MaxImages/iStock Unreleased via Getty Images

Amazon.com, Inc. (NASDAQ:AMZN) has been navigating a tricky business environment for the past few years. The pandemic led to skyrocketing demand for everything ecommerce but also froze the supply chain. Demand for cloud services also jumped, as businesses were forced to accommodate customers and remote employees while offices and storefronts were closed. This led to great business performance for Amazon in 2020 as the retail and AWS segments benefitted greatly. Revenue increased 37% in the year while operating profit increased 57%. The stock followed suit and rose 75% that year.

This brought Amazon into a massive, multi-year investment cycle so they could meet this newfound demand. Responding to customer needs is a typical Amazon response so these investments made sense at the time, but the situation was anything but typical. No one knew the longer term effects of the pandemic on the global economy, consumer behavior, or remote work. Nonetheless, Amazon dove headfirst into this investment cycle.

Unfortunately for Amazon, demand did normalize to more of a typical trend, and profits subsequently dropped as revenue growth slowed and operating expense growth increased. This brings us to the present and the current opportunity that exists for investors. Is Amazon now structurally less profitable and will profits remain depressed? Or will Amazon reap the rewards of the massive investments it has made over the past two years? I am inclined to believe the latter, and I think Amazon.com, Inc. stock is undervalued because of it. I come to this conclusion by examining the current trends in the financials, and by examining previous investment cycles and their results on Amazon’s profits.

Past Investment Cycles

Amazon is never too clear about its plan for investment cycles. The general answer to analyst questions about investments is something along the lines of “we are investing for long term growth and we’ll continue to do that as we see fit.” Over the past ten years there are two distinct investment cycles that I think are helpful to examine to give investors a better idea of what 2023 holds for Amazon. Those two periods of big investment were in 2014 and 2016-2017.

2014

In 2014, capital expenditures grew 42% over the previous year. Along with this, operating expenses grew 33% from the previous year. These investments were made to support long term growth of the retail segment and AWS. This spending led to a 76% year over year reduction in operating profit for the year.

The year after in 2015, investment slowed as capital expenditure spending declined 6% and growth in operating expenses decelerated to 27%. As a result, operating profit increased 1100%+ that year and the stock price followed as it posted a gain of over 100%. The slowdown in operating expenses was a big contributor to this jump in operating profit, but a jump in gross margin percentage along with sustained revenue growth also played a large role.

2016-2017

Amazon.com, Inc. capital expenditures grew 47% and 49% in 2016 and 2017 respectively. In those same years, operating expenses grew 31% and 42%. Operating profit did increase 87% in 2016 despite this growth in investment spending, but it declined about 2% in 2017.

The same thing that happened in 2015 after the 2014 investment cycle, also happened in 2018. Both capital expenditures and operating expenses grew at a much slower rate than the prior years, all while revenue growth was sustained and gross margin jumped another few percentage points. This led to a 200% increase in operating profit and a 30%+ increase in the stock price in 2018. This isn’t quite as impressive as the 100% increase in the stock price in 2015 but in the context of a 4% decline of the NASDAQ composite index in 2018 it is a very strong relative performance.

Most Recent Cycle

The investment cycle of the past few years is a bit more complex given the situation with the pandemic as it created a very uncertain global economic environment. But at a basic level, the facts of this cycle are the same as the ones in 2014 and 2016-2017.

In 2020, capital expenditures increased a whopping 176% from the prior year and went up another 58% in 2021. Operating expenses also grew 29% and 33% in 2020 and 2021. What’s a bit different from past investment cycles is that operating profit grew quite a bit in both years. This is once again due to a big 37% increase in revenue in 2020 and rising gross margin percentage. The stock followed operating profit and rose 70%+ from the in 2020.

The investment cycle came to an end in 2022 when Amazon management realized their investments led capacity to exceed demand. However we’re not seeing the typical rise in operating profit that comes at the end of these investment cycles. Through the first 9 months of 2022 versus the first 9 months of 2021, capital expenditures grew only 10% and operating expenses grew at a slower albeit still fast rate of 25%. The main issue is that so far in 2022 revenue has only grown 10%. Even though the gross margin percentage has risen, expense growth grew at more than double the rate of revenue growth which has led to a 55% decline in operating profit so far in 2022. The stock is down 50% year to date so it has once again followed operating profit. Obviously, 2022 was a bad year for most stocks, but remember that in 2018 when the NASDAQ index dropped for the year, Amazon’s stock rose 30% because of the increase in operating profit.

This makes the question for 2023 and beyond clear: what will happen to Amazon’s operating profit?

