ipopba

Buying into high-quality, rapidly-growing businesses can be a great way to generate a positive return. But this doesn’t necessarily mean that any company that meets this definition is a great prospect. You also need to factor in the price that you’re paying for that quality and growth. One firm that seems to be a bit pricey, even though it is growing nicely and proved its quality on February 13th when it beat analysts’ expectations for sales and profits for the final quarter of its 2022 fiscal year, is Arista Networks (NYSE:ANET). Operationally speaking, the picture for the company has been quite positive and I suspect that trend will continue for the foreseeable future. But because of how shares are priced, even with the recent outperformance reported by management, I do think a more appropriate rating for the business at this time is a ‘hold’. This is a rating that denotes my belief that shares should generate upside that more or less match what the broader market should achieve moving forward.

A great quarter doesn’t change things for Arista Networks

Operationally speaking, Arista Networks operates as a ‘data-driven, client-to-cloud’ business that’s geared toward next-generation data center and campus workspace environments. To really understand the company though, we should discuss some of what the problem is that management is trying to solve. According to the company, cloud networks and legacy networks are fundamentally different at their core. There are multiple points to this argument that management makes clear in their annual report. But the short version is that large-scale cloud networks often require higher network availability than traditional networks do. This is due, in part, to the fact that cloud networks are set up to largely be server-to-server, and, at their core, this setup permits a wide variety of programmability, usually using third-party applications, in order to achieve the goals that their users want. Legacy networks, meanwhile, are typically not programmable, making it difficult to use third-party applications and resulting in network traffic that is server-to-client in nature. The same third-party applications that would work on cloud networks can be difficult or even impossible to implement on legacy networks.

To address these concerns and more, Arista Networks has created a suite of products for its customer base. At the core of its platform is an advanced network operating system known as EOS (Extensible Operating System). This, combined with a set of network applications and ethernet switching and routing platforms, is supposed to provide improved price and performance for its customers while reducing time to market in delivering a cloud networking solution with scale and availability combined. The EOS offers not just a high-quality network, it also offers complete switch and router capabilities, and full programmability. It has grown to be trusted by over 9,000 customers spread across data center operations, cloud-native segments, private and public cloud networks, campus networks, and more. It is even used in edge computing activities. Through its Arista CloudVision automation platform, the company also offers complete network telemetry, network automation simplicity, and more.

