Since putting out my cautious piece on Archer Daniels Midland (ADM), the shares are down about 12% against a loss of 5.75% on the S&P500. The relative performance of the two suggests to me that Archer Daniels Midland was indeed relatively overpriced. Now that the shares have come down in price, and now that the company has announced full year earnings, I thought I’d check in on the name to see if it now makes sense to buy. For those who missed the title of this article and can stand neither the suspense nor my writing, I’ll jump to the point. I can recommend buying at these levels. In addition, I remain comfortable with the short put trade I put on earlier, and will be entering that trade again, but with much higher premia this time. I’ll go through my thinking about this company below.

Financial Update

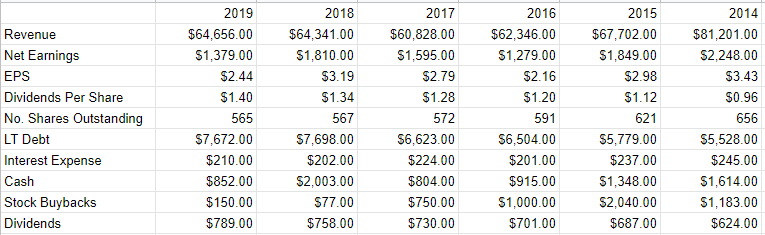

A review of the financial history here indicates that Archer Daniels Midland is hardly a growth company. Over the past six years, for example, revenue has declined at a CAGR of about 3.7%, while net earnings are down at a rate of 7.8%. The picture looks less grim when looking only at the past five years, but is still negative (revenue was 4.5% lower in 2019 than it was in 2015 and net income is fully 25% lower). An investor doesn’t buy this company for growth in my view.

Management has treated shareholders very well, in spite of this slowdown, having returned $5.2 billion to shareholders in the form of stock buybacks and just under $4.3 billion to owners in the form of ever growing dividend payments. The buyback program means that earnings per share have declined at a lower rate (CAGR of -5.5%) than net income, since shares outstanding have declined at a CAGR of about 2.5% over the past six years.

Turning briefly to the capital structure, debt levels have obviously grown dramatically over the past six years, yet interest expense has declined at a CAGR of -2.5%. Obviously the weighted average cost of the debt has declined, which is quite good for owners. In addition, the vast majority of debt (79.6%) is due after 2025, with the longest dated out to 2095. I think this suggests that there’s little worry about a credit or solvency crisis with the company anytime soon.

In my view, an investor does buy these shares for the dividend, and I should therefore spend some time writing about the dividend here, and its sustainability. Although the payout ratio remains sustainable in my view (currently at 57%), it should be noted that it’s ballooned over the past six years from about 28%. This is unsurprising in light of the fact that the business has slowed and dividends have grown. At some point, the sustainability of the dividend will come into question unless current trends reverse, but that time is not now in my view. In short, I don’t think the financials of this company are very exciting, but the dividend is safe for the foreseeable future.

{kind=link}

Source: Company filings

The Stock

I am usually a bit sheepish writing this section of the article, as it’s so repetitive, but the comment posts from my previous article suggest to me that people still need to be reminded that stock price matters a great deal. It’s possible that a great company can be a terrible investment if an investor overpays for that company. I’ll use a reductio ad absurdum example in an effort to drive the point home. Archer Daniels Midland is a wonderful business, but it’s not worth $1,000 per share, because that price far exceeds the present value of future cash this company can generate. At that price, the dividend yield is infinitesimal. The returns we make over time are largely a function of the price we pay for the stock. For example, someone who bought Archer Daniels Midland in May of 2015 is today sitting on a 25% loss. Someone who bought seven months later is sitting on a 25% gain. The price we pay really matters.

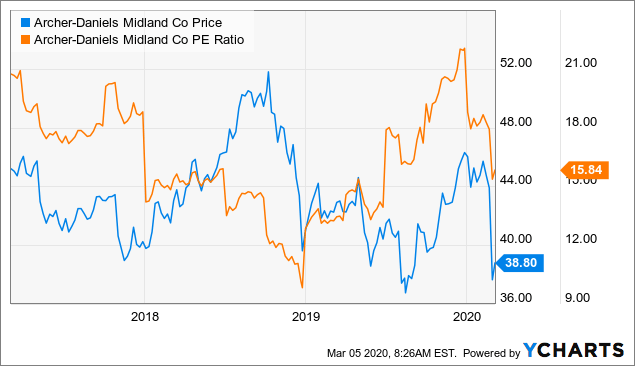

With that out of the way, I need to spend some time talking about the stock of this very well run, shareholder friendly, profitable business. In particular, I want to avoid stocks that are trading at a premium relative to the overall market, and to their own history. I do that in a few ways, ranging from the simple to the more complex. On the simple side, I look at a ratio of price to some measure of economic value. In my previous article on the name, I made much of the fact that ADM was trading on the high side of its valuation, sporting a PE of ~21. By comparison, this is a picture of their current valuation. It is compelling enough for me to buy.

Data by YCharts

Data by YCharts

Source: Ycharts

Insider Buys

I’ve said it before, and I’ll say it again. Some investors are better at this than the rest of us. Some are emotionally and intellectually more well equipped. Some have legions of analysts at their disposal. Finally, some who work at the business, live and breathe it, know it better than any Wall Street analyst ever will. Since January 1, 2019, three members of this last group (Donald Felsinger, Juan Luciano, and Ray Young) have purchased 98,514 shares between them at an average price of $40.05. In my view, when people who know a business better than anyone else put their own capital to work in it, we outsiders should at least take note of it. Also, insider buys are important indicators in my view, but not all buys are created equal. These people were obviously willing to buy at $40. We know nothing about how they felt about the shares when they were trading 12.5% higher than that figure, as there were no buys at that level (i.e. the price on the day of publication of my last article on ADM).

Options Update

In my previous article on the company, I recommended selling the January 2021 ADM puts with a strike of $35. I recommended this strategy because I think investors would do well over time if they can buy this business at that price. At the time, these were bid-asked at $.95-$1.08. They are currently bid-asked at $2.30-$2.68, so they are in a “loss” position. In my view, this is not problematic because the company is still an excellent buy at $35 per share.

For those who are new to the trade, I think selling these puts still makes sense, and the only difference now is that the investor will enjoy higher premia than I did for taking on this obligation. To put this trade in perspective, if the shares rally from these levels, the investor simply pockets the premium. If the shares drop below $35, the investor will be obliged to buy this great business at a price that represents a dividend yield just over 4%. In my view, this is a win-win trade, and for my part I’ll be doubling down and selling more of this strike and duration.

Conclusion

In my view, Archer Daniels Midland is a fine company that treats shareholders very well. I think the dividend is sustainable, at least for the moment, and for my part I wouldn’t mind if at some future date the company loses its status as an “aristocrat.” Apart from the fact that I’m a committed republican who dislikes such titles, I care about whether a dividend is sustainable. Management treats shareholders very well, and I think the business is obviously of critical importance to the world economy. Finally, when insiders buy at average prices below current market prices, that is a great sign in my view. The options trade I recommended earlier remains a “win-win” in my estimation, and for that reason, I’ll be doubling down over the next few days. I’ll also be buying shares for the same reason I eschewed them previously. They are now (finally) trading near the low end of their historical valuations.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in ADM over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: In addition to buying shares, I’ll be selling more of the short puts that I referenced in both my previous article, and this one.

Be the first to comment