2023 Forecast

Amazon’s operating profit in 2023 will rise if revenue grows, expenses are controlled, and gross margin rises. And if operating profit rises above expectations, the stock price will rise.

Revenue

Revenue growth is facing two main headwinds in 2023. First, if the dollar remains strong versus other currencies there will be FX headwinds. The headwind in 3Q 2022 was 460 basis points. Second, general macroeconomic weakness will damage sales growth on all fronts. Both the strong dollar and the current economic weakness are caused by the actions of the federal reserve so both could potentially be solved by actions of the federal reserve. If inflation dissipates convincingly, Jerome Powell and the fed could pivot. Additionally, the ECB is also getting more hawkish, which will help strengthen the Euro against the Dollar.

The revenue headwinds of 2022 could turn into tailwinds in 2022. Analysts are predicting 11% revenue growth in 2023. Adding back 4.5% to cancel out the FX effects and a few percentage points to account for an improved economy and revenue growth could be 18% in 2023.

Operating Expenses

Wage inflation, especially among tech workers, has added significantly to operating expenses over the past few years. However, with the recent layoffs and hiring freezes from tech companies, these pressures could ease in 2023. Amazon has already shown resolve to reduce operating expenses in loss producing segments. They first announced layoffs of 10,000 employees, many from the Alexa division which was reportedly on pace to lose $10 billion this year, but the number recently upped to 18,000. This is in addition to freezing corporate and AWS hiring into 2023. The commitment to reducing headcount will lead to much lower operating expenses in 2023. The end of past investment cycles have brought upwards of 10% reductions in operating expenses so operating expense growth could decelerate to 20% in 2023.

Gross Margin

Cost of sales go up at Amazon due to “increased product and shipping costs resulting from increased sales, increased investments in our fulfillment network, increased transportation costs, and increased wage rates.” Lower energy and fuel costs, along with a higher portion of total revenue from the higher margin segments, and less hiring and investment for the fulfillment network will help lower gross margin in 2023.

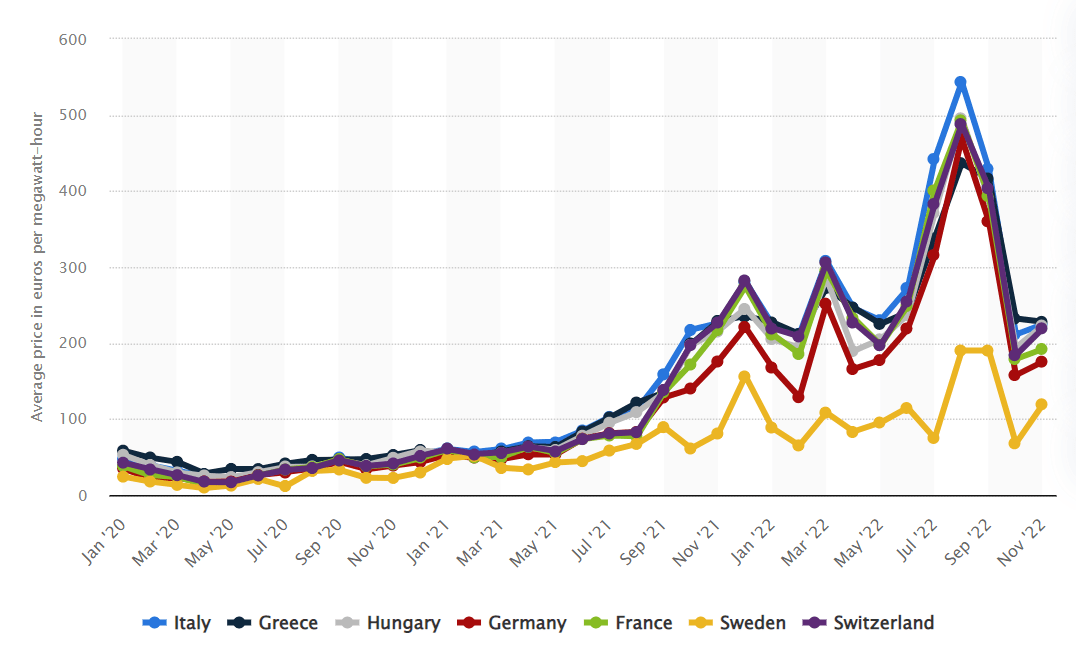

Below is a chart of energy prices in Europe. They have been elevated throughout 2022 and have contributed significantly to cost of goods for AWS.

