

Pgiam/iStock via Getty Images

On 10/10/22 Seeking Alpha published my article entitled “Atlis Motor Vehicles Is On A Road To Nowhere.” Since then the stock has continued to free-fall financially and has decreased from $17.80 to $3.25, or 81.7% as of 12/31/22. I initially intended to write this follow-up article after the issuance of the Annual Report 10-K, which contains audited financial statements and is due to be filed with the SEC by 3/15/23. However, several items of concern that I believe deserve to be brought to light at this time have prompted me to this article. Before I get into specifics, let’s take a peek at the company.

About AMV

Atlis Motor Vehicles, Inc. (NASDAQ:AMV) was formed as a Delaware corporation on 11/9/16 and is based in Mesa, Arizona. ATLIS is a vertically integrated, mobility technology company developing ATLIS Energy, a superior battery technology solution; ATLIS Charging, an advanced charging station; and ATLIS XT pickup truck.

Source: Company

Stock performance

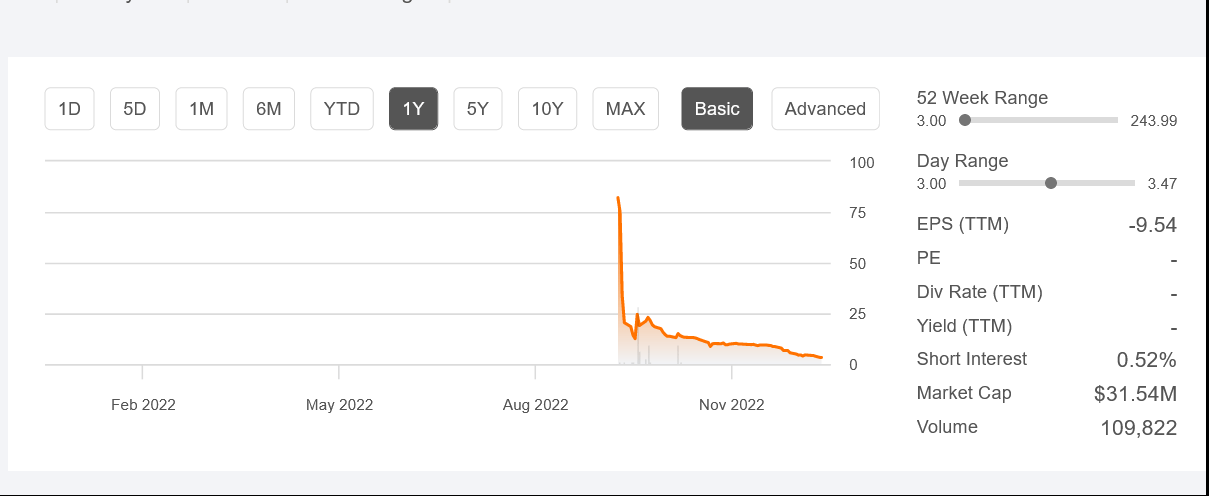

www.seekingalpha.com/amv

As the above chart shows, AMV has essentially cratered in Q4 of 2022, as the stock price plummeted from $20.40 to $3.25, which represents a decrease of 84%. In addition, 80% of the average daily volume from mid-Q4 until 12/31/22 has been ~ 100K, which is significantly less than the average daily volume of ~300K. On 12/27/22, AMV disclosed that the lock-up period regarding the Class A common stock purchased through Reg CF and Reg D that may have had restrictive legends had expired, which means that trading volume may accelerate going forward. I believe there is more downside risk to the stock from disgruntled stockholders as they may choose to limit their losses by selling into any rebound in the stock price. This would also increase the beta associated with AMV, which has had an extremely erratic trading history since it began trading on the NASDAQ on 9/27/22 via a Regulation A filing. The ungodly high/low price range of $243.99/$3.00 since becoming a public company underscores the pronounced volatility of this highly speculative stock. As I alluded to in my last article, there has been strong evidence of day trading in Q4, and I believe this may resurface periodically. High-volume days absent any news would signal the presence of this activity.

