Uwe Moser/iStock via Getty Images

Introduction

Aris Water Solutions (NYSE:ARIS) is a water services company with decent potential for value as it helps the oil industry become more environmentally sustainable. However, it has questionable metrics and a near-term bump in the row that would merit waiting for a good dip to buy the company in.

Company Profile

Aris Water Solutions provides water-related services for oil companies. More specifically, they provide the pipelines and facilities that allows for the processing of extracted water from oil wells and the recycling of water used in oil drilling. They are located specifically in the Permian basin, which is in the southeastern corner of New Mexico and part of Texas.

The company, according to their 10-K filing, came out of what seems to be a company split as part of their entire corporate restructuring. Here’s a diagram they show in their filing:

Aris Legacy Owners Corporate Structure Change (Aris Water Solutions)

It’s a little blurry due to the low resolution in the filings, but the legacy owners, which are the owners prior to the split and IPO, had their holdings split up between two new corporate entities, one a public holding company that holds the other company, Solaris Midstream Holdings.

There is also a sister company called Solaris Oilfield Infrastructure (SOI) that went public independently much earlier in 2017. It seems that historically Solaris itself split its own separate businesses and now what can be assumed as their water treatment segment (as in basic words it’s what it can be called) is trading as a public company since 2021.

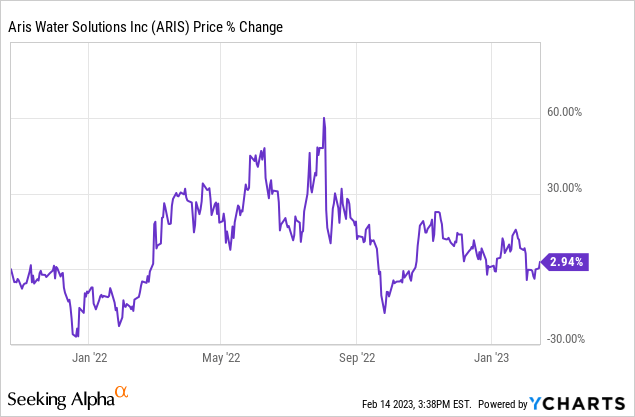

My first thoughts here are more of surprise. October 2021 was prior to the final rally of the bull market before 2022 poured cold ice on the rally big time, and the fact that as of writing Aris had sustained its price really well shows that it has performed decently since its IPO.

This is a double-edged sword for investors considering that we all can invest in Aris near the IPO price and have decent value for it, but it’s also somewhat bad too because there was a lack of sustained price appreciation, with ARIS topping at a 60% appreciation relative to their IPO price.

Investment Thesis

I somewhat like this company. The business model is rather interesting and I haven’t seen it much on the market. It takes part of the oil industry but Aris is a company that helps other companies further their Environmental, Social and Governance (‘ESG’) goals.

I also like that their business has two sources of revenue, which are demonstrated in the diagram the company shares with investors in their 10-K filing.

Aris’s Water Management Cycle (Aris Water Solutions)

The best part of this is that it looks to be a complete cycle that repeats itself, as the recycled water can be used for fracking (or drilling), which might as well also result in needing that water to be recollected and recycled over again for it to be usable for the same purposes.

It theoretically should allow for Aris to have a sustainable revenue stream where they operate thanks to the increasing need for alternative sources of water and outsourcing that water management to more specialized corporations like Aris. It was brought up in their 10-K filing, as quoted:

We believe they will increasingly outsource water management to integrated produced water infrastructure and recycling companies like us to manage their water-related needs in a cost and capital effective manner, creating new business development and acquisition opportunities for us

I would, however, caution against investing for the dividend, though, as will be discussed below. In short, however, their GAAP earnings are not conducive of a sustainable dividend.

However, I believe that this could be a worthwhile buy when this company dips. It isn’t too risky to invest at this price, but later on I’ll explain why this company may be better bought at less.