European Energy Prices (Statista)

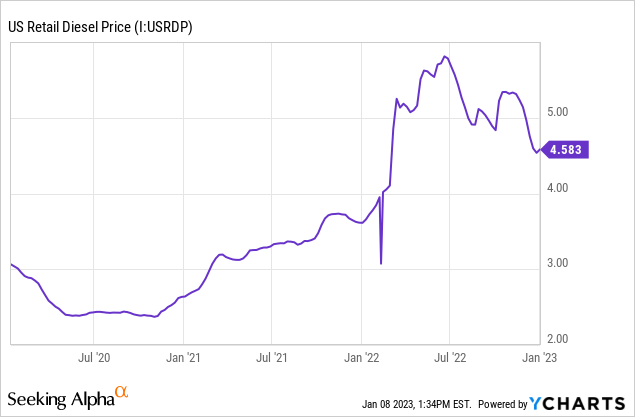

Below is a chart of U.S. diesel prices, which add costs to the retail segment. Like electricity prices in Europe, these prices have been elevated through 2022 and will be a tailwind for gross margin as they continue to drop through 2023.

I could see gross margin increasing by 200 basis points from these cost savings. So far in 2022 gross margin has been 44.3%, so I will forecast gross margin at 46.3% in 2023.

Forecast

Combining my forecasted revenue growth, gross margin and operating expense growth we can arrive at an operating profit forecast for 2023. 18% revenue growth from analyst projections of FY 2022 revenue of $511 billion is $603 billion. Applying a 46.3% gross margin to this revenue figure leads to $285 billion of gross profit. If operating expenses increase 20% from $216 billion (my projection of 2022 operating expenses) 2023 operating expenses would be $259 billion. This would lead to operating profit of $20 billion for 2023.

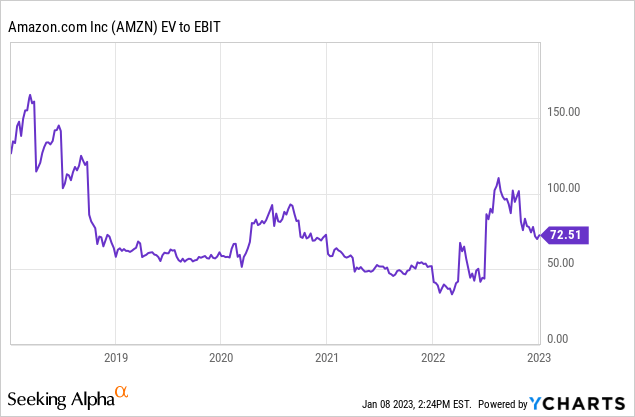

As seen from the chart above, the trough EV/operating profit multiple from the past 5 years is 60, so applying this multiple to $20 billion of operating profit brings us to an enterprise value of $1.2 trillion versus the current enterprise value of $900 billion. This represents 33% upside for the stock. Of course my assumptions are optimistic but I like the risk/reward as I think earnings will continue to rise in the years beyond 2023 as the company slows overall investment and continues to reap the rewards of the pandemic investment cycle.

Risks

The main risks involve the economy and macroeconomic forces. If the U.S. and the world go into a deep recession, revenue won’t grow 18%. Management already mentioned in the 3Q earnings call that AWS customers were very focused on cost cutting. On top of this ad spending would drop significantly.

These factors would hurt revenue growth but could help with reducing costs as fuel, energy prices, and wages would drop. A recession would cause inflation to drop, allowing the federal reserve to pause or cut rates. This could lead the dollar to drop versus other currencies. So while cost cutting could improve in this situation, revenue growth would be less than 18% and gross margin would likely not rise as much due to less growth in ads and AWS, the higher margin segments.

However the stock is already at a trough multiple on operating profit from 2022, a year that Amazon significantly underearned. With cost cutting measures and the drop in energy prices I have a hard time believing that earnings will drop much from 2022. This leads me to believe that potential upside is higher than the downside and the current setup for 2023 and beyond is favorable for Amazon investors.

Final Thoughts

At today’s price, I think Amazon stock offers an attractive risk/reward. It’s currently trading at a trough multiple on trough earnings and management is committed to cutting costs as seen from recent layoffs and hiring freezes. These measures should keep earnings from falling from these current depressed levels even if a global recession hits. It would take major multiple compression from an already depressed multiple, to take the stock down much more from current prices. On the other hand with my optimistic assumptions above, upside could be as high as 33% for the stock in 2023.

Even if the optimistic scenario does not play out, an investment in Amazon can be bailed out with a long term holding period. Management is constantly thinking about long term growth and in my opinion, AWS is one of the best businesses on Earth. This type of management along with these cloud computing tailwinds can only lead to good things for Amazon over time.

Be the first to comment