Author – SEC EDGAR Data

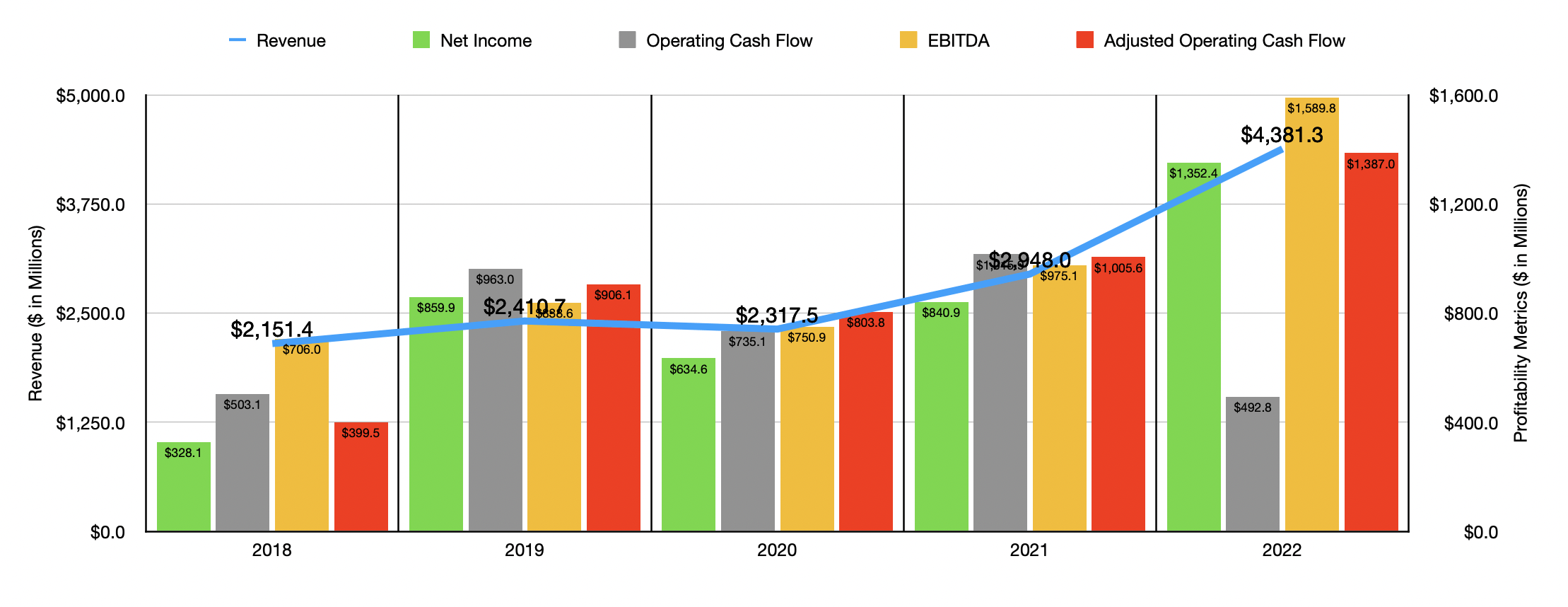

Over the past few years, the trajectory taken by Arista Networks has been quite positive. Revenue rose from $2.15 billion in 2018 to $2.95 billion in 2021. During its 2022 fiscal year, revenue skyrocketed, hitting $4.38 billion. The largest chunk of this revenue growth came from its product sales. This consists largely of sales of its switching and routing products, as well as related network applications. Revenue there spiked 56.3%, climbing from $2.38 billion to $3.72 billion. This increase, management said, reflected strong demand for its switching and routing platforms across its customer base. Service revenue, which is mostly focused around sales of PCS (Post-Contract Support) contracts that are usually purchased in conjunction with its products, rose a more modest but still impressive 16.6% year over year.

Bottom line results for the company also improved. Net income went from $328.1 million in 2018 to $840.9 million in 2021. In 2022, profits moved even higher, hitting $1.35 billion for the year. Other profitability metrics followed a similar path. Operating cash flow, for instance, rose from $503.1 million in 2018 to $1.01 billion in 2020. Where it diverges, though, is in the fact that, during 2022, it plunged to $492.8 million. If we adjust for changes in working capital, however, the metric would have risen from $1.01 billion in 2021 to $1.39 billion in 2022. Also on the rise during this time was EBITDA, a figure that rose from $706 million in 2018 to $1.59 billion in 2022.

Author – SEC EDGAR Data

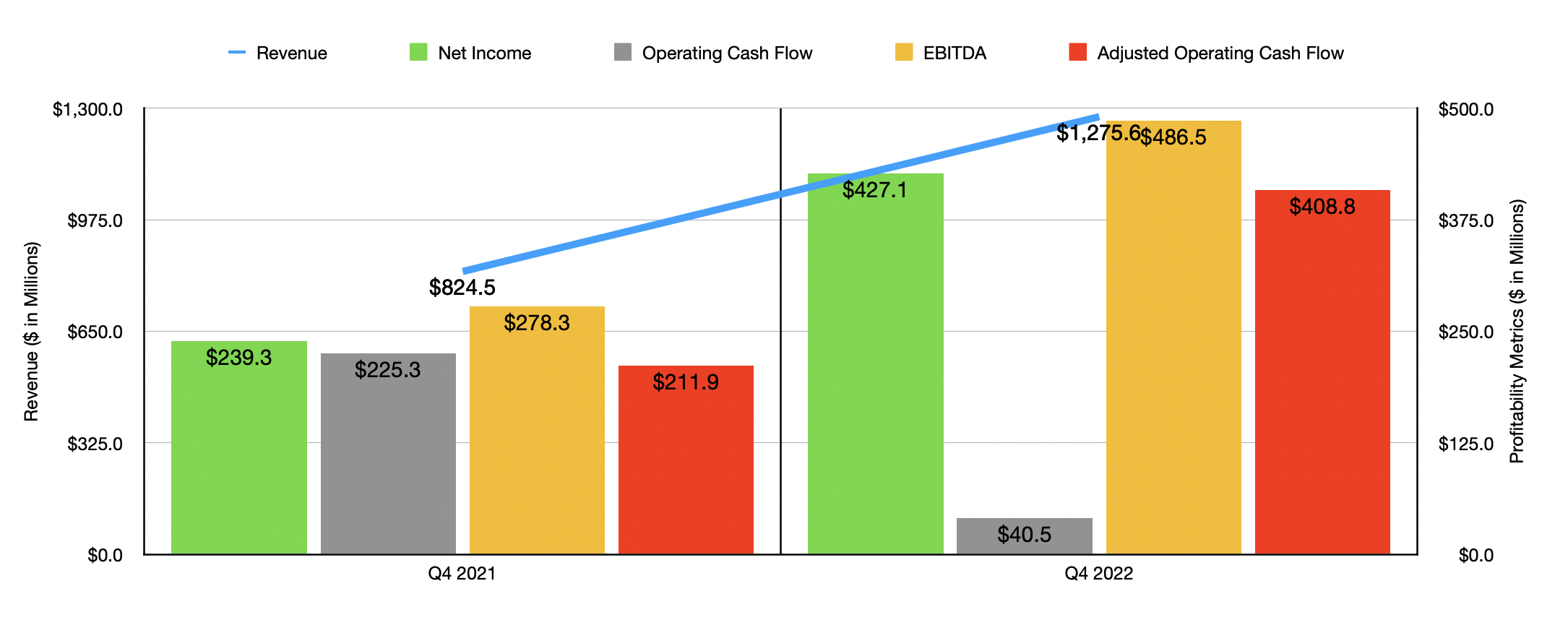

The data for 2022 includes, naturally, data covering the final quarter of the company’s 2022 fiscal year. This information was released by management on February 13th, after the market closed. The next day, February 14th, shares of the business rose about 4% in response to the development. The enthusiasm centered around both top line and bottom line results for the company. For instance, revenue of $1.28 billion came in 54.7% higher than the $824.5 million that the company reported only one year earlier. Not only that, the revenue generated by the company beat analysts’ expectations by $74.5 million. For the first quarter of its 2023 fiscal year, the company said to expect sales of between $1.28 billion and $1.33 billion. This would be significantly higher than the $877.1 million generated in the first quarter of 2022. Beyond that, management has not provided much in the way of guidance moving forward.

On the bottom line, the business generated earnings per share of $1.35. That was $0.29 per share higher than what analysts expected. On an adjusted basis, the $1.41 per share that the company reported came in $0.20 per share higher than what was expected. In absolute dollar terms, net income totaled $427.1 million for the final quarter of 2022. This stacks up nicely against the $239.3 million in profits the company achieved in the final quarter of 2021. Other profitability metrics were largely in sync with this. The one exception was operating cash flow, which actually plunged from $225.3 million to $40.5 million. On an adjusted basis, however, it rose from $211.9 million to $408.8 million. Meanwhile, EBITDA for the company expanded from $278.3 million to $486.5 million.