AMV vs. their peer group

The emerging EV sector is amid much froth, and the 4 stocks in the company’s peer group- Lightning eMotors, Inc. (ZEV), GreenPower Motor Company Inc. (GP), Vicinity Motor Corp. (VEV) and FreightCar America Inc. (RAIL) decreased by an average of 66.5% in the last 12 months. ZEV, which has declined 96.7% since my bearish article of 2/15/22 is currently rated hold, while the other cohorts are rated either sell or hard sell. In my view, all of these companies have a high risk of operating poorly, especially since industry behemoths Ford Motor Company (F) and General Motors Company (GM) will ramp up their EV offerings this year.

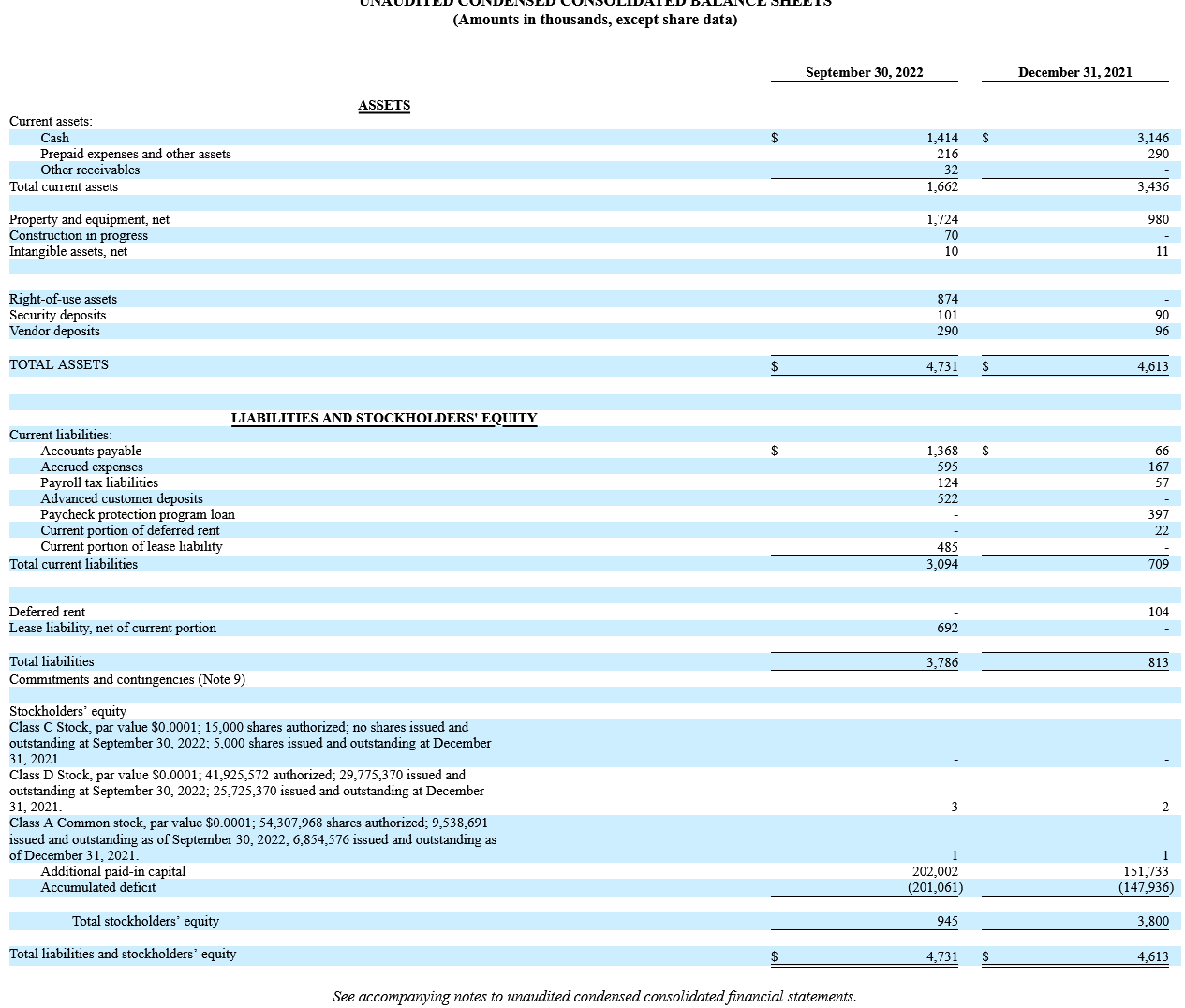

AMV balance sheets, income statements, and cash flow statements data

www.atlismotorvehicles.com

www.atlismotorvehicles.com

Key takeaways- condensed consolidated balance sheets:

- AMV has a cash balance of $1.4M as of 9/30/22 compared to a cash balance of $3.1M as of 12/31/21. This difference of $1.7M represents a decrease of 54.8% YTD.

- AMV had a current ratio of 0.54 as of 9/30/22 compared to a current ratio of 4.85 as of 12/31/21.

- AMV had a working capital deficit of $1.4M as of 9/30/22 compared to a working capital balance of $2.7M as of 12/31/21.

