AndreyPopov

Thesis

Atlassian (NASDAQ:TEAM) has low profitability and slowing growth. They operate in a highly competitive industry and could be disrupted. We would need to see a significant improvement in growth and profitability before viewing this as an opportunity to buy the dip.

Profitability Issues

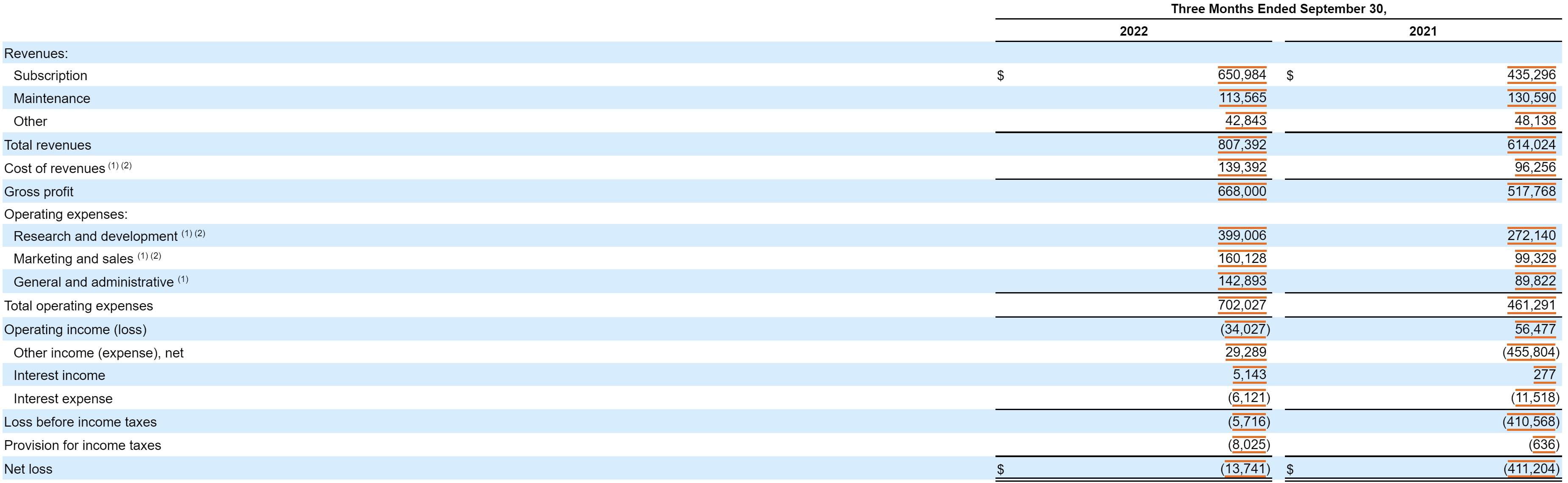

In their most recent quarter Atlassian reported a net loss of $13 million. Their quarterly revenue came in at $807 million, which is 31% growth year-over-year.

Income Statement (Atlassian Q1 Earnings Report)

The company had an operating profit in the year ago period but this year swung to an operating loss. This shift is bad news because it implies that Atlassian is facing increased cost pressures and/or competitive pressures.

Many would argue that the company is cash flow positive, however these cash flows are only positive because of SBC. If employees didn’t get the SBC they would just demand the shortfall be made up in cash. Many software companies point to non-GAAP measures of profitability in order to shift attention from their lack of GAAP net margins. A cloud based software business should have high net margins due to the nature of their operating model. If they don’t it should appear as a red flag to investors. While a lack of high GAAP net margins can be ignored if there is rapid revenue growth, the growth rate of Atlassian does not justify their lack of profitability especially when they trade at a PS ratio of 12.97.

Slowing Growth

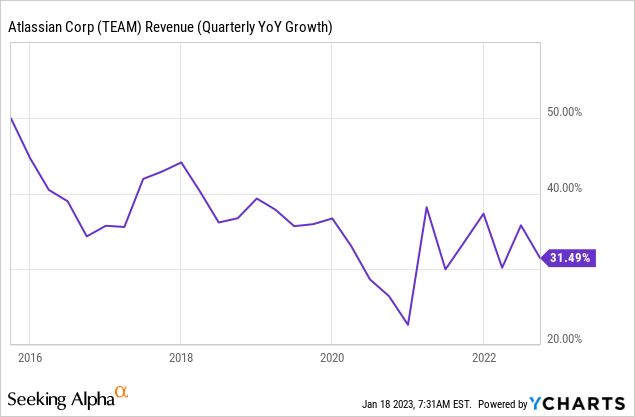

While growing revenue at a rate of over 30% would be great for many companies, as a loss making tech company Atlassian needs to show high levels of revenue growth in order to justify their low profitability. Considering they currently trade at a PS of 12.97 and are not profitable, 30% revenue growth just isn’t going to cut it anymore. Going forward it is likely that this revenue growth rate decelerates due to their now larger size as well as the increasingly competitive nature of their industry.