However, because the business model is sustainable and relies on further ESG optimization, I can see this company growing further into the future.

Oddities

Ever heard of a Tax Receivable Agreement (‘TRA’)? I haven’t. It’s the first time I hear of it and have to wonder if it affects the company any way.

To begin, using both the 10-K filing and this brochure I found while googling for more information on these agreements, I think I can understand what these agreements are and how they could affect the company.

TRAs usually happen when a company goes public. They are a mechanism for pre-IPO owners to extract value from the company without necessarily affecting the company’s value. The mechanism allows for those original owners to receive (usually) 85% of the tax savings accrued by the company in a given year. The terms may vary depending on the tax deductions targeted. Since Aris barely makes a loss and is very asset heavy, it is fair to assume that the target deductions are going to be from amortization and depreciation.

Looking closely at the terms disclosed in the 10-K, it also seems that these TRAs accrue as the original owners convert their Solaris LLC units into class A shares of Aris Water Solutions. Currently, there is a total TRA liability of $80 million.

The conditions of these TRA would only pose a danger to the company should the company willingly terminate the agreement or break their terms. If the company were to do so, they would be forced to pay around $200 million in lump-sum based on the 10-K and adjusted slightly in the absence of a newer 10-K updating this information.

Currently, Aris Water Solutions is very heavy on plant assets, which are somewhat hard to liquidate.

Aris Water Solutions

Aris would be better keeping the liability and the agreement as they are not prepared to handle a large lump-sum payment such as this without liquidating assets or incurring in debt.

I’m not the most informed and I don’t expect to instantly understand the mechanics of this, but this is what I can understand about this. The TRAs seem more like a remote danger than what I originally thought (which was an agreement to pay a certain amount that they disclosed every year, such as the $76 million I thought they would pay in the first million and later on).

This would, though, make my stance less bullish as getting rid of the TRA, if it actually weighed significantly on earnings, would have helped a lot with them, but I cannot really put any weighting on valuations or future on this liability.

Dividend and Earnings

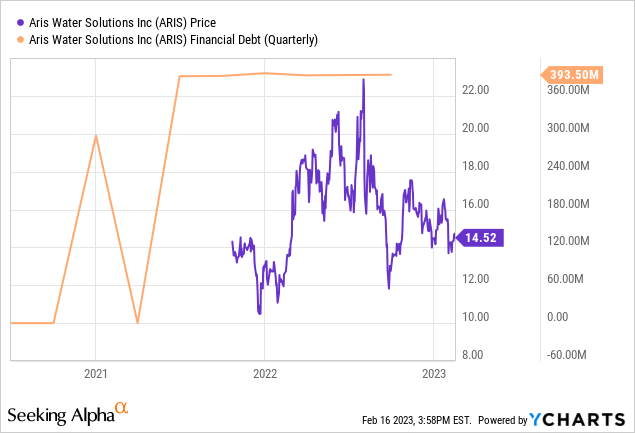

I have mixed feelings looking at the balance sheet and income statement. One the one hand, the business is bringing in money because a lot of their lack of GAAP earnings can be attributed to interest expense and depreciation, amortization and accretion. These are mostly factors that might or might not affect the company’s cash flow depending on how it’s executed.

Interest is accrued over time and paid for in certain periods. It’s possible to account for interest in each period as part of the debt they’re paying off, but the gentle increase of their long-term debt recently says otherwise.