www.atlismotorvehicles.com

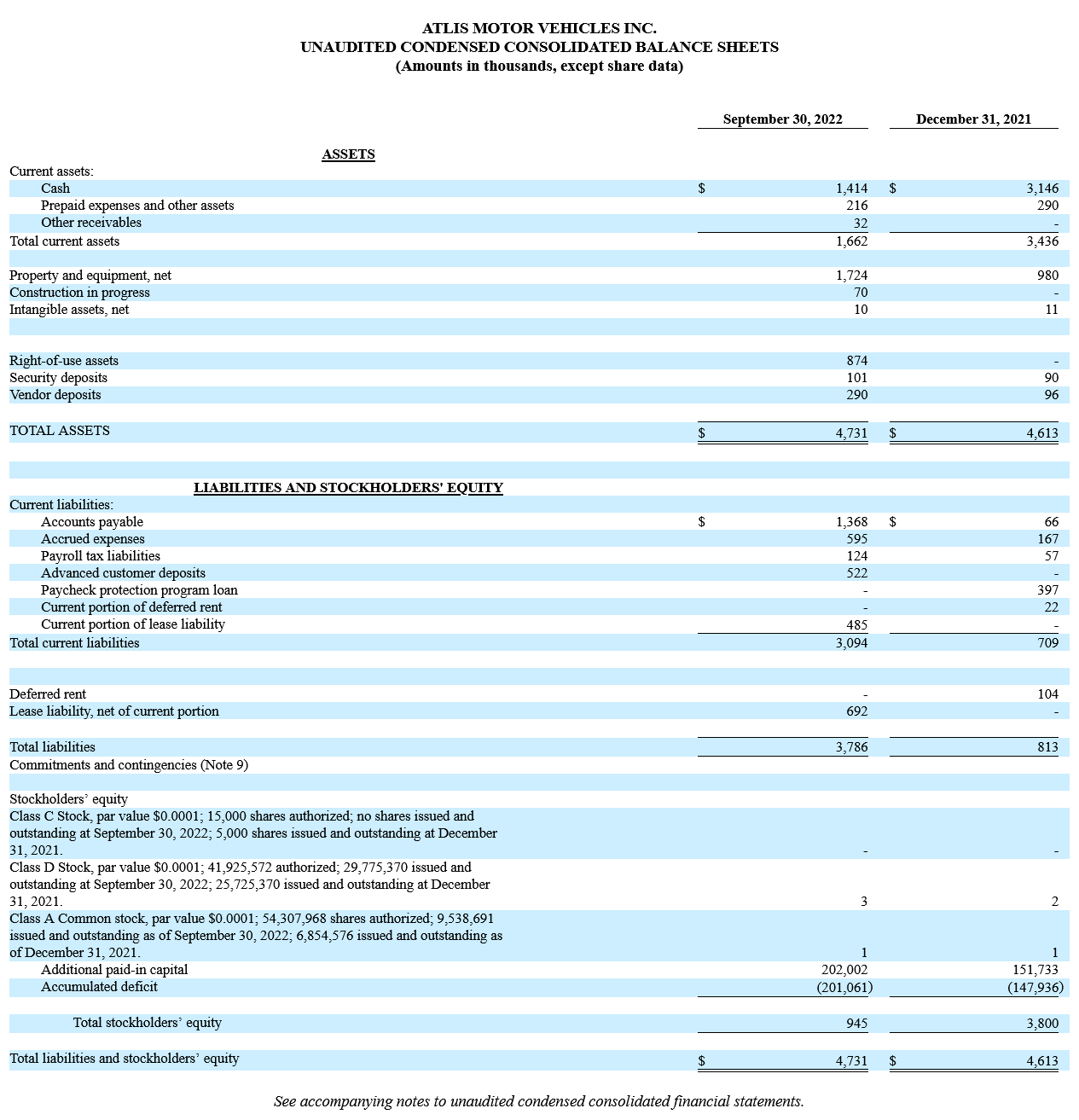

Key takeaways – condensed consolidated statements of operations:

- AMV had a net loss of $53.1M for the 9 months 9/30/22 compared to a net loss of $95.8M for the 9 months ended 9/30/21. which represents a decrease of $42.7M or 44.6%.

- AMV had stock based compensation expenses of $34.3M for the 9 months ended 9/30/22 compared to $88.3M for the 9 months ended 9/30/21.

- AMV had advertising expenses of $5.1M for the 9 months ended 9/30/22 compared to advertising expenses of $2.2M for the 9 months ended 9/30/21.

- AMV had a loss of $152K on disposal of property and equipment for the 9 months ended 9/30/22.

