adamdodd

Apple (AAPL) for good reason attracts a lot of attention as being Warren Buffett’s top holding in Berkshire Hathaway (BRK.A)(BRK.B). However, let’s not forget that another core holding for him is American Express (NYSE:AXP), which he has held for way longer than Apple.

It’s no wonder that AXP has been a darling for BRK’s portfolio, considering its strong branding, asset light nature, and customer loyalty. In this article, I highlight why AXP is an attractive buy for potentially strong long term returns at current levels, so let’s get started.

Why AXP?

American Express is a global financial institution with presence in 130 countries, providing consumers with business charge and credit card services. Its large network of cardmembers and merchants gives AXP a competitive edge, allowing it to offer a wide range of products and services, including credit cards, charge cards, and travel-related services. The company’s strong brand and reputation for customer service also help to attract and retain cardmembers and merchants.

In recent years, American Express has been focusing on expanding its digital capabilities to better serve its customers and stay competitive in the rapidly evolving payments industry. The company has been investing in mobile and digital technologies, such as mobile payments and digital wallets, and has been expanding its partnerships with other companies to offer new services and reach new markets.

This is exemplified by AXP’s announcement this month of its intent to acquire Nipendo, a platform used by companies to automate and streamline B2B payment processes. AXP expects to be able to achieve an end to end B2B platform with this acquisition, and serve as a launching pad to develop new capabilities for buyers and sellers.

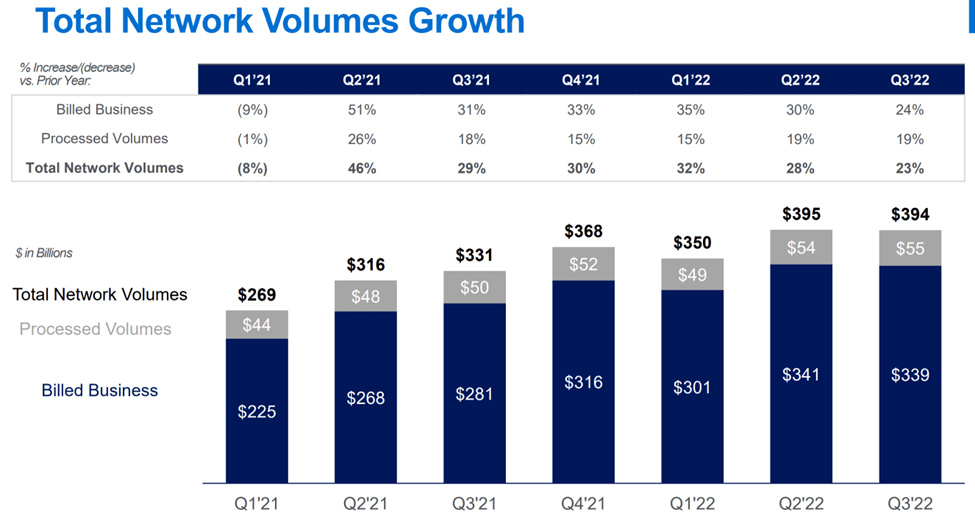

Meanwhile, AXP continues to demonstrate strong growth, with total revenue growing by 27% YoY on a constant currency basis and 3.3 million new proprietary cards added during the third quarter, its highest quarterly level of acquisitions since 2020. It’s also demonstrating positive operating leverage, as pretax pre-provision income grew at a faster pace at 43% growth.

The strong results were driven by strong billed and processed volumes across its network. For reference, billed business represents transaction volumes on payment products issued by AXP, while processed volumes represent transaction volumes on cards from third party merchants that rely on the AXP platform for processing.

AXP Network Volumes (Investor Presentation)

Looking forward, AXP is set to benefit from an easing of travel restrictions in China, which should boost travel spend there. Management also expects to see robust revenue growth this year driven by higher customer spend and engagement, as noted by management during the Q&A session of last month’s Goldman Sachs (GS) Financial Services conference:

Q: To build on some of the things that you touched upon, you talked about the success of the strategy. How does all this translate into better than 10% revenue growth beyond 2023? And then, you touched on a couple of things, maybe dig a little bit deeper on what is giving you the confidence in the strategy?

A: Look, we’ve had six straight quarters of 24% revenue growth, so that will give you a little bit of confidence and we’re staying focused. I think our business is a lot stronger after the pandemic than it was pre-pandemic. I think we learned a lot. We invested a lot in our customers. We’ve changed our model in terms of retention. We’ve changed value propositions. And we stood by our customers. And they’ve rewarded that with higher spending and more engagement.

