NoSystem images/E+ via Getty Images

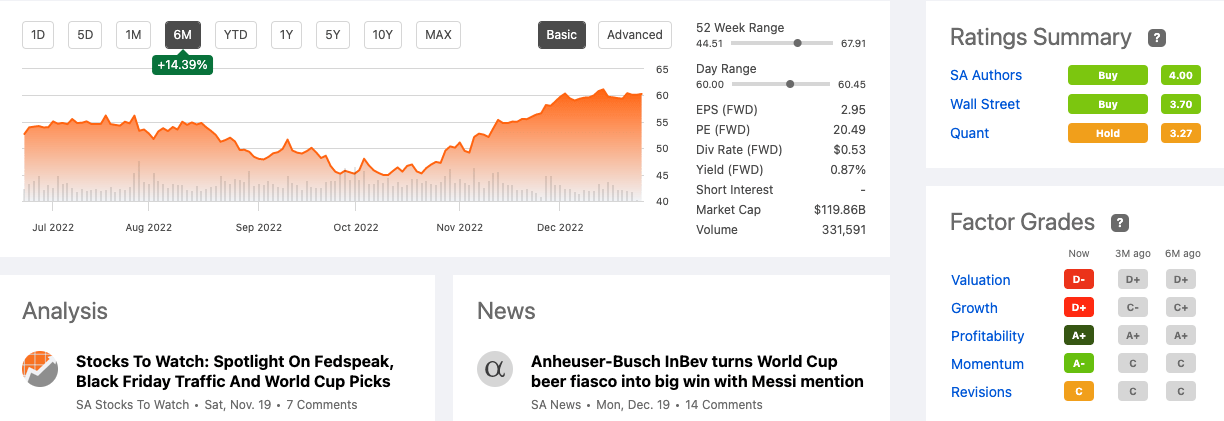

Anheuser-Busch InBev (BUD) has grown from a giant beer organisation to the fourth-largest beverage company in the world, with 500 brands in over 100 countries at a market cap of $119.86 billion. This company is known for big moves, whether in record-breaking acquisitions, or marketing spending for mass events such as the Super Bowl or the World Cup. Through premiumisation, cost-cutting and its beyond-beer strategy, revenues remain high irrespective of the downward beer-drinking trend in the US. Although the stock price has declined by 46.23% in five years, over the last six months, it has rewarded investors with returns of 14.39%.

Stock overview (SeekingAlpha.com)

BUD has been criticised for its high debt intake to accommodate its aggressive growth and brand presence across the globe. However, this powerhouse conglomerate with a global presence has beat earnings expectations in the prior quarter, is showing topline growth in most of its markets and is cutting down on its debt, for example, through divesture in Carlton & United Breweries (CUB). It’s also trading at a much lower value than many of its beverage stock peers. Although cautious of the increased price of beer, changes in consumer drinking habits and more conscious purchasing decisions, there is a lot of upside potential for this stock trading at a much lower value than in pre-COVID-19 years.

Overview

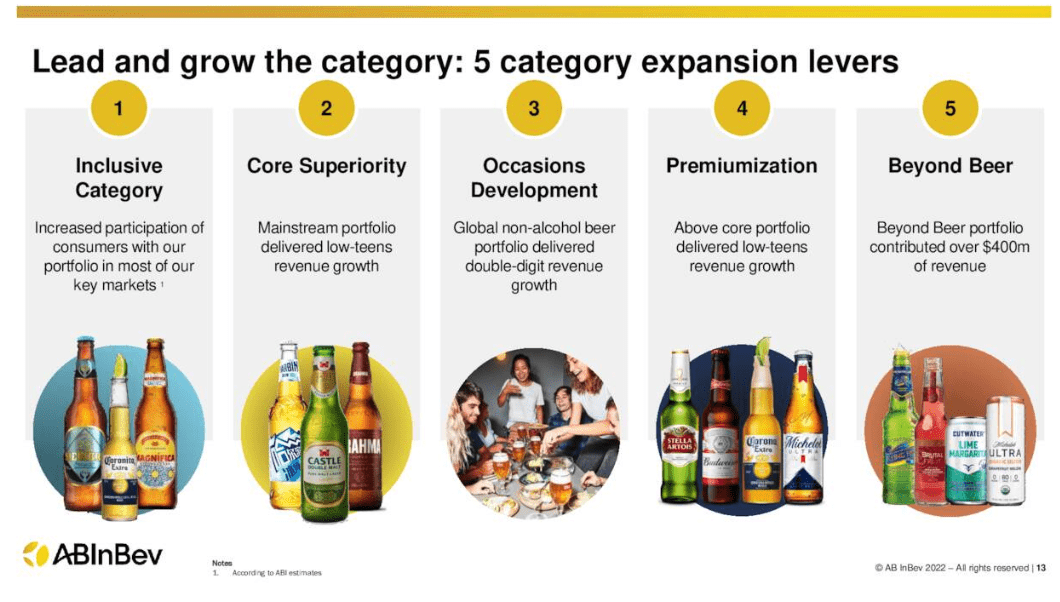

BUD is an international conglomerate, maintaining its dominant position through aggressive takeovers, multi-billion dollar marketing budgets, historically ruthless cost-cutting and expanding into new territories while diversifying its offerings over its long history. As the company grows into alternative beverages, we see it move further away from its original beer heritage. A key strategy for the company within its dominant beer sector has been premiumisation. In 2020 it produced less beer than forty years ago, with 83.8 million barrels, but total sales have increased.

Global Presence (Investor Presentation 2022)

The company has moved to a strategy of premium brands at higher prices and expanding into alternative beverages than just beer. Alcohol-free beer is a growing segment, especially as Gen Z are more interested in non-alcoholic drinks. Non-alcoholic Budweiser came out in 2020. Gen Z is more interested in non-alcoholic beverages.

Beverage Categories (Investor Presentation 2022)

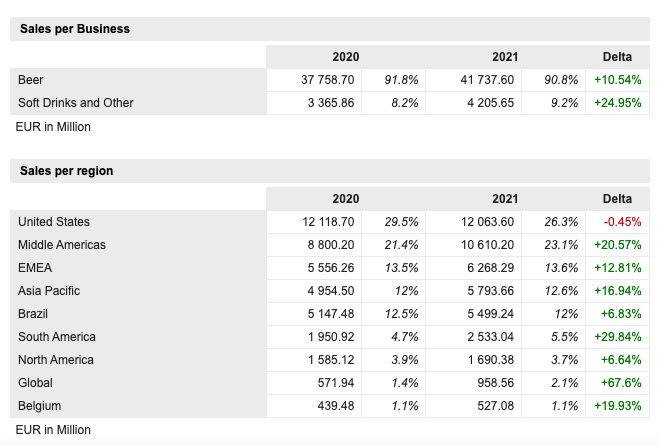

Although the company is most famous for its beer brands, spending billions on sales and advertising. We can see strategic changes in focus in the USA; for one, it has dropped its exclusive advertising rights for the Super Bowl for the first time in 33 years to promote the king of beers, Budweiser and Bud Light. A 30-second advertising spot on TV during this time averaged around $6.5 million. In 2019 it was estimated that the two brands spent $50 million on advertising. Below we see the sales per business and region, with an apparent decline in its largest market. Budweiser’s largest market is China, with a growth of 8.9% this year.

Shifting trends (Marketscreener.com)

Another marketing strategy is to be part of the FIFA World Cup, for which BUD pays $75 million every four years. However, the company’s estimated sales have been hit by a sudden last-minute decision to ban alcohol. A shoutout from World cup winner Lionel Messi and a sponsored campaign to #BringTheBud celebration throughout Argentina could do wonders for the brand. And Bud Zero has received a significant promotion as the only beer the company could sell.

The beer market in the USA is dominated by three dominant players, BUD, Molson Coors (TAP) and Constellation Brands (STZ). As the market size reduces, tenses amongst these players are rising. Brewing is no longer its industry. It falls into the beverage industry. Below we see some of the company’s most significant acquisitions. The SAB Miller deal is in the top five of largest deals ever made, and I believe this hostile and complex deal worthy of a Netflix series left the company with a debt overhang of $106 billion that it is still recovering from today, although things the position is finally on the up.

Acquisitions (Tracxn.com)

Financials

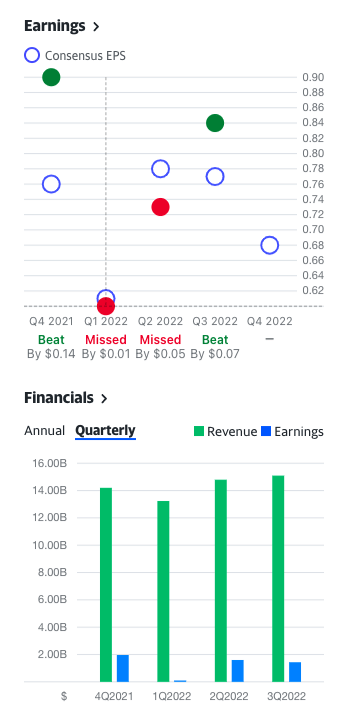

BUD has produced a robust set of Q3 results beating earning expectations for the first time this financial year by $0.07 per share. Furthermore, it has had positive top and bottom-line performance. In 2021 the company produced $53.4 billion in revenue. In Q3 2022, revenue increased by 12.1% year on year.