www.atlismotorvehicles.com

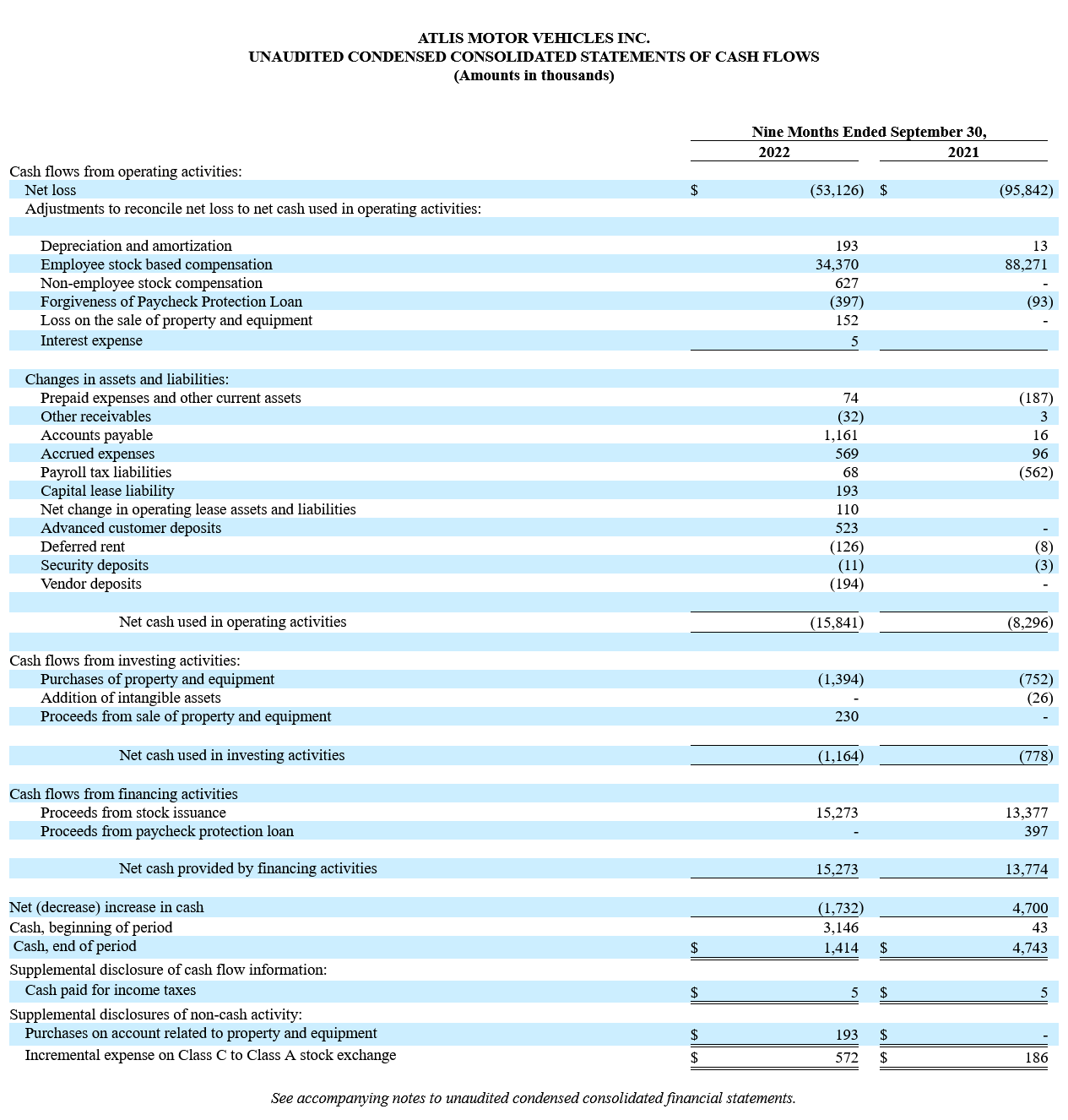

Key takeaways- condensed consolidated statements of cash flows:

- Net cash used in operating activities of $15.8M for the 9 months ended 9/30/22 compared to $8.3M for the 9 months ended 9/30/21.

- Net cash used in investing activities of $1.2M for the 9 months ended 9/30/22 compared to $0.8M for the 9 months ended 9/30/21.

- Net cash used in financing activities of $15.3M for the 9 months ended 9/30/22 compared to $13.8M for the 9 months ended 9/30/21.

Recap

Based on my review of AMV’s Q3 10-Q, it is clear that the company is woefully undercapitalized as of 9/30/22 as the cash balance decreased by $1.7M or 54.8% YTD. The present paltry cash balance of $1.4M will be grossly inadequate to meet their financial obligations for 2023 based on their present “run rate” coupled with announced planned increases in both capital expenditures and operating expenses associated with further development of their technology.

Q4 events

- On 11/3/22 AMV entered into a Securities Purchase Agreement (Private Placement) with unnamed institutional investors under which the company agreed to issue to the Investors, for gross proceeds of up to $27,000,000, Senior Secured Original Issue 10% Discount Convertible Promissory Notes in the aggregate principal amount of up to $30,000,000 and warrants to purchase several shares of the Company’s Class A common stock equal to 30% of the face value of the Notes divided by the volume weighted average price, in three tranches.

This capital infusion will help alleviate a cash crunch for the foreseeable future but it has a dilutive effect on present shareholders, compounded by the favorable terms and conditions negotiated by these investors.

- On 11/15/22 AMV announced that it had begun trial mass production of its battery technology, which they have previously stated is at “the core of their hardware ecosystem and platform and is designed to be capable of charging a full-size pickup in less than 15 minutes.”

As I stated in my prior article, that achievement would be “an instant game-changer for the company as they would have the opportunity for multi-million licensing deals with other vehicle manufacturers.” However, this is a “heavy lift” and if AMV is not able to develop its proprietary battery technology on time and on budget that would be an existential moment for the company.

