wellesenterprises/iStock Editorial via Getty Images

Archer Daniels Midland (NYSE:ADM) reported stellar results in Q1 2022 with net earnings soaring 53% YoY to USD 1.05 billion. Revenues rose 25% YoY to USD 23.65 billion. The momentum is a continuation from last year when net income jumped 53% YoY to USD 2.7 billion and revenues rose 32% YoY to USD 85.25 billion for the full year ended December 2021. ADM’s Q1 2022 performance was driven in part by an environment of tight supply and robust demand which pushed up commodity prices and in turn helped push up grain merchandising profits.

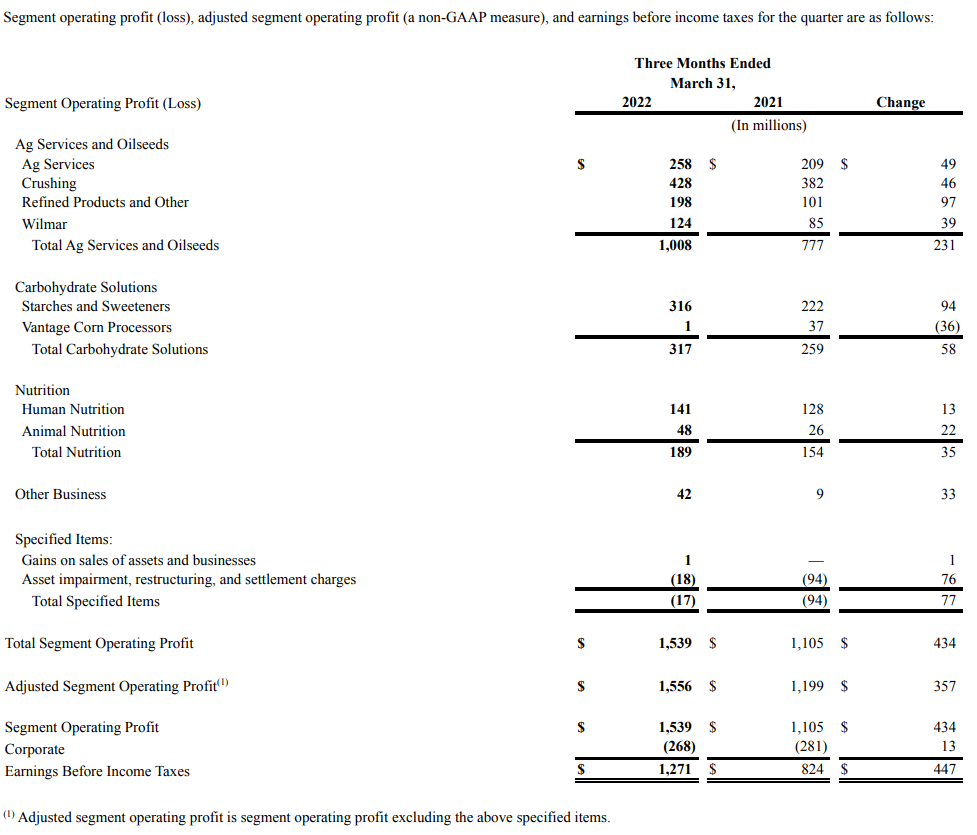

Profit growth was led by ADM’s core ‘Ag Services and Oilseeds’ segment (which is involved in selling, transporting and processing agricultural commodities and related trade finance activities), its biggest segment accounting for 65% of profits before taxes and 77% of revenues (as of Q1 2022); the segment’s profits rose to USD 1.008 billion during the quarter, up 30% YoY, driven by a tight demand-supply environment, primarily due to a short South American crop. Robust protein and vegetable oil demand helped crushing margins with the Crushing subsegment posting profits of USD 428 million, up 12% YoY. Strong biodiesel margins in Europe, Middle East & Africa (EMEA) along with good demand for refined oils in North America helped the ‘Refined Products and Other’ segment post a 96% YoY increase in profits to USD 198 million.