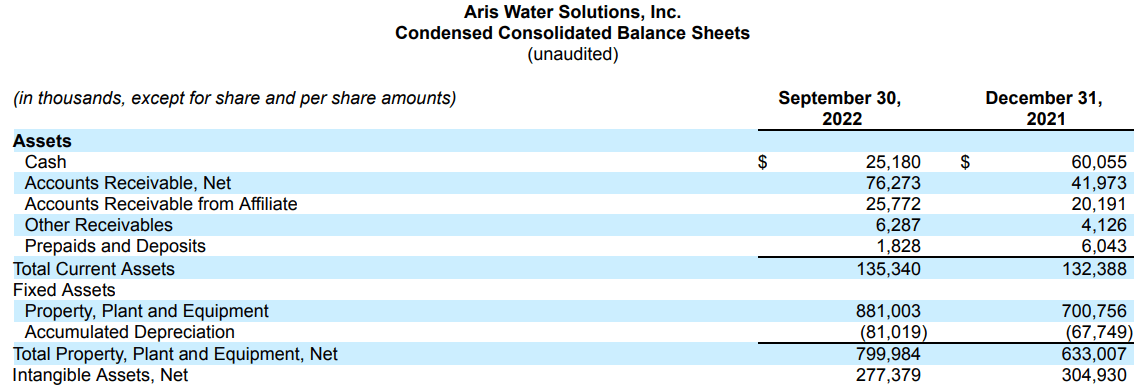

This is further reinforced when comparing the numbers provided in their 10-K consolidated financial statements.

First, the liabilities sheet:

Aris Water Solutions

To emphasize, in 2020, they had exactly $297 million logged in debt. If we look at their cash flow statement, we can see that this debt was from their credit facility.

Aris Water Solutions

We can also see that they paid their debt with longer-term senior notes, which accrue interest over time. This is a “kicking the can down the road” move done by a company overwhelmed by expenses.

As it’s important to see, their credit facility did not accrue as much interest in 2019 as their debt could be estimated to be worth $45 million based on these numbers (calculated by the known repayment of credit facility in 2019 worth $25 million and the excess of the repaid credit facility that was not listed in their balance sheet, which is $20 million). However, it seems that their credit facility did not give them enough runway to make it into GAAP profitability, or at least bringing enough money to repay that debt fair and square, which may justify moving that debt onto senior notes.

What’s very clear is that these senior notes accrued interest at a significantly higher rate as seen in their 231% increase year over year in interest expenses.

Aris Water Solutions

Another clue that can give us the nature of the note and interest expense is in newer 10-Qs (Q1, Q2 and Q3 of 2022). When looking at their financing activities listed in their cash flow statements, it seems they’ve been relatively quiet there. The only thing that is listed are dividend payments.

Now, I will be honest, I like myself a good dividend. But I feel that the dividend is proving to be a considerable weight if we look at how the net payment has been growing over time.

| Q1 2022 | Q2 2022 | Q3 2022 |

| $8.86M | $13.86M | $19.16M |

Have cash flows managed to hold up against this dividend? Let’s see. Before proceeding, I will note the equation for cash flows:

Operating income – taxes accrued – cash used in investing activities

This operating income will ignore depreciation and amortization.

| Q1 2022 | Q2 2022 | Q3 2022 | |

|

Revenue |

$70.97M | $76.39M | $90.78M |

|

Cost of Revenue |

$43.25M | $46.98M | $60.83M |

|

Less: Depreciation, Amortization and Depletion |

$16.58M | $16.2M | $16.94M |

|

Operating Expenses |

$27.39M | $17.58M | $20.94M |

|

Operating Income |

$16.91M | $28.03M | $25.95M |

|

Less: Tax Expense |

-$840k | $472k | $287k |

|

Cash Used in Investing Activities |

$9.81M | $38.51M | $44.58M |

|

Free Cash Flow |

$7.94M | -$10.95M | -$18.92M |

If we were to say just the operating income counts in this equation, there wouldn’t be any problems, but when looking at free cash flow, it seems that our dividends are being paid out of thin air. Sure, they can just not spend on the property, plant and equipment they need to operate, but if the idea is to grow, investing in the company is certainly the way to go.

The way the company is paying their dividends is the equivalent of playing with fireworks. It looks pretty up close but when the time is up, the explosions will simply lead to a third degree burn.