Bull case

The bull case remains largely based on company press releases, renderings, simulated images, website data, links to media coverage, and a 2022 “Wrap Up” which readers may access here. On 12/22/22 Maxim Group LLC initiated coverage of AMV with a price target of $15. However since Maxim Group LLC also acted as the exclusive placement agent for the private placement, I admit to a certain degree of “professional skepticism” in this regard.

Stock based compensation

- Stock based compensation has long been a complex and controversial accounting topic. I am philosophically agnostic about the subject because I fully realize that start-up companies are often faced with a Hobson’s choice given their need to preserve capital and their need to attract high-priced technical talent. That said, in my view that AMV has abused the underlying spirit and intent of ASC Topic 718 as the company has expensed $130.6M in stock based compensation from 1/1/20 to 9/30/22. On 4/14/22 Kailash Concepts Research published an article entitled “SBC: An Update on the Absurd” which gave “dubious awards” to companies where stock based compensation represents over 1/3 of sales. Although AMV is a pre-revenue development stage company, and since any number divided by zero is undefined, I would suggest that in the future it very well qualify for this “distinction.”

Common stock

The breakdown of common stock by class as of 9/30/22 and 12/31/21 was as follows:

|

September 30, 2022 |

December 31, 2021 |

|||||||

|

Class A |

9,538,691 |

6,854,576 |

||||||

|

Class C |

– |

5,000 |

||||||

|

Class D |

29,775,370 |

25,725,370 |

||||||

|

Total Shares Outstanding |

39,314,061 |

32,584,946 |

||||||

As the above table shows, Mark Hanchett, CEO beneficially owns and controls a majority of the voting power of the company via the superior voting rights associated with the Class D shares. This classifies AMV as a “controlled company” within the meaning of the Nasdaq listing rules. Under these rules, a company of which more than 50% of the voting power is held by an individual, a group or another company is a “controlled company” and may elect not to comply with certain corporate governance requirements of Nasdaq. As a result, stockholders do not have the same protections afforded to stockholders of companies that cannot rely on such exemptions and are subject to such requirements.”

Capital structure

www.atlismotorvehicles.com

As the above table shows, the Class D common stock is solely owned by Mark Hanchett, CEO, and Annie Pratt, President who own 22,603,676 and 8,071,696 shares of our Class D common stock, respectively, representing approximately 71% and 26% of the voting power of our outstanding capital stock, respectively, for an aggregate of 97% of the voting power of the outstanding capital stock of the company. In my view, this egregious example of the gross misalignment between equity and voting rights is not indicative of a shareholder-friendly company and would be viewed as a “deal killer” by many institutional investors.

Conclusion

Based on the foregoing financial and operational analysis, I believe that AMV continues to face multiple challenges going forward. The entire EV sector is in a reset mode which has resulted in significantly lower valuations, as the Wall Street environment has no appetite for money-losing companies like AMV, which has a limited operating history as a public company and an unproven technology that will require substantial capital beyond the $370M which the company says will allow them to achieve profitability In addition, the imminent emergence of industry titans Ford Motor and General Motors will be a high hurdle for AMV which lacks the financial firepower to succeed in this increasingly competitive market. On a broader level, recessionary fears may rise precipitously in 2023, possibly as early as mid-Q1. Potential headwinds include a weakening of the U.S. labor market, declining corporate sales, narrowing operating margins, and lower profitability across the broad spectrum of industries. This will make AMV’s access to capital very problematic, and their fragile financial statements and misaligned capital structure will severely limit their ability to attract institutional investors of any stature. This suboptimal situation will force them to resort to again to the private placement and other alternative asset class sources. AMV’s depressed stock price will give them little negotiating leverage which means that any funding they may manage to obtain will be on onerous terms and massively further dilute present stockholders and also be accompanied by costly accounting, legal, and transactional fees. As a result, in my opinion, Atlis Motor Vehicles Inc. needs a “Hail Mary.”

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment