LUMIKK555/iStock via Getty Images

2022 is likely a year that many investors can’t wait to put in the rear-view mirror. This is reflected by the year-end selling without even a Santa Claus rally this month, and much of this may have to do with tax loss harvesting. While some economists are predicting a recession next year, most think that it will be a mild one, if any, and that the second half of next year should see a rebound.

The market, however, is forward looking, and if one waits for an official recession, then it may be too late to buy. That’s why it may be a good idea to buy into value priced high yielding stocks that pay you for waiting.

This brings me to Ares Capital (NASDAQ:ARCC), which currently yields over 10%, which is more than 6x that of the S&P 500 (SPY). This article highlights why ARCC is attractively priced for income investors seeking high yield to start the new year.

Why ARCC?

Ares Capital is the largest BDC by asset size and is externally managed by the well-respected Ares Management (ARES), a leading alternative asset manager that operates in the credit, real estate, and private equity spaces.

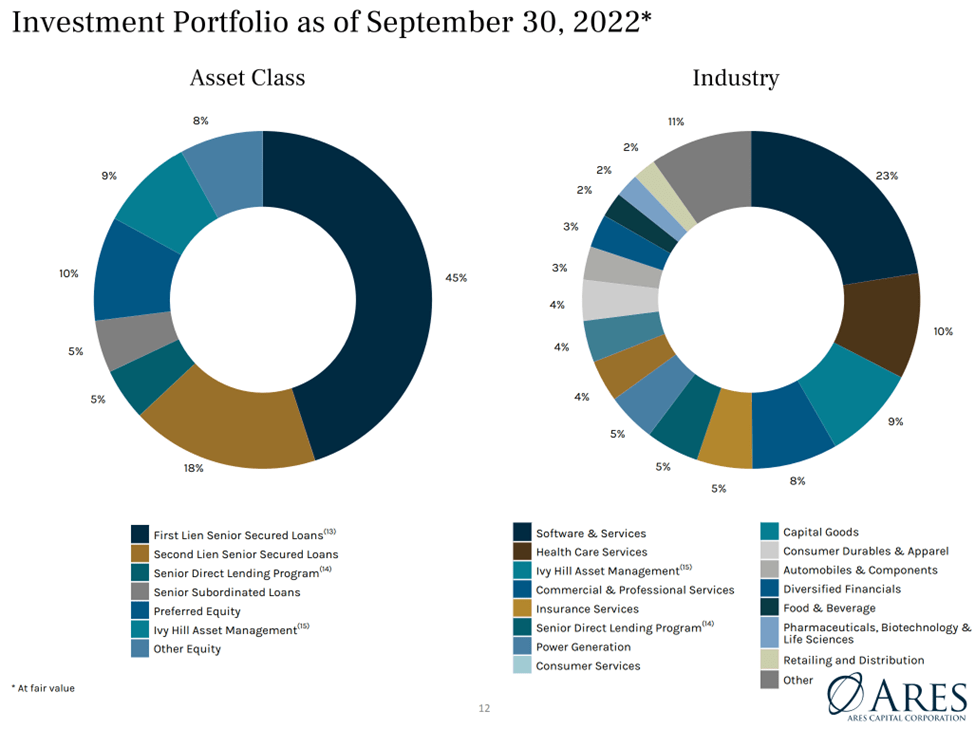

ARCC was one of the few BDCs to opportunistically grow its portfolio size during the 2020 pandemic year. Its portfolio has continued to grow over the past year, by 21% to $21 billion at fair value, and the number of portfolio companies has grown by 23% to 458. As shown below, ARCC’s portfolio is primarily allocated towards secured loans, and the portfolio is well diversified across segments that are generally defensive in nature.

ARCC Portfolio Mix (Investor Presentation)

Importantly, ARCC’s net asset value per share has remained relatively stable over the past year, increasing by $0.04 YoY to $18.56, with ups and down in between due to widening credit spreads amidst a higher interest rate environment. Speaking of which, ARCC is benefitting from a rising rate environment due to its 73% exposure to floating rate loans as a percentage of its portfolio fair value. This resulted in weighted average yield on debt rising by 180 basis points YoY to 10.7%.

Meanwhile, the portfolio remains overall healthy, with a nonaccrual that’s held steady in recent quarters at 1.6% of portfolio cost, sitting well below ARCC’s 10-year average of 2.5%. ARCC is also modestly leveraged with a debt to equity ratio of 1.27x, sitting well below the 2.0x statutory limit. I would expect the leverage ratio to improve in the upcoming Q4 release, as ARCC did an equity raise in November, issuing 8 million shares at around $19.73, equating to around $158 million in cash proceeds.

Risks to ARCC include a general economic slowdown, which could impact its borrowers. However, ARCC’s diversification and prudent underwriting standards have helped it to weather previous recessions, and this is not the experienced management team’s first rodeo. Moreover, a slowdown in the economy also reduces competition from traditional financing sources, putting ARCC in a solid position to capitalize, as management highlighted during the recent conference call:

Economic data continues to present a mixed picture as corporate fundamentals remain solid, yet the consensus outlook seems to point to demand softening and an overall slowdown in the U.S. economy. The credit markets and the leveraged finance markets, in particular, are exhibiting weak secondary liquidity and slowing new issuance. These trends and the lack of competition from traditional sources has made it a much more lender-friendly market and we are taking this opportunity to improve the strength of the existing portfolio and to price new transactions more attractively.

As our shareholders know, we’ve operated the company well through periods of volatility over the past 18 years. We’re taking the same approach today as we have in the past, focus on portfolio management and risk mitigation, while becoming incrementally more selective on new deals. We believe we can use the current market conditions to improve situations in our portfolio and also to finance larger companies that would otherwise turn to the liquid markets in less uncertain times.

Notably, management recently raised the regular quarterly dividend substantially, by 11.6% to $0.48, and it’s well-covered by $0.57 NII per share generated during the third quarter. Lastly, I see value in ARCC at the current price of $18.70, equating to price to NAV ratio of just 1.01x. As shown below, ARCC has generally traded at a premium to NAV over the past 3 years, up to a 20% premium as recently as March.

ARCC Price to Book (Seeking Alpha)

Investor Takeaway

ARCC benefits from its growing scale and has weathered economic headwinds before. Its portfolio composition is defensive in nature, with the majority invested in secured loans, and its dividend is well covered by net investment income. The portfolio is also overall healthy, and benefits from a rising rate environment. ARCC is now attractively priced with its price very close to NAV, presenting investors with a high-yielding opportunity to start the new year.

Be the first to comment