Author – SEC EDGAR Data

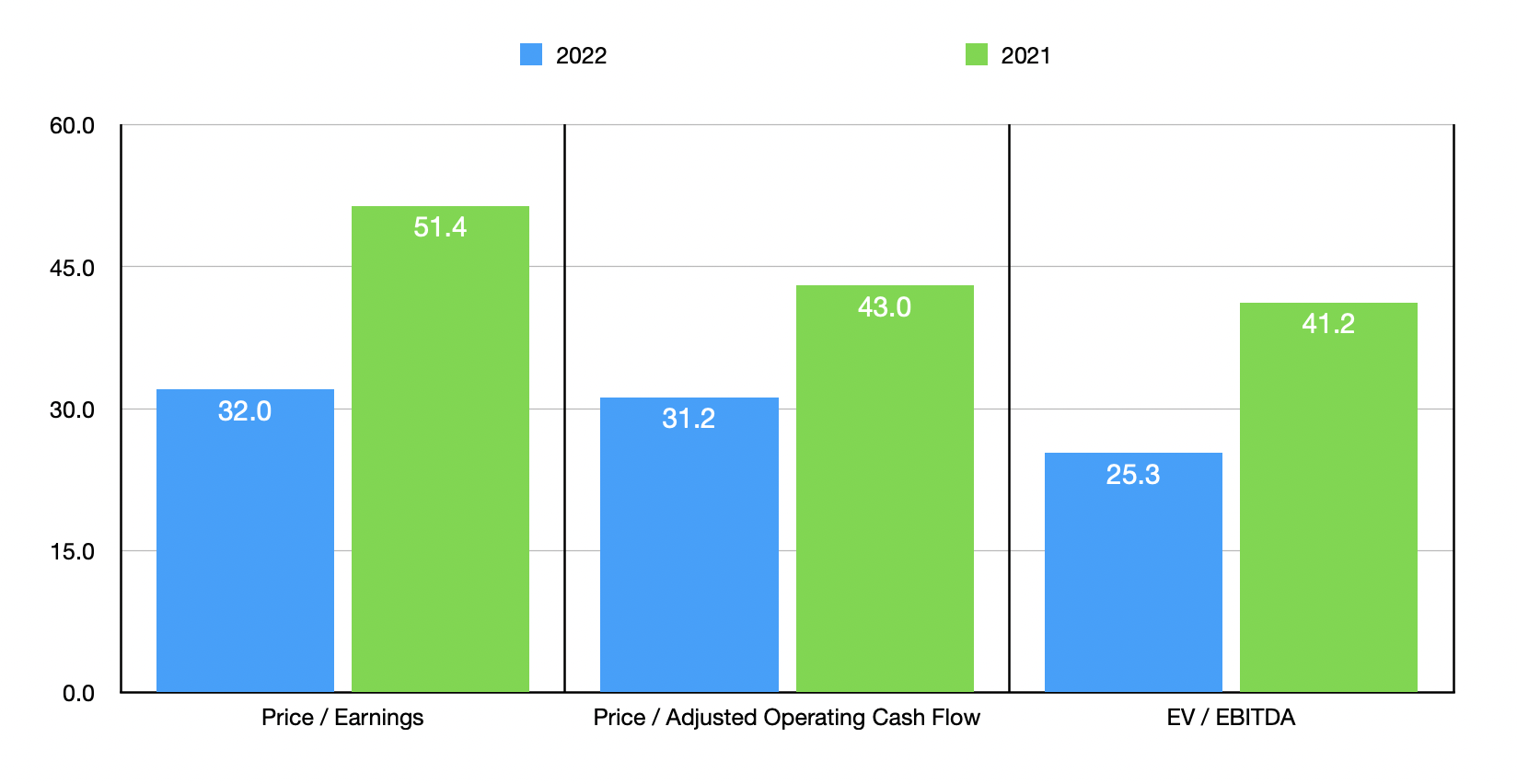

Based on the data that we have at our disposal, shares of Arista Networks are trading at a price-to-earnings multiple of 32. The price to adjusted operating cash flow multiple should be 31.2, while the EV to EBITDA multiple is 25.3. This last multiple is aided by the fact that the company has no debt on hand and enjoys $3.02 billion in cash and cash equivalents on its books. By comparison, if we were to use data from the 2021 fiscal year, these multiples would be 51.4, 43, and 41.2, respectively. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 21.8 to a high of 49. Using the price to operating cash flow approach, the range would be from 17.5 to 100 8.9. In both of these cases, two of the five companies were cheaper than Arista Networks. Meanwhile, using the EV to EBITDA approach, the range was from 13.1 to 38.9. In this case, four of the five companies were cheaper than our target.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Arista Networks | 32.0 | 31.2 | 25.3 |

| Motorola Solutions (MSI) | 34.1 | 25.5 | 22.9 |

| Ubiquiti (UI) | 48.8 | 96.5 | 38.9 |

| Juniper Networks (JNPR) | 21.8 | 105.9 | 13.1 |

| F5 Inc (FFIV) | 29.6 | 17.5 | 16.3 |

| Ciena Corp (CIEN) | 49.0 | 73.2 | 19.6 |

Takeaway

Based on the firm’s historical performance, as well as recent robust financial performance, I do believe that we are dealing with a very high-quality operation that will certainly continue to grow in the long run. For those with a long-term investment horizon, upside potential will likely exist. Having said that, shares of the company do look rather pricey on an absolute basis, while being more or less fairly valued compared to similar firms. Because of this, I feel as though a ‘hold’ rating is appropriate at this time. But in the event that the stock gets cheaper or if bottom line performance starts coming in quite strong in such that the stock starts to look cheaper, I could see this turning into a soft ‘buy’. After all, I don’t mind paying a premium for a high-quality business. But I don’t exactly like paying as much of a premium as what the market is demanding at this time.

Be the first to comment