ADM’s ‘Carbohydrate Solutions’ segment (ADM’s second largest segment accounting for 21% of profits before taxes and 14% of revenues and in Q1 2022), reported profits of USD 317 million up 22% YoY. The Carbohydrate Solutions segment, which includes its ethanol business, is involved in processing corn and wheat into ingredients such as starches and sweeteners. Broken down, the ‘Starches and Sweeteners’ subsegment, which includes ADM’s ethanol production from wet mills, delivered profits of USD 316 million during the quarter, up 42% YoY. The ‘Vantage Corn Processors’ subsegment, which includes ADM’s dry mills, reported profits of USD 1 million, down from USD 37 million in the same quarter last year. ADM noted that while the ‘Vantage Corn Processors’ delivered solid execution margins during the quarter, the subsegment’s profit decline was attributed to position losses on ethanol inventory as prices fell early in the quarter, as well as the divestment of its Peoria facility which had benefited from strong demand for USP-grade industrial alcohol in Q1 2021.

ADM’s ‘Nutrition’ segment (which accounts for 12% of profits before taxes and 8% of revenues), reported profits of USD 189 million, up 23% YoY. ‘Animal Nutrition’ led the way in terms of profit growth with profits nearly doubling to USD 48 million driven by demand strength in amino acids. The ‘Human Nutrition’ subsegment reported profit growth of 10% YoY to USD 141 million, helped by strong sales growth from flavors. Alternative proteins (which benefited from the Sojaprotein acquisition last year) helped drive the ‘Specialty Ingredients’ subsegment, while strong sales for fiber, probiotics and the acquisition of Deerland Probiotics and Enzymes last year helped drive ‘Health and Wellness’ sales. ADM’s Nutrition segment sells flavor and nutrition-related ingredients (such as plant-based proteins, natural flavors and colors, emulsifiers, soluble fiber, polyols hydrocolloids, probiotics, prebiotics, enzymes, botanical extracts, formula feeds, animal health and nutrition products).

ADM Q1 2022 10-Q

Near term tailwinds from tight agri-commodity supplies, robust demand, ethanol recovery

The tight demand-supply environment is expected to persist in the near term. Factors impacting agricultural commodity supplies including the conflict between Russia and Ukraine (a major grain-producing region with both countries being major producers of wheat and corn), and sanctions on Russia (who in addition to grain, is a major producer of gas, and for years the world’s largest producer of fertilizer) are generally expected to remain this year suggesting a continuation of tight supply conditions while food demand is generally expected to remain robust. American fertilizer giant Mosaic (MOS) expects global demand for grain and oilseeds to remain high in 2022 while stock-to-use ratios remain at the lowest point in more than a decade.

ADM paints a similar forecast with the company expecting tight supply conditions to continue over the next few years (until at least 2024) driven by short South American crops, weak Canadian canola crop, and disruptions in the Black Sea region. The sentiment echoes rivals like Bunge who also expect robust food demand and tight crop supplies to continue to persist thereby driving another year of strong results. The tight supply and robust demand environment is expected to help ADM deliver another year of strong results in 2022. Meanwhile, the crush margin environment is also expected to remain strong as vegetable oil demand recovers underpinned by rising demand for renewable fuel as economies reopen. ADM is increasing 2022 capex to about USD 1.3 billion to fund expansion projects, including soy crushing capacity expansion projects to capitalize on strong crush margins.

Ethanol demand, which plunged during the pandemic, is returning to pre-pandemic levels driven by a normalization of gasoline demand and a move by the White House last month to increase the ethanol blending mandate to counter rising fuel costs, which should help support strong results for ADM’s Carbohydrate Solutions segment.

