David Becker/Getty Images News

Last week, chip giant Intel (INTC) had one of the worst earnings reports I can ever remember in the semiconductor space. Not only did the company miss heavily reduced street estimates for Q4, but its guidance for the first quarter of 2023 was significantly below expectations. After the bell on Tuesday, we received competitor Advanced Micro Devices’ (NASDAQ:AMD) fourth quarter report, seen here, which featured results for both bulls and bears.

As a reminder, AMD estimates had come down quite dramatically as well since the company’s warning back in October. Since that time, the average street estimate for Q4 revenue had gone from $7.03 billion to $5.52 billion, or growth of 45.7% to 14.3%. AMD is still facing easier comps in its year ago periods, as the Xilinx acquisition closed in February 2022, otherwise the company would have reported a large decline in its top line. For Q4, AMD came in a little better than the street’s lowered number, with total revenues of just under $5.6 billion. Here are the results from each segment:

- Data Center segment revenue was $1.7 billion, up 42% year-over-year primarily driven by strong sales of EPYC™ server processors.

- Client segment revenue was $903 million, down 51% year-over-year due to reduced processor shipments resulting from a weak PC market and a significant inventory correction across the PC supply chain.

- Gaming segment revenue was $1.6 billion, down 7% year-over-year driven by lower gaming graphics sales partially offset by higher semi-custom product revenue.

- Embedded segment revenue was $1.4 billion, up 1,868% year-over-year primarily driven by the inclusion of Xilinx embedded revenue.

On a GAAP basis, Intel’s margin profile took a huge hit due to the amortization of intangibles acquired in the Xilinx deal. On a non-GAAP basis, gross margins were up 70 basis points over the prior year period, primarily thanks to the higher margin profile of the Xilinx acquisition. Earlier in the year AMD bulls were looking for a lot more margin gains once that deal had closed, but the revenue hits to other segments in the back half of last year has limited that potential upside for now.

Further down the income statement, results tailed off a bit as expected. As I mentioned previously, it’s hard for a business like this to adjust its cost structure in a major way in just a few months when revenues are suddenly dropping. Thus, non-GAAP operating expense growth of 45% was nearly three times the revenue growth rate, leading to a 4 percentage point dip in operating margin. Adjusted net income was down less than 1%, but non-GAAP EPS dropped 25% due to the much higher share count thanks to the Xilinx acquisition being all stock. The 69 cent non-GAAP profit reported beat the street by two cents, but again we are talking about heavily reduced estimates.

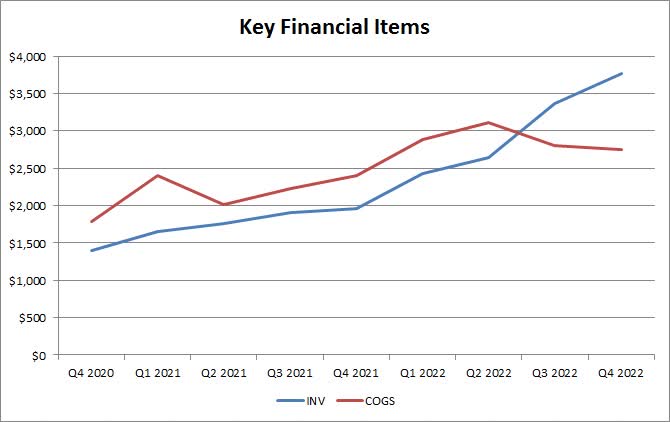

One interesting trend I’ve been watching in the semiconductor space recently has been rising inventories. A year ago, companies were having trouble with enough chip supply, but with revenues under pressure lately, that doesn’t seem to be the case anymore. As the chart below shows, AMD’s quarter ending inventory balance jumped above its most recent quarter’s cost of goods sold (“COGS”) figure in the back half of last year. The inventory to COGS ratio went from 0.78 in Q4 2020 to 0.81 in Q4 2021, but in the quarter just reported, the number had surged to 1.37. While you can’t sell product you don’t have, too much inventory could lead to price cuts and lower margins.

AMD Inventory vs. COGS (Company Filings)

After Intel guided Q1 2023 revenues to be several billion dollars below the street, everyone was curious to see what AMD would say about the quarter. Some of Intel’s problems have been self-inflicted, so expectations were that AMD would provide much better guidance overall. Of course, since the October warning, street estimates had gone from $6.85 billion for Q1 to $5.51 billion, or from growth of 16.3% to a decline of 6.5%. Here’s what AMD management said in the earnings release:

For the first quarter of 2023, AMD expects revenue to be approximately $5.3 billion, plus or minus $300 million, a decrease of approximately 10% year-over-year. Year-over-year the Client and Gaming segments are expected to decline, partially offset by Embedded and Data Center segment growth. AMD expects non-GAAP gross margin to be approximately 50% in the first quarter of 2023.

While the guidance certainly isn’t terrible like Intel’s was, I don’t think it was rather great either. I know AMD supporters will say that it’s not as bad as feared, but don’t forget that this stock has surged from its late 2022 lows. The year over year revenue decline also comes at a time when AMD’s inventory starts 2023 up almost 93% above its 2022 starting point. I did think, however, that the margin guidance was decent, as a $300 million sequential revenue decline could have led to more than a one percentage point decline in non-GAAP gross margins.

When looking at cash flow, AMD’s results weakened a bit. Free cash flow in Q4 was just $443 million, down significantly from $736 million in the year ago period, resulting in the cash flow margin percentage almost being sliced in half to 8%. The company did generate over $3.1 billion in free cash flow for the full year, although that was down a little over $100 million as compared to 2021. Share repurchases also slowed down a bit in Q4, as the company looks to offset the dilution from the Xilinx acquisition.

Going into Tuesday’s report, the average price target on the street was a little under $90 a share, implying decent upside from the stock’s $75.15 closing price. However, as I’ve discussed with many stocks over the past year or two, analysts have had sky high targets that they’ve been constantly cutting. At the end of March last year, for instance, the average AMD price target was still over $150, and it has dropped more than 40% since.

To value AMD, I’m looking at two items. The first is a 10% discount to the average street price target, to reflect the street being too bullish lately, which gets us to about $81 currently. Also, AMD shares were trading at a 20 times adjusted EPS multiple going into Tuesday’s report, and I don’t think the overall report changes anything in a major way. However, AMD has beaten the street a lot in recent years and I liked the margin guidance, so I think $3.70 in non-GAAP EPS is possible this year, or about a dime more than the street. At the 20 times multiple, you get $74, so I think that $74 to $81 range is very fair for AMD. Thus, I wouldn’t be pounding the table to buy here, but I also wouldn’t sell the name unless we get some really hawkish news out of the Fed that sets up the entire market to fall.

In the end, we received a rather mixed report from AMD on Tuesday. Q4 results were slightly better than heavily reduced street estimates, as the Xilinx acquisition certainly saved the quarter from a meaningful revenue decline. While the company’s current quarter guidance wasn’t as bad as what we saw from Intel, revenues were still projected to be less than expectations were calling for. I still believe AMD is set up for a decent future, although it will take a little time to work through these inventory and growth challenges, so the stock seems fairly valued currently as a result.

Be the first to comment