Tunatura

Apellis Overview – Path To Approval Of Empaveli in PNH

Apellis Pharmaceuticals (NASDAQ:APLS) raised ~$150m via its initial public offering (“IPO”) back in November 2017, issuing just over 10.7m share at a price of $14 per share. The company described itself as:

focused on the development of novel therapeutic compounds to treat disease through the inhibition of the complement system, which is an integral component of the immune system, at the level of C3, the central protein in the complement cascade.

Originally based in Kentucky, but now headquartered in Waltham, Massachusetts, Apellis’ lead candidate APL-2, or Pegcetacoplan, was approved to treat paroxysmal nocturnal hemoglobinuria (“PNH”) in patients who are either treatment-naïve, or who are switching from C5 inhibitors eculizumab or ravulizumabin in May 2021, under the brand name Empaveli.

The drug generated $45.4m of revenues across the first 9m of 2022, whilst also securing approval for the same indication in the UK, Europe, Saudi Arabia, and Australia, under the brand name Aspaveli, where its marketing and sales are handled by partner Swedish Orphan Biovitrum AB (“SOBI”).

In this market, Empaveli competes against AstraZeneca’s (AZN) Soliris, developed by Alexion Pharmaceuticals which the Anglo / Swedish Pharma acquired in 2021 in a ~$13bn deal. Soliris earned revenues of ~$2.92bn in the first 9m of 2022, although it is approved in several other indications, including Myasthenia Gravis.

The difference between these 2 drugs that both target the complement system – defined as “part of the immune system that enhances the ability of antibodies and phagocytic cells to clear microbes and damaged cells from an organism” – is that Empaveli targets the complement protein C3, whilst Soliris targets the protein C5. In its 2021 10-K submission Apellis states:

We believe that inhibition of the complement system by targeting C3 may enable a broad range of therapeutic approaches, and that pegcetacoplan has the potential to address the limitations of existing treatment options or provide a treatment option in indications where there currently are none.

To date, Apellis’ thesis is proving very sound. Empaveli was able to outperform Soliris in a head-to-head study in 2021, improving hemoglobin levels in anemic PNH patients faster than Soliris, and meeting the study’s primary endpoint, whilst also meeting a secondary endpoint after 85% of patients taking pegcetacoplan were transfusion free at Week 16, versus 15% in the Soliris arm.

PNH could eventually become a blockbuster (>$1bn sales per annum) market for Empaveli, more or less justifying Apellis’ current $5.9bn market cap valuation, and rewarding investors who bought at the IPO price with a >250% return on their investment – but things could get much better than that.

PDUFA Date For Empaveli In Geographic Atrophy Arrives Next Month

On February 26th, the FDA will announce whether it has approved Empaveli to treat the eye disease Geographic Atrophy, a late stage form of age-related macular degeneration (“AMD”).

For context, whilst Apellis estimates that “there are approximately 1,500 patients with PNH currently being treated with C5 inhibitors and another 150 patients who are expected to be newly diagnosed each year”, the company believes GA is “a disease that affects approximately one million people in the United States and five million people worldwide”.

There are no approved therapies to treat GA, therefore if approved, Empaveli will enter a market estimated to be similar in size to the “Wet” Advanced Macular Degeneration (“AMD”) market, Wet AMD being another branch of the overall AMD market. Regeneron’s Eylea, the current standard of care in Wet AMD, is set to earn >$9bn in annual revenues in 2022.

In reality, for reasons I will touch on below, Empaveli may not drive the kinds of revenues that Eylea does, but blockbuster sales in the GA indication seem virtually guaranteed should Empaveli be approved, which seems the likeliest outcome.

Apellis’ share price did fall in value by >50% in September 2021 – from >$65, to ~$30 – after the company reported data from its 2 pivotal Phase 3 studies, DERBY and OAKS, which tested Empaveli in <1,200 adults with GA secondary to age-related macular degeneration.

Whilst the OAKS study met its primary endpoint, generating significant reduction in GA lesion growth at 12 months of 22% (p=0.0003) and 16% (p=0.0052) for the monthly and bi-monthly dosing regimes respectively, the Derby study did not, generating reductions of 12% (p=0.0528) and 11% (p=0.0750) for monthly and every-other-month treatment.

The failure of DERBY opened the door for Iveric Bio (ISEE) and its Zimura therapy – a C5 complement inhibitor also indicated for GA and showing promising results – to potentially forge ahead in the race for approval, but Zimura’s pivotal trial data also left questions to be answered and the company only fully completed its New Drug Application (“NDA”) for a rolling review of Zimura in December.