Software Overload

The project and team management software sector is becoming increasingly competitive. Here are just a few companies that participate in the industry:

Oracle Corporation

ServiceNow

SAP SE

Elecosoft

NetSuite

Citrix Systems, Inc.

Deltek, Inc.

Unit4

Zoho Corporation Pvt. Ltd.

Total Synergy

Hive

Digité, Inc.

Wrike, Inc.

MeisterLabs

monday.com

Basecamp

ProjectManager.com, Inc.

Whizible

Zilicus Solutions

Asana

Atlassian

There are many more smaller companies and startups competing in the management software sector that aren’t listed here. The competitive landscape is more fierce than it was in the past because of how relatively easy it is to create these solutions. An established tech firm or startup can create project/team management software in a short period of time and with very similar functionality to the most popular products. All of these companies are eager for their solution to be the one that customers choose and are willing to burn mountains of cash to make that happen. This can result in a price war scenario when there is little else to differentiate solutions.

If a larger tech firm bundles software that is similar to what Atlassian provides with their other enterprise software products, over the long-run it makes it difficult for customers to go out of their way to choose Atlassian (think Microsoft Teams vs Zoom).

Granted, it isn’t this simple in reality and Atlassian is continuously creating new products for their customers to use as well as boasting a high customer satisfaction rate. That being said, increasing competition is never great for a company that already struggles to operate profitably.

Price Action

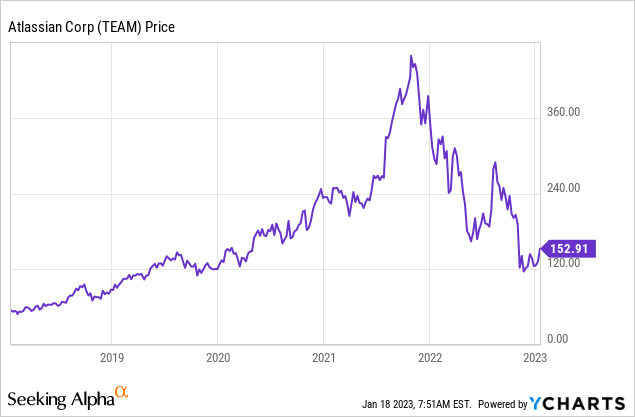

Up until 2022 Atlassian’s stock had been a great performer. The company has since fallen victim to a risk-off investing environment where growth stocks have fallen out of favor. We do not view this as an opportunity to buy the dip. There are many better opportunities out there for investors to allocate their capital.

Valuation

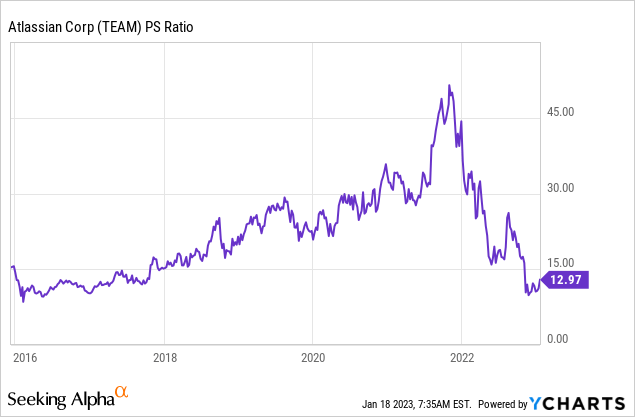

Atlassian is currently unprofitable and has never generated meaningful profits so analyzing them on a price to earnings basis is futile. Our next best solution is to evaluate them on a price to sales basis.

While it has come down considerably, a PS of 12.97 is still very rich for a company that is only growing revenue 30% year-over-year. I say “only” because as a loss making company Atlassian has a greater burden to produce high levels of revenue growth to justify their lack of profitability.

We view the current valuation of Atlassian as being too expensive. If the company is able to increase their rate of revenue growth and significantly improve profitability we would likely change our minds, but for now the company remains a show me story.

Risks

One risk to this bearish thesis is if Atlassian can continue to innovate and is able to outcompete their rivals. This is up to management to execute and is certainly a possibility, however due to the sheer amount of competition we would be cautious in assuming that Atlassian can beat the competition without taking a hit on pricing.

Another risk to this bearish thesis is Atlassian’s ability to accelerate revenue growth and become highly profitable. If they can achieve this the stock will likely be cheap at these levels. We have seen too many software companies that never could quite generate high levels of profit and will wait for management to prove us wrong here.

While there are risks to the upside investors don’t lose anything by waiting on the sidelines, especially when there are a multitude of better opportunities out there. In this type of market investors can afford to be picky.

Key Takeaway

A PS multiple of 12.97 is not justified by Atlassian’s rate of growth given their lack of profitability. We would wait for another massive selloff or a significant improvement in operating results before considering an investment in this company.

Be the first to comment