sankai/iStock via Getty Images

Investment Thesis

Arch Resources (NYSE:ARCH) is a high-paying dividend stock that hasn’t gone anywhere fast. In fact, ever since I recommended it, despite promising fundamentals, investors haven’t been all that interested in this coal miner.

The setup is very simple, 50% of its free cash flow comes back to shareholders via its dividend. The rest is either used for repurchases or capital preservation. That’s it, no need to get distracted with coking or thermal coal.

At the more nuanced level, a substantial amount of Arch’s coal is tied up to the steel industry. But that insight is starting to wither away as Arch openly discusses selling some of its coking coal into the thermal market.

There’s a lot to be bullish about here, including getting a 17% annualized dividend.

What’s Happening Right Now?

Recently news broke out that coal prices in the US reached an all-time high. For a commodity that so many investors have been skeptical about its underlying value, the reality of the situation is that coal prices are going through the roof.

ARCH’s Capital Allocation Strategy

The reason why I’m very much bullish on Arch is because of its capital allocation strategy, see below:

Arch is going to return 50% of its free cash flow to shareholders via dividends. And whatever is left is either going to buybacks or capital preservation.

Today Arch’s debt position is not a problem, given that Arch has more than $100 million of net cash.

Also, I’d already noted previously, Arch’s reclamation fund capital infusion has now been completed. And the receivable build-up of working capital is temporary in nature. Both uses of cash flows will not repeat in Q3.

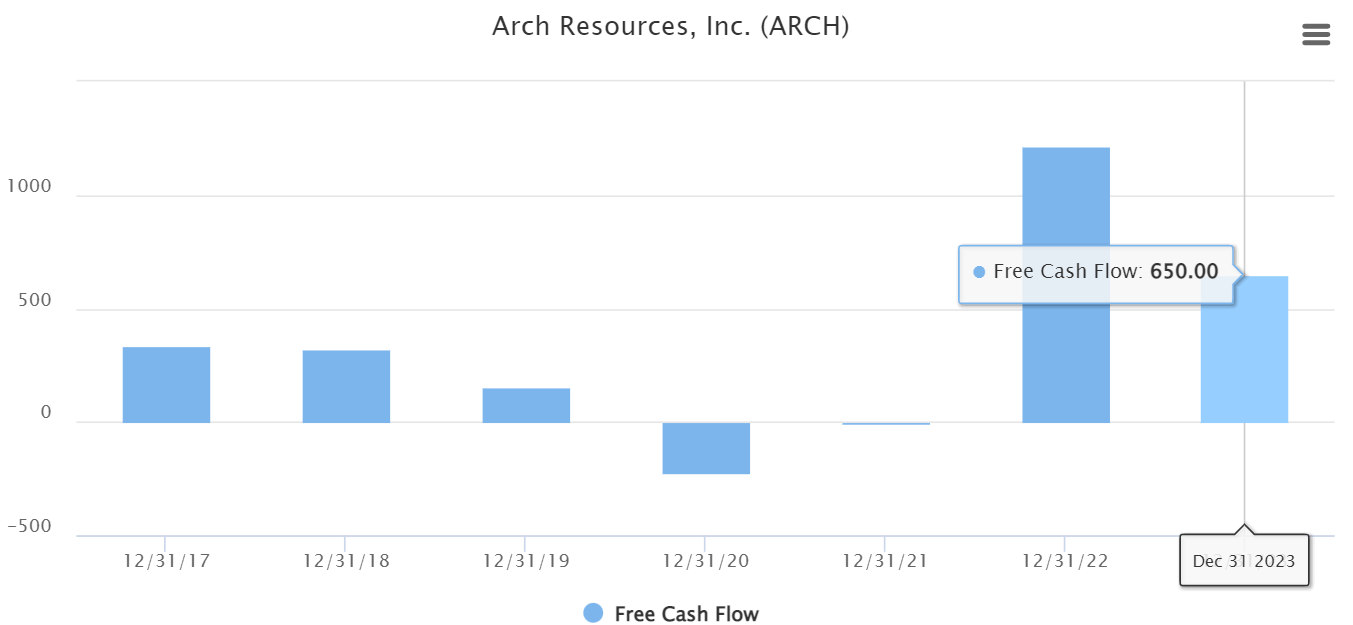

ARCH Stock Valuation — Worst Case, Investors Are Paying 4x FCF

Here’s where there’s room for some nuances. On the one hand, analysts following Arch continue to believe that Arch’s free cash flow will roll off in 2023.

TIKR.com

As I noted in a different coal stock, even if coal prices were to come down, and even if analysts were right about Arch, something that I don’t believe to be true, in that case, Arch trades for 4x next year’s free cash flow.

This is depressed free cash flow assuming that free cash flows drop in 2023.

How is that not cheap enough?

But thinking through this rationale, here’s how things stand right now. To the best of my calculations, I believe that Arch is going to return to shareholders somewhere around $6 to $8 via a variable dividend.

That means investors will get at least a 4.6% yield in the upcoming quarter. That’s close to 17% annualized. Indeed, if Arch doesn’t return more than $6 in special dividends, I’ll be astounded.

The Bottom Line

This is a very exciting time to be an investor in Arch. After everything that investors have gone through, it now appears that coal prices just reached an all-time high in the US.

Meanwhile, Arch is still trading for around 4x next year’s free cash flow. And investors are going to get close to a 17% annualized return.

The core takeaway here is this, Arch is not investing for growth! This business is simply returning capital to shareholders.

And the one thing that has been holding back Arch is that investors have come to believe that since it’s predominantly a metallurgical (coking) story, with steel prices in the bin, there would be no need for coking coal.

However, Arch’s management team declared last quarter that Arch was looking to cross-sell into the thermal market, given the wide spreads between coking prices and seaborn thermal coal prices.

There’s a lot to be bullish about here.

Be the first to comment