Financial Overview (Finance.Yahoo.com)

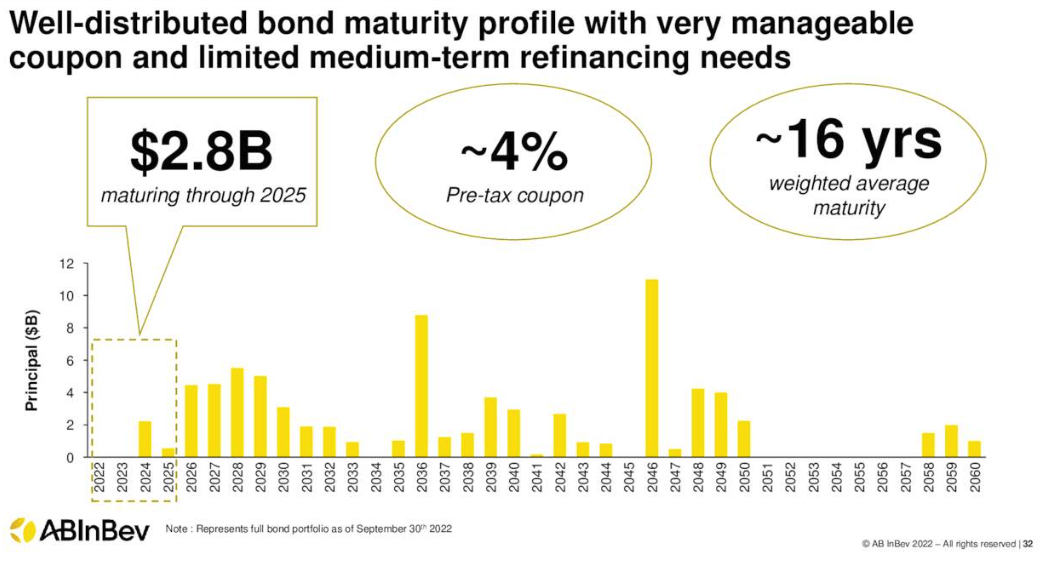

One of the most significant issues with this company today is its debt. However, as we can see below, the company has achievable medium-term refinancing requirements. While interest rate hikes could significantly impact expenses, 94% of BUD’s bonds portfolio is on fixed interest rates.

Bond Portfolio (Investor Presentation 2022)

The company has a dividend program with an annual (forward) dividend of $0.53. However, it could be more compelling to invest in the company as it is low compared to fellow beer peers such as Heineken (OTCQX:HEINY). Furthermore, the dividend has been decreasing since 2017 at a CAGR of 32.96%

Valuation

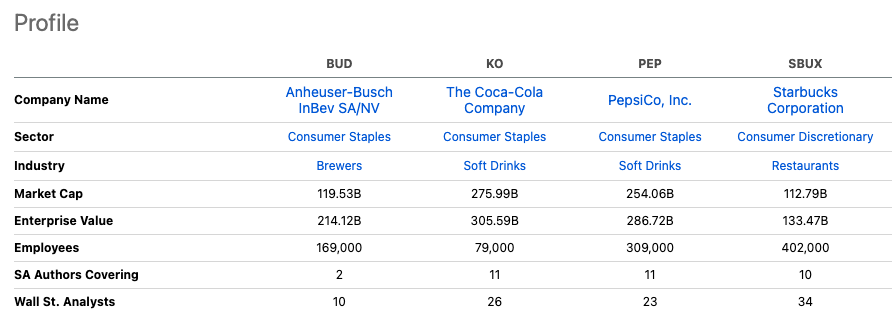

BUD is well perceived by some recognised analysts such as Evercore ISI, which values the importance of the non-alcohol beer market segment as one that is growing in value and will take on an essential role in the future. BUD is rated as Outperform. Furthermore, a Morningstar analyst puts the fair value at $90 and gives a very optimistic view of BUD, especially in holding over the next 20 years. While Credit Suisse recently downgraded the stock to a SELL rating. If we take a look at a peer valuation compared to some of the largest beverage producers.

Beverage Peers (SeekingAlpha.com)

Although BUD has the lowest valuation grade of F. If we look into the numbers, we see that it is the lowest-priced stock, with the lowest price-to-earnings ratio at 20.47 and the price-to-sales ratio at 2.12.

Relative Peer Valuation (SeekingAlpha.com)

Final thoughts

This is a company with serious brand power, market share, and profit margins from economies of scale and a firm hold on global distribution. It went through a majorly aggressive and hostile takeover which is still impacting the company today as it continues to attempt to divest less effective brands, such as in Germany and Australia. As the company starts to get a hold of its debt levels and it is still priced well below many of its beverage company peers. I believe there is still upside potential and therefore recommend taking a bullish stance on this company.

Be the first to comment