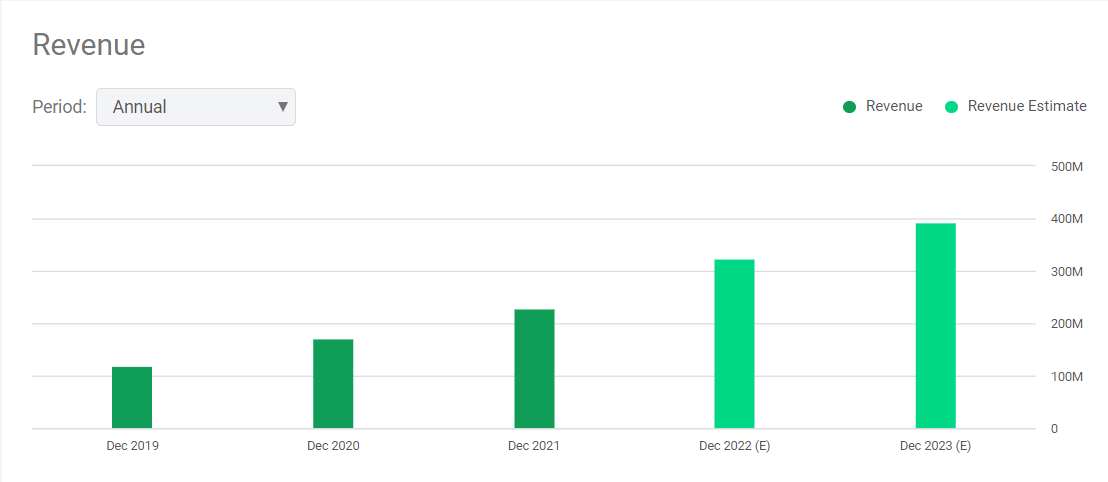

What do other analysts see in the future? For this, I’ll look at the graphs laid out in Seeking Alpha as it’s one way I can see the projections analysts have and use that as what the stock is pricing in to help understand if this dividend is sustainable, along with the business itself.

Seeking Alpha

That revenue metric sure looks enticing, if Aris were to grow all the way to $400M in revenue, this stock would be fairly priced with the potential this has.

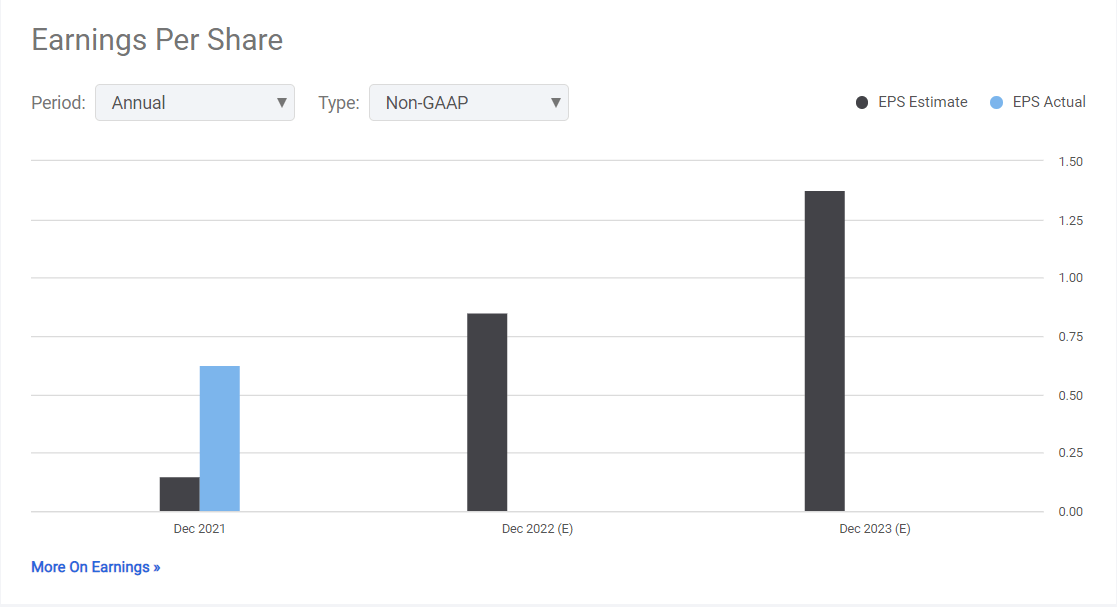

Seeking Alpha

Then, looking at their non-GAAP EPS estimates, one can feel in good comfort that things will go smoothly, right? Well, that is until Aris provided a warning for their results.