Near term risks to AXP include uncertainties with the economy. However, there were uncertainties in early 2022 as well, and AXP was able to sail through an inflationary environment virtually unscathed. Moreover, AXP benefits from a well-positioned customer profile, with management noting last month that credit losses and credit profiles are better than they have ever seen in recent memory.

Importantly, AXP carries a strong BBB+ rated balance sheet. While its 1.3% dividend yield is rather low, it’s well-covered by a very low 20% payout ratio and comes with a 5-year dividend CAGR of 9.2%.

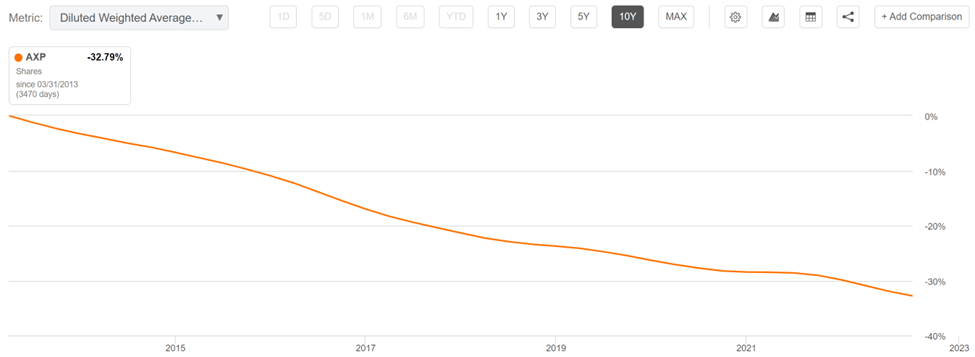

That still may not seem very impressive to income-oriented investors, but AXP stock is more designed for total return investors who do not need immediate income. That’s because it focuses more on share buybacks, which is a more tax efficient manner of capital returns. As shown below, AXP has retired an impressive 33% of its share count over the past decade.

AXP Shares Outstanding (Seeking Alpha)

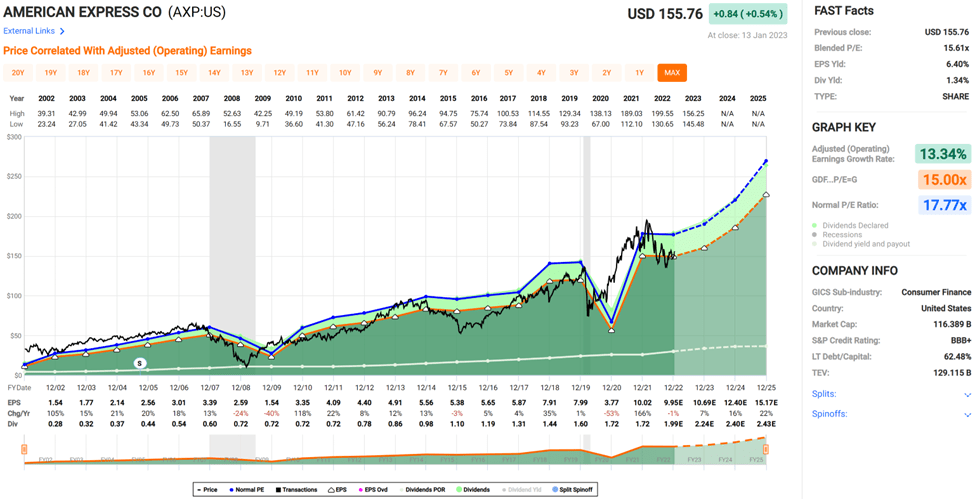

Lastly, I see value in AXP at the current price of $155.76 with a forward P/E of 15.6, sitting below its normal P/E of 17.8. While analysts expect just 5% EPS growth this year, they expect AXP to resume double digit EPS growth in the mid-teens next year and have a $163 price target of AXP’s shares. While long-term investors could wait to buy AXP at a discount, that shouldn’t make too much of a difference for those willing to hold onto it for 5 to 10 years or beyond.

AXP Valuation (FAST Graphs)

Investor Takeaway

American Express is strongly positioned for the future with robust trends in customer engagement, new card additions, and processing volumes. The company benefits from a BBB+ rated balance sheet, low dividend payout, and share repurchases that create value for shareholders. With a reasonably attractive valuation, those focused on potentially strong long-term total returns may want to consider a position at current levels.

Be the first to comment