Alternative protein to support mid-term growth

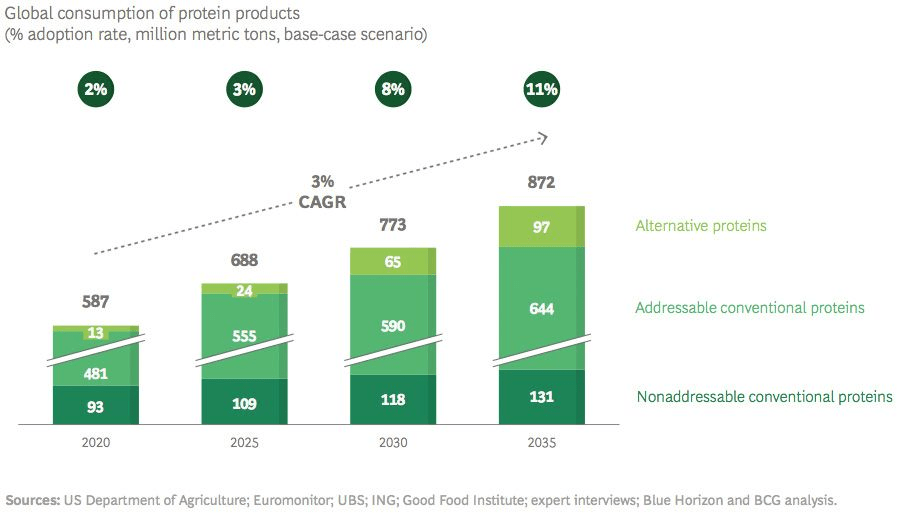

ADM’s ‘Nutrition’ segment has benefited from rising demand for alternative proteins (the segment reported operating profits of USD 691 million in FY 2021, up 20% YoY) and there is ample potential for further growth in the medium term. Research figures estimate plant-based protein adoption is set to increase from about 2% in 2020 to 11% by 2035, with consumption of alternative proteins expected to reach 97 million tons by then, up from 13 million tons in 2020, a seven-fold increase.

Consultancy.eu

ADM, which has a vast portfolio of alternative protein ingredients from numerous plant-based sources is positioned to capitalize on the opportunity, and the company continues to expand its portfolio and capabilities through acquisitions and innovation as part of the company’s growth strategy. In April 2022, ADM announced a USD 300 million investment into its alternative protein production facility in Decatur, Illinois, to capitalize on growing demand for alternative proteins. The facility, expected to be complete by 2025, comes after ADM acquired Serbian non-GMO soybean protein ingredients supplier Sojaprotein in July last year, and invested USD 32 million into Air Protein in January last year. ADM has also struck partnerships to bolster its plant-protein presence; ADM tied up with Brazilian beef and hamburger patty company Marfrig to create a plant-based JV – PlantPlus Foods – and struck a partnership with Asia Sustainable Foods (a company owned by Singaporean sovereign wealth fund Temasek) to create a JV that would specialize in developing microbial -based proteins aimed at creating alternatives to meat and dairy protein. Meanwhile organic innovation efforts have seen ADM establish protein innovation labs in Singapore, and in Decatur, Illinois.

Financials

Limited operations in Ukraine and Russia

ADM has limited operations in Ukraine (the company operates a crushing plant, a grain port terminal and trading office in the country and has about 650 employees), and almost no operations in Russia. Ukrainian operations have been scaled down/idled since the Russia-Ukraine conflict in February 2022, resulting in an immaterial impairment charge in Q1 2022.

Improving profitability

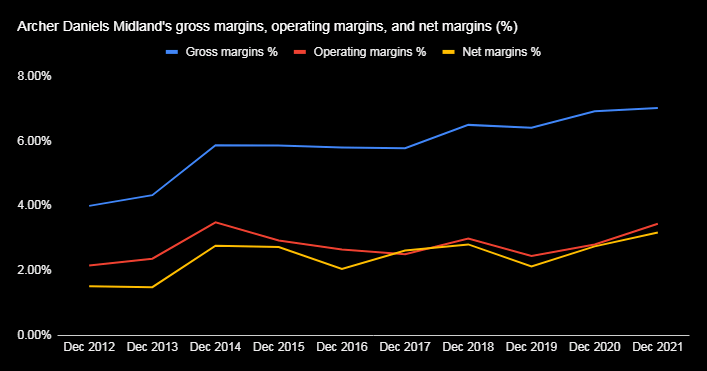

Strategic initiatives including efforts to cut costs, streamline assets, and shift towards higher-value businesses such as flavors over the past several years have been generating results with ADM’s profitability metrics showing a consistent increase. Gross margins, operating margins, and net margins have moved upwards over the past several years.