The only detail they provided was that their EBITDA (earnings before interest, taxes, depreciation and amortization) would be around $36 million this quarter, and $149 million for the year. This is lower than the midpoint of $40 million EBITDA they forecasted last quarter, which was already a decreased forecast compared to the quarter prior, as said in their Q3 earnings call.

The main reason for this can be attributed to winter seasonality. Winter in December was particularly chilly in the Permian basin and caused changes in their customer’s usual operations. This was a domino effect that can highlight one of the risks to their operations.

The headline also reads inflation, but they do have contracts that adjust for inflation, as Amanda Brock stated in their Q3 earnings call:

“We will also see the benefit of our CPI-linked revenue escalation clauses in our contracts as they hit annual reset dates in the first half of next year.”

Inflation was not even mentioned in the news article, so it really can’t be taken as a driver of their decline. Strangely enough, the stock was bought back somewhat the same day the news came out.

1-Day Chart – Recent Moves (Yahoo! Finance)

The stock is not back from where it was before the announcement, but I think a real 11% decline was merited here.

Valuation

With all this in mind, how should the stock be valued? If we use EBITDA valuation for what’s expected for the full year ($149 million), the stock is trading at 2.5x EBITDA valuation as of the close of February 16th. If we look at their operating income (calculated at $29.57 million), it is trading around 3.7x their trailing twelve months (ttm) operating income (calculated to be around $100.46 million). If we look at their ttm free cash flow, there really is no way to calculate as Q4 2021’s free cash flow was calculated at $15.24 million, which isn’t enough to calculate for the negative free cash flow.

If we were to use their trailing twelve month non-GAAP EPS, we see Aris floating with an EPS of $0.78.

Seeking Alpha

If we use my usual 20x valuation cap, Aris would have their valuation capped at around $15.60. This isn’t much of a profit chance. I currently am not aware of any relevant competitors in the water processing space dedicated to oil companies, so I don’t have any comparative metrics to know what a fair EBITDA is. Their current equity attributable to stockholders as of Q3 2022 is $276.3 million and their ttm revenues are $304 million.

With a market cap of $380 million approximately, Aris Water Solutions boasts a rather modest valuation with some slight upside potential. Their implied shares outstanding as of Q3 2022 is around 30.81 million, multiplied with the valuation cap of $15.60 would provide an estimated $480 million in market cap.

To be modest, I would place a price target of $15.50, which is slightly below the valuation cap and provides some more wiggle room. It is partially backed by Aris’s revenues and equity position and would imply a 7.1% premium to February 16th’s closing price.

Not much incentive here to buy, if I’m honest. I do foresee valuations increasing over time, but for the nearer term, I can’t exactly justify buying above this point. The materializing near-term risks to the expected revenues of nearly $400 million and 2023 non-GAAP EPS of $1.38 make it a little hard to see pricing in valuations that expect that.

Conclusion

Aris Water Solutions is a decent company with potential. Currently, the balance sheet is not spectacular, their cash flows are questionable at best, their GAAP net income is borderline non-existent, but their growth is currently great with a speed bump in the near term.

If any major dip happens, this company is worth buying as it helps the oil industry become more sustainable. However, later on, it’s worth researching how the switch to renewables and electric would affect this company in the long term.

For now, I rate Aris Water Solutions a Hold with a price target of $15.50.

Be the first to comment