As such, Apellis has a major stock price catalyst arriving in late February, and it is hard to imagine its shares doing anything but soaring if the FDA gives its approval for Empaveli in GA. At the very least, shares seem likely to recapture September 2022 highs of >$68, before the FDA opted to extend its NDA review period by 3 months, from November to February, in order to include 24-month data from the DERBY and OAKS studies.

That implies an upside opportunity of >30%, which could be just the beginning of a longer-term uptrend. Empaveli is also progressing through a Phase 3 study in the rare kidney diseases IC-MPGN and C3G, a Phase 2 study in the central nervous system condition Amyotrophic Lateral Sclerosis (“ALS”), a Phase 3 in Coronary artery disease (“CAD”), and a Phase 2 in Hematopoietic stem cell transplantation-associated thrombotic microangiopathy (HSCT-TMA).

To summarize the investment opportunity, Apellis appears to have made serene progress with pegcetacoplan – by biotech standards at least – winning approval in the rare blood disease PNH – a potential blockbuster indication – and now targeting approval in an indication in which analysts expect peak revenues can exceed $3bn.

With several other label expansion opportunities in play in markets that offer the possibility of blockbuster sales, it can certainly be argued that Apellis’ current valuation and share price are lagging its progress and undervaluing the potential of Empaveli – although there are caveats to consider.

Firstly, there is substantial single asset risk – Empaveli is a new type of drug class and unfoerseen safety issues or more missed endpoints in key trials could undermine its earning potential.

Secondly, Empaveli is being pitched into markets that may be underserved, but perhaps not for long – rival biotech and Pharma candidates could upstage the drug and leave Apellis losing the battle for market share.

Thirdly (and not necessarily finally), although reasonably well funded, with current assets of >$830m as of Q322, Apellis may struggle to compete with better funded rivals, especially if the Big Pharma industry begins to target C3.

Breaking Down The GA Study Data & Assessing The Market

In an investor presentation delivered at this months’ JP Morgan Healthcare conference, Apellis management states that it is “positioning Apellis for an extraordinary 2023”, and it is hard to disagree.

GA is – according to Apellis – “the leading cause of blindness worldwide” and a poll sponsored by the company reveals that nearly 7 in 10 patients believed the impact of GA on their independence and quality of life was worse than expected, whilst 90% of physicians surveyed indicated that they would use pergcetacoplan to treat patients.

Apellis now boasts ~100 field based employees of whom nine out of ten have retina / ophthalmology experience, and Apellis is ready to launch Empaveli, with medical education programs, commercial campaigns, and engagement with payers covering 80% of Medicare Advantage lives forming a three-pronged attack on the GA market.

Perhaps the preparedness is not surprising, given Apellis has seen its GA PDUFA date deadline extended by 3 month – but is the study data strong enough to ensure the FDA approves Empaveli on Feb 26th?

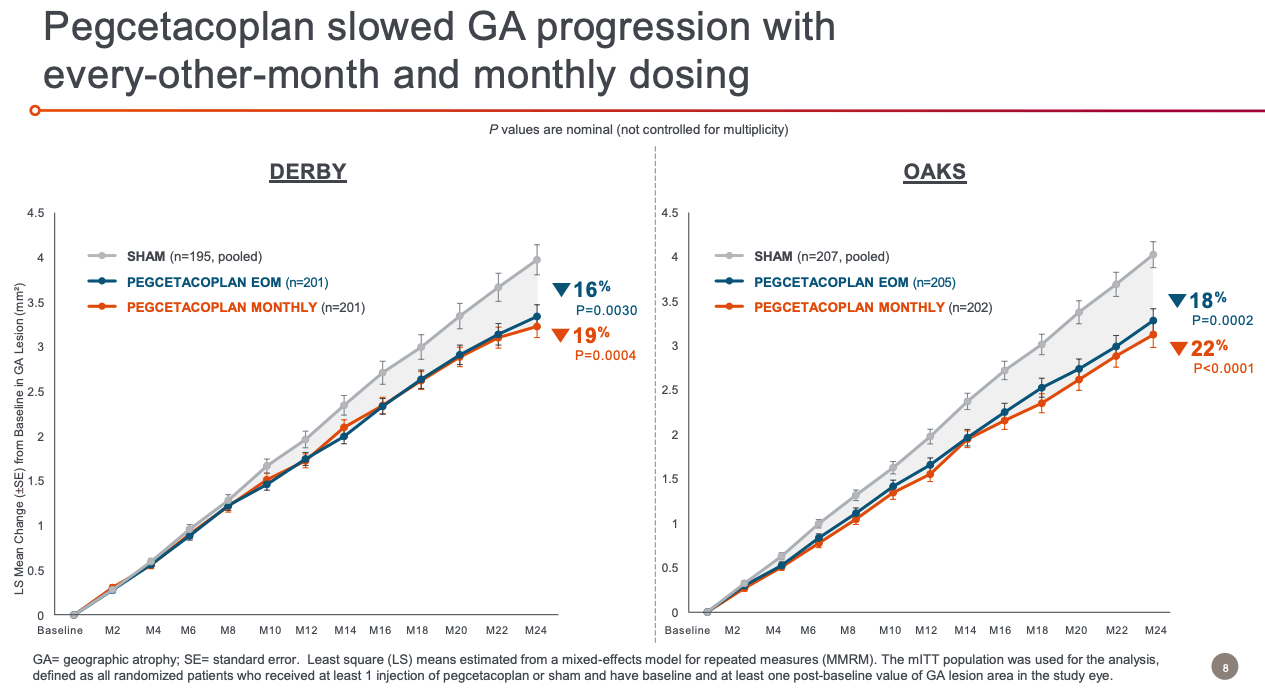

It seems that the DERBY study data has improved over time – after failing to achieve statistical significance at 12 months, after 24 months the data appears to be of the required standard at both dosing regimens, as shown below:

DEBY and OAKS study data at 24 months (Apellis presentation)

The treatment effect is shown to improve over time, and is also effective regardless of lesion location, again using both the once-monthly, and every-other-month dosing regimes.

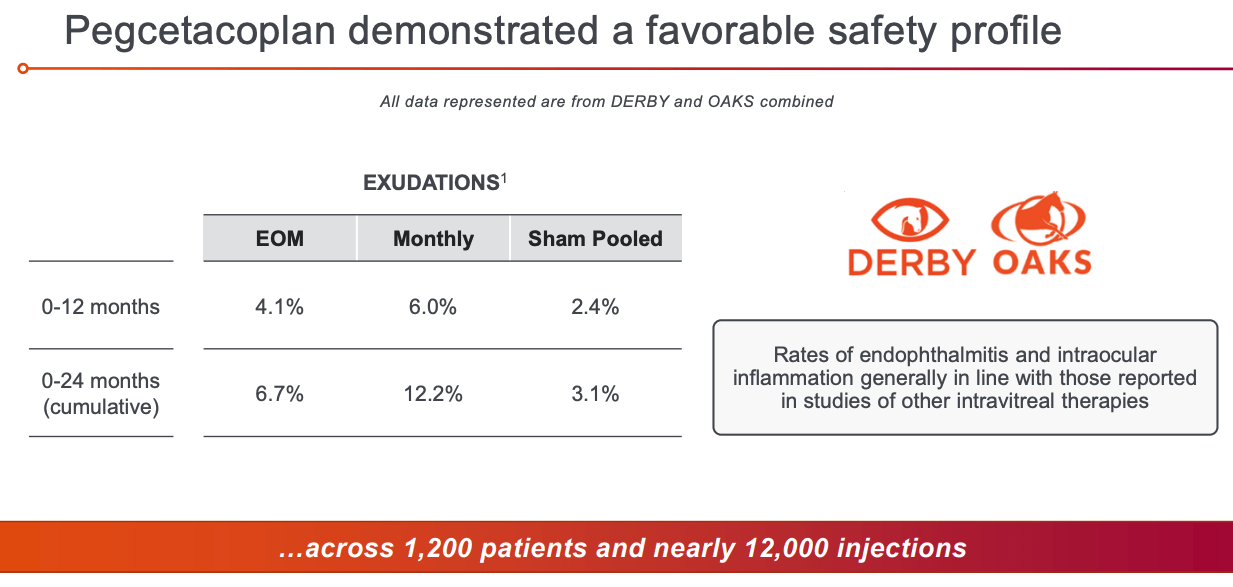

Pegcetacoplan safety profile (Apellis presentation)

The safety profile – as shown above, and also supported by the fact Empaveli is already approved in another indication – looks satisfactory. Management says that there have been no instances of meningococcal infection in >800 patient years of pegcetacoplan exposure, and a thrombosis rate of 1.13 events per 100 patients years.

As such, it’s hard to think of reasons why the FDA would not approve Empaveli next month, giving Apellis a 9-12 months start on its main rival, Iveric. As much as an approval is an almost guaranteed upside catalyst for Apellis shares, however, it appears analysts are yet to be completely convinced by the market opportunity.