Author

ADM has been actively making strategic acquisitions lately (such as South African flavor distributor Comban in February 2022, Latin American flavor company FISA in December 2021, pet treats and supplements company PedigreeOvens, PetDine, The pound Bakery, and NaturaDine in September 2021, Sojaprotein in July 2021), and ADM is expected to remain on the hunt for acquisition opportunities. ADM has noted that M&A, along with organic growth initiatives, will remain as one of its innovation pillars. A decent debt position supports this strategy. ADM is comparable to smaller rival Bunge (BG) in terms of profitability but is superior in terms of leverage.

|

Gross margin % |

7.04% |

5.84% |

|

Net margin % |

3.42% |

3.12% |

|

Return on assets % |

3.45% |

5.65% |

|

Long term debt / equity |

58.68 |

81.4 |

Summary

Agricultural commodity traders such as ADM, Bunge, Cargill, and Louis Dreyfus tend to thrive during times of crisis when agricultural commodity supplies tend to fall short of demand. This tight commodity supply environment is expected to persist in 2022 (possibly longer). Meanwhile demand for soybean oil and soybean meal for renewable diesel and sustainable aviation fuel and from the livestock feed industry is expected to remain strong as well, which could support crush margins. These factors suggest another year of strong profits and wide margins for ADM’s core Ag Services and Oilseeds segment while the Carbohydrate Solutions segment should continue seeing positive momentum partly driven by U.S. gasoline demand normalizing to pre-pandemic levels. ADM’s Nutrition segment is benefiting from growing demand for alternative proteins, and this segment offers good growth prospects in the medium term.

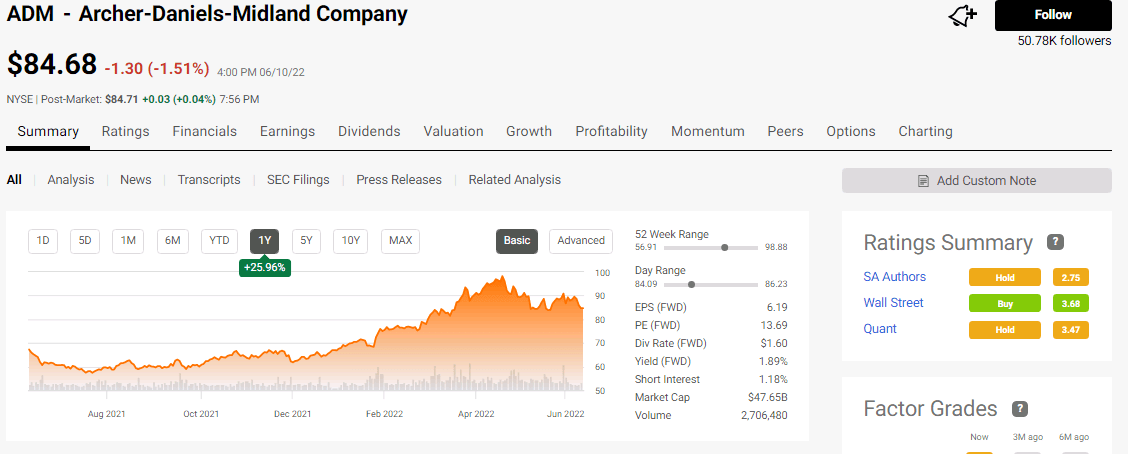

ADM’s stock is already up 25% over the past year and anticipated strong results for 2022 may already largely be baked into the stock.

Seeking Alpha

Moreover, while 2022 is expected to be another year of strong results and margins, soaring inflation could result in moderating demand beyond 2022 (particularly in emerging markets where food makes up a relatively larger proportion of incomes), which could impact profit margins, and therefore ADM’s stock price as well.

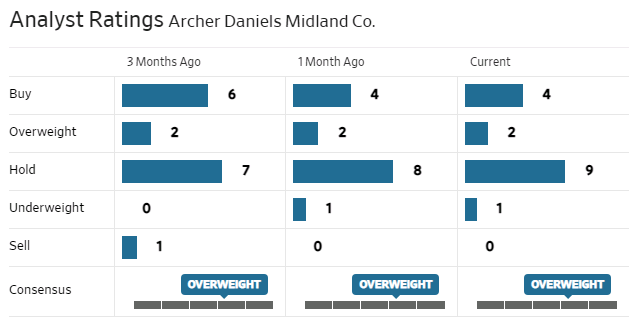

Analysts are largely neutral on the stock.

WSJ

Be the first to comment