In November, the investment bank Jefferies (JEF) downgraded both Apellis and Iveric stock from BUY to HOLD, setting a price target for Apellis of just $40, after conducting its own research into the GA market, via ophthalmologists and retinal surgeons. Jefferies’ analysts stated that:

While wAMD and GA disease prevalence is similar, we learned that Docs see ~1/2 as many GA patients as they do wAMD patients currently

Jefferies concluded that patients may decide that the trouble of receiving regular intravitreal injections outweighs their benefit, and that it does not expect complement inhibitors to have the same effect on the GA market as VEGF inhibitors such as Eylea have had on the Wet AMD market.

I would broadly agree that peak sales expectations for Empaveli – in PNH as well as GA – have been somewhat overblown, particularly looking at 2022 sales to date, but I also believe that the improvement in performance over time is a potentially significant plus point, and also point readers to this article from 2011, suggesting that analysts estimated Eylea would earn $1.1bn in revenues by 2021 – in fact the drug now earns nearly 10x that figure.

So long as reimbursement can be secured, the sheer number of patients with GA ought to result in blockbuster sales, although in PNH Empaveli apparently has a list price of ~$458k, which seems exorbitantly high and could scare away health insurers. A 1-year course of treatment with Eylea costs >$10k. It will be interesting to see the price point chosen for Empaveli in GA.

A final point is that Empaveli is likely to retain its first mover advantage for a short period only. Besides Iveric, according to Evaluate Pharma, Annexon Biopharma (ANNX), Novartis (NVS), Ionis Pharmaceuticals (IONS) / Roche (OTCQX:RHHBY), AstraZeneca (AZN), Stealth Bipharma, Johnson & Johnson (JNJ) and Astellas Biopharma all have GA targeting drug candidates in Phase 1 or 2 studies, whilst Alkeus Pharmaceuticals has a Phase 3 stage assets reading out final data this year.

Interestingly, however, NGM Biopharmaceuticals (NGM) recently reported that its GA indicated C3 complement inhibitor (the same MoA as Empaveli) NGM621 failed to meet endpoints in a Phase 2 study, whilst the Pharma giant Roche has abandoned development of Galegenimab, after failing to prove its worth in the clinic.

That speaks to the tricky nature of designing drugs for GA, and although a new generation of stem cell therapeutics led by a collaboration between Roche and Lineage Cell Therapeutics offers hope of improving vision, based on improvements in best corrected visual acuity, which is beyond the capabilities of Empaveli, my feeling is that all of these biotechs and pharmas would gladly swap places with Apellis.

Looking ahead, Apellis is already planning to try to break into the Wet-AMD / anti-VEGF markets, where it could take on Eylea directly, and is looking at combining pegcetacoplan with small interfering RNA (“sIRNA”) to reduce treatment frequency, with an Investigational New Drug Application to the FDA (to allow in-human studies to begin) in H123.

Conclusion – Apellis Has Developed An Exceptional Drug And Is Well Ahead Of The Competition – The Short and Long Term Share Price Upside Prospects Look Encouraging

To summarize all of the above, having taken an extra 3 months to assess the 24-month DERBY and OAKS Phase 3 study data, I can find few reasons why the FDA would opt against approving Empaveli in GA on February 26th, although it should be stressed that nothing is ever guaranteed when it comes to the drug approval process.

Although analysts seem skeptical about the market opportunity based on a potentially unfavorable convenience vs reward profile, the fact that Emapveli is likely to be the only treatment on the market in GA for at least a year, plus the huge market opportunity based on patient numbers leads me to think that the drug has bona fide blockbuster potential in this indication.

At a conservative estimate of $1.5bn in peak sales across PNH and GA, Apellis’ current market cap of $5.9bn represents ~4x price to forward sales. That may seem high, but when we consider the struggles other companies have faced developing similar drugs, and the future opportunities in fields such as ALS, CAD, and Wet AMD, I don’t think a double-digit billion market cap would not necessarily flatter Apellis.

Astrazeneca paid $13.3bn to acquire Alexion, for example, and Soliris has delivered exceptional sales, but it is possible that Empaveli is the superior drug. I could see a large Pharma paying anything up to $10bn to gain access to Empaveli.

As such, I see a clear upside opportunity arriving at the end of February with the GA PDUFA date, and longer-term the prospects for further share price growth, as revenues begin to climb, look solid also.

Be the first to comment